36.5 Marketing Return

Event Analysis

Nature of series

- Continuous

Univariate: Class Bass, Classic FDA

Multivariate Unidirectional: functional regression, classic Koyck, ADL, ARIMA

Multivariate Multidirectional: VAR, VARX, PVAR, Simultaneous Equation

- Punctuated

Event is dependent: Hazard models, split hazard, bivariate hazard

Evident is independent: Event analysis, synthetic control, DID

Decreasing rigor of causal inference

- Lab Experiment

- Field Experiment

- Nature Experiment

- Instrumental Variables

- Granger causality (improves with shocks)

- Times series regression (improves with shocks)

- Cross-sectional regression

Levels of testing causality in field

Correlation

Multiple regression: control for other plausible causes

Times series model (use of current and past values: Koyck, ADL, ARIMA)

First differences (effect of changes)

Lag of first differences (Arellano & Bond)

Granger causality (use of only past values of independent variables + control of past values of dependent variables (VAR), preferably in differences).

Intervention or event analysis

Natural experiments

RCT

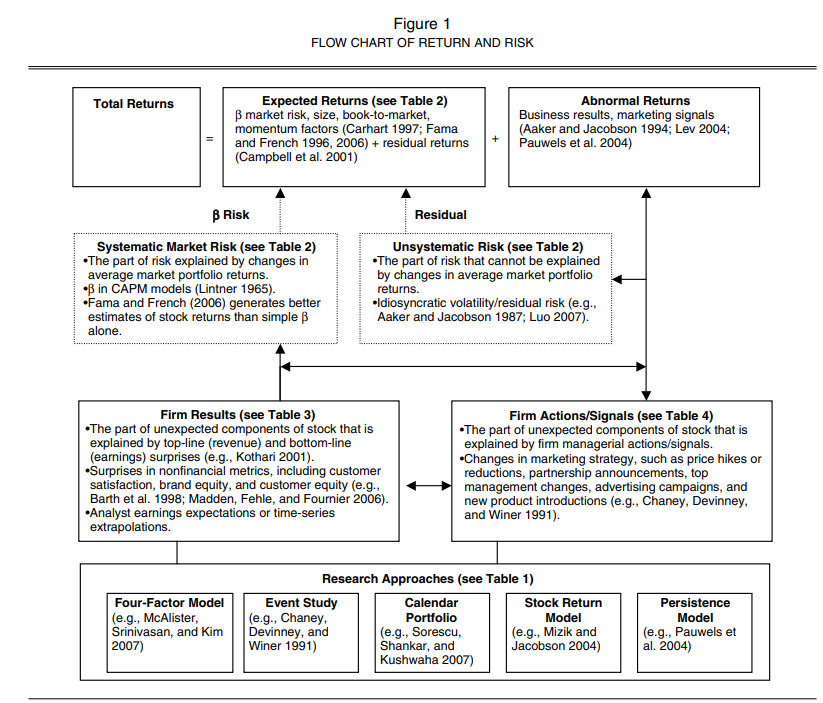

Concept of Abnormal Return:

Stock price (\(P_t\)) = random walk

Return = \(P_t - P_{t-1}\) = white noise

Panel Regression

Sample similar firms, \(j\)

Identify each of their similar events: First stage regression (WRDS)

Estimate abnormal returns of each of these firms associated with each of those events \(e_{jt}\)

2nd stage: equation

Pool abnormal returns

Estimate factors that may affect the distribution of \(e_{jt}\)

Strength of event analysis

Increases with clearly defined event, narrow window of treatment, removal of confounding events

Long time series for baseline

large number of firms

diverse contexts of treatments

Extraction effects of known predictors

temporal dependent series (returns)

punctuated independent series: event

Focus on effects of event on series of returns

simulates a natural experiment

Define: a natural or artificial shock

Types of natural experiments:

Compare treated vs. untreated

compared before and after

DiD

Synthetic control

Types of pre-temporal controls

One prior period

baseline of prior period

synthetic control

function of known factors (Fama-French 4)

Cross-over (treated becomes control and rev)

Time capsule in Marketing

| Event | Source |

|---|---|

| market Entry | Factiva, Lexis-Nexis |

| new product | Factiva, Thomson Reuters |

| Consumers satisfaction | CSI |

| Innovation activities | Factiva, Cap IQ |

| Acquisitions | Factiva, SDC platinum |

| Quality | Web chat, product reviews |

| Advertising | TNS Stradegy, YouTube |

| Recalls | Govt web, others |

| Sales | Yahoo fin, 10k GFK, euromonitor, Nielsen |

| Earnings | SEC Filings |

| Stock Prices | CRSP, WRDS |

36.5.1 (Fornell et al. 2006) Customer satisfaction and stock return

Historically, people understand that customer satisfaction affects firm economic performance. But we haven’t studied the relationship between customer satisfaction and stock performance.

People don’t incorporate the info about customer satisfaction into the stock price right away (market is not so efficient)

From the literature, we understand that there are 4 determinants of a company’s market value

Acceleration of cash flow: speed of buyer response marketing efforts

increase in cash cash flows: repeat business and low marginal costs of sales

reduction in cash flow risk: lower by satisfaction

increase in the residual value of the business

Data: Compsutat + American Customer Satisfaction Index

Regression (correlation) analysis

\[ \ln Market value = \alpha + \beta_1 \ln Book value \\ + \beta_2 \ln Bookvalueliability + \beta_3 \ln ACSI \]

There is evidence for a correlation market value and customer satisfaction.

However, investors don’t always respond positively to increased satisfaction news

The firms is giving away consumer surplus

firms that already have leads over competition

Why trade-off between satisfaction and productivity

reverse causality

timing expectation (i.e., measurement of satisfaction)

36.5.1.1 Event study

- Suing market model to estimate abnormal return

\[ AR_{jt} = R_{jt} - (\alpha_j + \beta_j R_{mt}) \]

where \(j\) = firm, and \(t\) = day

estimation period = 255 days ending 46 days before the event date (McWilliams and Siegel 1997)

one-day event period = day when Wall Street Journal publish ACSI announcement.

5 days before and after event to rule out other news (PR Newswire, Dow Jones, Business Wires)

M&A, Spin-offs, stock splits

CEO or CFO changes,

Layoffs, restructurings, earnings announcements, lawsuits

No evidence for the effect of ACSI on CAR

36.5.2 (S. Srinivasan and Hanssens 2009) Marketing and Firm Value

Marketing investments don’t always translate to firm value readily.

Marketing investments are typically intangible:

brand equity

customer equity

customer satisfaction

R&D

product quality

specific marketing-mix actions

Market is not so efficient: e.g.

- Intangible-intensive firms are usually undervalued (Lev 1989)

Market Valuation Modeling:

Fame-French factor explains excess returns come from

market risk factor: excess return on a broad market portfolio

size risk factor: difference in return between a large and small cap portfolio

value risk factor: difference in return between high and low book-to-market stocks

Momentum: Carhart (1997)

Metrics:

Top-line (revenue)

bottom-line (earnings) surprises

Methods: 4-factor model can still have omitted variables

Metrics on Marketing and Firm value

Market cap: need to

isolate the book value (using Tobin’s q)

Incorporate random-walk behavior in stock prices (first difference of log(stock price))

stock returns

| Method | Characteristics | Litimations | Examples | Dependent/Independent |

|---|---|---|---|---|

| Four Factor Model | Assume efficient market theory | sensitive to benchmark portfolio correlation analysis can contain omitted variable bias examine cross-sectional variation only |

Tobin’s q/ Branding strategy Firm val/ brand value estimates Stock returns/ brand valuation |

|

| Event Study | Assume efficient market Causal Analysis |

can’t measure long-term effect | (Horsky and Swyngedouw 1987): name change (Chaney, Devinney, and Winer 1991): new product intro (Lane and Jacobson 1995): brand extension |

Stock returns/ name events Stock returns/ new product intro Stock returns/ brand extensions Stock returns/ Internet channel |

| Calendar protfolio | Include firms with certain to measure long-term impact more accurate than event studies |

Can’t measure per event effect might be sensitive to benchmark prtofolio |

(A. Sorescu, Shankar, and Kushwaha 2007) | Stock returns/ new product |

| Stock return response model | based on Carhart (1997) and EMH account dynamic properties of stock returns incorporate continuous events |

detailed data at the brand so business unit level marketing info must be public single equation model without temporal chain |

(D. A. Aaker and Jacobson 1994) |

Stock returns/ perceived quality Stock return / brand attitude stock return/ strategic shifts Stock returns/ marketing actions |

| Persistence modeling | system of equations: consumer (demand equation), manager (decision rule equation), competition, (competitive reaction equation), investor (stock price equation) VAR: examines both short-term and long-term robust to deviations from stationarity incorporate dynamic feedback loops |

detailed data at the business unit level time-series over a long horizon reduced-form models |

Firm value/ new product intro, sales promotions stock returns/ advertising |

4 factor model:

\[ R_{it} - R_{rf,t} = \alpha_i + \beta_i (R_{mt} - R_{rf,t}) + s_i SMB_t \\ h_i HML_t + u_i UMD_t + \epsilon-{it} \]

where

\(R_{it}\) = stock return for firm \(i\) at time \(t\)

\(R_{rf,t}\) = risk-free rate in period \(t\)

market factor = \(R_{mt}\) = market return in period \(t\)

Size factor = \(SMB_t\) = return on a value-weighted portfolio of small stocks - the return of big stocks

Value factor = \(HML_t\) = return on a vlaue-weighted portfolio of high book-to-market stocks - return on a value-wegihted portfolio of low book-to-market stocks

Momentum factor \(UMD_t\) = average return on 2 high prior-return portfolio - the average return on two low prior return portfolio

36.5.3 (Sood and Tellis 2009) Innovation and Stock Return

Innovation is important for firms

But firms are cautious when investing in R&D (long-term effect hard to justify)

Finding: innovations effect on stock prices is underestimated when events are distinct vs. aggregate

3 types of innovation activities

- Initiation: alliance, funding, expansions

- Development: Prototypes, patents

- Commercialization: Porudct Launch, awards

Takeaways

Total market returns to an innovation project: 643 mil (compared to 49 mil the return to an average event in the innovation project)

Positive events increase returns for all three types of events

Negative events decrease return for development and commercialization stages only

The absolute value of the market returns is higher for negative announcements than for positive announcements

36.5.4 (Jacobson and Mizik 2009b)

Disagreeing with previous research conclusion that there was a systemic mispricing of customer satisfaction into the stock price (Fornell et al. 2006) (Aksoy et al. 2008), the anomaly stem from only a small group of satisfaction leaders in the computer and internet sector. (i.e., sampling bias).

This study is consistent with (O’Sullivan, Hutchinson, and O’Connell 2009)

36.5.5 (Jacobson and Mizik 2009a)

36.5.6 (Borah and Tellis 2014) Choice of Payoff from announcements (Innovations)

- Whether a firm should make, buy or ally regarding new technologies

Innovation phases:

- Initiation

Make

Buy

Ally

- Development

- Commercialization

New product launch

initial shipments

new app and markets for the new products

awards

Models

- Model of returns

- Model of investment choice: multinomial logit model

- Model of payoffs:

36.5.7 (Tirunillai and Tellis 2012) Chatter effect on stock performance

Research questions:

Cor(UGC, stock performance)

What is the direction of causality

Among the UGC metrics, which best relates to stock performance

What are the dynamics of the relationship in terms of wear-in, war-out, and duration?

Data: 4 years, 6 markets , 15 firms

Findings:

Volume of chatter increases abnormal returns by a few day (using Granger causality tests) and trading volume

Positive UGC has no effect on abnormal returns

Negative UGC has negative effect on abnormal returns with a short “wear-in” and long “wear-out”

Interaction between chatter volume and negative chatter have a positive effect on trading volume

negative UGC positively correlates with idiosyncratic risk

Positive UGC has no effect on the idiosyncratic risk

Offline ad also increases the volume of chatter and decreases negative chatter

UGC:

- Product reviews + product ratings

Stock performance:

A measure of shareholder value

Available at the daily level

Assumption:

Market is not efficient: it takes time for the market to reflect info about UGC.

Asymmetric response across UGC metrics:

Losses loom larger than gain

investors discount positive info because it’s unreliable

Positive messages are usually influenced by the firms, but not negative

Sampling:

Product categories that have rich data on UGC (digital, high tech and popular consumer durable)

Product categories that reviews are related to sales

Public firm only

No M&A during the period

The sample markets should be representative of the whole market.

Time: June 2005 - Jan 2010

Media:

Product reviews instead of text or videos, etc because intuitively people use this form to express their opinion

Consumer reviews instead of evaluations, blogs, forums, because it’s more focused and greater signal-to-noise ratio

Consumer reviews instead of expert review because of wisdom of the crowds

3 popular websites: Amazon.com, Epinions.com, Yahoo! Shopping.

ratings + text reviews

Measures

UGC: ratings, volume chatter, positive valence, negative valence

Stock market performance

Abnormal returns: Fame-French (1993) three-factor + Carhart 1997 momentum factor.

Idiosyncratic risk: same model as abnormal returns

Trading volume: = daily turnover = volume of trade / shares outstanding at the end of the day

Using EGARCH specification:

\[ R_{i,t} - R_{f,t} = \alpha_i + \beta_{i, MKT} (R_{MKT, t} - R_{f,t}) + \beta_{i, SMB} SMB_t \\ + \beta_{i, HML} HML_t + \beta_{i, MOM} MOM_t + \epsilon_{i,t} \]

where

- \(\epsilon_{i,t} \sim N(0, \sigma_{i,t})\)

\[ \ln(\sigma^2_{i,t} ) = a_i + \sum_{j = 1}^p b_{i,j} \ln (\sigma^2_{i,t-j}) \\ + \sum_{k=1}^q c_{i,k}\{ \Theta (\frac{\epsilon_{i, t - k}}{\sigma_{i, t - k}}) + \Gamma (| \frac{\epsilon_{i, t-k}}{\sigma_{i, t-k}}| - (\frac{2}{\pi})^{1/2})\} \]

Control Variables

Analysts’ Forecasts: IBES Database

Advertising: TV ad from TNS media Intelligence

Media Citations: Number of articles in print media from LexisNexis (with relevancy score above 60%) and Factiva (using company tag)

New product Announcement: also LexisNexis and Factiva (following (Sood, James, and Tellis 2009))

Models

Vector Auto-regression (VAR)

can handle continuous events (instead of discrete events used in event studies)

account for immediate and lagged-term of the independent variables

capture the carryover effects over time with the generalized impulse response function

Controls for trends, seasonality, non-stationary, serial correlation, and reserve causality (Luo 2009)

Procedure

- Estimate the stationary (unit roots + co-integration) properties of stock performance and UGC

Stationarity test: Augmented Dickey-Fuller test + Kwiatkowski-Philips-Schmidt-Shin test

Co-integration: Johansen’s procedure (Johansen et al. 1992)

- Granger causality test

- Estimate dynamics of carryover effect using impulse response function

- Not sensitive to the causal ordering to the causal ordering of the variable in the system of equations

- Estimate the effect of UGC using variance decomposition: relative importance of metrics of UGC