30.9 Staggered Dif-n-dif

See Wing et al. (2024) checklist.

Recommendations by Baker, Larcker, and Wang (2022)

TWFE DiD regressions are suitable for single treatment periods or when treatment effects are homogeneous, provided there’s a solid rationale for effect homogeneity.

For TWFE staggered DiD, researchers should evaluate bias risks, plot treatment timings to check for variations, and use decompositions like Goodman-Bacon (2021) when possible. If decompositions aren’t feasible (e.g., unbalanced panel), the percentage of never-treated units can indicate bias severity. Expected treatment effect variability should also be discussed.

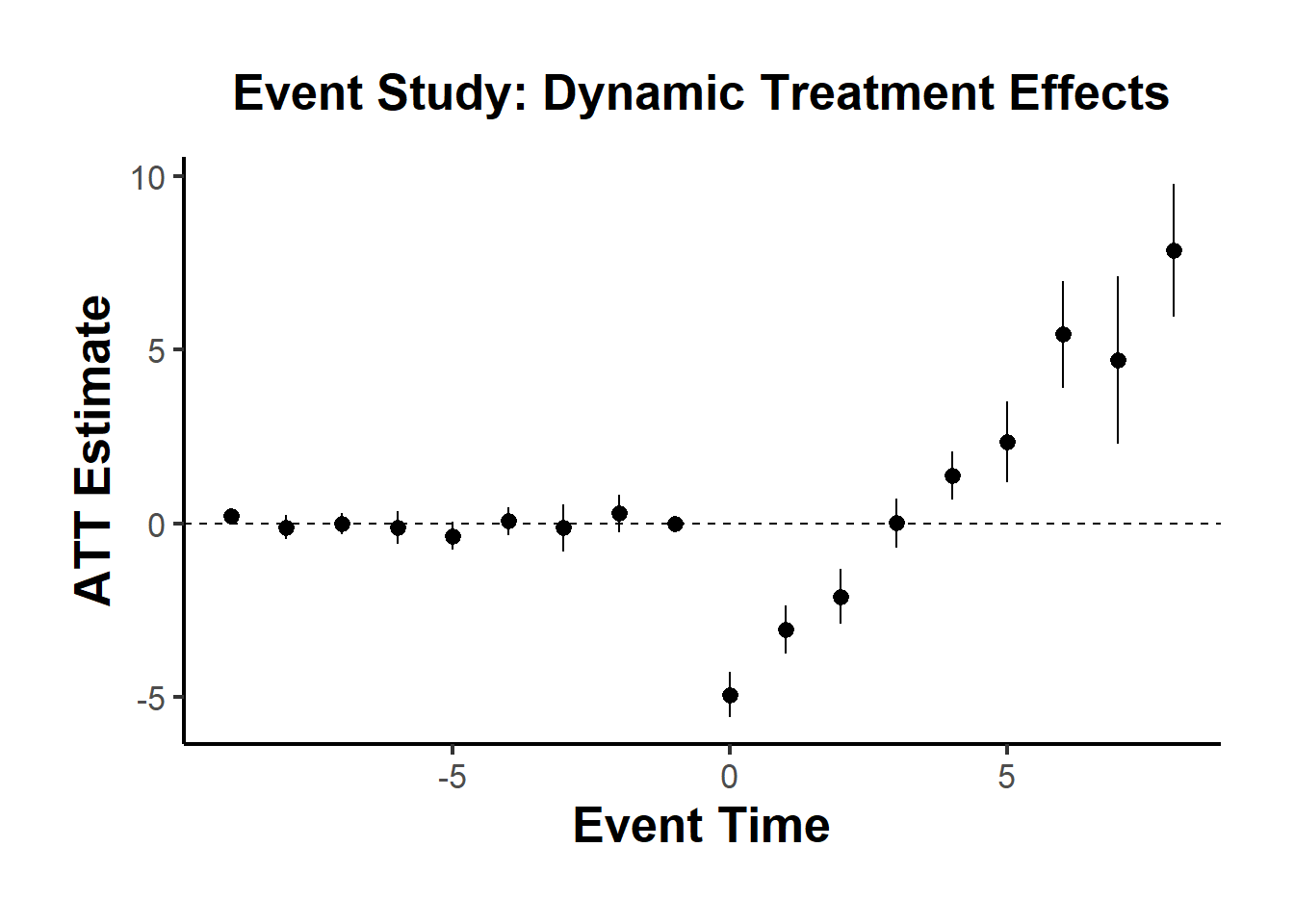

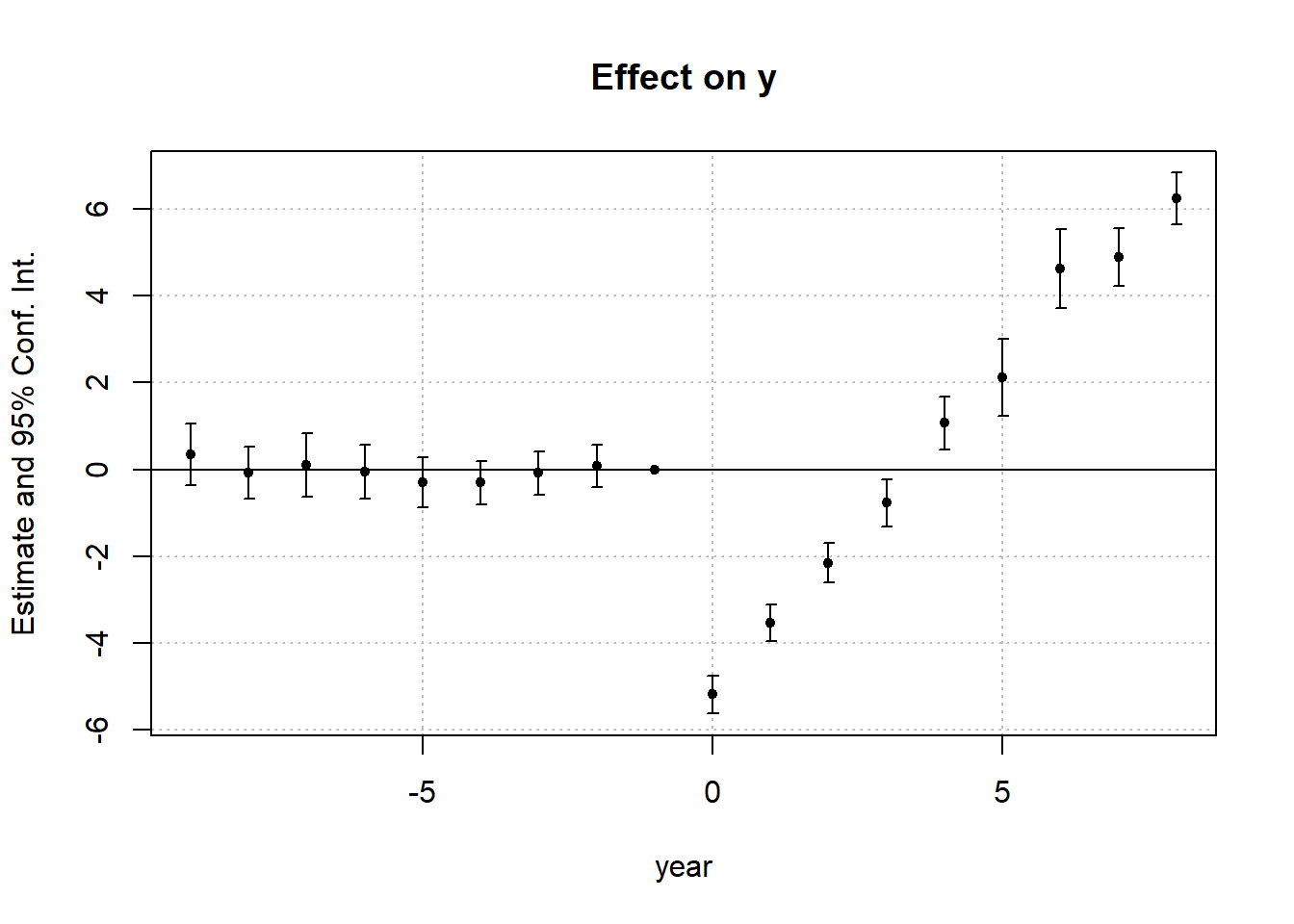

In TWFE staggered DiD event studies, avoid binning time periods without evidence of uniform effects. Use full relative-time indicators, justify reference periods, and be wary of multicollinearity causing bias.

To address treatment timing and bias concerns, use alternative estimators like stacked regressions, L. Sun and Abraham (2021), Callaway and Sant’Anna (2021), or separate regressions for each event with “clean” controls.

Justify the selection of comparison groups (not-yet treated, last treated, never treated) and ensure the parallel-trends assumption holds, especially when anticipating no effects for certain groups.

Notes:

- When subjects are treated at different point in time (variation in treatment timing across units), we have to use staggered DiD (also known as DiD event study or dynamic DiD).

- For design where a treatment is applied and units are exposed to this treatment at all time afterward, see (Athey and Imbens 2022)

For example, basic design (Stevenson and Wolfers 2006)

Yit=∑kβkTreatmentkit+∑iηiStatei+∑tλtYeart+Controlsit+ϵit

where

Treatmentkit is a series of dummy variables equal to 1 if state i is treated k years ago in period t

SE is usually clustered at the group level (occasionally time level).

To avoid collinearity, the period right before treatment is usually chosen to drop.

The more general form of TWFE (L. Sun and Abraham 2021):

First, define the relative period bin indicator as

Dlit=1(t−Ei=l)

where it’s an indicator function of unit i being l periods from its first treatment at time t

- Static specification

Yit=αi+λt+μg∑l≥0Dlit+ϵit

where

αi is the the unit FE

λt is the time FE

μg is the coefficient of interest g=[0,T)

we exclude all periods before first adoption.

- Dynamic specification

Yit=αi+λt+L∑l=−Kl≠−1μlDlit+ϵit

where we have to exclude some relative periods to avoid multicollinearity problem (e.g., either period right before treatment, or the treatment period).

In this setting, we try to show that the treatment and control groups are not statistically different (i.e., the coefficient estimates before treatment are not different from 0) to show pre-treatment parallel trends.

However, this two-way fixed effects design has been criticized by L. Sun and Abraham (2021); Callaway and Sant’Anna (2021); Goodman-Bacon (2021). When researchers include leads and lags of the treatment to see the long-term effects of the treatment, these leads and lags can be biased by effects from other periods, and pre-trends can falsely arise due to treatment effects heterogeneity.

Applying the new proposed method, finance and accounting researchers find that in many cases, the causal estimates turn out to be null (Baker, Larcker, and Wang 2022).

Assumptions of Staggered DID

Rollout Exogeneity (i.e., exogeneity of treatment adoption): if the treatment is randomly implemented over time (i.e., unrelated to variables that could also affect our dependent variables)

- Evidence: Regress adoption on pre-treatment variables. And if you find evidence of correlation, include linear trends interacted with pre-treatment variables (Hoynes and Schanzenbach 2009)

- Evidence: (Deshpande and Li 2019, 223)

- Treatment is random: Regress treatment status at the unit level to all pre-treatment observables. If you have some that are predictive of treatment status, you might have to argue why it’s not a worry. At best, you want this.

- Treatment timing is random: Conditional on treatment, regress timing of the treatment on pre-treatment observables. At least, you want this.

No confounding events

Exclusion restrictions

No-anticipation assumption: future treatment time do not affect current outcomes

Invariance-to-history assumption: the time a unit under treatment does not affect the outcome (i.e., the time exposed does not matter, just whether exposed or not). This presents causal effect of early or late adoption on the outcome.

And all the assumptions in listed in the Multiple periods and variation in treatment timing

Auxiliary assumptions:

Constant treatment effects across units

Constant treatment effect over time

Random sampling

Effect Additivity

Remedies for staggered DiD (Baker, Larcker, and Wang 2022):

Each treated cohort is compared to appropriate controls (not-yet-treated, never-treated)

(Callaway and Sant’Anna 2021) consistent for average ATT. more complicated but also more flexible than (L. Sun and Abraham 2021)

- (L. Sun and Abraham 2021) (a special case of (Callaway and Sant’Anna 2021))

Stacked DID (biased but simple):

30.9.1 Stacked DID

Notations following these slides

Yit=βFEDit+Ai+Bt+ϵit

where

Ai is the group fixed effects

Bt is the period fixed effects

Steps

- Choose Event Window

- Enumerate Sub-experiments

- Define Inclusion Criteria

- Stack Data

- Specify Estimating Equation

Event Window

Let

κa be the length of the pre-event window

κb be the length of the post-event window

By setting a common event window for the analysis, we essentially exclude all those events that do not meet this criteria.

Sub-experiments

Let T1 be the earliest period in the dataset

TT be the last period in the dataset

Then, the collection of all policy adoption periods that are under our event window is

ΩA={Ai|T1+κa≤Ai≤TT−κb}

where these events exist

at least κa periods after the earliest period

at least κb periods before the last period

Let d=1,…,D be the index column of the sub-experiments in ΩA

and ωd be the event date of the d-th sub-experiment (e.g., ω1 = adoption date of the 1st experiment)

Inclusion Criteria

- Valid treated Units

Within sub-experiment d, all treated units have the same adoption date

This makes sure a unit can only serve as a treated unit in only 1 sub-experiment

- Clean controls

Only units satisfying Ai>ωd+κb are included as controls in sub-experiment d

This ensures controls are only

never treated units

units that are treated in far future

But a unit can be control unit in multiple sub-experiments (need to correct SE)

- Valid Time Periods

All observations within sub-experiment d are from time periods within the sub-experiment’s event window

This ensures in sub-experiment d, only observations satisfying ωd−κa≤t≤ωd+κb are included

library(did)

library(tidyverse)

library(fixest)

data(base_stagg)

# first make the stacked datasets

# get the treatment cohorts

cohorts <- base_stagg %>%

select(year_treated) %>%

# exclude never-treated group

filter(year_treated != 10000) %>%

unique() %>%

pull()

# make formula to create the sub-datasets

getdata <- function(j, window) {

#keep what we need

base_stagg %>%

# keep treated units and all units not treated within -5 to 5

# keep treated units and all units not treated within -window to window

filter(year_treated == j | year_treated > j + window) %>%

# keep just year -window to window

filter(year >= j - window & year <= j + window) %>%

# create an indicator for the dataset

mutate(df = j)

}

# get data stacked

stacked_data <- map_df(cohorts, ~ getdata(., window = 5)) %>%

mutate(rel_year = if_else(df == year_treated, time_to_treatment, NA_real_)) %>%

fastDummies::dummy_cols("rel_year", ignore_na = TRUE) %>%

mutate(across(starts_with("rel_year_"), ~ replace_na(., 0)))

# get stacked value

stacked <-

feols(

y ~ `rel_year_-5` + `rel_year_-4` + `rel_year_-3` +

`rel_year_-2` + rel_year_0 + rel_year_1 + rel_year_2 + rel_year_3 +

rel_year_4 + rel_year_5 |

id ^ df + year ^ df,

data = stacked_data

)$coefficients

stacked_se = feols(

y ~ `rel_year_-5` + `rel_year_-4` + `rel_year_-3` +

`rel_year_-2` + rel_year_0 + rel_year_1 + rel_year_2 + rel_year_3 +

rel_year_4 + rel_year_5 |

id ^ df + year ^ df,

data = stacked_data

)$se

# add in 0 for omitted -1

stacked <- c(stacked[1:4], 0, stacked[5:10])

stacked_se <- c(stacked_se[1:4], 0, stacked_se[5:10])

cs_out <- att_gt(

yname = "y",

data = base_stagg,

gname = "year_treated",

idname = "id",

# xformla = "~x1",

tname = "year"

)

cs <-

aggte(

cs_out,

type = "dynamic",

min_e = -5,

max_e = 5,

bstrap = FALSE,

cband = FALSE

)

res_sa20 = feols(y ~ sunab(year_treated, year) |

id + year, base_stagg)

sa = tidy(res_sa20)[5:14, ] %>% pull(estimate)

sa = c(sa[1:4], 0, sa[5:10])

sa_se = tidy(res_sa20)[6:15, ] %>% pull(std.error)

sa_se = c(sa_se[1:4], 0, sa_se[5:10])

compare_df_est = data.frame(

period = -5:5,

cs = cs$att.egt,

sa = sa,

stacked = stacked

)

compare_df_se = data.frame(

period = -5:5,

cs = cs$se.egt,

sa = sa_se,

stacked = stacked_se

)

compare_df_longer <- compare_df_est %>%

pivot_longer(!period, names_to = "estimator", values_to = "est") %>%

full_join(compare_df_se %>%

pivot_longer(!period, names_to = "estimator", values_to = "se")) %>%

mutate(upper = est + 1.96 * se,

lower = est - 1.96 * se)

ggplot(compare_df_longer) +

geom_ribbon(aes(

x = period,

ymin = lower,

ymax = upper,

group = estimator

)) +

geom_line(aes(

x = period,

y = est,

group = estimator,

col = estimator

),

linewidth = 1) +

causalverse::ama_theme()

Stack Data

Estimating Equation

Yitd=β0+β1Tid+β2Ptd+β3(Tid×Ptd)+ϵitd

where

Tid = 1 if unit i is treated in sub-experiment d, 0 if control

Ptd = 1 if it’s the period after the treatment in sub-experiment d

Equivalently,

Yitd=β3(Tid×Ptd)+θid+γtd+ϵitd

β3 averages all the time-varying effects into a single number (can’t see the time-varying effects)

Stacked Event Study

Let YSEtd=t−ωd be the “time since event” variable in sub-experiment d

Then, YSEtd=−κa,…,0,…,κb in every sub-experiment

In each sub-experiment, we can fit

Ydit=κb∑j=−κaβdj×1(TSEtd=j)+κb∑m=−κaδdj(Tid×1(TSEtd=j))+θdi+ϵdit

- Different set of event study coefficients in each sub-experiment

Yitd=κb∑j=−κaβj×1(TSEtd=j)+κb∑m=−κaδj(Tid×1(TSEtd=j))+θid+ϵitd

Clustering

Clustered at the unit x sub-experiment level (Cengiz et al. 2019)

Clustered at the unit level (Deshpande and Li 2019)

30.9.2 Goodman-Bacon Decomposition

Paper: (Goodman-Bacon 2021)

For an excellent explanation slides by the author, see

Takeaways:

A pairwise DID (τ) gets more weight if the change is close to the middle of the study window

A pairwise DID (τ) gets more weight if it includes more observations.

Code from bacondecomp vignette

library(bacondecomp)

library(tidyverse)

data("castle")

castle <- bacondecomp::castle %>%

dplyr::select("l_homicide", "post", "state", "year")

head(castle)

#> l_homicide post state year

#> 1 2.027356 0 Alabama 2000

#> 2 2.164867 0 Alabama 2001

#> 3 1.936334 0 Alabama 2002

#> 4 1.919567 0 Alabama 2003

#> 5 1.749841 0 Alabama 2004

#> 6 2.130440 0 Alabama 2005

df_bacon <- bacon(

l_homicide ~ post,

data = castle,

id_var = "state",

time_var = "year"

)

#> type weight avg_est

#> 1 Earlier vs Later Treated 0.05976 -0.00554

#> 2 Later vs Earlier Treated 0.03190 0.07032

#> 3 Treated vs Untreated 0.90834 0.08796

# weighted average of the decomposition

sum(df_bacon$estimate * df_bacon$weight)

#> [1] 0.08181162Two-way Fixed effect estimate

library(broom)

fit_tw <- lm(l_homicide ~ post + factor(state) + factor(year),

data = bacondecomp::castle)

head(tidy(fit_tw))

#> # A tibble: 6 × 5

#> term estimate std.error statistic p.value

#> <chr> <dbl> <dbl> <dbl> <dbl>

#> 1 (Intercept) 1.95 0.0624 31.2 2.84e-118

#> 2 post 0.0818 0.0317 2.58 1.02e- 2

#> 3 factor(state)Alaska -0.373 0.0797 -4.68 3.77e- 6

#> 4 factor(state)Arizona 0.0158 0.0797 0.198 8.43e- 1

#> 5 factor(state)Arkansas -0.118 0.0810 -1.46 1.44e- 1

#> 6 factor(state)California -0.108 0.0810 -1.34 1.82e- 1Hence, naive TWFE fixed effect equals the weighted average of the Bacon decomposition (= 0.08).

library(ggplot2)

ggplot(df_bacon) +

aes(

x = weight,

y = estimate,

# shape = factor(type),

color = type

) +

labs(x = "Weight", y = "Estimate", shape = "Type") +

geom_point() +

causalverse::ama_theme()

With time-varying controls that can identify variation within-treatment timing group, the”early vs. late” and “late vs. early” estimates collapse to just one estimate (i.e., both treated).

30.9.3 DID with in and out treatment condition

30.9.3.1 Panel Match

As noted in (Imai and Kim 2021), the TWFE estimator is not a fully nonparametric approach and is sensitive to incorrect model specifications (i.e., model dependence).

- To mitigate model dependence, they propose matching methods for panel data.

- Implementations are available via the

wfe(Weighted Fixed Effects) andPanelMatchR packages.

Imai and Kim (2021)

This case generalizes the staggered adoption setting, allowing units to vary in treatment over time. For N units across T time periods (with potentially unbalanced panels), let Xit represent treatment and Yit the outcome for unit i at time t. We use the two-way linear fixed effects model:

Yit=αi+γt+βXit+ϵit

for i=1,…,N and t=1,…,T. Here, αi and γt are unit and time fixed effects. They capture time-invariant unit-specific and unit-invariant time-specific unobserved confounders, respectively. We can express these as αi=h(Ui) and γt=f(Vt), with Ui and Vt being the confounders. The model doesn’t assume a specific form for h(.) and f(.), but that they’re additive and separable given binary treatment.

The least squares estimate of β leverages the covariance in outcome and treatment (Imai and Kim 2021, 406). Specifically, it uses the within-unit and within-time variations. Many researchers prefer the two fixed effects (2FE) estimator because it adjusts for both types of unobserved confounders without specific functional-form assumptions, but this is wrong (Imai and Kim 2019). We do need functional-form assumption (i.e., linearity assumption) for the 2FE to work (Imai and Kim 2021, 406)

Two-Way Matching Estimator:

It can lead to mismatches; units with the same treatment status get matched when estimating counterfactual outcomes.

Observations need to be matched with opposite treatment status for correct causal effects estimation.

Mismatches can cause attenuation bias.

The 2FE estimator adjusts for this bias using the factor K, which represents the net proportion of proper matches between observations with opposite treatment status.

Weighting in 2FE:

Observation (i,t) is weighted based on how often it acts as a control unit.

The weighted 2FE estimator still has mismatches, but fewer than the standard 2FE estimator.

Adjustments are made based on observations that neither belong to the same unit nor the same time period as the matched observation.

This means there are challenges in adjusting for unit-specific and time-specific unobserved confounders under the two-way fixed effect framework.

Equivalence & Assumptions:

Equivalence between the 2FE estimator and the DID estimator is dependent on the linearity assumption.

The multi-period DiD estimator is described as an average of two-time-period, two-group DiD estimators applied during changes from control to treatment.

Comparison with DiD:

In simple settings (two time periods, treatment given to one group in the second period), the standard nonparametric DiD estimator equals the 2FE estimator.

This doesn’t hold in multi-period DiD designs where units change treatment status multiple times at different intervals.

Contrary to popular belief, the unweighted 2FE estimator isn’t generally equivalent to the multi-period DiD estimator.

While the multi-period DiD can be equivalent to the weighted 2FE, some control observations may have negative regression weights.

Conclusion:

- Justifying the 2FE estimator as the DID estimator isn’t warranted without imposing the linearity assumption.

Application (Imai, Kim, and Wang 2021)

Matching Methods:

Enhance the validity of causal inference.

Reduce model dependence and provide intuitive diagnostics (Ho et al. 2007)

Rarely utilized in analyzing time series cross-sectional data.

The proposed matching estimators are more robust than the standard two-way fixed effects estimator, which can be biased if mis-specified

Better than synthetic controls (e.g., (Xu 2017)) because it needs less data to achieve good performance and and adapt the the context of unit switching treatment status multiple times.

Notes:

- Potential carryover effects (treatment may have a long-term effect), leading to post-treatment bias.

Proposed Approach:

Treated observations are matched with control observations from other units in the same time period with the same treatment history up to a specified number of lags.

Standard matching and weighting techniques are employed to further refine the matched set.

Apply a DiD estimator to adjust for time trend.

The goal is to have treated and matched control observations with similar covariate values.

Assessment:

- The quality of matches is evaluated through covariate balancing.

Estimation:

- Both short-term and long-term average treatment effects on the treated (ATT) are estimated.

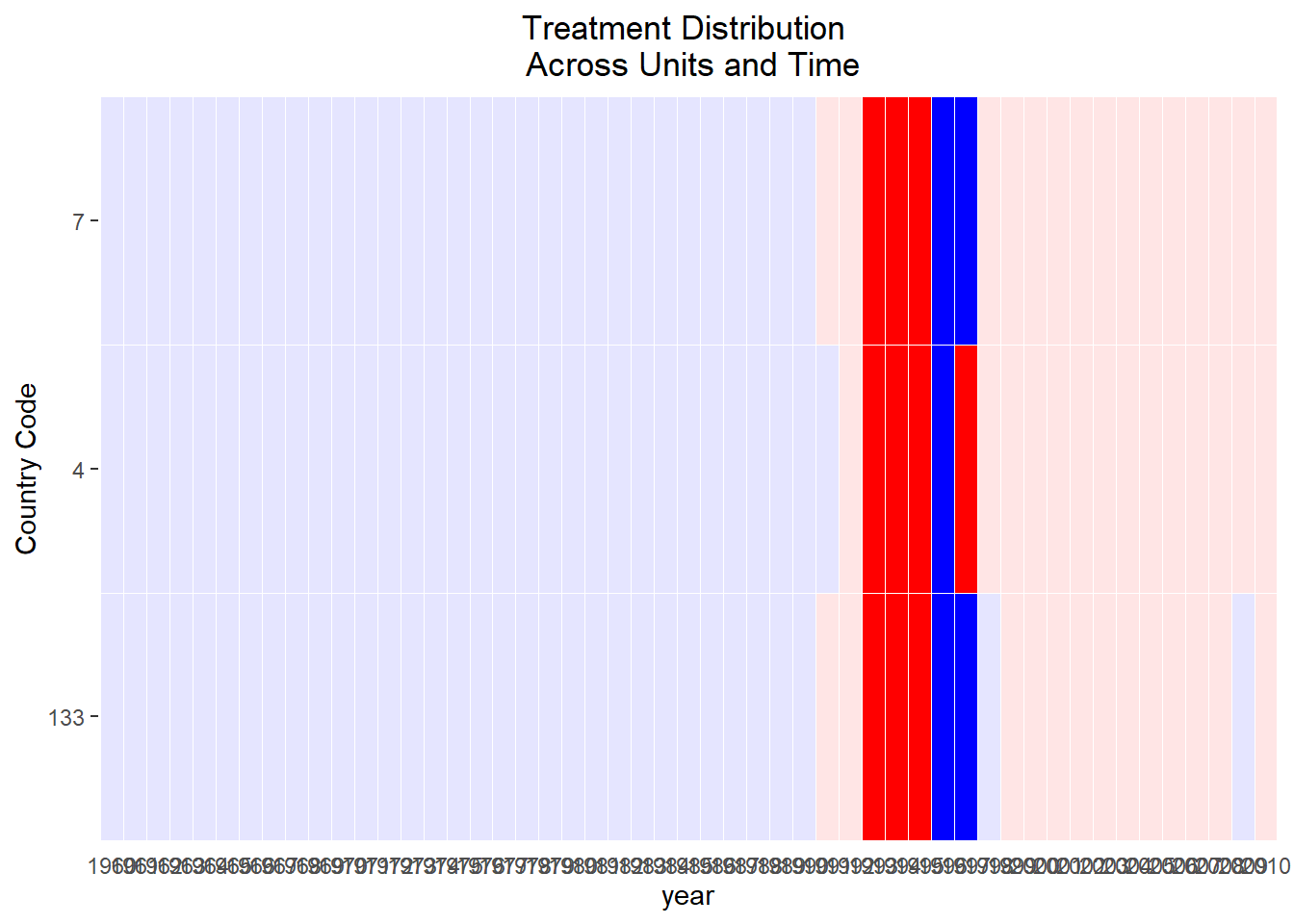

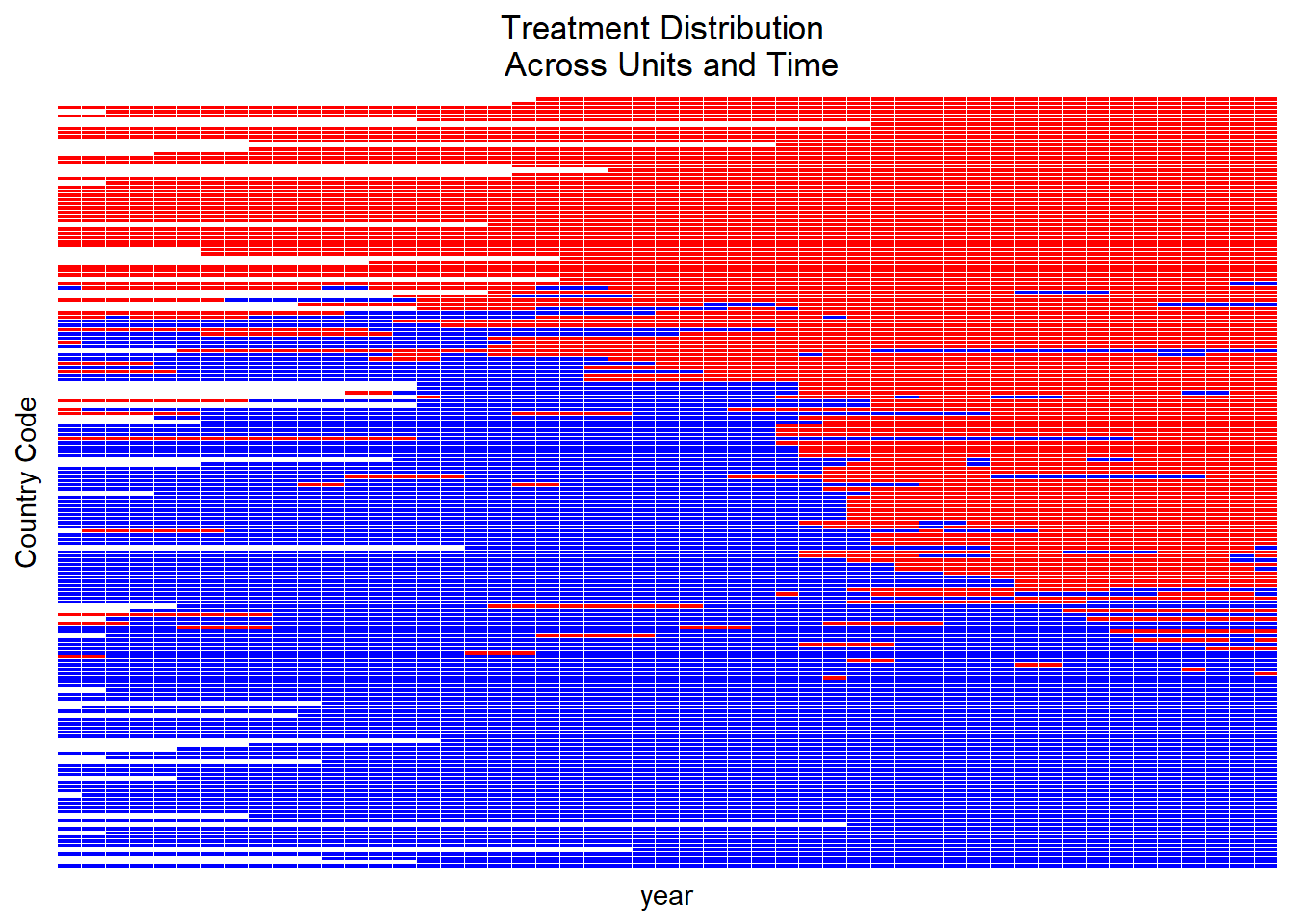

Treatment Variation plot

Visualize the variation of the treatment across space and time

Aids in discerning whether the treatment fluctuates adequately over time and units or if the variation is primarily clustered in a subset of data.

DisplayTreatment(

unit.id = "wbcode2",

time.id = "year",

legend.position = "none",

xlab = "year",

ylab = "Country Code",

treatment = "dem",

hide.x.tick.label = TRUE, hide.y.tick.label = TRUE,

# dense.plot = TRUE,

data = dem

)

- Select F (i.e., the number of leads - time periods after treatment). Driven by what authors are interested in estimating:

F=0 is the contemporaneous effect (short-term effect)

F=n is the the treatment effect on the outcome two time periods after the treatment. (cumulative or long-term effect)

- Select L (number of lags to adjust).

Driven by the identification assumption.

Balances bias-variance tradeoff.

Higher L values increase credibility but reduce efficiency by limiting potential matches.

Model assumption:

No spillover effect assumed.

Carryover effect allowed up to L periods.

Potential outcome for a unit depends neither on others’ treatment status nor on its past treatment after L periods.

After defining causal quantity with parameters L and F.

- Focus on the average treatment effect of treatment status change.

- δ(F,L) is the average causal effect of treatment change (ATT), F periods post-treatment, considering treatment history up to L periods.

- Causal quantity considers potential future treatment reversals, meaning treatment could revert to control before outcome measurement.

Also possible to estimate the average treatment effect of treatment reversal on the reversed (ART).

Choose L,F based on specific needs.

A large L value:

Increases the credibility of the limited carryover effect assumption.

Allows more past treatments (up to t−L) to influence the outcome Yi,t+F.

Might reduce the number of matches and lead to less precise estimates.

Selecting an appropriate number of lags

Researchers should base this choice on substantive knowledge.

Sensitivity of empirical results to this choice should be examined.

The choice of F should be:

Substantively motivated.

Decides whether the interest lies in short-term or long-term causal effects.

A large F value can complicate causal effect interpretation, especially if many units switch treatment status during the F lead time period.

Identification Assumption

Parallel trend assumption conditioned on treatment, outcome (excluding immediate lag), and covariate histories.

Doesn’t require strong unconfoundedness assumption.

Cannot account for unobserved time-varying confounders.

Essential to examine outcome time trends.

- Check if they’re parallel between treated and matched control units using pre-treatment data

Constructing the Matched Sets:

For each treated observation, create matched control units with identical treatment history from t−L to t−1.

Matching based on treatment history helps control for carryover effects.

Past treatments often act as major confounders, but this method can correct for it.

Exact matching on time period adjusts for time-specific unobserved confounders.

Unlike staggered adoption methods, units can change treatment status multiple times.

Matched set allows treatment switching in and out of treatment

Refining the Matched Sets:

Initially, matched sets adjust only for treatment history.

Parallel trend assumption requires adjustments for other confounders like past outcomes and covariates.

Matching methods:

Match each treated observation with up to J control units.

Distance measures like Mahalanobis distance or propensity score can be used.

Match based on estimated propensity score, considering pretreatment covariates.

Refined matched set selects most similar control units based on observed confounders.

Weighting methods:

Assign weight to each control unit in a matched set.

Weights prioritize more similar units.

Inverse propensity score weighting method can be applied.

Weighting is a more generalized method than matching.

The Difference-in-Differences Estimator:

Using refined matched sets, the ATT (Average Treatment Effect on the Treated) of policy change is estimated.

For each treated observation, estimate the counterfactual outcome using the weighted average of control units in the refined set.

The DiD estimate of the ATT is computed for each treated observation, then averaged across all such observations.

For noncontemporaneous treatment effects where F>0:

The ATT doesn’t specify future treatment sequence.

Matched control units might have units receiving treatment between time t and t+F.

Some treated units could return to control conditions between these times.

Checking Covariate Balance:

The proposed methodology offers the advantage of checking covariate balance between treated and matched control observations.

This check helps to see if treated and matched control observations are comparable with respect to observed confounders.

Once matched sets are refined, covariate balance examination becomes straightforward.

Examine the mean difference of each covariate between a treated observation and its matched controls for each pretreatment time period.

Standardize this difference using the standard deviation of each covariate across all treated observations in the dataset.

Aggregate this covariate balance measure across all treated observations for each covariate and pretreatment time period.

Examine balance for lagged outcome variables over multiple pretreatment periods and time-varying covariates.

- This helps evaluate the validity of the parallel trend assumption underlying the proposed DiD estimator.

Relations with Linear Fixed Effects Regression Estimators:

The standard DiD estimator is equivalent to the linear two-way fixed effects regression estimator when:

Only two time periods exist.

Treatment is given to some units exclusively in the second period.

This equivalence doesn’t extend to multiperiod DiD designs, where:

More than two time periods are considered.

Units might receive treatment multiple times.

Despite this, many researchers relate the use of the two-way fixed effects estimator to the DiD design.

Standard Error Calculation:

Approach:

Condition on the weights implied by the matching process.

These weights denote how often an observation is utilized in matching (G. W. Imbens and Rubin 2015)

Context:

Analogous to the conditional variance seen in regression models.

Resulting standard errors don’t factor in uncertainties around the matching procedure.

They can be viewed as a measure of uncertainty conditional upon the matching process (Ho et al. 2007).

Key Findings:

Even in conditions favoring OLS, the proposed matching estimator displayed higher robustness to omitted relevant lags than the linear regression model with fixed effects.

The robustness offered by matching came at a cost - reduced statistical power.

This emphasizes the classic statistical tradeoff between bias (where matching has an advantage) and variance (where regression models might be more efficient).

Data Requirements

The treatment variable is binary:

0 signifies “assignment” to control.

1 signifies assignment to treatment.

Variables identifying units in the data must be: Numeric or integer.

Variables identifying time periods should be: Consecutive numeric/integer data.

Data format requirement: Must be provided as a standard

data.frameobject.

Basic functions:

Utilize treatment histories to create matching sets of treated and control units.

Refine these matched sets by determining weights for each control unit in the set.

- Units with higher weights have a larger influence during estimations.

Matching on Treatment History:

Goal is to match units transitioning from untreated to treated status with control units that have similar past treatment histories.

Setting the Quantity of Interest (

qoi =)attaverage treatment effect on treated unitsatcaverage treatment effect of treatment on the control unitsartaverage effect of treatment reversal for units that experience treatment reversalateaverage treatment effect

library(PanelMatch)

# All examples follow the package's vignette

# Create the matched sets

PM.results.none <-

PanelMatch(

lag = 4,

time.id = "year",

unit.id = "wbcode2",

treatment = "dem",

refinement.method = "none",

data = dem,

match.missing = TRUE,

size.match = 5,

qoi = "att",

outcome.var = "y",

lead = 0:4,

forbid.treatment.reversal = FALSE,

use.diagonal.variance.matrix = TRUE

)

# visualize the treated unit and matched controls

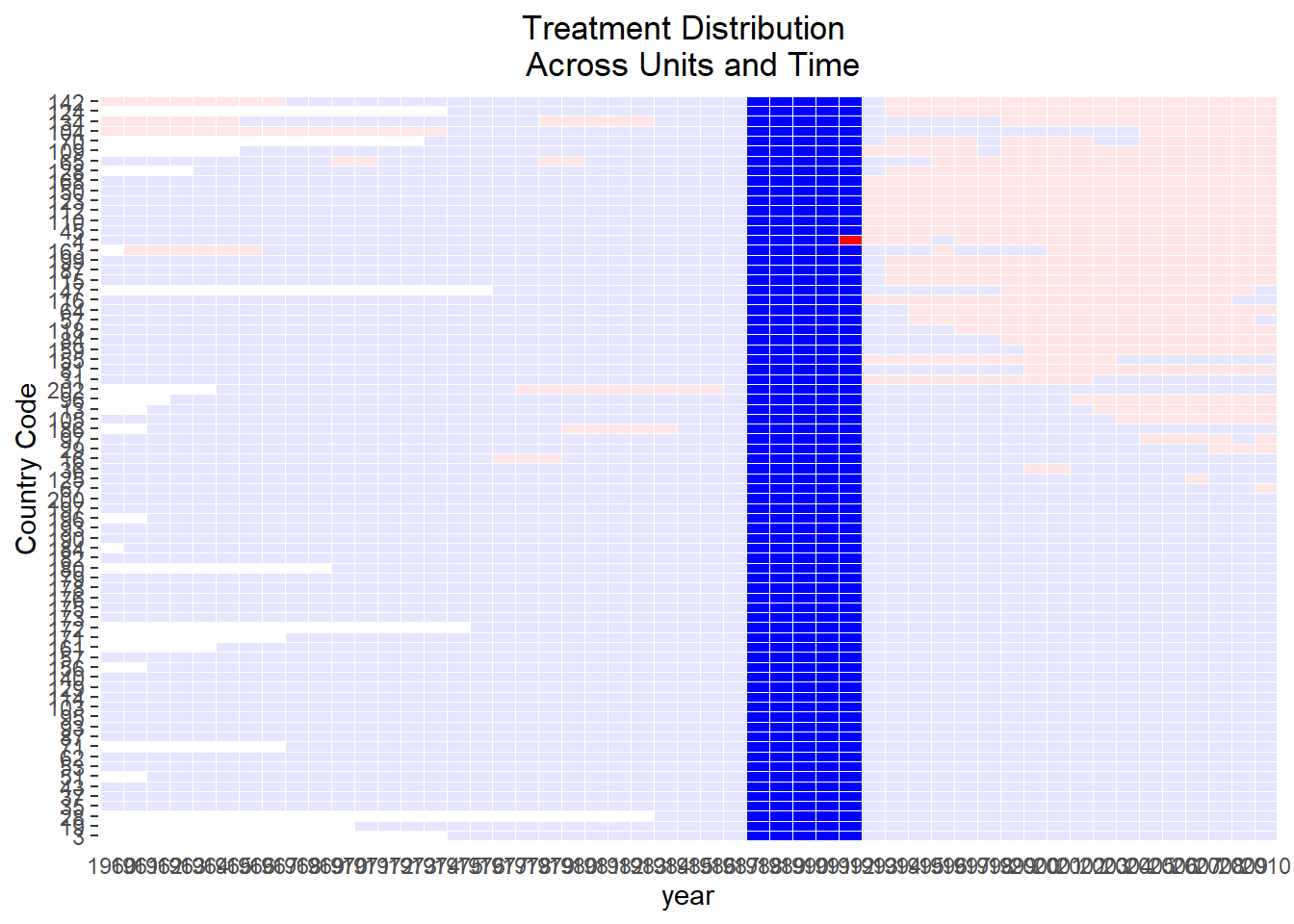

DisplayTreatment(

unit.id = "wbcode2",

time.id = "year",

legend.position = "none",

xlab = "year",

ylab = "Country Code",

treatment = "dem",

data = dem,

matched.set = PM.results.none$att[1],

# highlight the particular set

show.set.only = TRUE

)

Control units and the treated unit have identical treatment histories over the lag window (1988-1991)

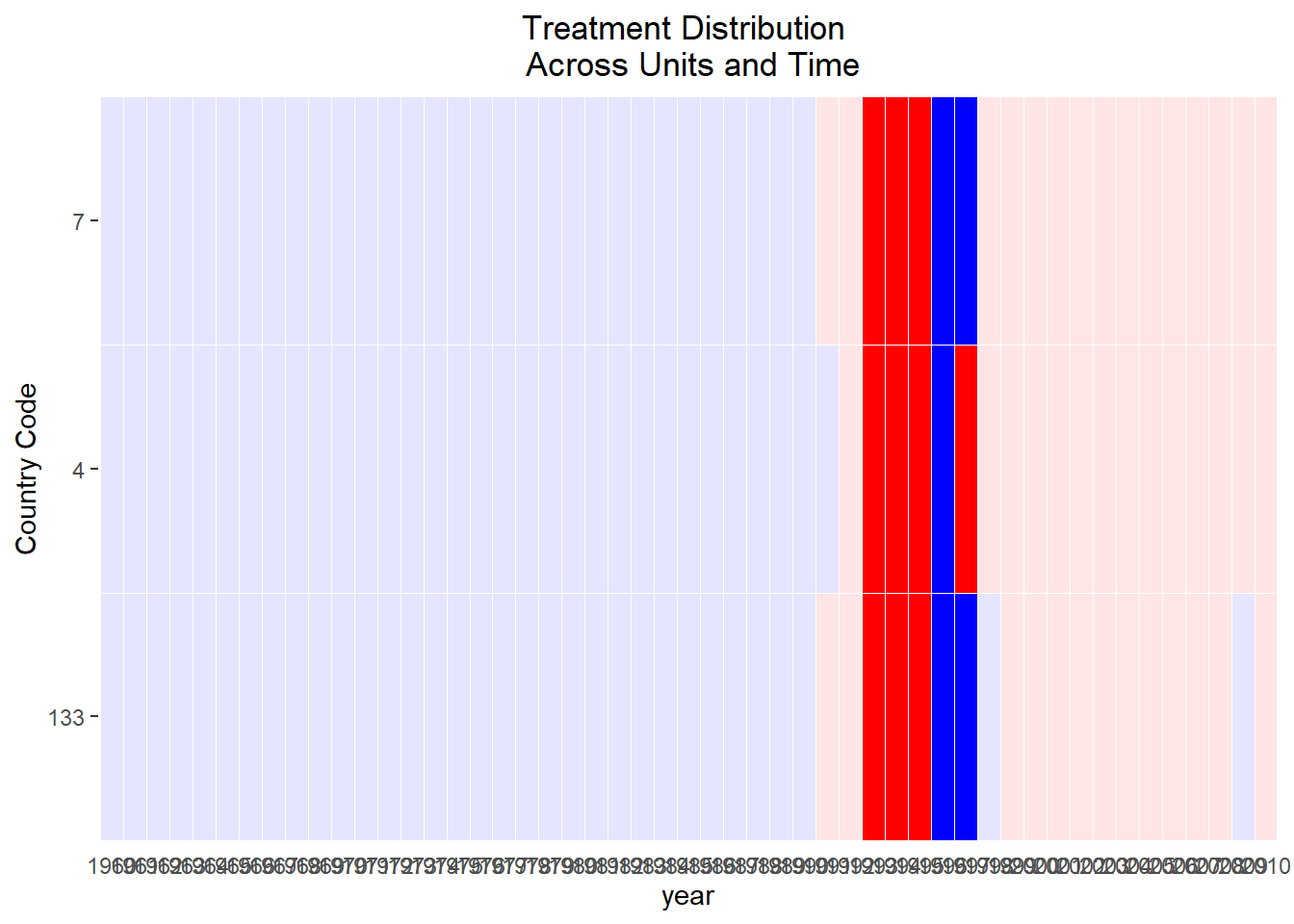

DisplayTreatment(

unit.id = "wbcode2",

time.id = "year",

legend.position = "none",

xlab = "year",

ylab = "Country Code",

treatment = "dem",

data = dem,

matched.set = PM.results.none$att[2],

# highlight the particular set

show.set.only = TRUE

)

This set is more limited than the first one, but we can still see that we have exact past histories.

Refining Matched Sets

Refinement involves assigning weights to control units.

Users must:

Specify a method for calculating unit similarity/distance.

Choose variables for similarity/distance calculations.

Select a Refinement Method

Users determine the refinement method via the

refinement.methodargument.Options include:

mahalanobisps.matchCBPS.matchps.weightCBPS.weightps.msm.weightCBPS.msm.weightnone

Methods with “match” in the name and Mahalanobis will assign equal weights to similar control units.

“Weighting” methods give higher weights to control units more similar to treated units.

Variable Selection

Users need to define which covariates will be used through the

covs.formulaargument, a one-sided formula object.Variables on the right side of the formula are used for calculations.

“Lagged” versions of variables can be included using the format:

I(lag(name.of.var, 0:n)).

Understanding

PanelMatchandmatched.setobjectsThe

PanelMatchfunction returns aPanelMatchobject.The most crucial element within the

PanelMatchobject is the matched.set object.Within the

PanelMatchobject, the matched.set object will have names like att, art, or atc.If

qoi = ate, there will be two matched.set objects: att and atc.

Matched.set Object Details

matched.set is a named list with added attributes.

Attributes include:

Lag

Names of treatment

Unit and time variables

Each list entry represents a matched set of treated and control units.

Naming follows a structure:

[id variable].[time variable].Each list element is a vector of control unit ids that match the treated unit mentioned in the element name.

Since it’s a matching method, weights are only given to the

size.matchmost similar control units based on distance calculations.

# PanelMatch without any refinement

PM.results.none <-

PanelMatch(

lag = 4,

time.id = "year",

unit.id = "wbcode2",

treatment = "dem",

refinement.method = "none",

data = dem,

match.missing = TRUE,

size.match = 5,

qoi = "att",

outcome.var = "y",

lead = 0:4,

forbid.treatment.reversal = FALSE,

use.diagonal.variance.matrix = TRUE

)

# Extract the matched.set object

msets.none <- PM.results.none$att

# PanelMatch with refinement

PM.results.maha <-

PanelMatch(

lag = 4,

time.id = "year",

unit.id = "wbcode2",

treatment = "dem",

refinement.method = "mahalanobis", # use Mahalanobis distance

data = dem,

match.missing = TRUE,

covs.formula = ~ tradewb,

size.match = 5,

qoi = "att" ,

outcome.var = "y",

lead = 0:4,

forbid.treatment.reversal = FALSE,

use.diagonal.variance.matrix = TRUE

)

msets.maha <- PM.results.maha$att# these 2 should be identical because weights are not shown

msets.none |> head()

#> wbcode2 year matched.set.size

#> 1 4 1992 74

#> 2 4 1997 2

#> 3 6 1973 63

#> 4 6 1983 73

#> 5 7 1991 81

#> 6 7 1998 1

msets.maha |> head()

#> wbcode2 year matched.set.size

#> 1 4 1992 74

#> 2 4 1997 2

#> 3 6 1973 63

#> 4 6 1983 73

#> 5 7 1991 81

#> 6 7 1998 1

# summary(msets.none)

# summary(msets.maha)Visualizing Matched Sets with the plot method

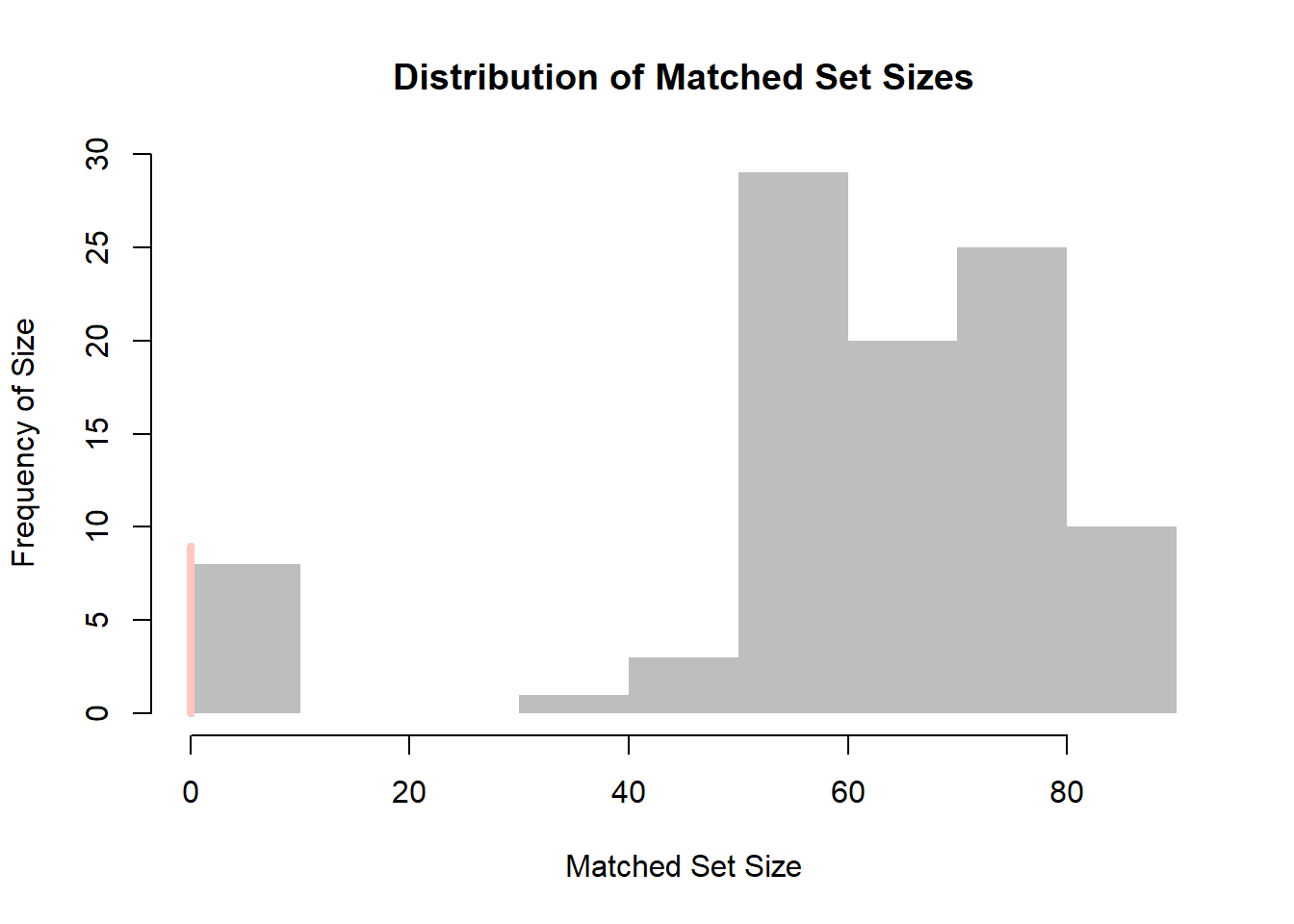

Users can visualize the distribution of the matched set sizes.

A red line, by default, indicates the count of matched sets where treated units had no matching control units (i.e., empty matched sets).

Plot adjustments can be made using

graphics::plot.

Comparing Methods of Refinement

Users are encouraged to:

Use substantive knowledge for experimentation and evaluation.

Consider the following when configuring

PanelMatch:The number of matched sets.

The number of controls matched to each treated unit.

Achieving covariate balance.

Note: Large numbers of small matched sets can lead to larger standard errors during the estimation stage.

Covariates that aren’t well balanced can lead to undesirable comparisons between treated and control units.

Aspects to consider include:

Refinement method.

Variables for weight calculation.

Size of the lag window.

Procedures for addressing missing data (refer to

match.missingandlistwise.deletearguments).Maximum size of matched sets (for matching methods).

Supportive Features:

print,plot, andsummarymethods assist in understanding matched sets and their sizes.get_covariate_balancehelps evaluate covariate balance:- Lower values in the covariate balance calculations are preferred.

PM.results.none <-

PanelMatch(

lag = 4,

time.id = "year",

unit.id = "wbcode2",

treatment = "dem",

refinement.method = "none",

data = dem,

match.missing = TRUE,

size.match = 5,

qoi = "att",

outcome.var = "y",

lead = 0:4,

forbid.treatment.reversal = FALSE,

use.diagonal.variance.matrix = TRUE

)

PM.results.maha <-

PanelMatch(

lag = 4,

time.id = "year",

unit.id = "wbcode2",

treatment = "dem",

refinement.method = "mahalanobis",

data = dem,

match.missing = TRUE,

covs.formula = ~ I(lag(tradewb, 1:4)) + I(lag(y, 1:4)),

size.match = 5,

qoi = "att",

outcome.var = "y",

lead = 0:4,

forbid.treatment.reversal = FALSE,

use.diagonal.variance.matrix = TRUE

)

# listwise deletion used for missing data

PM.results.listwise <-

PanelMatch(

lag = 4,

time.id = "year",

unit.id = "wbcode2",

treatment = "dem",

refinement.method = "mahalanobis",

data = dem,

match.missing = FALSE,

listwise.delete = TRUE,

covs.formula = ~ I(lag(tradewb, 1:4)) + I(lag(y, 1:4)),

size.match = 5,

qoi = "att",

outcome.var = "y",

lead = 0:4,

forbid.treatment.reversal = FALSE,

use.diagonal.variance.matrix = TRUE

)

# propensity score based weighting method

PM.results.ps.weight <-

PanelMatch(

lag = 4,

time.id = "year",

unit.id = "wbcode2",

treatment = "dem",

refinement.method = "ps.weight",

data = dem,

match.missing = FALSE,

listwise.delete = TRUE,

covs.formula = ~ I(lag(tradewb, 1:4)) + I(lag(y, 1:4)),

size.match = 5,

qoi = "att",

outcome.var = "y",

lead = 0:4,

forbid.treatment.reversal = FALSE

)

get_covariate_balance(

PM.results.none$att,

data = dem,

covariates = c("tradewb", "y"),

plot = FALSE

)

#> tradewb y

#> t_4 -0.07245466 0.291871990

#> t_3 -0.20930129 0.208654876

#> t_2 -0.24425207 0.107736647

#> t_1 -0.10806125 -0.004950238

#> t_0 -0.09493854 -0.015198483

get_covariate_balance(

PM.results.maha$att,

data = dem,

covariates = c("tradewb", "y"),

plot = FALSE

)

#> tradewb y

#> t_4 0.04558637 0.09701606

#> t_3 -0.03312750 0.10844046

#> t_2 -0.01396793 0.08890753

#> t_1 0.10474894 0.06618865

#> t_0 0.15885415 0.05691437

get_covariate_balance(

PM.results.listwise$att,

data = dem,

covariates = c("tradewb", "y"),

plot = FALSE

)

#> tradewb y

#> t_4 0.05634922 0.05223623

#> t_3 -0.01104797 0.05217896

#> t_2 0.01411473 0.03094133

#> t_1 0.06850180 0.02092209

#> t_0 0.05044958 0.01943728

get_covariate_balance(

PM.results.ps.weight$att,

data = dem,

covariates = c("tradewb", "y"),

plot = FALSE

)

#> tradewb y

#> t_4 0.014362590 0.04035905

#> t_3 0.005529734 0.04188731

#> t_2 0.009410044 0.04195008

#> t_1 0.027907540 0.03975173

#> t_0 0.040272235 0.04167921get_covariate_balance Function Options:

Allows for the generation of plots displaying covariate balance using

plot = TRUE.Plots can be customized using arguments typically used with the base R

plotmethod.Option to set

use.equal.weights = TRUEfor:Obtaining the balance of unrefined sets.

Facilitating understanding of the refinement’s impact.

# Use equal weights

get_covariate_balance(

PM.results.ps.weight$att,

data = dem,

use.equal.weights = TRUE,

covariates = c("tradewb", "y"),

plot = TRUE,

# visualize by setting plot to TRUE

ylim = c(-1, 1)

)

# Compare covariate balance to refined sets

# See large improvement in balance

get_covariate_balance(

PM.results.ps.weight$att,

data = dem,

covariates = c("tradewb", "y"),

plot = TRUE,

# visualize by setting plot to TRUE

ylim = c(-1, 1)

)

balance_scatter(

matched_set_list = list(PM.results.maha$att,

PM.results.ps.weight$att),

data = dem,

covariates = c("y", "tradewb")

)

PanelEstimate

Standard Error Calculation Methods

There are different methods available:

Bootstrap (default method with 1000 iterations).

Conditional: Assumes independence across units, but not time.

Unconditional: Doesn’t make assumptions of independence across units or time.

For

qoivalues set toatt,art, oratc(Imai, Kim, and Wang 2021):- You can use analytical methods for calculating standard errors, which include both “conditional” and “unconditional” methods.

PE.results <- PanelEstimate(

sets = PM.results.ps.weight,

data = dem,

se.method = "bootstrap",

number.iterations = 1000,

confidence.level = .95

)

# point estimates

PE.results[["estimates"]]

#> t+0 t+1 t+2 t+3 t+4

#> 0.2609565 0.9630847 1.2851017 1.7370930 1.4871846

# standard errors

PE.results[["standard.error"]]

#> t+0 t+1 t+2 t+3 t+4

#> 0.6486861 0.9904181 1.3500793 1.7214773 2.1019165

# use conditional method

PE.results <- PanelEstimate(

sets = PM.results.ps.weight,

data = dem,

se.method = "conditional",

confidence.level = .95

)

# point estimates

PE.results[["estimates"]]

#> t+0 t+1 t+2 t+3 t+4

#> 0.2609565 0.9630847 1.2851017 1.7370930 1.4871846

# standard errors

PE.results[["standard.error"]]

#> t+0 t+1 t+2 t+3 t+4

#> 0.4844805 0.8170604 1.1171942 1.4116879 1.7172143

summary(PE.results)

#> Weighted Difference-in-Differences with Propensity Score

#> Matches created with 4 lags

#>

#> Standard errors computed with conditional method

#>

#> Estimate of Average Treatment Effect on the Treated (ATT) by Period:

#> $summary

#> estimate std.error 2.5% 97.5%

#> t+0 0.2609565 0.4844805 -0.6886078 1.210521

#> t+1 0.9630847 0.8170604 -0.6383243 2.564494

#> t+2 1.2851017 1.1171942 -0.9045586 3.474762

#> t+3 1.7370930 1.4116879 -1.0297644 4.503950

#> t+4 1.4871846 1.7172143 -1.8784937 4.852863

#>

#> $lag

#> [1] 4

#>

#> $qoi

#> [1] "att"

plot(PE.results)

Moderating Variables

# moderating variable

dem$moderator <- 0

dem$moderator <- ifelse(dem$wbcode2 > 100, 1, 2)

PM.results <-

PanelMatch(

lag = 4,

time.id = "year",

unit.id = "wbcode2",

treatment = "dem",

refinement.method = "mahalanobis",

data = dem,

match.missing = TRUE,

covs.formula = ~ I(lag(tradewb, 1:4)) + I(lag(y, 1:4)),

size.match = 5,

qoi = "att",

outcome.var = "y",

lead = 0:4,

forbid.treatment.reversal = FALSE,

use.diagonal.variance.matrix = TRUE

)

PE.results <-

PanelEstimate(sets = PM.results,

data = dem,

moderator = "moderator")

# Each element in the list corresponds to a level in the moderator

plot(PE.results[[1]])

To write up for journal submission, you can follow the following report:

In this study, closely aligned with the research by (Acemoglu et al. 2019), two key effects of democracy on economic growth are estimated: the impact of democratization and that of authoritarian reversal. The treatment variable, Xit, is defined to be one if country i is democratic in year t, and zero otherwise.

The Average Treatment Effect for the Treated (ATT) under democratization is formulated as follows:

δ(F,L)=E{Yi,t+F(Xit=1,Xi,t−1=0,{Xi,t−l}Ll=2)−Yi,t+F(Xit=0,Xi,t−1=0,{Xi,t−l}Ll=2)|Xit=1,Xi,t−1=0}

In this framework, the treated observations are countries that transition from an authoritarian regime Xit−1=0 to a democratic one Xit=1. The variable F represents the number of leads, denoting the time periods following the treatment, and L signifies the number of lags, indicating the time periods preceding the treatment.

The ATT under authoritarian reversal is given by:

E[Yi,t+F(Xit=0,Xi,t−1=1,{Xi,t−l}Ll=2)−Yi,t+F(Xit=1,Xit−1=1,{Xi,t−l}Ll=2)|Xit=0,Xi,t−1=1]

The ATT is calculated conditioning on 4 years of lags (L=4) and up to 4 years following the policy change F=1,2,3,4. Matched sets for each treated observation are constructed based on its treatment history, with the number of matched control units generally decreasing when considering a 4-year treatment history as compared to a 1-year history.

To enhance the quality of matched sets, methods such as Mahalanobis distance matching, propensity score matching, and propensity score weighting are utilized. These approaches enable us to evaluate the effectiveness of each refinement method. In the process of matching, we employ both up-to-five and up-to-ten matching to investigate how sensitive our empirical results are to the maximum number of allowed matches. For more information on the refinement process, please see the Web Appendix

The Mahalanobis distance is expressed through a specific formula. We aim to pair each treated unit with a maximum of J control units, permitting replacement, denoted as |Mit≤J|. The average Mahalanobis distance between a treated and each control unit over time is computed as:

Sit(i′)=1LL∑l=1√(Vi,t−l−Vi′,t−l)TΣ−1i,t−l(Vi,t−l−Vi′,t−l)

For a matched control unit i′∈Mit, Vit′ represents the time-varying covariates to adjust for, and Σit′ is the sample covariance matrix for Vit′. Essentially, we calculate a standardized distance using time-varying covariates and average this across different time intervals.

In the context of propensity score matching, we employ a logistic regression model with balanced covariates to derive the propensity score. Defined as the conditional likelihood of treatment given pre-treatment covariates (Rosenbaum and Rubin 1983), the propensity score is estimated by first creating a data subset comprised of all treated and their matched control units from the same year. This logistic regression model is then fitted as follows:

eit({Ui,t−l}Ll=1)=Pr(Xit=1|Ui,t−1,…,Ui,t−L)=11=exp(−∑Ll=1βTlUi,t−l)

where Uit′=(Xit′,VTit′)T. Given this model, the estimated propensity score for all treated and matched control units is then computed. This enables the adjustment for lagged covariates via matching on the calculated propensity score, resulting in the following distance measure:

Sit(i′)=|logit{ˆeit({Ui,t−l}Ll=1)}−logit{ˆei′t({Ui′,t−l}Ll=1)}|

Here, ˆei′t({Ui,t−l}Ll=1) represents the estimated propensity score for each matched control unit i′∈Mit.

Once the distance measure Sit(i′) has been determined for all control units in the original matched set, we fine-tune this set by selecting up to J closest control units, which meet a researcher-defined caliper constraint C. All other control units receive zero weight. This results in a refined matched set for each treated unit (i,t):

M∗it={i′:i′∈Mit,Sit(i′)<C,Sit≤S(J)it}

S(J)it is the Jth smallest distance among the control units in the original set Mit.

For further refinement using weighting, a weight is assigned to each control unit i′ in a matched set corresponding to a treated unit (i,t), with greater weight accorded to more similar units. We utilize inverse propensity score weighting, based on the propensity score model mentioned earlier:

wi′it∝ˆei′t({Ui,t−l}Ll=1)1−ˆei′t({Ui,t−l}Ll=1)

In this model, ∑i′∈Mitwi′it=1 and wi′it=0 for i′∉Mit. The model is fitted to the complete sample of treated and matched control units.

Checking Covariate Balance A distinct advantage of the proposed methodology over regression methods is the ability it offers researchers to inspect the covariate balance between treated and matched control observations. This facilitates the evaluation of whether treated and matched control observations are comparable regarding observed confounders. To investigate the mean difference of each covariate (e.g., Vit′j, representing the j-th variable in Vit′) between the treated observation and its matched control observation at each pre-treatment time period (i.e., t′<t), we further standardize this difference. For any given pretreatment time period, we adjust by the standard deviation of each covariate across all treated observations in the dataset. Thus, the mean difference is quantified in terms of standard deviation units. Formally, for each treated observation (i,t) where Dit=1, we define the covariate balance for variable j at the pretreatment time period t−l as: Bit(j,l)=Vi,t−l,j−∑i′∈Mitwi′itVi′,t−l,j√1N1−1∑Ni′=1∑T−Ft′=L+1Di′t′(Vi′,t′−l,j−ˉVt′−l,j)2 where N1=∑Ni′=1∑T−Ft′=L+1Di′t′ denotes the total number of treated observations and ˉVt−l,j=∑Ni=1Di,t−l,j/N. We then aggregate this covariate balance measure across all treated observations for each covariate and pre-treatment time period: ˉB(j,l)=1N1N∑i=1T−F∑t=L+1DitBit(j,l) Lastly, we evaluate the balance of lagged outcome variables over several pre-treatment periods and that of time-varying covariates. This examination aids in assessing the validity of the parallel trend assumption integral to the DiD estimator justification.

In Figure ??, we demonstrate the enhancement of covariate balance thank to the refinement of matched sets. Each scatter plot contrasts the absolute standardized mean difference, as detailed in Equation (??), before (horizontal axis) and after (vertical axis) this refinement. Points below the 45-degree line indicate an improved standardized mean balance for certain time-varying covariates post-refinement. The majority of variables benefit from this refinement process. Notably, the propensity score weighting (bottom panel) shows the most significant improvement, whereas Mahalanobis matching (top panel) yields a more modest improvement.

library(PanelMatch)

library(causalverse)

runPanelMatch <- function(method, lag, size.match=NULL, qoi="att") {

# Default parameters for PanelMatch

common.args <- list(

lag = lag,

time.id = "year",

unit.id = "wbcode2",

treatment = "dem",

data = dem,

covs.formula = ~ I(lag(tradewb, 1:4)) + I(lag(y, 1:4)),

qoi = qoi,

outcome.var = "y",

lead = 0:4,

forbid.treatment.reversal = FALSE,

size.match = size.match # setting size.match here for all methods

)

if(method == "mahalanobis") {

common.args$refinement.method <- "mahalanobis"

common.args$match.missing <- TRUE

common.args$use.diagonal.variance.matrix <- TRUE

} else if(method == "ps.match") {

common.args$refinement.method <- "ps.match"

common.args$match.missing <- FALSE

common.args$listwise.delete <- TRUE

} else if(method == "ps.weight") {

common.args$refinement.method <- "ps.weight"

common.args$match.missing <- FALSE

common.args$listwise.delete <- TRUE

}

return(do.call(PanelMatch, common.args))

}

methods <- c("mahalanobis", "ps.match", "ps.weight")

lags <- c(1, 4)

sizes <- c(5, 10)You can either do it sequentailly

res_pm <- list()

for(method in methods) {

for(lag in lags) {

for(size in sizes) {

name <- paste0(method, ".", lag, "lag.", size, "m")

res_pm[[name]] <- runPanelMatch(method, lag, size)

}

}

}

# Now, you can access res_pm using res_pm[["mahalanobis.1lag.5m"]] etc.

# for treatment reversal

res_pm_rev <- list()

for(method in methods) {

for(lag in lags) {

for(size in sizes) {

name <- paste0(method, ".", lag, "lag.", size, "m")

res_pm_rev[[name]] <- runPanelMatch(method, lag, size, qoi = "art")

}

}

}or in parallel

library(foreach)

library(doParallel)

registerDoParallel(cores = 4)

# Initialize an empty list to store results

res_pm <- list()

# Replace nested for-loops with foreach

results <-

foreach(

method = methods,

.combine = 'c',

.multicombine = TRUE,

.packages = c("PanelMatch", "causalverse")

) %dopar% {

tmp <- list()

for (lag in lags) {

for (size in sizes) {

name <- paste0(method, ".", lag, "lag.", size, "m")

tmp[[name]] <- runPanelMatch(method, lag, size)

}

}

tmp

}

# Collate results

for (name in names(results)) {

res_pm[[name]] <- results[[name]]

}

# Treatment reversal

# Initialize an empty list to store results

res_pm_rev <- list()

# Replace nested for-loops with foreach

results_rev <-

foreach(

method = methods,

.combine = 'c',

.multicombine = TRUE,

.packages = c("PanelMatch", "causalverse")

) %dopar% {

tmp <- list()

for (lag in lags) {

for (size in sizes) {

name <- paste0(method, ".", lag, "lag.", size, "m")

tmp[[name]] <-

runPanelMatch(method, lag, size, qoi = "art")

}

}

tmp

}

# Collate results

for (name in names(results_rev)) {

res_pm_rev[[name]] <- results_rev[[name]]

}

stopImplicitCluster()library(gridExtra)

# Updated plotting function

create_balance_plot <- function(method, lag, sizes, res_pm, dem) {

matched_set_lists <- lapply(sizes, function(size) {

res_pm[[paste0(method, ".", lag, "lag.", size, "m")]]$att

})

return(

balance_scatter_custom(

matched_set_list = matched_set_lists,

legend.title = "Possible Matches",

set.names = as.character(sizes),

legend.position = c(0.2, 0.8),

# for compiled plot, you don't need x,y, or main labs

x.axis.label = "",

y.axis.label = "",

main = "",

data = dem,

dot.size = 5,

# show.legend = F,

them_use = causalverse::ama_theme(base_size = 32),

covariates = c("y", "tradewb")

)

)

}

plots <- list()

for (method in methods) {

for (lag in lags) {

plots[[paste0(method, ".", lag, "lag")]] <-

create_balance_plot(method, lag, sizes, res_pm, dem)

}

}

# # Arranging plots in a 3x2 grid

# grid.arrange(plots[["mahalanobis.1lag"]],

# plots[["mahalanobis.4lag"]],

# plots[["ps.match.1lag"]],

# plots[["ps.match.4lag"]],

# plots[["ps.weight.1lag"]],

# plots[["ps.weight.4lag"]],

# ncol=2, nrow=3)

# Standardized Mean Difference of Covariates

library(gridExtra)

library(grid)

# Create column and row labels using textGrob

col_labels <- c("1-year Lag", "4-year Lag")

row_labels <- c("Maha Matching", "PS Matching", "PS Weigthing")

major.axes.fontsize = 40

minor.axes.fontsize = 30

png(

file.path(getwd(), "images", "did_balance_scatter.png"),

width = 1200,

height = 1000

)

# Create a list-of-lists, where each inner list represents a row

grid_list <- list(

list(

nullGrob(),

textGrob(col_labels[1], gp = gpar(fontsize = minor.axes.fontsize)),

textGrob(col_labels[2], gp = gpar(fontsize = minor.axes.fontsize))

),

list(textGrob(

row_labels[1],

gp = gpar(fontsize = minor.axes.fontsize),

rot = 90

), plots[["mahalanobis.1lag"]], plots[["mahalanobis.4lag"]]),

list(textGrob(

row_labels[2],

gp = gpar(fontsize = minor.axes.fontsize),

rot = 90

), plots[["ps.match.1lag"]], plots[["ps.match.4lag"]]),

list(textGrob(

row_labels[3],

gp = gpar(fontsize = minor.axes.fontsize),

rot = 90

), plots[["ps.weight.1lag"]], plots[["ps.weight.4lag"]])

)

# "Flatten" the list-of-lists into a single list of grobs

grobs <- do.call(c, grid_list)

grid.arrange(

grobs = grobs,

ncol = 3,

nrow = 4,

widths = c(0.15, 0.42, 0.42),

heights = c(0.15, 0.28, 0.28, 0.28)

)

grid.text(

"Before Refinement",

x = 0.5,

y = 0.03,

gp = gpar(fontsize = major.axes.fontsize)

)

grid.text(

"After Refinement",

x = 0.03,

y = 0.5,

rot = 90,

gp = gpar(fontsize = major.axes.fontsize)

)

dev.off()

#> png

#> 2Note: Scatter plots display the standardized mean difference of each covariate j and lag year l as defined in Equation (??) before (x-axis) and after (y-axis) matched set refinement. Each plot includes varying numbers of possible matches for each matching method. Rows represent different matching/weighting methods, while columns indicate adjustments for various lag lengths.

# Step 1: Define configurations

configurations <- list(

list(refinement.method = "none", qoi = "att"),

list(refinement.method = "none", qoi = "art"),

list(refinement.method = "mahalanobis", qoi = "att"),

list(refinement.method = "mahalanobis", qoi = "art"),

list(refinement.method = "ps.match", qoi = "att"),

list(refinement.method = "ps.match", qoi = "art"),

list(refinement.method = "ps.weight", qoi = "att"),

list(refinement.method = "ps.weight", qoi = "art")

)

# Step 2: Use lapply or loop to generate results

results <- lapply(configurations, function(config) {

PanelMatch(

lag = 4,

time.id = "year",

unit.id = "wbcode2",

treatment = "dem",

data = dem,

match.missing = FALSE,

listwise.delete = TRUE,

size.match = 5,

outcome.var = "y",

lead = 0:4,

forbid.treatment.reversal = FALSE,

refinement.method = config$refinement.method,

covs.formula = ~ I(lag(tradewb, 1:4)) + I(lag(y, 1:4)),

qoi = config$qoi

)

})

# Step 3: Get covariate balance and plot

plots <- mapply(function(result, config) {

df <- get_covariate_balance(

if (config$qoi == "att")

result$att

else

result$art,

data = dem,

covariates = c("tradewb", "y"),

plot = F

)

causalverse::plot_covariate_balance_pretrend(df, main = "", show_legend = F)

}, results, configurations, SIMPLIFY = FALSE)

# Set names for plots

names(plots) <- sapply(configurations, function(config) {

paste(config$qoi, config$refinement.method, sep = ".")

})To export

library(gridExtra)

library(grid)

# Column and row labels

col_labels <-

c("None",

"Mahalanobis",

"Propensity Score Matching",

"Propensity Score Weighting")

row_labels <- c("ATT", "ART")

# Specify your desired fontsize for labels

minor.axes.fontsize <- 16

major.axes.fontsize <- 20

png(file.path(getwd(), "images", "p_covariate_balance.png"), width=1200, height=1000)

# Create a list-of-lists, where each inner list represents a row

grid_list <- list(

list(

nullGrob(),

textGrob(col_labels[1], gp = gpar(fontsize = minor.axes.fontsize)),

textGrob(col_labels[2], gp = gpar(fontsize = minor.axes.fontsize)),

textGrob(col_labels[3], gp = gpar(fontsize = minor.axes.fontsize)),

textGrob(col_labels[4], gp = gpar(fontsize = minor.axes.fontsize))

),

list(

textGrob(

row_labels[1],

gp = gpar(fontsize = minor.axes.fontsize),

rot = 90

),

plots$att.none,

plots$att.mahalanobis,

plots$att.ps.match,

plots$att.ps.weight

),

list(

textGrob(

row_labels[2],

gp = gpar(fontsize = minor.axes.fontsize),

rot = 90

),

plots$art.none,

plots$art.mahalanobis,

plots$art.ps.match,

plots$art.ps.weight

)

)

# "Flatten" the list-of-lists into a single list of grobs

grobs <- do.call(c, grid_list)

# Arrange your plots with text labels

grid.arrange(

grobs = grobs,

ncol = 5,

nrow = 3,

widths = c(0.1, 0.225, 0.225, 0.225, 0.225),

heights = c(0.1, 0.45, 0.45)

)

# Add main x and y axis titles

grid.text(

"Refinement Methods",

x = 0.5,

y = 0.01,

gp = gpar(fontsize = major.axes.fontsize)

)

grid.text(

"Quantities of Interest",

x = 0.02,

y = 0.5,

rot = 90,

gp = gpar(fontsize = major.axes.fontsize)

)

dev.off()

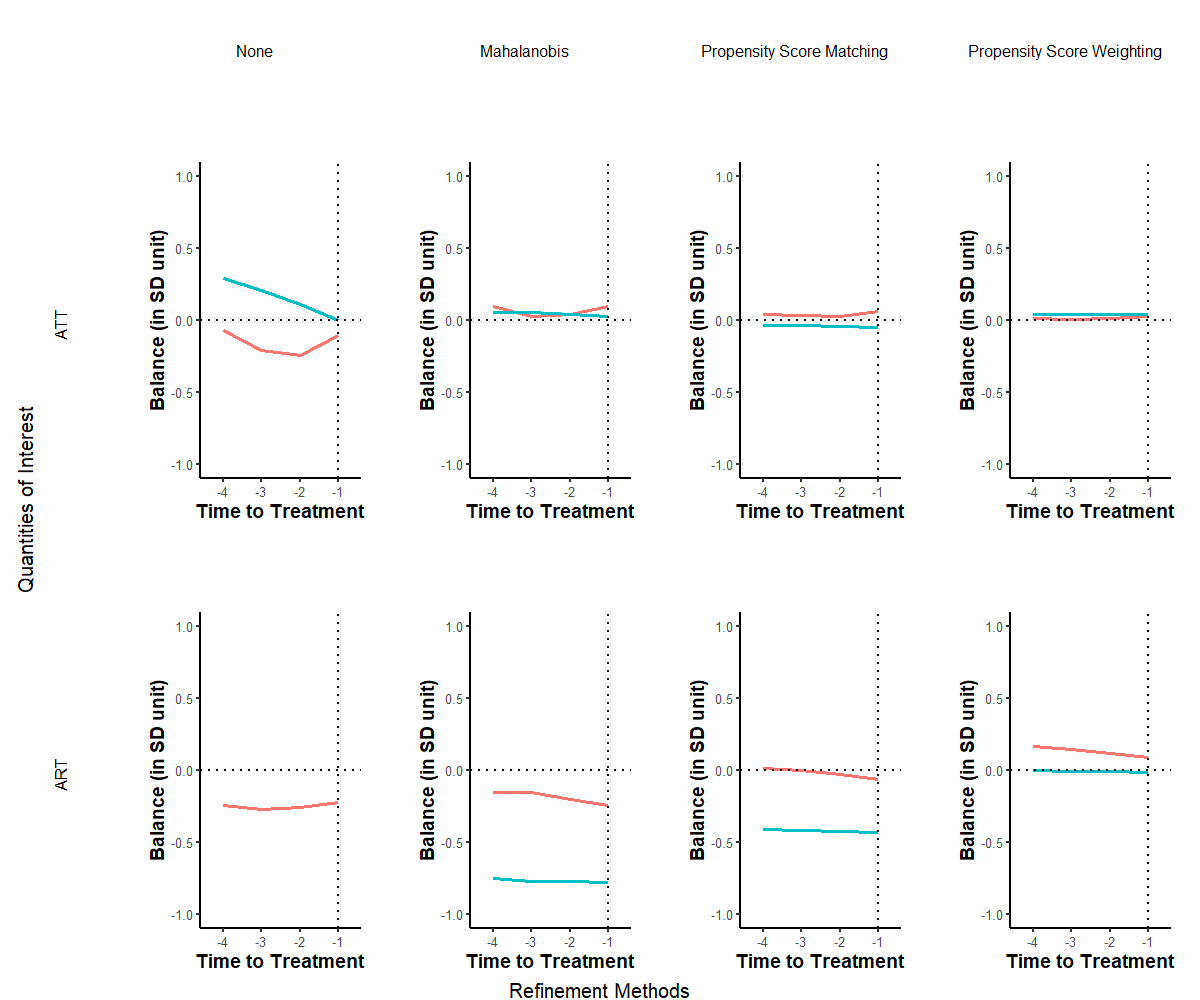

Note: Each graph displays the standardized mean difference, as outlined in Equation (??), plotted on the vertical axis across a pre-treatment duration of four years represented on the horizontal axis. The leftmost column illustrates the balance prior to refinement, while the subsequent three columns depict the covariate balance post the application of distinct refinement techniques. Each individual line signifies the balance of a specific variable during the pre-treatment phase.The red line is tradewb and blue line is the lagged outcome variable.

In Figure ??, we observe a marked improvement in covariate balance due to the implemented matching procedures during the pre-treatment period. Our analysis prioritizes methods that adjust for time-varying covariates over a span of four years preceding the treatment initiation. The two rows delineate the standardized mean balance for both treatment modalities, with individual lines representing the balance for each covariate.

Across all scenarios, the refinement attributed to matched sets significantly enhances balance. Notably, using propensity score weighting considerably mitigates imbalances in confounders. While some degree of imbalance remains evident in the Mahalanobis distance and propensity score matching techniques, the standardized mean difference for the lagged outcome remains stable throughout the pre-treatment phase. This consistency lends credence to the validity of the proposed DiD estimator.

Estimation Results

We now detail the estimated ATTs derived from the matching techniques. Figure below offers visual representations of the impacts of treatment initiation (upper panel) and treatment reversal (lower panel) on the outcome variable for a duration of 5 years post-transition, specifically, (F=0,1,…,4). Across the five methods (columns), it becomes evident that the point estimates of effects associated with treatment initiation consistently approximate zero over the 5-year window. In contrast, the estimated outcomes of treatment reversal are notably negative and maintain statistical significance through all refinement techniques during the initial year of transition and the 1 to 4 years that follow, provided treatment reversal is permissible. These effects are notably pronounced, pointing to an estimated reduction of roughly X% in the outcome variable.

Collectively, these findings indicate that the transition into the treated state from its absence doesn’t invariably lead to a heightened outcome. Instead, the transition from the treated state back to its absence exerts a considerable negative effect on the outcome variable in both the short and intermediate terms. Hence, the positive effect of the treatment (if we were to use traditional DiD) is actually driven by the negative effect of treatment reversal.

# sequential

# Step 1: Apply PanelEstimate function

# Initialize an empty list to store results

res_est <- vector("list", length(res_pm))

# Iterate over each element in res_pm

for (i in 1:length(res_pm)) {

res_est[[i]] <- PanelEstimate(

res_pm[[i]],

data = dem,

se.method = "bootstrap",

number.iterations = 1000,

confidence.level = .95

)

# Transfer the name of the current element to the res_est list

names(res_est)[i] <- names(res_pm)[i]

}

# Step 2: Apply plot_PanelEstimate function

# Initialize an empty list to store plot results

res_est_plot <- vector("list", length(res_est))

# Iterate over each element in res_est

for (i in 1:length(res_est)) {

res_est_plot[[i]] <-

plot_PanelEstimate(res_est[[i]],

main = "",

theme_use = causalverse::ama_theme(base_size = 14))

# Transfer the name of the current element to the res_est_plot list

names(res_est_plot)[i] <- names(res_est)[i]

}

# check results

# res_est_plot$mahalanobis.1lag.5m

# Step 1: Apply PanelEstimate function for res_pm_rev

# Initialize an empty list to store results

res_est_rev <- vector("list", length(res_pm_rev))

# Iterate over each element in res_pm_rev

for (i in 1:length(res_pm_rev)) {

res_est_rev[[i]] <- PanelEstimate(

res_pm_rev[[i]],

data = dem,

se.method = "bootstrap",

number.iterations = 1000,

confidence.level = .95

)

# Transfer the name of the current element to the res_est_rev list

names(res_est_rev)[i] <- names(res_pm_rev)[i]

}

# Step 2: Apply plot_PanelEstimate function for res_est_rev

# Initialize an empty list to store plot results

res_est_plot_rev <- vector("list", length(res_est_rev))

# Iterate over each element in res_est_rev

for (i in 1:length(res_est_rev)) {

res_est_plot_rev[[i]] <-

plot_PanelEstimate(res_est_rev[[i]],

main = "",

theme_use = causalverse::ama_theme(base_size = 14))

# Transfer the name of the current element to the res_est_plot_rev list

names(res_est_plot_rev)[i] <- names(res_est_rev)[i]

}# parallel

library(doParallel)

library(foreach)

# Detect the number of cores to use for parallel processing

num_cores <- 4

# Register the parallel backend

cl <- makeCluster(num_cores)

registerDoParallel(cl)

# Step 1: Apply PanelEstimate function in parallel

res_est <-

foreach(i = 1:length(res_pm), .packages = "PanelMatch") %dopar% {

PanelEstimate(

res_pm[[i]],

data = dem,

se.method = "bootstrap",

number.iterations = 1000,

confidence.level = .95

)

}

# Transfer names from res_pm to res_est

names(res_est) <- names(res_pm)

# Step 2: Apply plot_PanelEstimate function in parallel

res_est_plot <-

foreach(

i = 1:length(res_est),

.packages = c("PanelMatch", "causalverse", "ggplot2")

) %dopar% {

plot_PanelEstimate(res_est[[i]],

main = "",

theme_use = causalverse::ama_theme(base_size = 10))

}

# Transfer names from res_est to res_est_plot

names(res_est_plot) <- names(res_est)

# Step 1: Apply PanelEstimate function for res_pm_rev in parallel

res_est_rev <-

foreach(i = 1:length(res_pm_rev), .packages = "PanelMatch") %dopar% {

PanelEstimate(

res_pm_rev[[i]],

data = dem,

se.method = "bootstrap",

number.iterations = 1000,

confidence.level = .95

)

}

# Transfer names from res_pm_rev to res_est_rev

names(res_est_rev) <- names(res_pm_rev)

# Step 2: Apply plot_PanelEstimate function for res_est_rev in parallel

res_est_plot_rev <-

foreach(

i = 1:length(res_est_rev),

.packages = c("PanelMatch", "causalverse", "ggplot2")

) %dopar% {

plot_PanelEstimate(res_est_rev[[i]],

main = "",

theme_use = causalverse::ama_theme(base_size = 10))

}

# Transfer names from res_est_rev to res_est_plot_rev

names(res_est_plot_rev) <- names(res_est_rev)

# Stop the cluster

stopCluster(cl)To export

library(gridExtra)

library(grid)

# Column and row labels

col_labels <- c("Mahalanobis 5m",

"Mahalanobis 10m",

"PS Matching 5m",

"PS Matching 10m",

"PS Weighting 5m")

row_labels <- c("ATT", "ART")

# Specify your desired fontsize for labels

minor.axes.fontsize <- 16

major.axes.fontsize <- 20

png(file.path(getwd(), "images", "p_did_est_in_n_out.png"), width=1200, height=1000)

# Create a list-of-lists, where each inner list represents a row

grid_list <- list(

list(

nullGrob(),

textGrob(col_labels[1], gp = gpar(fontsize = minor.axes.fontsize)),

textGrob(col_labels[2], gp = gpar(fontsize = minor.axes.fontsize)),

textGrob(col_labels[3], gp = gpar(fontsize = minor.axes.fontsize)),

textGrob(col_labels[4], gp = gpar(fontsize = minor.axes.fontsize)),

textGrob(col_labels[5], gp = gpar(fontsize = minor.axes.fontsize))

),

list(

textGrob(row_labels[1], gp = gpar(fontsize = minor.axes.fontsize), rot = 90),

res_est_plot$mahalanobis.1lag.5m,

res_est_plot$mahalanobis.1lag.10m,

res_est_plot$ps.match.1lag.5m,

res_est_plot$ps.match.1lag.10m,

res_est_plot$ps.weight.1lag.5m

),

list(

textGrob(row_labels[2], gp = gpar(fontsize = minor.axes.fontsize), rot = 90),

res_est_plot_rev$mahalanobis.1lag.5m,

res_est_plot_rev$mahalanobis.1lag.10m,

res_est_plot_rev$ps.match.1lag.5m,

res_est_plot_rev$ps.match.1lag.10m,

res_est_plot_rev$ps.weight.1lag.5m

)

)

# "Flatten" the list-of-lists into a single list of grobs

grobs <- do.call(c, grid_list)

# Arrange your plots with text labels

grid.arrange(

grobs = grobs,

ncol = 6,

nrow = 3,

widths = c(0.1, 0.18, 0.18, 0.18, 0.18, 0.18),

heights = c(0.1, 0.45, 0.45)

)

# Add main x and y axis titles

grid.text(

"Methods",

x = 0.5,

y = 0.02,

gp = gpar(fontsize = major.axes.fontsize)

)

grid.text(

"",

x = 0.02,

y = 0.5,

rot = 90,

gp = gpar(fontsize = major.axes.fontsize)

)

dev.off()30.9.3.2 Counterfactual Estimators

- Also known as imputation approach (Liu, Wang, and Xu 2022)

- This class of estimator consider observation treatment as missing data. Models are built using data from the control units to impute conterfactuals for the treated observations.

- It’s called counterfactual estimators because they predict outcomes as if the treated observations had not received the treatment.

- Advantages:

- Avoids negative weights and biases by not using treated observations for modeling and applying uniform weights.

- Supports various models, including those that may relax strict exogeneity assumptions.

- Methods including

- Fixed-effects conterfactual estimator (FEct) (DiD is a special case):

- Based on the [Two-way Fixed-effects], where assumes linear additive functional form of unobservables based on unit and time FEs. But FEct fixes the improper weighting of TWFE by comparing within each matched pair (where each pair is the treated observation and its predicted counterfactual that is the weighted sum of all untreated observations).

- Interactive Fixed Effects conterfactual estimator (IFEct) Xu (2017):

- When we suspect unobserved time-varying confounder, FEct fails. Instead, IFEct uses the factor-augmented models to relax the strict exogeneity assumption where the effects of unobservables can be decomposed to unit FE + time FE + unit x time FE.

- Generalized Synthetic Controls are a subset of IFEct when treatments don’t revert.

- Matrix completion (MC) (Athey et al. 2021):

- Generalization of factor-augmented models. Different from IFEct which uses hard impute, MC uses soft impute to regularize the singular values when decomposing the residual matrix.

- Only when latent factors (of unobservables) are strong and sparse, IFEct outperforms MC.

- [Synthetic Controls] (case studies)

- Fixed-effects conterfactual estimator (FEct) (DiD is a special case):

Identifying Assumptions:

- Function Form: Additive separability of observables, unobservables, and idiosyncratic error term.

- Hence, these models are scale dependent (Athey and Imbens 2006) (e.g., log-transform outcome can invadiate this assumption).

- Strict Exogeneity: Conditional on observables and unobservables, potential outcomes are independent of treatment assignment (i.e., baseline quasi-randomization)

- In DiD, where unobservables = unit + time FEs, this assumption is the parallel trends assumption

- Low-dimensional Decomposition (Feasibility Assumption): Unobservable effects can be decomposed in low-dimension.

- For the case that Uit=ft×λi where ft = common time trend (time FE), and λi = unit heterogeneity (unit FE). If Uit=ft×λi , DiD can satisfy this assumption. But this assumption is weaker than that of DID, and allows us to control for unobservables based on data.

Estimation Procedure:

- Using all control observations, estimate the functions of both observable and unobservable variables (relying on Assumptions 1 and 3).

- Predict the counterfactual outcomes for each treated unit using the obtained functions.

- Calculate the difference in treatment effect for each treated individual.

- By averaging over all treated individuals, you can obtain the Average Treatment Effect on the Treated (ATT).

Notes:

- Use jackknife when number of treated units is small (Liu, Wang, and Xu 2022, 166).

30.9.3.2.1 Imputation Method

Liu, Wang, and Xu (2022) can also account for treatment reversals and heterogeneous treatment effects.

Other imputation estimators include

[@gardner2022two and @borusyak2021revisiting]

N. Brown, Butts, and Westerlund (2023)

library(fect)

PanelMatch::dem

model.fect <-

fect(

Y = "y",

D = "dem",

X = "tradewb",

data = na.omit(PanelMatch::dem),

method = "fe",

index = c("wbcode2", "year"),

se = TRUE,

parallel = TRUE,

seed = 1234,

# twfe

force = "two-way"

)

print(model.fect$est.avg)

plot(model.fect)

plot(model.fect, stats = "F.p")F-test H0: residual averages in the pre-treatment periods = 0

To see treatment reversal effects

30.9.3.2.2 Placebo Test

By selecting a part of the data and excluding observations within a specified range to improve the model fitting, we then evaluate whether the estimated Average Treatment Effect (ATT) within this range significantly differs from zero. This approach helps us analyze the periods before treatment.

If this test fails, either the functional form or strict exogeneity assumption is problematic.

30.9.3.2.3 (No) Carryover Effects Test

The placebo test can be adapted to assess carryover effects by masking several post-treatment periods instead of pre-treatment ones. If no carryover effects are present, the average prediction error should approximate zero. For the carryover test, set carryoverTest = TRUE. Specify a post-treatment period range in carryover.period to exclude observations for model fitting, then evaluate if the estimated ATT significantly deviates from zero.

Even if we have carryover effects, in most cases of the staggered adoption setting, researchers are interested in the cumulative effects, or aggregated treatment effects, so it’s okay.

out.fect.c <-

fect(

Y = "y",

D = "dem",

X = "tradewb",

data = na.omit(PanelMatch::dem),

method = "fe",

index = c("wbcode2", "year"),

se = TRUE,

carryoverTest = TRUE,

# how many periods of carryover

carryover.period = c(1, 3)

)

plot(out.fect.c, stats = "carryover.p")We have evidence of carryover effects.

30.9.3.3 Matrix Completion

Applications in marketing:

- Bronnenberg, Dubé, and Sanders (2020)

To estimate average causal effects in panel data with units exposed to treatment intermittently, two literatures are pivotal:

Unconfoundedness (G. W. Imbens and Rubin 2015): Imputes missing potential control outcomes for treated units using observed outcomes from similar control units in previous periods.

Synthetic Control (Abadie, Diamond, and Hainmueller 2010): Imputes missing control outcomes for treated units using weighted averages from control units, matching lagged outcomes between treated and control units.

Both exploit missing potential outcomes under different assumptions:

Unconfoundedness assumes time patterns are stable across units.

Synthetic control assumes unit patterns are stable over time.

Once regularization is applied, both approaches are applicable in similar settings (Athey et al. 2021).

Matrix Completion method, nesting both, is based on matrix factorization, focusing on imputing missing matrix elements assuming:

- Complete matrix = low-rank matrix + noise.

- Missingness is completely at random.

It’s distinguished by not imposing factorization restrictions but utilizing regularization to define the estimator, particularly effective with the nuclear norm as a regularizer for complex missing patterns (Athey et al. 2021).

Contributions of Athey et al. (2021) matrix completion include:

- Recognizing structured missing patterns allowing time correlation, enabling staggered adoption.

- Modifying estimators for unregularized unit and time fixed effects.

- Performing well across various T and N sizes, unlike unconfoundedness and synthetic control, which falter when T>>N or N>>T, respectively.

Identifying Assumptions:

- SUTVA: Potential outcomes indexed only by the unit’s contemporaneous treatment.

- No dynamic effects (it’s okay under staggered adoption, it gives a different interpretation of estimand).

Setup:

- Yit(0) and Yit(1) represent potential outcomes of Yit.

- Wit is a binary treatment indicator.

Aim to estimate the average effect for the treated:

τ=∑(i,t):Wit=1[Yit(1)−Yit(0)]∑i,tWit

We observe all relevant values for Yit(1)

We want to impute missing entries in the Y(0) matrix for treated units with Wit=1.

Define M as the set of pairs of indices (i,t), where i∈N and t∈T, corresponding to missing entries with Wit=1; O as the set of pairs of indices corresponding to observed entries in Y(0) with Wit=0.

Data is conceptualized as two N×T matrices, one incomplete and one complete:

Y=(Y11Y12?⋯Y1T??Y23⋯?Y31?Y33⋯?⋮⋮⋮⋱⋮YN1?YN3⋯?),

and

W=(001⋯0110⋯1010⋯1⋮⋮⋮⋱⋮010⋯1),

where

Wit={1if (i,t)∈M,0if (i,t)∈O,

is an indicator for the event that the corresponding component of Y, that is Yit, is missing.

Patterns of missing data in Y:

Block (treatment) structure with 2 special cases

Single-treated-period block structure (G. W. Imbens and Rubin 2015)

Single-treated-unit block structure (Abadie, Diamond, and Hainmueller 2010)

Staggered Adoption

Shape of matrix Y:

Thin (N>>T)

Fat (T>>N)

Square (N≈T)

Combinations of patterns of missingness and shape create different literatures:

Horizontal Regression = Thin matrix + single-treated-period block (focusing on cross-section correlation patterns)

Vertical Regression = Fat matrix + single-treated-unit block (focusing on time-series correlation patterns)

TWFE = Square matrix

To combine, we can exploit both stable patterns over time, and across units (e.g., TWFE, interactive FEs or matrix completion).

For the same factor model

Y=UVT+ϵ

where U is N×R and V is T×R

The interactive FE literature focuses on a fixed number of factors R in U,V, while matrix completion focuses on impute Y using some forms regularization (e.g., nuclear norm).

- We can also estimate the number of factors R Moon and Weidner (2015)

To use the nuclear norm minimization estimator, we must add a penalty term to regularize the objective function. However, before doing so, we need to explicitly estimate the time (λt) and unit (μi) fixed effects implicitly embedded in the missing data matrix to reduce the bias of the regularization term.

Yit=Lit+P∑p=1Q∑q=1XipHpqZqt+μi+λt+Vitβ+ϵit

where

Xip is a matrix of p variables for unit i

Zqt is a matrix of q variables for time t

Vit is a matrix of time-varying variables.

Lasso-type l1 norm (||H||=∑pp=1∑Qq=1|Hpq|) is used to shrink H→0

There are several options to regularize L:

- Frobenius (i.e., Ridge): not informative since it imputes missing values as 0.

- Nuclear Norm (i.e., Lasso): computationally feasible (using SOFT-IMPUTE algorithm (Mazumder, Hastie, and Tibshirani 2010)).

- Rank (i.e., Subset selection): not computationally feasible

This method allows to

use more covariates

leverage data from treated units (can be used when treatment effect is constant and pattern of missing is not complex).

have autocorrelated errors

have weighted loss function (i.e., take into account the probability of outcomes for a unit being missing)

30.9.4 Gardner (2022) and Borusyak, Jaravel, and Spiess (2021)

Estimate the time and unit fixed effects separately

Known as the imputation method (Borusyak, Jaravel, and Spiess 2021) or two-stage DiD (Gardner 2022)

# remotes::install_github("kylebutts/did2s")