29.9 Application

Packages:

eventstudiesererEventStudyAbnormalReturnsPerformanceAnalytics

In practice, people usually sort portfolio because they are not sure whether the FF model is specified correctly.

Steps:

- Sort all returns in CRSP into 10 deciles based on size.

- In each decile, sort returns into 10 decides based on BM

- Get the average return of the 100 portfolios for each period (i.e., expected returns of stocks given decile - characteristics)

- For each stock in the event study: Compare the return of the stock to the corresponding portfolio based on size and BM.

Notes:

Sorting produces outcomes that are often more conservative (e.g., FF abnormal returns can be greater than those that used sorting).

If the results change when we do B/M first then size or vice versa, then the results are not robust (this extends to more than just two characteristics - e.g., momentum).

Examples:

Forestry:

(Mei and Sun 2008) M&A on financial performance (forest product)

(C. Sun and Liao 2011) litigation on firm values

library(erer)

# example by the package's author

data(daEsa)

hh <- evReturn(

y = daEsa, # dataset

firm = "wpp", # firm name

y.date = "date", # date in y

index = "sp500", # index

est.win = 250, # estimation window wedith in days

digits = 3,

event.date = 19990505, # firm event dates

event.win = 5 # one-side event window wdith in days (default = 3, where 3 before + 1 event date + 3 days after = 7 days)

)

hh; plot(hh)

#>

#> === Regression coefficients by firm =========

#> N firm event.date alpha.c alpha.e alpha.t alpha.p alpha.s beta.c beta.e

#> 1 1 wpp 19990505 -0.135 0.170 -0.795 0.428 0.665 0.123

#> beta.t beta.p beta.s

#> 1 5.419 0.000 ***

#>

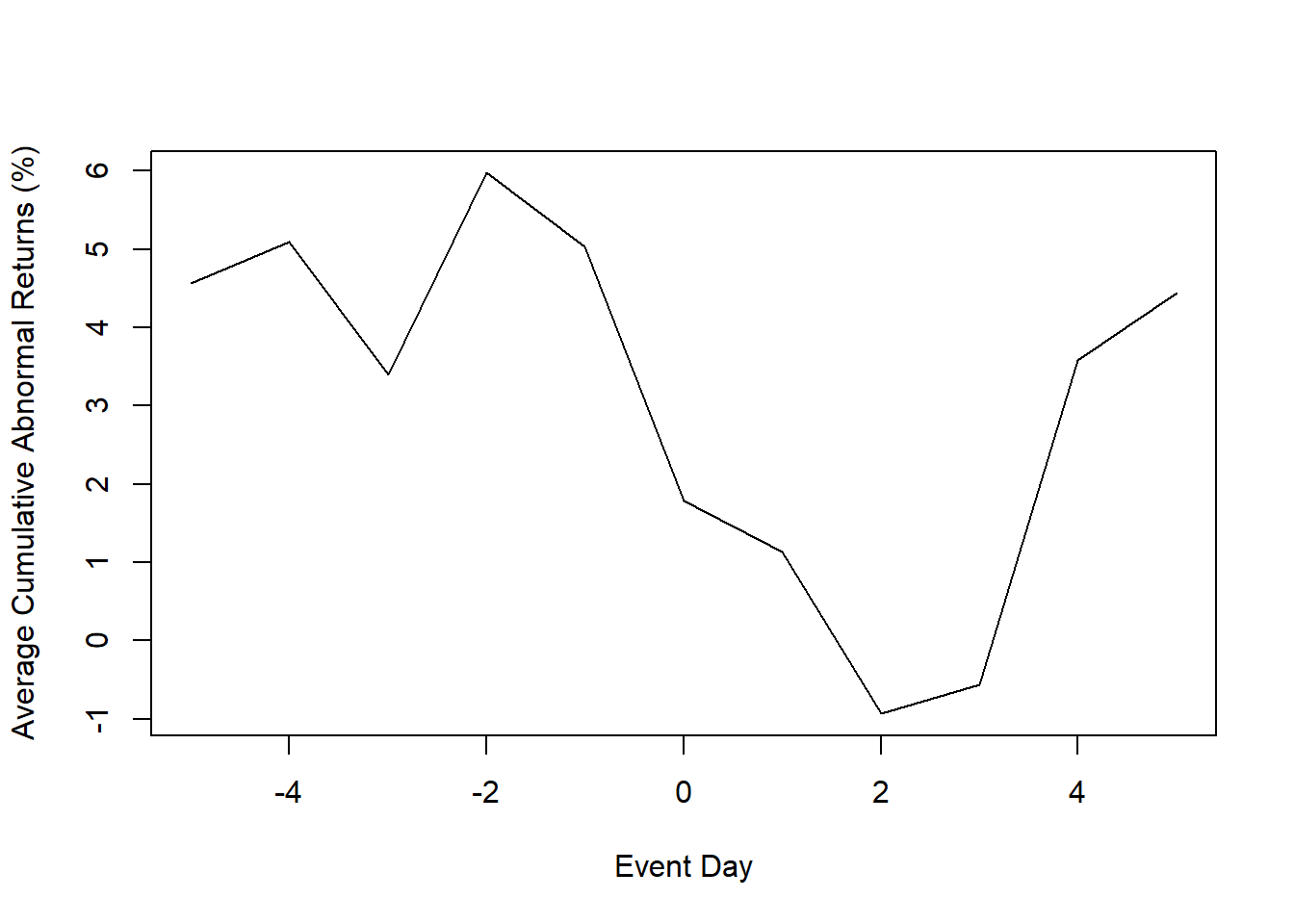

#> === Abnormal returns by date ================

#> day Ait.wpp HNt

#> 1 -5 4.564 4.564

#> 2 -4 0.534 5.098

#> 3 -3 -1.707 3.391

#> 4 -2 2.582 5.973

#> 5 -1 -0.942 5.031

#> 6 0 -3.247 1.784

#> 7 1 -0.646 1.138

#> 8 2 -2.071 -0.933

#> 9 3 0.368 -0.565

#> 10 4 4.141 3.576

#> 11 5 0.861 4.437

#>

#> === Average abnormal returns across firms ===

#> name estimate error t.value p.value sig

#> 1 CiT.wpp 4.437 8.888 0.499 0.618

#> 2 GNT 4.437 8.888 0.499 0.618

Example by Ana Julia Akaishi Padula, Pedro Albuquerque (posted on LAMFO)

Example in AbnormalReturns package

29.9.1 Eventus

2 types of output:

Using different estimation methods (e.g., market model to calendar-time approach)

Does not include event-specific returns. Hence, no regression later to determine variables that can affect abnormal stock returns.

Cross-sectional Analysis of Eventus: Event-specific abnormal returns (using monthly or data data) for cross-sectional analysis (under Cross-Sectional Analysis section)

- Since it has the stock-specific abnormal returns, we can do regression on CARs later. But it only gives market-adjusted model. However, according to (A. Sorescu, Warren, and Ertekin 2017), they advocate for the use of market-adjusted model for the short-term only, and reserve the FF4 for the longer-term event studies using monthly daily.

29.9.1.1 Basic Event Study

- Input a text file contains a firm identifier (e.g., PERMNO, CUSIP) and the event date

- Choose market indices: equally weighted and the value weighted index (i.e., weighted by their market capitalization). And check Fama-French and Carhart factors.

- Estimation options

Estimation period:

ESTLEN = 100is the convention so that the estimation is not impacted by outliers.Use “autodate” options: the first trading after the event date is used if the event falls on a weekend or holiday

- Abnormal returns window: depends on the specific event

- Choose test: either parametric (including Patell Standardized Residual (PSR)) or non-parametric

29.9.1.2 Cross-sectional Analysis of Eventus

Similar to the Basic Event Study, but now you can have event-specific abnormal returns.

29.9.2 Evenstudies

This package does not use the Fama-French model, only the market models.

This example is by the author of the package

library(eventstudies)

# firm and date data

data("SplitDates")

head(SplitDates)

# stock price data

data("StockPriceReturns")

head(StockPriceReturns)

class(StockPriceReturns)

es <-

eventstudy(

firm.returns = StockPriceReturns,

event.list = SplitDates,

event.window = 5,

type = "None",

to.remap = TRUE,

remap = "cumsum",

inference = TRUE,

inference.strategy = "bootstrap"

)

plot(es)29.9.3 EventStudy

You have to pay for the API key. (It’s $10/month).

Example by the authors of the package

Data Prep

library("Quandl")

library("quantmod")

Quandl.auth("LDqWhYXzVd2omw4zipN2")

TWTR <- Quandl("NSE/OIL",type ="xts")

candleChart(TWTR)

Reference market in Germany is DAX

# Index Data

# indexName <- c("DAX")

indexData <- tq_get("^GDAXI", from = "2014-05-01", to = "2015-12-31") %>%

mutate(date = format(date, "%d.%m.%Y")) %>%

mutate(symbol = "DAX")

head(indexData)Create files

01_RequestFile.csv02_FirmData.csv03_MarketData.csv

Calculating abnormal returns

# get & set parameters for abnormal return Event Study

# we use a garch model and csv as return

# Attention: fitting a GARCH(1, 1) model is compute intensive

esaParams <- EventStudy::ARCApplicationInput$new()

esaParams$setResultFileType("csv")

esaParams$setBenchmarkModel("garch")

dataFiles <-

c(

"request_file" = file.path(getwd(), "data", "EventStudy", "01_requestFile.csv"),

"firm_data" = file.path(getwd(), "data", "EventStudy", "02_firmDataPrice.csv"),

"market_data" = file.path(getwd(), "data", "EventStudy", "03_marketDataPrice.csv")

)

# check data files, you can do it also in our R6 class

EventStudy::checkFiles(dataFiles)arEventStudy <- estSetup$performEventStudy(estParams = esaParams,

dataFiles = dataFiles,

downloadFiles = T)library(EventStudy)

apiUrl <- "https://api.eventstudytools.com"

Sys.setenv(EventStudyapiKey = "")

# The URL is already set by default

options(EventStudy.URL = apiUrl)

options(EventStudy.KEY = Sys.getenv("EventStudyapiKey"))

# use EventStudy estAPIKey function

estAPIKey(Sys.getenv("EventStudyapiKey"))

# initialize object

estSetup <- EventStudyAPI$new()

estSetup$authentication(apiKey = Sys.getenv("EventStudyapiKey"))