28 Synthetic Control

Examples in marketing:

- (Tirunillai and Tellis 2017): offline TV ad on Online Chatter

- (Yanwen Wang, Wu, and Zhu 2019): mobile hailing technology adoption on drivers’ hourly earnings

- (Guo, Sriram, and Manchanda 2020): payment disclosure laws effect on physician prescription behavior using Timing of the Massachusetts open payment law as the exogenous shock

- (Adalja et al. 2023): mandatory GMO labels had no impact on consumer demand (Using Vermont as a mandatory state)

Notes

The SC method provides asymptotically normal estimators for various linear panel data models, given sufficiently large pre-treatment periods, making it a natural alternative to the Difference-in-differences model (Arkhangelsky and Hirshberg 2023).

SCM is superior than Matching Methods because it not only matches on covariates (i.e., pre-treatment variables), but also outcomes.

For a review of the method, see (Abadie 2021)

SCMs can also be used under the Bayesian framework (Bayesian Synthetic Control) where we do not have to impose any restrictive priori (S. Kim, Lee, and Gupta 2020)

Different from Matching Methods because SCMs match on the pre-treatment outcomes in each period while Matching Methods match on the number of covariates.

A data driven procedure to construct more comparable control groups (i.e., black box).

To do causal inference with control and treatment group using Matching Methods, you typically have to have similar covariates in the control and the treated groups. However, if you don’t methods like Propensity Scores and DID can perform rather poorly (i.e., large bias).

Advantages over Difference-in-differences

- Maximization of the observable similarity between control and treatment (maybe also unobservables)

- Can also be used in cases where no untreated case with similar on matching dimensions with treated cases

- Objective selection of controls.

Advantages over linear regression

Regression weights for the estimator will be outside of [0,1] (because regression allows extrapolation), and it will not be sparse (i.e., can be less than 0).

No extrapolation under SCMs

Explicitly state the fit (i.e., the weight)

Can be estimated without the post-treatment outcomes for the control group (can’t p-hack)

Advantages:

- From the selection criteria, researchers can understand the relative importance of each candidate

- Post-intervention outcomes are not used in synthetic. Hence, you can’t retro-fit.

- Observable similarity between control and treatment cases is maximized

Disadvantages:

- It’s hard to argue for the weights you use to create the “synthetic control”

SCM is recommended when

- Social events to evaluate large-scale program or policy

- Only one treated case with several control candidates.

Assumptions

Donor subject is a good match for the synthetic control (i.e., gap between the dependent of the donor subject and that of the synthetic control should be 0 before treatment)

Only the treated subject undergoes the treatment and not any of the subjects in the donor pool.

No other changes to the subjects during the whole window.

The counterfactual outcome of the treatment group can be imputed in a linear combination of control groups.

Identification: The exclusion restriction is met conditional on the pre-treatment outcomes.

Synth provides an algorithm that finds weighted combination of the comparison units where the weights are chosen such that it best resembles the values of predictors of the outcome variable for the affected units before the intervention

Setting (notation followed professor Alberto Abadie)

\(J + 1\) units in periods \(1, \dots, T\)

The first unit is the treated one during \(T_0 + 1, \dots, T\)

\(J\) units are called a donor pool

\(Y_{it}^I\) is the outcome for unit \(i\) if it’s exposed to the treatment during \(T_0 + 1 , \dots T\)

\(Y_{it}^N\) is the outcome for unit \(i\) if it’s not exposed to the treatment

We try to estimate the effect of treatment on the treated unit

\[ \tau_{1t} = Y_{1t}^I - Y_{1t}^N \]

where we observe the first treated unit already \(Y_{1t}^I = Y_{1t}\)

To construct the synthetic control unit, we have to find appropriate weight for each donor in the donor pool by finding \(\mathbf{W} = (w_2, \dots, w_{J=1})'\) where

\(w_j \ge 0\) for \(j = 2, \dots, J+1\)

\(w_2 + \dots + w_{J+1} = 1\)

The “appropriate” vector \(\mathbf{W}\) here is constrained to

\[ \min||\mathbf{X}_1 - \mathbf{X}_0 \mathbf{W}|| \]

where

\(\mathbf{X}_1\) is the \(k \times 1\) vector of pre-treatment characteristics for the treated unit

\(\mathbf{X}_0\) is the \(k \times J\) matrix of pre-treatment characteristics for the untreated units

For simplicity, researchers usually use

\[ \begin{aligned} &\min||\mathbf{X}_1 - \mathbf{X}_0 \mathbf{W}|| \\ &= (\sum_{h=1}^k v_h(X_{h1}- w_2 X-{h2} - \dots - w_{J+1} X_{hJ +1})^{1/2} \end{aligned} \]

where

- \(v_1, \dots, v_k\) is a vector positive constants that represent the predictive power of the \(k\) predictors on \(Y_{1t}^N\) (i.e., the potential outcome of the treated without treatment) and it can be chosen either explicitly by the researcher or by data-driven methods

For penalized synthetic control (Abadie and L’hour 2021), the minimization problem becomes

\[ \min_{\mathbf{W}} ||\mathbf{X}_1 - \sum_{j=2}^{J + 1}W_j \mathbf{X}_j ||^2 + \lambda \sum_{j=2}^{J+1} W_j ||\mathbf{X}_1 - \mathbf{X}_j||^2 \]

where

\(W_j \ge 0\) and \(\sum_{j=2}^{J+1} W_j = 1\)

-

\(\lambda >0\) balances over-fitting of the treated and minimize the sum of pairwise distances

\(\lambda \to 0\): pure synthetic control (i.e solution for the unpenalized estimator)

\(\lambda \to \infty\): nearest neighbor matching

Advantages:

For \(\lambda >0\), you have unique and sparse solution

Reduces the interpolation bias when averaging dissimilar units

Penalized SC never uses dissimilar units

Then the synthetic control estimator is

\[ \hat{\tau}_{1t} = Y_{1t} - \sum_{j=2}^{J+1} w_j^* Y_{jt} \]

where \(Y_{jt}\) is the outcome for unit \(j\) at time \(t\)

Consideration

Under the factor model (Abadie, Diamond, and Hainmueller 2010)

\[ Y_{it}^N = \mathbf{\theta}_t \mathbf{Z}_i + \mathbf{\lambda}_t \mathbf{\mu}_i + \epsilon_{it} \]

where

\(Z_i\) = observables

\(\mu_i\) = unobservables

\(\epsilon_{it}\) = unit-level transitory shock (i.e., random noise)

with assumptions of \(\mathbf{W}^*\) such that

\[ \begin{aligned} \sum_{j=2}^{J+1} w_j^* \mathbf{Z}_j &= \mathbf{Z}_1 \\ &\dots \\ \sum_{j=2}^{J+1} w_j^* Y_{j1} &= Y_{11} \\ \sum_{j=2}^{J+1} w_j^* Y_{jT_0} &= Y_{1T_0} \end{aligned} \]

Basically, we assume that the synthetic control is a good counterfactual when the treated unit is not exposed to the treatment.

Then,

the bias bound depends on close fit, which is controlled by the ratio between \(\epsilon_{it}\) (transitory shock) and \(T_0\) (the number of pre-treatment periods). In other words, you should have good fit for \(Y_{1t}\) for pre-treatment period (i.e., \(T_0\) should be large while small variance in \(\epsilon_{it}\))

When you have poor fit, you have to use bias correction version of the synthetic control. See Ben-Michael, Feller, and Rothstein (2020)

-

Overfitting can be the result of small \(T_0\) (the number of pre-treatment periods), large \(J\) (the number of units in the donor pool), and large \(\epsilon_{it}\) (noise)

- Mitigation: put only similar units (to the treated one) in the donor pool

To make inference, we have to create a permutation distribution (by iteratively reassigning the treatment to the units in the donor pool and estimate the placebo effects in each iteration). We say there is an effect of the treatment when the magnitude of value of the treatment effect on the treated unit is extreme relative to the permutation distribution.

It’s recommended to use one-sided inference. And the permutation distribution is superior to the p-values alone (because sampling-based inference is hard under SCMs either because of undefined sampling mechanism or the sample is the population).

For benchmark (permutation) distribution (e.g., uniform), see (Firpo and Possebom 2018)

28.1 Applications

28.1.1 Example 1

simulate data for 10 states and 30 years. State A receives the treatment T = 20 after year 15.

set.seed(1)

year <- rep(1:30, 10)

state <- rep(LETTERS[1:10], each = 30)

X1 <- round(rnorm(300, mean = 2, sd = 1), 2)

X2 <- round(rbinom(300, 1, 0.5) + rnorm(300), 2)

Y <- round(1 + 2 * X1 + rnorm(300), 2)

df <- as.data.frame(cbind(Y, X1, X2, state, year))

df$Y <- as.numeric(as.character(df$Y))

df$X1 <- as.numeric(as.character(df$X1))

df$X2 <- as.numeric(as.character(df$X2))

df$year <- as.numeric(as.character(df$year))

df$state.num <- rep(1:10, each = 30)

df$state <- as.character(df$state)

df$`T` <- ifelse(df$state == "A" & df$year >= 15, 1, 0)

df$Y <- ifelse(df$state == "A" & df$year >= 15,

df$Y + 20, df$Y)

str(df)

#> 'data.frame': 300 obs. of 7 variables:

#> $ Y : num 2.29 4.51 2.07 8.87 4.37 1.32 8 7.49 6.98 3.72 ...

#> $ X1 : num 1.37 2.18 1.16 3.6 2.33 1.18 2.49 2.74 2.58 1.69 ...

#> $ X2 : num 1.96 0.4 -0.75 -0.56 -0.45 1.06 0.51 -2.1 0 0.54 ...

#> $ state : chr "A" "A" "A" "A" ...

#> $ year : num 1 2 3 4 5 6 7 8 9 10 ...

#> $ state.num: int 1 1 1 1 1 1 1 1 1 1 ...

#> $ T : num 0 0 0 0 0 0 0 0 0 0 ...

dataprep.out <-

dataprep(

df,

predictors = c("X1", "X2"),

dependent = "Y",

unit.variable = "state.num",

time.variable = "year",

unit.names.variable = "state",

treatment.identifier = 1,

controls.identifier = c(2:10),

time.predictors.prior = c(1:14),

time.optimize.ssr = c(1:14),

time.plot = c(1:30)

)

synth.out <- synth(dataprep.out)

#>

#> X1, X0, Z1, Z0 all come directly from dataprep object.

#>

#>

#> ****************

#> searching for synthetic control unit

#>

#>

#> ****************

#> ****************

#> ****************

#>

#> MSPE (LOSS V): 9.831789

#>

#> solution.v:

#> 0.3888387 0.6111613

#>

#> solution.w:

#> 0.1115941 0.1832781 0.1027237 0.312091 0.06096758 0.03509706 0.05893735 0.05746256 0.07784853

print(synth.tables <- synth.tab(

dataprep.res = dataprep.out,

synth.res = synth.out)

)

#> $tab.pred

#> Treated Synthetic Sample Mean

#> X1 2.028 2.028 2.017

#> X2 0.513 0.513 0.394

#>

#> $tab.v

#> v.weights

#> X1 0.389

#> X2 0.611

#>

#> $tab.w

#> w.weights unit.names unit.numbers

#> 2 0.112 B 2

#> 3 0.183 C 3

#> 4 0.103 D 4

#> 5 0.312 E 5

#> 6 0.061 F 6

#> 7 0.035 G 7

#> 8 0.059 H 8

#> 9 0.057 I 9

#> 10 0.078 J 10

#>

#> $tab.loss

#> Loss W Loss V

#> [1,] 9.761708e-12 9.831789

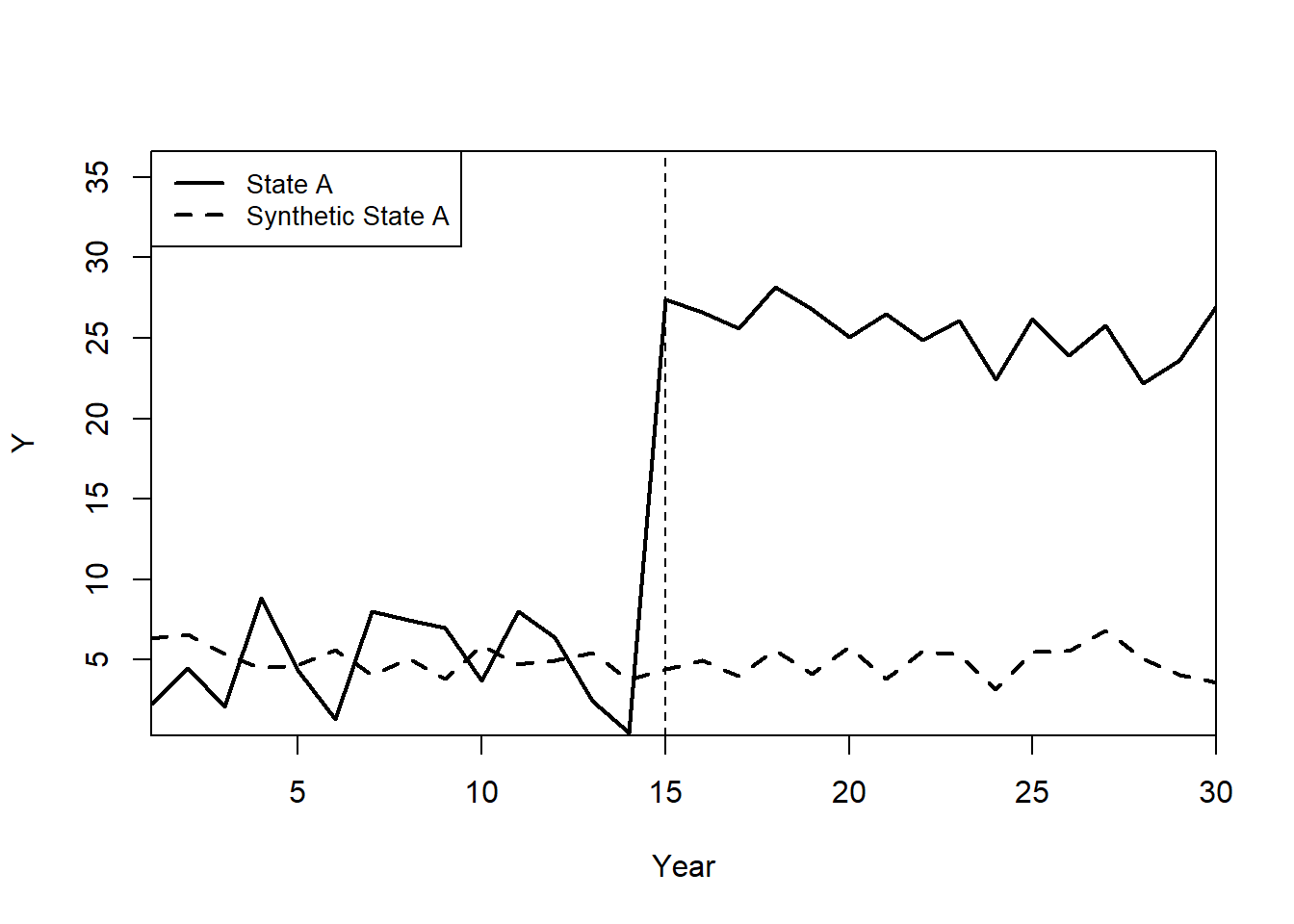

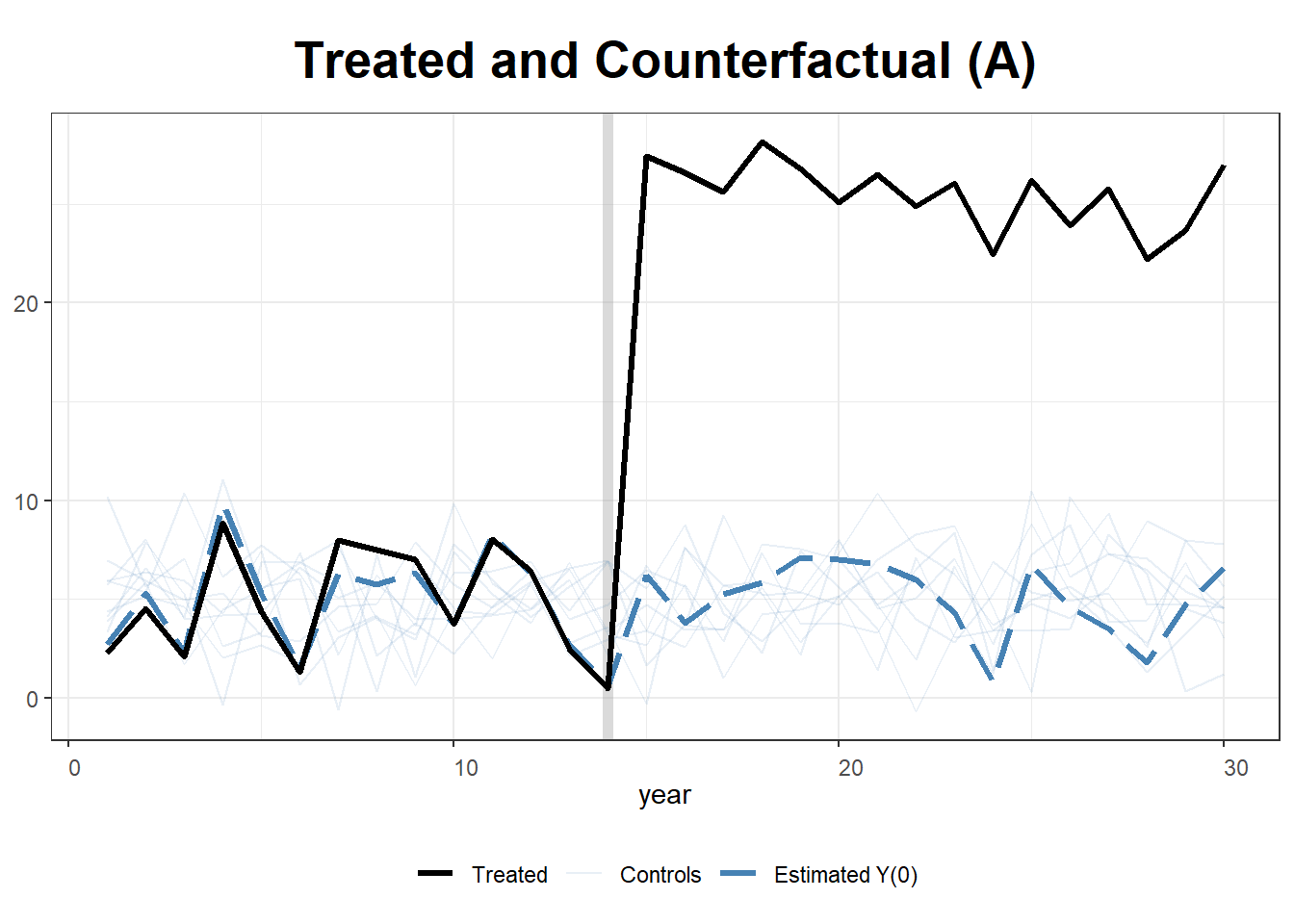

path.plot(synth.res = synth.out,

dataprep.res = dataprep.out,

Ylab = c("Y"),

Xlab = c("Year"),

Legend = c("State A","Synthetic State A"),

Legend.position = c("topleft")

)

abline(v = 15,

lty = 2)

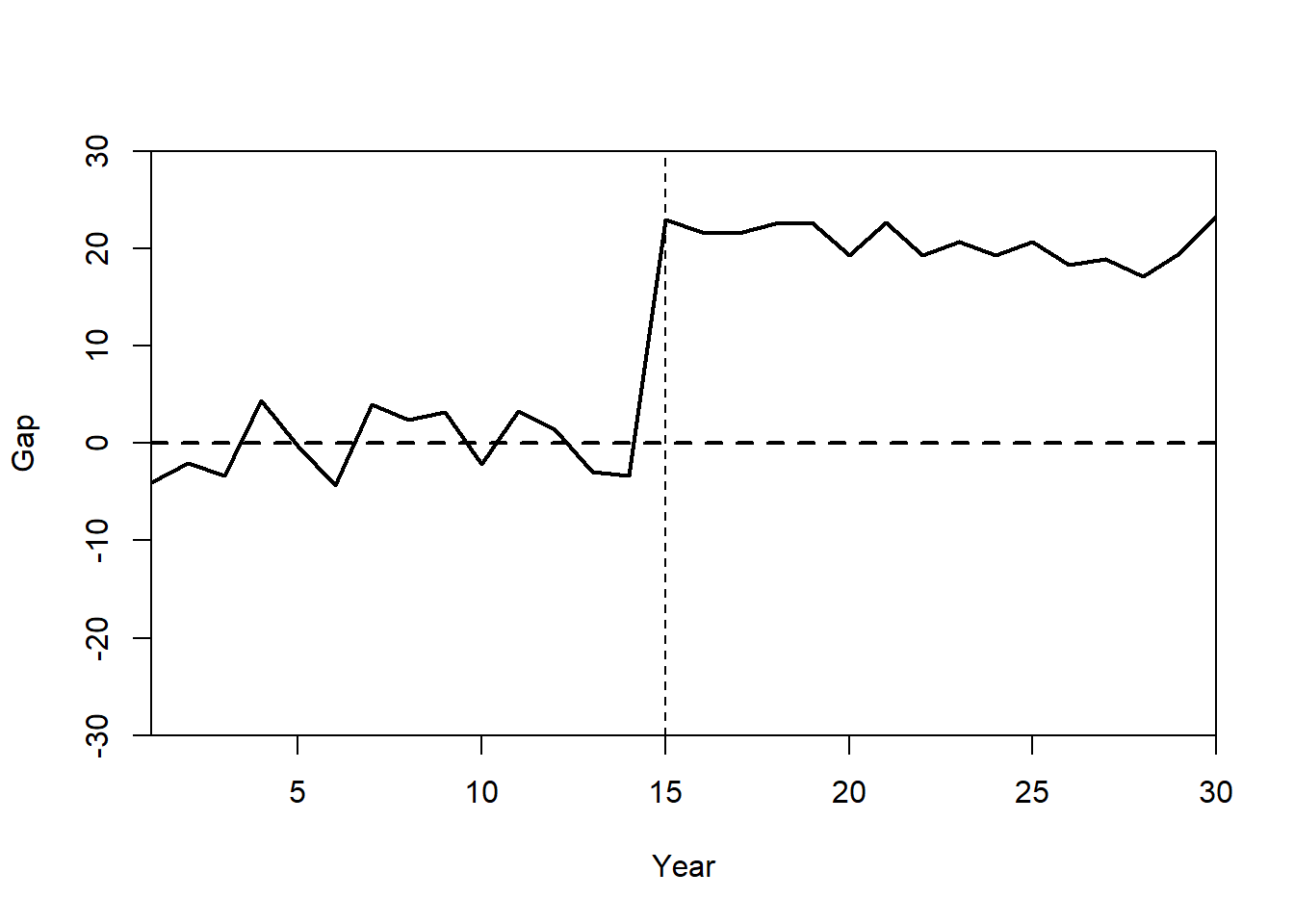

Gaps plot:

gaps.plot(synth.res = synth.out,

dataprep.res = dataprep.out,

Ylab = c("Gap"),

Xlab = c("Year"),

Ylim = c(-30, 30),

Main = ""

)

abline(v = 15,

lty = 2)

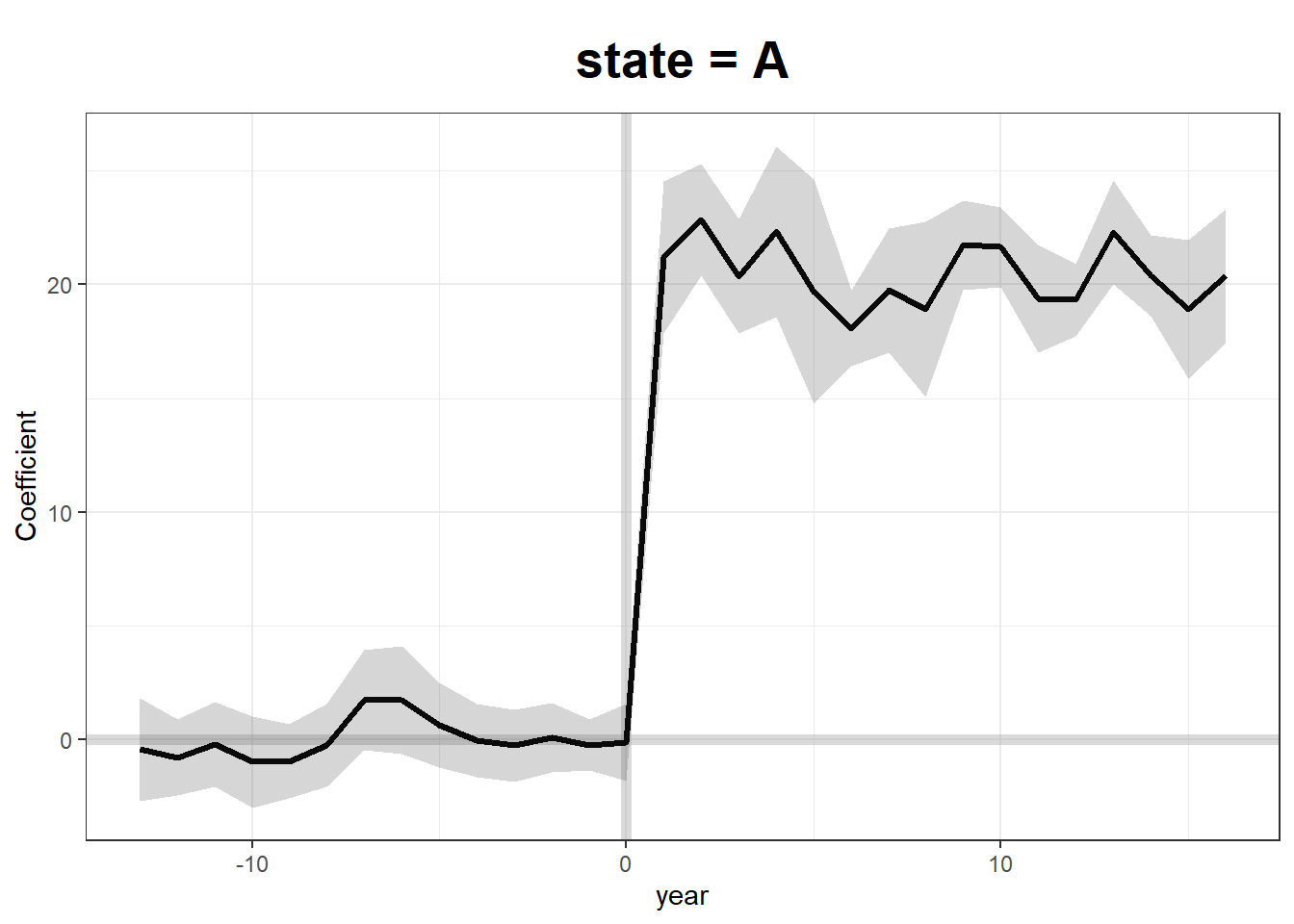

Alternatively, gsynth provides options to estimate iterative fixed effects, and handle multiple treated units at tat time.

Here, we use two=way fixed effects and bootstrapped standard errors

gsynth.out <- gsynth(

Y ~ `T` + X1 + X2,

data = df,

index = c("state", "year"),

force = "two-way",

CV = TRUE,

r = c(0, 5),

se = TRUE,

inference = "parametric",

nboots = 1000,

parallel = F # TRUE

)

#> Cross-validating ...

#> r = 0; sigma2 = 1.13533; IC = 0.95632; PC = 0.96713; MSPE = 1.65502

#> r = 1; sigma2 = 0.96885; IC = 1.54420; PC = 4.30644; MSPE = 1.33375

#> r = 2; sigma2 = 0.81855; IC = 2.08062; PC = 6.58556; MSPE = 1.27341*

#> r = 3; sigma2 = 0.71670; IC = 2.61125; PC = 8.35187; MSPE = 1.79319

#> r = 4; sigma2 = 0.62823; IC = 3.10156; PC = 9.59221; MSPE = 2.02301

#> r = 5; sigma2 = 0.55497; IC = 3.55814; PC = 10.48406; MSPE = 2.79596

#>

#> r* = 2

#>

#>

Simulating errors .............

Bootstrapping ...

#> ..........

plot(gsynth.out)

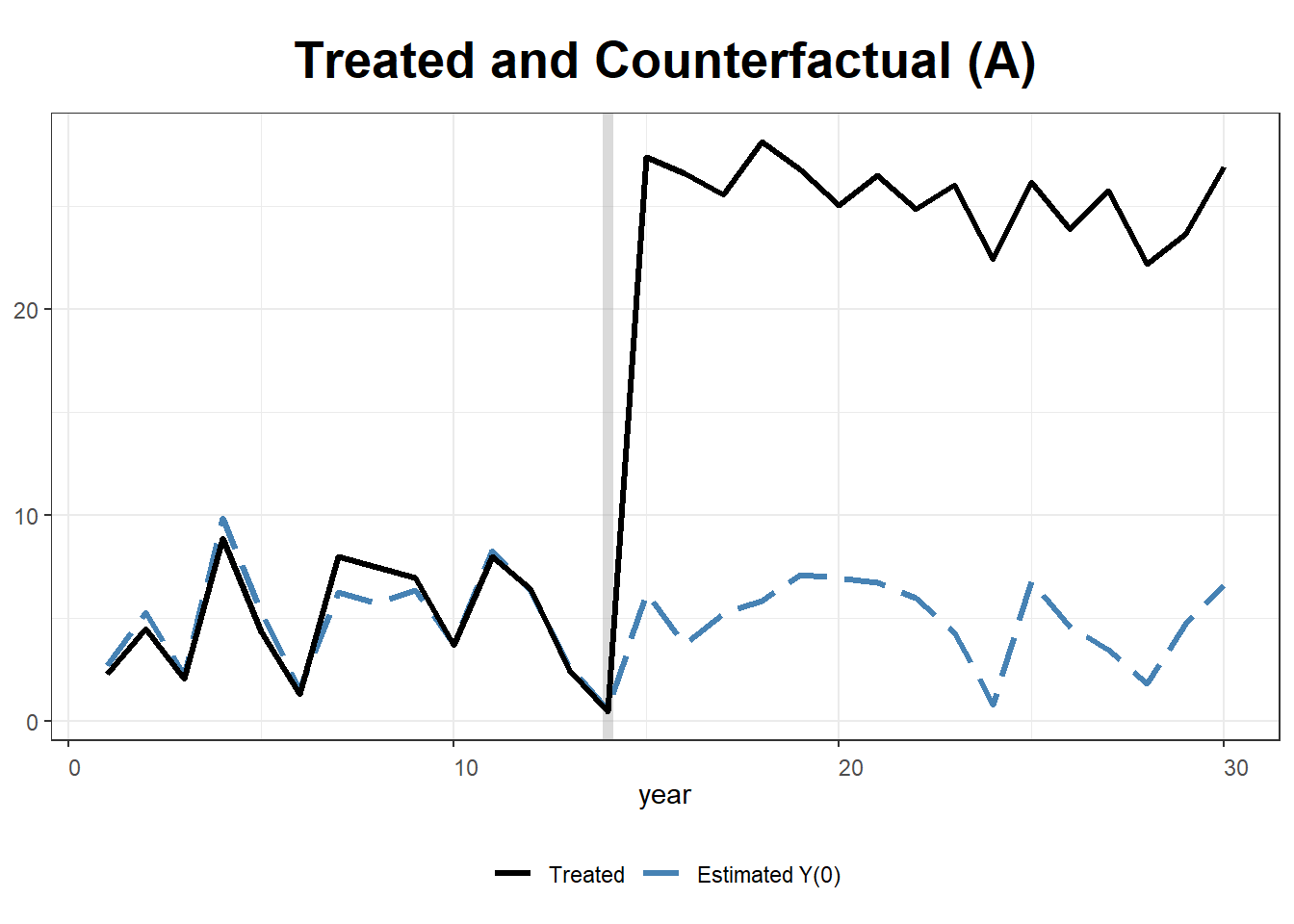

plot(gsynth.out, type = "counterfactual")

plot(gsynth.out, type = "counterfactual", raw = "all")

# shows estimations for the control cases28.1.2 Example 2

by Leihua Ye

library(Synth)

data("basque")

dim(basque) #774*17

#> [1] 774 17

head(basque)

#> regionno regionname year gdpcap sec.agriculture sec.energy sec.industry

#> 1 1 Spain (Espana) 1955 2.354542 NA NA NA

#> 2 1 Spain (Espana) 1956 2.480149 NA NA NA

#> 3 1 Spain (Espana) 1957 2.603613 NA NA NA

#> 4 1 Spain (Espana) 1958 2.637104 NA NA NA

#> 5 1 Spain (Espana) 1959 2.669880 NA NA NA

#> 6 1 Spain (Espana) 1960 2.869966 NA NA NA

#> sec.construction sec.services.venta sec.services.nonventa school.illit

#> 1 NA NA NA NA

#> 2 NA NA NA NA

#> 3 NA NA NA NA

#> 4 NA NA NA NA

#> 5 NA NA NA NA

#> 6 NA NA NA NA

#> school.prim school.med school.high school.post.high popdens invest

#> 1 NA NA NA NA NA NA

#> 2 NA NA NA NA NA NA

#> 3 NA NA NA NA NA NA

#> 4 NA NA NA NA NA NA

#> 5 NA NA NA NA NA NA

#> 6 NA NA NA NA NA NAtransform data to be used in synth()

dataprep.out <- dataprep(

foo = basque,

predictors = c(

"school.illit",

"school.prim",

"school.med",

"school.high",

"school.post.high",

"invest"

),

predictors.op = "mean",

# the operator

time.predictors.prior = 1964:1969,

#the entire time frame from the #beginning to the end

special.predictors = list(

list("gdpcap", 1960:1969, "mean"),

list("sec.agriculture", seq(1961, 1969, 2), "mean"),

list("sec.energy", seq(1961, 1969, 2), "mean"),

list("sec.industry", seq(1961, 1969, 2), "mean"),

list("sec.construction", seq(1961, 1969, 2), "mean"),

list("sec.services.venta", seq(1961, 1969, 2), "mean"),

list("sec.services.nonventa", seq(1961, 1969, 2), "mean"),

list("popdens", 1969, "mean")

),

dependent = "gdpcap",

# dv

unit.variable = "regionno",

#identifying unit numbers

unit.names.variable = "regionname",

#identifying unit names

time.variable = "year",

#time-periods

treatment.identifier = 17,

#the treated case

controls.identifier = c(2:16, 18),

#the control cases; all others #except number 17

time.optimize.ssr = 1960:1969,

#the time-period over which to optimize

time.plot = 1955:1997

) #the entire time period before/after the treatmentwhere

\(X_1\) = the control case before the treatment

\(X_0\) = the control cases after the treatment

\(Z_1\): the treatment case before the treatment

\(Z_0\): the treatment case after the treatment

synth.out = synth(data.prep.obj = dataprep.out, method = "BFGS")

#>

#> X1, X0, Z1, Z0 all come directly from dataprep object.

#>

#>

#> ****************

#> searching for synthetic control unit

#>

#>

#> ****************

#> ****************

#> ****************

#>

#> MSPE (LOSS V): 0.008864606

#>

#> solution.v:

#> 0.02773094 1.194e-07 1.60609e-05 0.0007163836 1.486e-07 0.002423908 0.0587055 0.2651997 0.02851006 0.291276 0.007994382 0.004053188 0.009398579 0.303975

#>

#> solution.w:

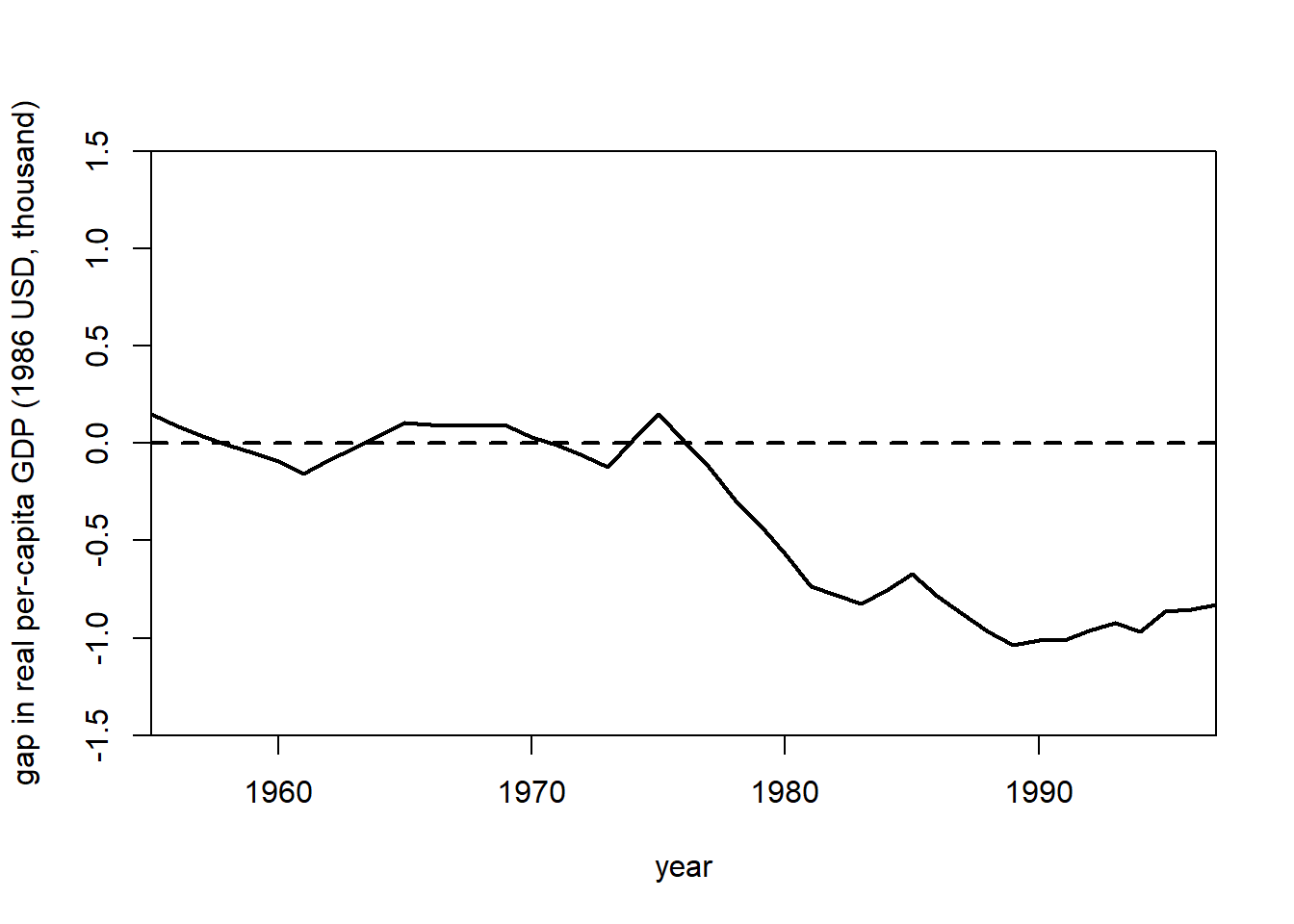

#> 2.53e-08 4.63e-08 6.44e-08 2.81e-08 3.37e-08 4.844e-07 4.2e-08 4.69e-08 0.8508145 9.75e-08 3.2e-08 5.54e-08 0.1491843 4.86e-08 9.89e-08 1.162e-07Calculate the difference between the real basque region and the synthetic control

gaps = dataprep.out$Y1plot - (dataprep.out$Y0plot

%*% synth.out$solution.w)

gaps[1:3,1]

#> 1955 1956 1957

#> 0.15023473 0.09168035 0.03716475

synth.tables = synth.tab(dataprep.res = dataprep.out,

synth.res = synth.out)

names(synth.tables)

#> [1] "tab.pred" "tab.v" "tab.w" "tab.loss"

synth.tables$tab.pred[1:13,]

#> Treated Synthetic Sample Mean

#> school.illit 39.888 256.337 170.786

#> school.prim 1031.742 2730.104 1127.186

#> school.med 90.359 223.340 76.260

#> school.high 25.728 63.437 24.235

#> school.post.high 13.480 36.153 13.478

#> invest 24.647 21.583 21.424

#> special.gdpcap.1960.1969 5.285 5.271 3.581

#> special.sec.agriculture.1961.1969 6.844 6.179 21.353

#> special.sec.energy.1961.1969 4.106 2.760 5.310

#> special.sec.industry.1961.1969 45.082 37.636 22.425

#> special.sec.construction.1961.1969 6.150 6.952 7.276

#> special.sec.services.venta.1961.1969 33.754 41.104 36.528

#> special.sec.services.nonventa.1961.1969 4.072 5.371 7.111Relative importance of each unit

synth.tables$tab.w[8:14, ]

#> w.weights unit.names unit.numbers

#> 9 0.000 Castilla-La Mancha 9

#> 10 0.851 Cataluna 10

#> 11 0.000 Comunidad Valenciana 11

#> 12 0.000 Extremadura 12

#> 13 0.000 Galicia 13

#> 14 0.149 Madrid (Comunidad De) 14

#> 15 0.000 Murcia (Region de) 15

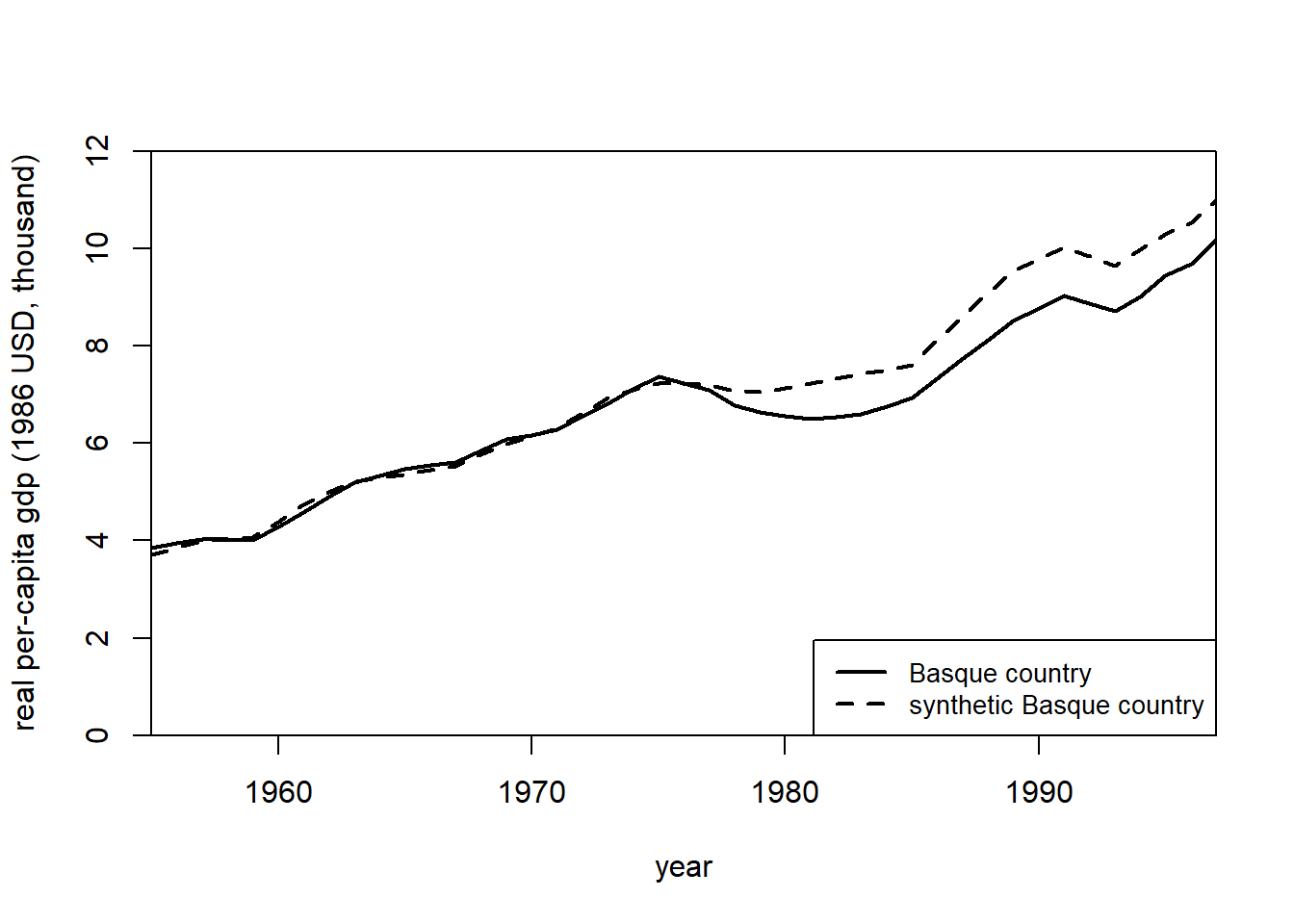

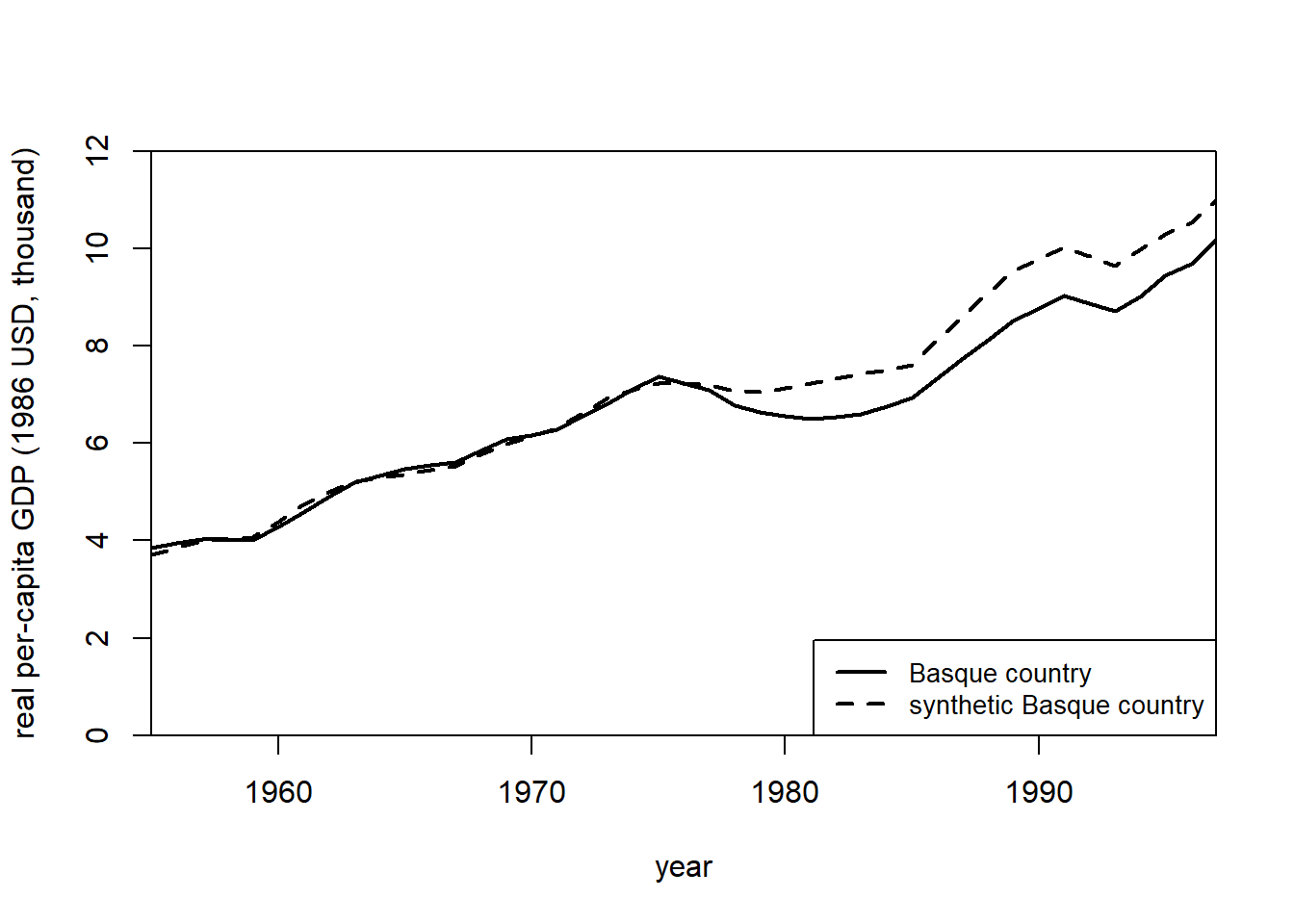

# plot the changes before and after the treatment

path.plot(

synth.res = synth.out,

dataprep.res = dataprep.out,

Ylab = "real per-capita gdp (1986 USD, thousand)",

Xlab = "year",

Ylim = c(0, 12),

Legend = c("Basque country",

"synthetic Basque country"),

Legend.position = "bottomright"

)

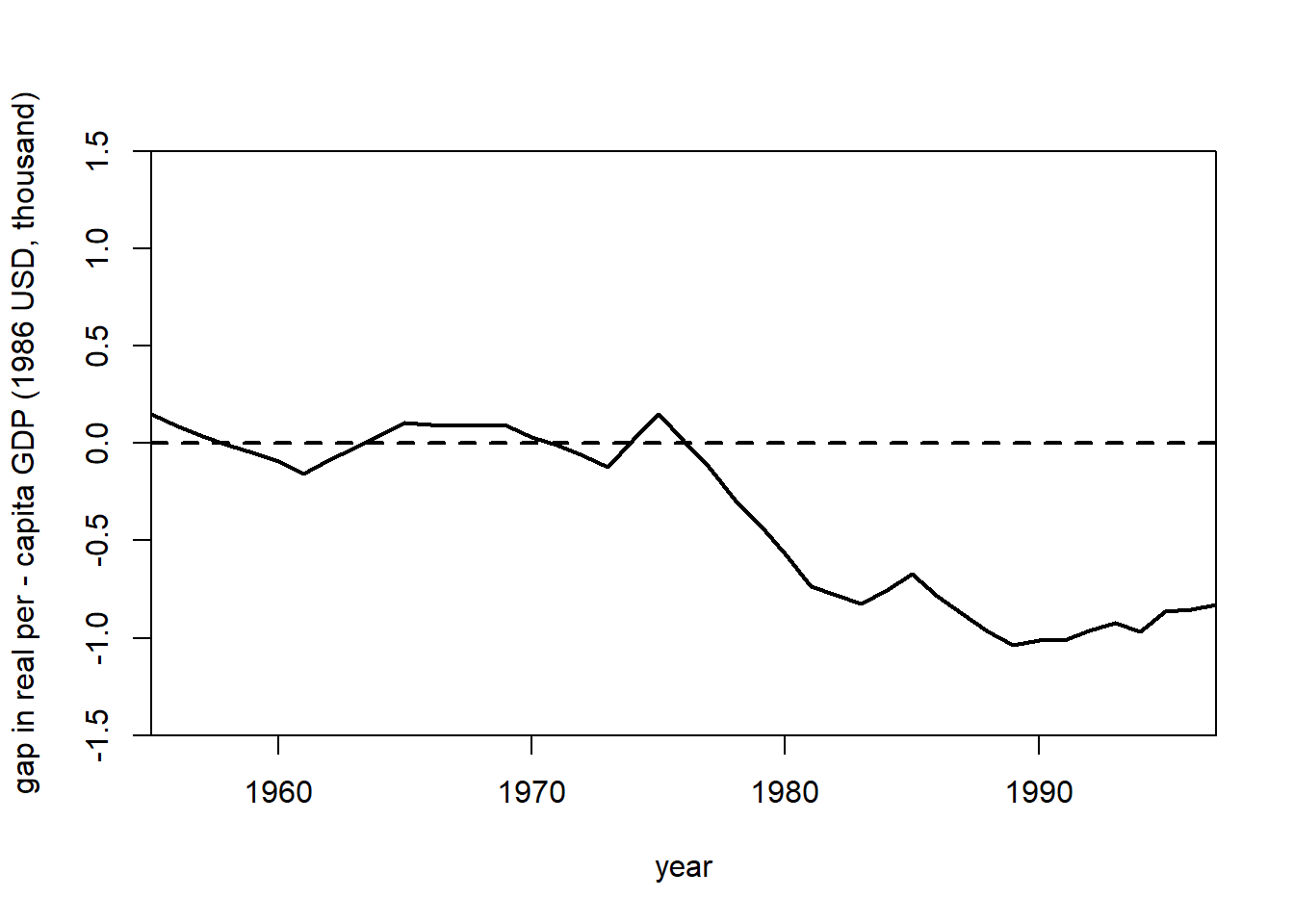

gaps.plot(

synth.res = synth.out,

dataprep.res = dataprep.out,

Ylab = "gap in real per - capita GDP (1986 USD, thousand)",

Xlab = "year",

Ylim = c(-1.5, 1.5),

Main = NA

)

Doubly Robust Difference-in-Differences

Example from DRDID package

library(DRDID)

data(nsw_long)

# Form the Lalonde sample with CPS comparison group

eval_lalonde_cps <- subset(nsw_long, nsw_long$treated == 0 |

nsw_long$sample == 2)Estimate Average Treatment Effect on Treated using Improved Locally Efficient Doubly Robust DID estimator

out <-

drdid(

yname = "re",

tname = "year",

idname = "id",

dname = "experimental",

xformla = ~ age + educ + black + married + nodegree + hisp + re74,

data = eval_lalonde_cps,

panel = TRUE

)

summary(out)

#> Call:

#> drdid(yname = "re", tname = "year", idname = "id", dname = "experimental",

#> xformla = ~age + educ + black + married + nodegree + hisp +

#> re74, data = eval_lalonde_cps, panel = TRUE)

#> ------------------------------------------------------------------

#> Further improved locally efficient DR DID estimator for the ATT:

#>

#> ATT Std. Error t value Pr(>|t|) [95% Conf. Interval]

#> -901.2703 393.6247 -2.2897 0.022 -1672.7747 -129.766

#> ------------------------------------------------------------------

#> Estimator based on panel data.

#> Outcome regression est. method: weighted least squares.

#> Propensity score est. method: inverse prob. tilting.

#> Analytical standard error.

#> ------------------------------------------------------------------

#> See Sant'Anna and Zhao (2020) for details.28.1.3 Example 3

by Synth package’s authors

synth() requires

\(X_1\) vector of treatment predictors

\(X_0\) matrix of same variables for control group

\(Z_1\) vector of outcome variable for treatment group

\(Z_0\) matrix of outcome variable for control group

use dataprep() to prepare data in the format that can be used throughout the Synth package

dataprep.out <- dataprep(

foo = basque,

predictors = c(

"school.illit",

"school.prim",

"school.med",

"school.high",

"school.post.high",

"invest"

),

predictors.op = "mean",

time.predictors.prior = 1964:1969,

special.predictors = list(

list("gdpcap", 1960:1969 , "mean"),

list("sec.agriculture", seq(1961, 1969, 2), "mean"),

list("sec.energy", seq(1961, 1969, 2), "mean"),

list("sec.industry", seq(1961, 1969, 2), "mean"),

list("sec.construction", seq(1961, 1969, 2), "mean"),

list("sec.services.venta", seq(1961, 1969, 2), "mean"),

list("sec.services.nonventa", seq(1961, 1969, 2), "mean"),

list("popdens", 1969, "mean")

),

dependent = "gdpcap",

unit.variable = "regionno",

unit.names.variable = "regionname",

time.variable = "year",

treatment.identifier = 17,

controls.identifier = c(2:16, 18),

time.optimize.ssr = 1960:1969,

time.plot = 1955:1997

)find optimal weights that identifies the synthetic control for the treatment group

synth.out <- synth(data.prep.obj = dataprep.out, method = "BFGS")

#>

#> X1, X0, Z1, Z0 all come directly from dataprep object.

#>

#>

#> ****************

#> searching for synthetic control unit

#>

#>

#> ****************

#> ****************

#> ****************

#>

#> MSPE (LOSS V): 0.008864606

#>

#> solution.v:

#> 0.02773094 1.194e-07 1.60609e-05 0.0007163836 1.486e-07 0.002423908 0.0587055 0.2651997 0.02851006 0.291276 0.007994382 0.004053188 0.009398579 0.303975

#>

#> solution.w:

#> 2.53e-08 4.63e-08 6.44e-08 2.81e-08 3.37e-08 4.844e-07 4.2e-08 4.69e-08 0.8508145 9.75e-08 3.2e-08 5.54e-08 0.1491843 4.86e-08 9.89e-08 1.162e-07

gaps <- dataprep.out$Y1plot - (dataprep.out$Y0plot %*% synth.out$solution.w)

gaps[1:3, 1]

#> 1955 1956 1957

#> 0.15023473 0.09168035 0.03716475

synth.tables <-

synth.tab(dataprep.res = dataprep.out, synth.res = synth.out)

names(synth.tables) # you can pick tables to see

#> [1] "tab.pred" "tab.v" "tab.w" "tab.loss"

path.plot(

synth.res = synth.out,

dataprep.res = dataprep.out,

Ylab = "real per-capita GDP (1986 USD, thousand)",

Xlab = "year",

Ylim = c(0, 12),

Legend = c("Basque country",

"synthetic Basque country"),

Legend.position = "bottomright"

)

gaps.plot(

synth.res = synth.out,

dataprep.res = dataprep.out,

Ylab = "gap in real per-capita GDP (1986 USD, thousand)",

Xlab = "year",

Ylim = c(-1.5, 1.5),

Main = NA

)

You could also run placebo tests

28.1.4 Example 4

by Michael Robbins and Steven Davenport who are authors of MicroSynth with the following improvements:

Standardization

use.survey = TRUEand permutation (perm = 250andjack = TRUE) for placebo testsOmnibus statistic (set to

omnibus.var) for multiple outcome variablesincorporate multiple follow-up periods

end.post

Notes:

-

Both predictors and outcome will be used to match units before intervention

Outcome variable has to be time-variant

Predictors are time-invariant

# right now the package is not availabe for R version 4.2

library(microsynth)

data("seattledmi")

cov.var <-

c(

"TotalPop",

"BLACK",

"HISPANIC",

"Males_1521",

"HOUSEHOLDS",

"FAMILYHOUS",

"FEMALE_HOU",

"RENTER_HOU",

"VACANT_HOU"

)

match.out <- c("i_felony", "i_misdemea", "i_drugs", "any_crime")

sea1 <- microsynth(

seattledmi,

idvar = "ID",

timevar = "time",

intvar = "Intervention",

start.pre = 1,

end.pre = 12,

end.post = 16,

match.out = match.out, # outcome variable will be matched on exactly

match.covar = cov.var, # specify covariates will be matched on exactly

result.var = match.out, # used to report results

omnibus.var = match.out, # feature in the omnibus p-value

test = "lower",

n.cores = min(parallel::detectCores(), 2)

)

sea1

summary(sea1)

plot_microsynth(sea1)

sea2 <- microsynth(

seattledmi,

idvar = "ID",

timevar = "time",

intvar = "Intervention",

start.pre = 1,

end.pre = 12,

end.post = c(14, 16),

match.out = match.out,

match.covar = cov.var,

result.var = match.out,

omnibus.var = match.out,

test = "lower",

perm = 250,

jack = TRUE,

n.cores = min(parallel::detectCores(), 2)

)28.2 Augmented Synthetic Control Method

package: augsynth (Ben-Michael, Feller, and Rothstein 2021)

28.3 Synthetic Control with Staggered Adoption

references: https://ebenmichael.github.io/assets/research/jamboree.pdf (Ben-Michael, Feller, and Rothstein 2022) package: augsynth

28.5 Generalized Synthetic Control

reference: (Xu 2017)

- Bootstrap procedure here is biased (K. T. Li and Sonnier 2023). Hence, we need to follow K. T. Li and Sonnier (2023) in terms of SEs estimation.

28.6 Other Advances

L. Sun, Ben-Michael, and Feller (2023) Using Multiple Outcomes to Improve SCM

- Common Weights Across Outcomes: This paper proposes using a single set of synthetic control weights across multiple outcomes, rather than estimating separate weights for each outcome.

Reduced Bias with Low-Rank Factor Model: By balancing a vector or an index of outcomes, this approach yields lower bias bounds under a low-rank factor model, with further improvements as the number of outcomes increases.

Evidence: re-analysis of the Flint water crisis’s impact on educational outcome.