36 Strategic Dynamic Models

(Tülin Erdem and Keane 1996) is a good paper to think of structural modeling in marketing

What is interesting and impactful?

Correctness is not king

-

Challenge audience assumptions

Too strong = absurd

Took weak = not interesting

Sweet spot

Pitfall in Empirical Approach

Selective (biased) sample

Omit competition

-

Ignore

Dynamics

Heterogeneity

Endogeneity

Marketing Complexity

Sales response to a single marketing instrument

Marketing Mix Interaction

Competitive Effects

Delayed Response

Multiple Territories

Multiple products

Functional Interactions

Multiple Goals

Methodology

Verbal Model

Mathematical Model

Purpose

-

Measurement models

- Conjoint model

Decision support models

Theoretical models

36.1 Market Entry

Pioneering paradox

-

Market entry massively important

Big decision

Start of business strategy

-

Perennial conflicts:

Pioneer vs. 2nd move vs. late entry

Incumbent vs. Entrant

Huge payoff if played well

-

One explanation: Fixation

Fixation: focus on micro hurdle /breakthrough

Entrenchment: hang on to /perfect early success

Marketing Myopia

Baggage: routines. bureaucracy hinders vision

Another explanation: high failure rate of ideas

Third Explanation: Trend Projection Hot hand bias

Anything can be wrong. As a reviewer you have to say why you have a better explanation for a result

36.1.1 (Peter N. Golder and Tellis 1993)

-

Downfall of previous research using PIMS and ASSESSOR or business press:

survivorship bias

single-informant self-reports: measurement errors

Half of market pioneers fail and mean market share is lower (compared to previous studies)

Early market leaders have greater long-term success and enter about 13 years after the first pioneers

-

Theories of pioneer advantages

-

Consumer-based:

Uncertainty in trying later entrants

Consumer stable preferences

Learning theory: pioneer = standard

Positioning advantage

Consumer with high switching costs will stay

-

Product-based:

- Barrier to entry: economies of scale + learning + technological leadership + limited suppliers

-

-

Theories of pioneer disadvantages

Free-riders: late entrants can come in at lower cost

Shifts in technology, customer needs

Incumbent inertia

Improper positioning (late entrants can pick optimal position later because pioneers’ high cost of switching)

changing resource requirement

insufficient investments

-

Data: historical analysis based on all publicly available sources of info.

Prospective contrast to retrospective (from database)

Might be less biased because of multiple sources (instead of single informants).

Examples: business week, advertising age

-

Criteria for selection:

Competence

Objectivity

Reliability

Corroboration: Confirmation Bias?

-

Sampling (have to justify you chose what you choose): before sampling was drawn.

Sample 1: consumer goods + new product categories and its extensions.

Sample 2: categories from Advertising Age

Sample 3: acknowledged pioneers

-

Limitation:

Did not consider marketing mix

Customer-oriented definition of product category = arbitrary

Sample selection

Uncertainty regarding survivorship bias

36.1.2 (J. Johnson and Tellis 2008)

Market entry into China and India

Smaller firms are more successful than larger firms

Markets that are more open have less success rate.

Success is greater for companies (1) enter earlier, (2) have greater control of entry mode, (3) similar to the host country.

India is a tougher market than China (i.e., less successes)

-

Drivers of Entry success:

-

Firm differentiation

-

Firm strategy

-

Entry mode: export, license and franchise, alliance, joint venture, wholly owned subsidiary (related to degrees of control over its marketing resources from lowest to highest). Opposite prediction

Resource-based: degree of control increases with success likelihood, and help control resource leakage, and complementary resources.

Transactions cost: cost increases with degree of control (high investment -> high levels of investment to break even).

-

Entry timing:

Early entry: lock up key resources (e.g., distribution channels + suppliers), create standard, consumer preferences, exploit governmental incentives.

Late entry: pioneers usually don’t have long-term success (Peter N. Golder and Tellis 1993), learn lesson from early entrants, lower learning curve

-

-

Firm resources: Firm size

Larger > Smaller: more resources, more product- and marketing-specific knowledge, can absorb more negative periods

Smaller > larger: less bureaucracy, which lower innovative ability (Chandy and Tellis 2000)

-

-

Country differentiation

-

Host-country characteristics:

-

Openness: lack of regulatory and obstacles to entry

Good: increase demand, competition on quality, higher efficiency and lower prices

Bad: increase competition from foreign entrants (thin margins, high cost of purchases, hiring of talent).

-

Country risk: negatively affect entry success

Political: tariffs, regulations

Financial + Economic: recession, currency crises, inflation.

-

-

-

Host-home location

Cultural distance: closer better

-

Economic distance:

- Closer better: similar market segments (transformable market demand knowledge), similar physical infrastructure (greater efficiency in operations, lowering costs), more market knowledge

-

-

Data: historical analysis where data meet the following criteria:

Competence

Neutrality / Objectivity

Reliability

Corroboration

Contemporaneity

-

Small sample size

192 from China

64 from India

| Variable | Measure | Source |

|---|---|---|

| Success | Degree of success numerical rating | Historical Analysis from LexisNexis and ABI/INFORM |

| Entry mode | 6 points scale based on (E. Anderson and Gatignon 1986) | Archival data |

| Entry timing | Arbitrary: China: 1978, India 1991. | Archival data |

| Firm size | year-end sales for the focal firm | Compustat, Mergent Online |

| Economic distance | (D. Mitra and Golder 2002) | International Financial Statistics yearbook |

| Cultural distance | Follow (Kogut and Singh 1988) | Hofstede (1991, 2001) |

| Openness | Fraction of foreign direct investment over the host country’s GDP | International Monetary Fund |

| Country Risk | Based on International Country Risk Guide (Erb, Harvey, and Viskanta 1996) | International Country Risk Guide |

36.1.3 (Zervas, Proserpio, and Byers 2017)

Use DiD identification strategy

-

sharing economy decreases demand for hotel via less aggressive hotel room pricing.

- Those with low price and don’t cater to business travelers suffer most.

Data: from Airbnb (using review history) and 300 hotels in Texas (Texas Comptroller of Public Accounts),

-

Dependent variables:

Cumulative measure

Instantaneous measure

10% increases in the market share of Airbnb lead to .39% decrease in hotel room revenue

36.2 Product Adoption and Diffusion

36.2.1 Background

Every new thing either diffuses through population or fails

Researchers are interested in the shape and processes of diffusion

Bass is the first to model in marketing

Diffusion in different fields:

Demography

Archaeology

Geography

Epidemiology

Sociology

Linguistics

Physics

Cosmology

Models of Diffusion

Negative Exponential

Bass

FDA

Network

Levels of analysis:

Class:

Category

Technology

Brand

Classic model

does not account fro marketing mix

requires peak sales for stable estimates (if you have the peaks, you don’t need the model)

no repurscrhsases

no multiple generation

does not fit viral patterns

36.2.1.1 (Chandrasekaran and Tellis 2007) A review of new products diffusion

Products = idea, person, good, or service

New product \(\neq\) innovation

| In econ | In marketing | |

|---|---|---|

| Diffusion | “the spread of an innovation across social groups over time (p. 39) | “the communication of an innovation through the population” |

| Phenomenon (spread of a product) \(\neq\) drivers (communication) | Phenomenon (spread of a product) = driver (communication) |

This paper focuses on the econ definition

Product’s life cycle stages:

- Commercialization: when the product was first sold

- Takeoff: dramatic and sustained increase in sales

- Introduction: between commercialization and takeoff

- Slowdown: decreasing in sales

- Growth: between takeoff and slowdown

- Maturity: Slowdown until decline.

Generalizations:

Shape of the Diffusion Curve: cumulative sales over time is S-shaped curve.

-

Parameters of the Bass model:

-

Coefficient of innovation or external influence (\(p\))

mean between 0.0007 and 0.03

mean for developed countries is 0.001 and developing countries is 0.0003

-

Coefficient of imitation or internal influence (\(q\))

mean between 0.38 and 0.53

industrial/medical innovation > consumer durables

0.51 for developed countries and 0.56 for developing countries

-

the market potential (\(\alpha\) or \(m\))

- 0.52 for developed countries and 0.17 for developing countries.

-

-

Cautions regarding the parameters:

Time to peak sales: 19 years for developing and 16 for developed countries.

Biases in parameter estimation: static models (e.g., Bass) lead to downward biases in market potential and innovation while upward bias in imitation.

Drivers: WOM, communication, economics, marketing mix variables (e.g., prices, consumer heterogeneity, consumer learning), purchasing power parity adjusted per capita income, international trade.

-

Turning points of the diffusion curve

-

Takeoff

Time to takeoff: 6-10 years (varies by countries,products, time).

Drivers: price decrease

-

Slowdown

Sales decline by 15-32%

Drivers: price decline, market penetration, wealth (GNP), and info cascades (fast takeoff = fast decline)

-

-

Findings across stages

-

Duration:

introduction: 6-10 years

growth: 8-10 years

early maturity: 5 years

-

duration of growth:

time saving products > non-time saving products

leisure enhancing products < non-leisure enhancing products

introduction and early maturity duration get shorter over time (but not growth)

Price: price reduction is getting larger as time progresses (for both introduction nd growth).

-

Growth rates:

Introduction: 31%

Takeoff: 428%

Growth: 45%

Slowdown: -15%

Early maturity: -25%

Late maturity: 3.7%

-

Future Research:

Measurement: When to start or stop, or takeoff, differentiation between first purchases and repurchases, demand is better than supply measure,

Theories: no reconciliation yet

Models: comprehensive (from commercialization to takeoff, growth, and slowdown)

Findings: More fine-tune subgroups, include failed diffusion, and consider other countries.

Specification

The probability that an individual will purchase at time \(T\) is a function of the number of previous buyers.

\[ P(t) = \frac{f(t)}{1 - F(t)} = p + \frac{q}{m} Y(t) \]

where

\(P(t)\) = hazard rate

\(Y(t)\) = cumulative number of adopters at \(t\)

\(p\) = probability of an initial purchase at time 0 (when \(Y(0) = 0\)) (also known as innovators importance).

\(\frac{q}{m} Y(t)\) = pressure of prior adopters on imitators

\(m\) = number of initial purchases before any replacement purchases (i.e., market size)

\(F(t)\) = cumulative fraction of adopters at time \(t\)

\(f(t)\) = likelihood of purchase at time \(t\)

Rearrange the formula to get the likelihood of purchase at time \(t\)

\[ f(t) = (p + q F(t) ) [1 - F(t)] \]

The number of adoptions at time \(t\) is

\[ S(t) = mf(t) = pm + (q - p) Y(t) - \frac{q}{m} Y^2(t) \]

then Bass solves the differential equation:

\[ dt = \frac{dF}{p + (q - p) F - qF^2} \]

to obtain cumulative adoption at time \(t\)

\[ F(t) = \frac{1 - e^{-( p + q)t}}{q + (q/p) e^{-( p + q)t}} \]

Hence, the cumulative number of adopters is

\[ Y(t) = m \frac{1 - e^{-( p + q)t}}{q + (q/p) e^{-( p + q)t}} \]

Rewriting the number of adoptions at time \(t\)

\[ S_t = a + bY_{t-1} + c Y^2_{t-1}, t = 2, 3, \dots \]

where

\(S_t\) = sales at time \(t\)

\(Y_{t-1}\) = cumulative sales through period \(t-1\)

\(a = p \times m\)

\(b = q - p\)

\(c = - q /m\)

Equivalently,

\[ p = a/m \\ q = -cm \\ m = (-b \pm (b^2 - 4 ac)^{1/2})/2c \]

Strengths

Good fit to the S-shaped curve (thank to the quadratic term)

-

Appealing interpretations:

\(p\) = coefficient of innovation (i.e., spontaneous rate of adoption in the population) or external influence (e.g., mass -media communications)

\(q\) = coefficient of imitation (i.e., effect of prior cumulative adopters on adoption) or internal influence (e.g., interpersonal communication influence from prior adopters).

Good application: time (\(t\)) or magnitude (\(S(t)\)) of peak sales.

\[ t^* = \frac{1}{p + q} \times \ln (\frac{q}{p}) \\ S(t)^* = m \times \frac{(p + q)^2}{4q} \]

-

Incorporated prior literature

If \(p =0\), the Bass model is a logistic diffusion function (driven only be imitation adoption)

If \(q = 0\), the Bass model is an exponential function (driven only innovation adoption)

Limitations

Bass requires 2 most important events that we want to predict in the first place: takeoff and slowdown to have stable estimates.

Unstable estimates after incorporating new observations.

Do not directly account for marketing mix variables (price, promotion), but indirectly capture by \(m, p\)

Assumes product definition is static (no growth or changes in product as time progresses)

-

Using OLS which can cause

Multicollinearity between \(Y_{t-1}, Y^2_{t-1}\) (making the estimates unstable)

Do not estimate the SE for \(p, q, m\)

Time interval bias (model uses discrete time series data to estimate a continuous model)

-

Hard to determine starting and ending points of the the sales time.

Supposedly, we need to use first adoptions of new product as sales (\(S_t\)), but data could not capture this, only both first purchases and repurchases

Sales should start from the first year of commercialization, but usually we only have reports when products are selling well already

No clear stopping rule for the time interval.

Improvements

-

Incorporating marketing mix

Price: affect market potential (\(m\)) and probability of adoption (\(P(t)\)) and heterogeneous across products

Advertising

Distribution: 2 adoption processes: retailer and consumer, where number of retailers who affect determine the market potential \(m\) for consumers

(Bass, Krishnan, and Jain 1994) incorporate both price and promotion to the Generalized Bass model

\[ \frac{f(t)}{1 - F(t)} = (p + q F(t) )x(t) \]

where \(x(t)\) is the current marketing effort (sum of advertising and price) on the conditional probability of product adoption at time \(t\) such that

\[ x(t) = 1 + \beta_1 \frac{\Delta P(t)}{P(t-1)} + \beta_2 \frac{\Delta A(t)}{A(t-1)} \]

where

\(\Delta P(t) = P(t) - P(t-1)\) rate of changes in price

\(\Delta A(t) = A(t) - A(t-1)\) rate of changes in advertising

When prices and advertising remain constant, GB model reduces to Bass model. But it seems like they only stop at 2 variables (not all marketing mix variables or macro and micro econ variables - income changes).

-

Incorporate supply restrictions

- Include another stage between potential adopter to adopters which is waiting applicants.

\[ \frac{d A(t)}{dt} = [p + \frac{q_1}{m}A(t) + \frac{q_2}{m} N(t)][ m - A(t) - N(t) ] - c(t) A(t) \\ = \text{[Waiting population + Adopters] - conversion rate of applicants to adopters}\\ \]

and

\(\frac{d N(t)}{dt} = c(t) A(t)\)

where

\(d(A)/dt\) is the rate of changes of waiting applicants

\(c(t)\) is the supply coefficient

the second equation is the impact of supply restrictions on adoption rate

The growth of new applicants is

\[ \frac{d Z(t)}{dt} = \frac{d A(t)}{dt} + \frac{dN(t)}{dt} \\ = (p + \frac{q_1}{m} A(t) + \frac{q_2}{m} N(t) ) (m - A(t) - N(t)) \]

To incorporate waiting applicants abandoning their adoption decision after some time see (Ho, Savin, and Terwiesch 2002)

-

Incorporate competitive effects

Instead of using product category as the unit of analysis, we can model at the brand level (different brand might have different rate of diffusion).

-

A new brand can

increase the entire market potential (\(m\)) (by increased promotion and product variety)

compete in the existing market potential (interfere the diffusion process of other brands)

Diffusion depends on the order of entry and competition.

-

Incorporate complementary effects

- In market that has indirect network externalities, co-diffusion exists and asymmetric

Incorporate technological generations for successive generations of the same product (i.e., substitution effects).

\[ S_1(t) = m_1F_1(t) - m_1 F_1(t) F_2(t - r_2) \]

where \(r_2\) is the introduction time of the next-generation product.

\[ S_2(t) = F_2(t- r_2) [m_2 + F_1(t) m_1] \]

where

\(S_i(t)\) = sales of generation \(i\)

\(F_i(t)\) = fraction of adoption for each generation

\(m_i\) = market potential for each generation

Leapfrogging behavior is possible (i.e., skip a generation to buy the next one) (Mahajan and Muller 1996)

-

Incorporate time-varying parameters

Model market potential (\(m\)) as a function of time-varying exogenous and endogenous variables (Mahajan and Peterson 1978)

Model coefficient of imitation to be time-varying (Easingwood, Mahajan, and Muller 1983)

\[ \frac{d F(t)}{dt} = [ p + q F(t)^\delta][ 1 - F(t)] \]

where \(\delta\) is the nonuniform influence

when \(\delta = 1\), the model becomes the Bass model

When \(\delta \in [0,1]\), means high initial coefficient of imitation,

When \(\delta >1\), means delay in influence -> lower and later peak.

Different adopters could influence later adopters differently (people who adopted more recently are more vocal) (Sharma and Bhargava 1994)

- Incorporate replacement and mufti-unit purchases

(Balasubramanian and Kamakura 1989)

\[ y(t) = [a + bX(t)][\alpha \text{Population}(t) P^\beta (t) - X(t)] + r(t) + e(t) \]

where

\(y(t)\) = sales

\(P(t)\) = price index

\(X(t)\) = total units in use at the beginning of year \(t\) with dead units are replaced already

\(r(t)\) = number o units that have died or need replacement at year \(t\)

\(a\) = coefficient of innovation

\(b\) = coefficient imitation

\(\beta\) = price change effect on ultimate penetration

\(\alpha\) = ultimate penetration (price is at its original level)

(Steffens 2003) models multiple units purchase by a single household.

Incorporate trail-repeat purchases

Incorporate variations across countries

Evaluation:

- All of the improvements still rest on the assumption of one driving mechanism: knowledge dispersion through WOM.

Improvements in estimation

MLE: avoid time-interval bias, but underestimates the SE (Schmittlein and Mahajan 1982)

-

Non linear least squares: (V. Srinivasan and Mason 1986) need lots of obs

Estimates are more flexible

No time-interval bias

valid SE

-

Hierarchical Bayesian method

Incorporate parameter updating

Problem with definition of similar products (fixed by (Bayus 1993) with product segmentation scheme)

Adaptive techniques: stochastic techniques (parameter vary over time) ((J. Xie et al. 1997)augmented Kalman filter)

-

Genetic algorithms:

can find global optimum

better estimate (less bias).

Alternative models of diffusion

-

Alternative drivers:

-

Affordability: (Peter N. Golder and Tellis 1998) model as Cobb-Douglas model:

\(S = P^{\beta_1} \times I^{\beta-2} \times CS^{\beta_3} \times MP^{\beta_4} \times e^\epsilon\)

Sales = product (price, income, consumer sentiment, market presence)

(Horsky 1990) incoproates both price and income and WOM on sales growth.

Heterogeneity: aggregate level diffusion models: (J. H. Roberts and Urban 1988), (Oren and Schwartz 1988), (Chatterjee and Eliashberg 1990), (Bemmaor 1984) (Song and Chintagunta 2003b), (Sinha and Chandrashekaran 1992) (Karshenas and Stoneman 1993)

Strategy: model supply side: (market entry, marketing mix, location) (Dekimpe, Parker, and Sarvary 2000), (Bulte and Lilien 2001),(Bart J. Bronnenberg and Mela 2004)

-

-

Alternative phenomena:

-

Spatial diffusion (Mahajan and Peterson 1979), (Redmond 2003), (Garber et al. 2004)

Contagious diffusion (infectious diseases)

Expansion diffusion (one source like wildfire)

Hierarchical diffusion (ordered series of classes)

Relocation diffusion:

Diffusion of entertainment products: follow exponential decay (Eliashberg and Sawhney 1994), (Eliashberg et al. 2000), (Elberse and Eliashberg 2003), (Moe and Fader 2002), (J. Lee, Boatwright, and Kamakura 2003)

-

Modeling the turning points in diffusion

-

Takeoff: follow (Peter N. Golder and Tellis 1997) definition: “point of transition from the introduction stage to the growth stage”

-

Measurement

(Peter N. Golder and Tellis 1997): threshold takeoff (compare to other in the categories)

Logistic curve rule: first turning point of the logistic curve (max of the 2nd derivative) (hindsight only)

Maximum growth rule: largest sales increases within 3 years (not size invariant)

(Agarwal and Bayus 2002) measure based on annual percentage change in sales

(Stremersch and Tellis 2004) adapted the threshold method for international markets

(Garber et al. 2004) rule of thumb: 10-20 market penetration

-

Drivers

(Peter N. Golder and Tellis 1997) price declines lead to takeoff

(Agarwal and Bayus 2002) increase in firm entry lead to better product quality, marketing infrastructures

(Tellis, Stremersch, and Yin 2003) venturesome culture lead to takeoff

Model: either proportional hazards (Peter N. Golder and Tellis 1997) or log-logistic hazard (Tellis, Stremersch, and Yin 2003)

Evaluation: Only model successful innovation so far.

-

-

Slowdown: point of transition from the growth stage to the maturity stage (Peter N. Golder and Tellis 1997)

Measurement: (Peter N. Golder and Tellis 2004) “operationalize as the first year of two consecutive years after takeoff in which sales are lower than the highest previous sales.” (p.72)

-

Explanation:

Dual-market phenomenon: early adopters vs. early majority (Goldenberg, Libai, and Muller 2001)

Informational cascades: negative cascades (Peter N. Golder and Tellis 2004)

Affordability(Peter N. Golder and Tellis 2004)

-

Modeling:

Cellular automata models: (Goldenberg, Libai, and Muller 2001)

Hazard models: (Peter N. Golder and Tellis 2004)

Evaluation: still new can have more research

36.2.1.2 (Bass 1969)

Assumption:

The timing of a consumer’s initial purchase is correlated with the number of previous

This paper looks at new class of products (not new brands or new models of older products)

Focus on infrequently purchased products

Theory of Adoption and Diffusion

Innovators: adopt independently (regardless of others’ opinions): pressure to adopt does not increase with the growth of the adoption.

Imitators (include early adopters, early majority, late majority): adoption depends on the timing of adoption (i.e., influenced by the decisions of others to adopt.

Laggards

“The probability that an initial purchase will be made at \(T\) given that no purchase has yet been made is a linear function of the number of previous buyers” (p. 216)

\[ P(T) = p + \frac{q}{m} Y(T) \]

where \(p\) and \(q/m\) are constants

\(Y(T)\) is the number of previous buyers.

When \(Y(T) = 0\), \(p\) represents the probability of an initial purchase at \(T = 0\)

\((q/m) Y(T)\) is the pressures on imitators to adopt.

Model Assumptions:

36.2.2 Discussion

36.2.2.1 (Sood, James, and Tellis 2009)

Functional regression

-

Contributions:

Theoretically sound (integrate info across categorizes)

Augmented Functional regression outperforms existing models

Product-specific effects are more helpful in predicting penetration than country-specific effects.

They use yearly cumulative penetration of each category as the unit of analysis (i.e., curve/ function).

-

3 functional data analysis techniques:

Functional principal components

functional regression

functional cluster analysis

To treat discrete intervals: use smoothing spline to generate continuous smooth curves

Even though the spline approach requires a lot of data to smooth, other appearances to create smoothness are still available. Hence, you can still use function regression and or cluster with 2 or 3 time points.

-

Advantage s of functional regression:

incorporate info from other products

nonparametric fitting procedure

uses the functional nature of the penetration curves.

Predictions on: number of years to take off, peak marginal penetration and the level of peak marginal penetration

Good: tell a story from simple to more sophisticated model to justify their improvements in the paper.

-

2 dimensions that are not captured by simple extrapolation models:

info from prior history of the new product

intrinsic info across products and countries.

-

Classic Bass model ignores:

other categories (fixed by meta-bass and augmented meta-bass)

uses parametric methods.

-

Questions:

Technically could redo the analysis with new dataset (including 2009 till now) to see the out of sample performance.

No hypothesis, just model and probable explanation

Use only curves under the same category to predict the new product (not all categories).

36.2.2.2 (Appel, Libai, and Muller 2019)

Growth, Popularity and the Long Tail: Evidence from Digital Markets

part of MSI’s working paper series and MSI insights

Context: digitized markets (long-tail markets)

Most popular products do have S-shaped curve, but lower-popularity products exponential-like decline (“slide”) or a combination of slide and bell (S&B) are more common.

-

Shortcomings of previous research:

- Pro-innovation bias: success correlates with importance in the new product development research

Data: SourceForge (exclude inactive and less than 200 downloads): 5 years with high Gini coefficient - 0.96 (i.e., high concentration).

-

Dominant patterns:

-

A bell-shaped pattern: bell (popular products)

- Caveat in the movie market: popular products decline over time.

An exponential-like decline beginning at launch: slide

Combination of the first 2: S&B

-

Proposed model: inception model (inception effect = heightened external growth).

-

Long-tail market:

Supply side: low cost of inventory, stocking, efficient delivery, and low cost of new products development.

Demand-side: easy to search, recommendation system, social networks and online communities.

Popularity = extent of demand = number of downloads.

The shape of new product growth: previous literature says S-shaped

-

Non-S-shaped markets:

-

r-shaped cumulative curve: because of

Large budget for promotion: movies

Pre-launch buzz: on social media

-

The role of popularity on the shape of growth: was ignored in the literature

Free and Open-Source Software (FOSS)

-

Data Analysis:

Stage 1: To facilitate comparison, scale pattern to a (0,1) by dividing each observation by the total sum of downloads, and smooth the graph using Hodrick-Prescott filter

Stage 2: Use peaks-and-troughs algorithm for the classification

Descriptive: the S-shaped curve is representative for more popular products, while for those that are not as popular, we have a blend of S&B and slide as well.

Try to observe the same pattern with smartphone app download (data provided by Mobility - an anonymous app providers for businesses)

-

Drivers of Multi-pattern Growth

-

Analogy to movies (characterized by an exponential decline): not similar because

different product types (utilitarian vs. entertainment)

Different pattern exhibited by popular and unpopular: while in movies the exponential decline is from blockbuster, and sleepers has a bell shape, under this dataset, less popular product has the exponential decline, while the popular products are bell-shaped.

Analogy to supermarkets: not good because FDP is affected by social influence, supermarkets are usually under large investments and not much social influence.

-

The inception alternative: 2 influences of new product growth

Internal: from previous adopters

External (not from previous adopters): marketing mix, social media posts, recommendation, expert opinions, influencers. Expected to stronger early on and decay. (i.e., inception effect - external influence as a function of time with an initial external influence parameter \(p(t) = pe^{\delta t}\))

-

The relationship between inception and popularity: The higher the product’s popularity, the lower the share of adoptions due to the inception effects (i.e., products with high initial investment that failed to reach critical is less popular).

Inception is typically a necessary but not sufficient condition to reach popularity.

36.2.2.3 (Tellis et al. 2020)

No awards (nominated only)

Emotion is more effective than information

brand hurts, but branding is used a lot

surprise and humor are good, but videos don’t use

Limitation: Because these emotions are rare, maybe that why they are effective. But if everyone starts using these tactics, maybe that they wont’ work anymore.

36.2.2.4 (Chandrasekaran, Tellis, and James 2020)

Was rejected 5 times.

Leapfrogging, Cannibalization, and survival during disruptive technological change

-

2 types of dilemma when it comes to new technology:

Incumbent: invest in new technology or old or both

Entrant: target niche or mass.

Solution: relation between new technology and old one (i.e., high rate of disengagement - cannibalization or low rate of disengagement- coexistence)

-

Data:

Successive technology penetration across multiple countries and years

Sales of contemporaneous pair across multiples countries

Case analyses

“Disruption occurs if the incumbent focuses on the old technology to the exclusion of the new one” (p. 4)

-

Definitions:

Successive/New technology: not new version/generations of the same product

Cannibalization: “the extent to which the successive technology”eats” into real or potential sales (or penetration) of the old technology due to substitution.”(p. 5)

Rate of disengagement \(F_{12}\): (account for partial substitution)

-

Adopter segments for a new successive technology:

Leapfroggers: adopt new, but would never have adopted the old

Switchers: Adopted old, but switch to new once it’s introduced

Opportunists: wait for the old, but end up with the new one.

Dual users: both technologies

Models: based on (J. A. Norton and Bass 1987)

\[ S_1 (t) = m_1 F_1(t) (1- F_{12}(t- \tau_2 + 1)) \\ S_2 (t) = F_2(T- \tau_2 + 1) (m_2 + m_1 F_1(t)) \]

where

- \(S_i(t)\) = penetration of technology \(i\) in period \(t\)

- \(m_1\) = long-run penetration for technology 1

- \(m_1 + m_2\) = long-run penetration for technology 2

The fraction of all potential technology_g consumers for each technology (g = technology 1 or 2)

\[ F_g(t) = \frac{p_g(1 - e^{-(p_g + q_g)^t})}{p_g + q_g e^{-(p_g + q_g)t}} \]

where

\(t \ge 0\)

\(g = 1, 2\)

\(p\) = innovation coefficient

\(q\) = imitation coefficient

\(p_{12}, q_{12}\) = disengagement coefficients

\(F_1, F_2, F_{12}\) = adoption rate of technology 1, technology 2, and disengagement rate at which technology 1 customers abandon to get technology 2

Model contributions:

Model the adoption rate of technology 2 different from disengagement rate of technology 1 (\(F_2 \neq F_{12}\))

Varying \(p, q\) (for different technologies)

\(F_1\) has the same function form as \(F_1, F_2\) (because it fits the data well, and reduces to previous model which matches previous literature)

Model can be applied to both generational and technology diffusion

Model Estimation

Using nonlinear least squares to estimate the parameters that that minimize

\[ \sum_{i = 1}^n (s_{i1} - m_1 F_1(t_i)) (1 - F_{12} (t_i - \tau_2 + 1))^2 \\ + \sum_{i=1}^n (s_{i2} - F_2 (t_i - \tau_2 + 1)(m_2 + m_1F_1(t_i)))^2 \]

Segments of adopters

\[ S_2(t) = L_2(t) + DU_2(t) + SW_2(t) + O_2(t) \]

while

\[ S_1(t) = L_1(t) - CAN_2(t) = L_1(t) - (SW_2(t) + O_2(t)) \]

where

\(SW\) = switchers

\(O\) = Opportunists

\(CAN\) = Canalization

\(L\) = Leapfroggers

\(DU\) = dual -users

Market growth segment = sum(leapfroggers, dual users)

Cannibalization = sum(switchers, opportunists).

36.2.2.5 (Prins and Verhoef 2007) Marketing effects on adoption timing

Studies the effects of direct marketing and mass marketing on adoption timing (in the context of a new e-service among existing customers)

Data: 6k customers of a Dutch telecom operator over 25 months

-

Findings:

advertising shortens the time to adoption (including those by competitors)

Mass marketing has a greater effect on loyal customers (compared direct marketing)

-

Related literature:

Adoption

customer management

Adoption timing is defined as “the time between the introduction and the adoption of the new service” (p. 170) following (Jan-Benedict E. M. Steenkamp and Gielens 2003)

Switchers to competitive services are considered as non-adopters (even if they adopt comeptitor’s new service). It’s valid when the focus is on the adoption of the folca company’s new service among existing customers.

(Donkers, Franses, and Verhoef 2003) demonstrates that if oversampling is not accompanied by stratfied sampling on the independent variables, it should not affect the parameter estimates or SE for are event in binnary choice models.

Meausres of Time to adoption: For each tiem period \(t\), a customer can either adopt the new serive or not. The time to adoption for each customer is the time elasped in \(t\) since the intro of the service. Dependent vairable = indivudal time to adoption.

36.3 Take-off Disruption

Marginal Prob vs. Hazard of Death (what is the conditional probability of dying conditional on you are alive)

Sometimes we study takeoff instead of sales of new products because new products either takeoff or die, wee dont’ see flat salles. (managerial implication: invest if takeoff)

We have to wait at least till the peak of the hazard function (5 years)

Pervasiveness of disruption: US

36.3.1 Disruptive Technologies

Companies stay too close to their current customers, without accounting for future ones.

-

For each industry, there is performance trajectory that help track new technology performance in comparison with old ones’.

Sustaining technology: maintain the rate of improvement

Disruptive technology:

-

Solution to cultivate disruptive technologies:

Is the technology disruptive or sustaining?

What is the strategic significance of the disruptive technology?

Where is the initial market for the disruptive technology?

There should be a separate organization or business that handle disruptive technology

36.3.2 (Peter N. Golder and Tellis 1997) takeooff

-

Key issues:

How long does it typically take a product to take off?

Is there a takeoff pattern?

Can we predict takeoff?

If the baseline sales is small, it takes a large increase in sales to takeoff, but if the baseline sales is big, it takes only a small increase in sales to takeoff. Hence, there is a threshold for takeoff

-

Definition of takeoff: “the first year in which an individual category’s growth rate relative to base sales crosses this threshold.” (p. 256) or “the point of transition from the introductory stage to the growth stage of the product file cycle.” (p. 257)

- Metric: the first large increase in sales in the new category (still don’t quite understand)

Operational definition of takeoff: “threshold for takeoff as a plot of the percentage increase in sales relative to its base sales that demarcates the takeoff.” (p. 259)

Independent variables: price, year of introduction, market penetration (percentage of households that have purchased a new product), and controls (product specific, and economic variables)

-

Found:

price at takeoff is lower than price at the introduction stage

Average time to takeoff is 6 years

penetration at takeoff is 1.7%

Products usually takeoff around 3 price points: $1000, $500, $100

Model: Cox’s proportional hazard mode

\[ h_i(t) = h(t; z_{it}) = h_0 (t) \times e^{z_{it} \beta} \]

where

\(h_0(t)\) is the baseline hazard function

\(z_{it}\) are the independent variables

\(\beta\) is the same for all categories (questionable choice)

Do not include unbosomed heterogeneity because each event is unique (non repeated)

Samples:

- 11 consumer durables (usually studied in diffusion research)

- 10 recently introduced consumer durables

- 10 categories during the review process.

Model performance

\(U^2\) measure reduction in uncertainty

Forecasts: (1) at introduction (2) one year ahead

36.3.3 (Chandy and Tellis 2000) Incumbent’s curse

- Present this paper

- Definition: “A radical product innovation is a new product that incorporates a substantially different core technology and provides substantially higher customer benefits relative to previous products in the industry” (Chandy and Tellis 1998).

- Theory of S-curves: figure 1

- Reasons incumbents don’t like radical innovations:

Perceived incentives: prospect theory (incumbents stand to lose, innovators stand to gain)

Organizational filter: resources are invested in important tasks that yield money.

Organizational routines: repetitive tasks are very efficient.

Opportunities of incumbents: market capabilities (customer knowledge, customer franchise, market power)

- Size and incumbency are positively correlated

Theory of (bureaucratic) inertia: it’s hard to get new idea through a large firm because of filtering and screening + no incentives to do so.

Opportunities of large firms: financial and technical capabilities

- There are more nonincumbents (i.e., small firms) as innovators in the US than other countries (e.g., Japan, or Western Europe) because of (1) institution (2) culture

- Historical analysis: 1 author + 9 assistants over 4 years

- Sample frame:

Product classes: consumer durables + office products

High unit sales (> 1 mil) (from Predicasts)

Radically new technology: (1) identify the most significant product innvoaitosn in each product category (2) 3 experts rate the radicalness

- Measures

Radical innovation means (1) differences in core technology: utilizing a distinct core technology (2) superiority in user benefits:gives a lot more value to the customer than the first product in the same category.

Firm size: employees, sales volumn, value of asset from Moody’s Industrial Manual and S&P manual, for private firms: company directories - Industrial laboratories Directory, Edison Electric Light Co.

Innovator (firm that first commercialized the radical innovation) and incumbent (firms that sell previous generation product on the introduction date)

- Results: 64 out of 93 innovations have data.

- Categorical Analysis:

Large firms are more likely to be incumbents

Small firms were more radical in their innovation before the World War 2, large firms are radical in their innovation recently.

US innovators are from non-incumbent. Before the World War II, the US innovation were likely to come from smaller firms, but recent US innovation tend to come from large firms.

- Multivariate

While larger organizations have historically introduced fewer innovative inventions, the tendency in recent years has been the polar opposite.

In recent years, US corporations have developed more radical ideas than non-US firms.

- Further Analyses

Relevant Population: Large firms account for a significantly higher proportion of radical innovations when compared to its total number of firms in the economy. In any product class (incumbent vs. non), the number of incumbent is much smaller than non incumbents, but incumbents still account for half of the nubmer of radical innovations.

Alternative measure of firm size

Radical Innovator: but what if incumbents can be early entrants?

36.3.4 (Tellis, Stremersch, and Yin 2003) International Takeoff

137 products across 10 categories inn 16 countries

Parametric hazard model

Takeoff in Europe (e.g., 6 years after introductionn) is different from those in US

Time-to-takeoff varies by countries and categories

Not much evidence for the effect of culture and economic factors on inter-country differences in time-to-takeoff

Use waterfall strategy when going international.

Countries with less uncertainty avoidance will have greater adoption

Countries with higher education will have greater adoption

36.3.5 (Hauser, Tellis, and Griffin 2006)Review on Innovation

5 fields

Consumer response to innovation

Organzattion and innovation

Market entry strategies

prescriptive technique for product development processes

Defense against market entry

36.3.6 (Chandrasekaran and Tellis 2008) Global Takeoff

16 products in 31 countries

Parametric hazard model

Economic variable (developed vs. developing) (isn’t this kinda contradict (Tellis, Stremersch, and Yin 2003), product types (work vs. fun), cultural clusters, calendar time can affect takeoff time

Takeoff is getting shorter over time

36.3.7 (Sood and Tellis 2011) Predict takeoff

36.3.8 (M. Zhang and Luo 2016) Restaurant survival from Yelp

36.4 Advertising Response (Effectiveness)

Consumer response to advertising

Key issues

Does advertising work?

When, where, why and for how long?

5 effects of ad exposure

Short

Sleeper

Hysteresis

Long

Instant

Simple model of ad response

\[ S_t = \alpha + \beta A_t + \mu_t \]

- Does not capture the carryover effect

Using (Koyck 1954) model captures carryover

\[ S_t + \alpha + \beta A_t + \beta \lambda A_{t-1} + \dots + \epsilon_t \]

This is a moving average model with an infinite lag that precisely captures carryover effect of advertising

Then, we need the Koyck transformation, lag on period and multiply by \(\lambda\) (carryover effect) (\(0 < \lambda < 1\))

Then

\[ \lambda S_{t-1} = \alpha \lambda + \beta \lambda A_{t-1} + \dots + \epsilon_t \lambda \]

With subtraction,

\[ \begin{aligned} S_t - \lambda S_{t-1} &= \alpha - \alpha \lambda + \beta A_t + \epsilon_t - \epsilon_t \lambda \\ S_t &= \alpha - \alpha \lambda + \lambda S_{t-1} + \beta A_t + \epsilon_t - \epsilon_t \lambda \\ S_t &= \alpha + \lambda S_{t-1} + \beta A_t + u_t \end{aligned} \]

Pros:

An infinite lag series turns to 1 period auto-regressive model

easy to estimate

\(\lambda\) is the carryover or decay in effect of advertising

\(\beta\) = current effect of ad

\(\beta \lambda/ (1- \lambda)\) carryover effect of ad

\(\beta / (1- \lambda)\) = total effect advertising

p% duration interval = \(\log (1-p) / \log \lambda\)

If include a lagged ad term

\[ S_t = \alpha + \lambda S_{t-1} + \beta A_t + \beta_1 A_{t-1} + \mu_t \]

Separate inertia from ad carryover

separate out decay from multiple independent variables

identify shape of decay

(Clarke 1976) found major limitation of Koyck model

Aggregation bias: the larger the data interval: the larger the estimated \(\lambda\), the larger the estimated carryover effect, the longer the estimated duration of ad

People used to think the best data interval time is the inter-purchase time. But (Tellis and Franses 2006) showed that unit exposure time is the optimal data interval (the smallest interval within which advertising occurs only once and at the same time every period)

General Autoregressive distributed Lag Model (ADL, ARMA)

\[ S_t = \alpha + \lambda S_{t-1} + \lambda S_{t-2} + \dots + \beta A_t + \beta A_{t-1} + \dots + \mu_t \]

pros:

-

rich variety of decay shapes

\(\beta\) affect number and position of bumps

\(\lambda\) affect speed of decay

precursor to Vector Autoregressive model (VAR)

cons:

aggregate data at population level and time cannot identify ad exposure

aggregate time cannot identify treated period

reverse causality: ad set on expected sales

multicollinearity

Major advances in ad response modeling:

-

Dis-aggregate data

modeling at individual household, consumer

modeling by day, hour

modeling moment-to-moment

modeling exposure (not $)

-

quasi-experiments

DID

Synthetic control

36.4.1 (Tellis, Chandy, and Thaivanich 2000) Direct TV ad

Study Context

A referral is “a call by a customer for the firm’s service” (p. 33)

-

Theory of message repetition:

A current effect on behavior

A carryover effect on behavior

A non behavior effect on attitude and memory

-

Research questions:

-

Given current brand equity, what is the effect of advertising on referrals?

Ad placement

Creatives

Time period

Age and repetition

Is marginal benefit greater than marginal cost for advertising?

-

Model

\[ R_t = \alpha + \gamma_1 R_{t-1} + \gamma_2 R_{t-2} + \gamma_3 R_{t-3} + \dots \\ + \beta_0 A_t + \beta_1 A_{t-1} + \beta A_{t-2} + \dots + \epsilon \]

where

\(A\) = advertising

\(R\) = referral

Controls: Opening hour + time of the day.

Expect:

Morning ads have longer decay than other time

Differences in creatives

Transfer function analysis

temporal patterns: auto correlations + partial auto-correlation show patterns at the hourly and weekly level

-

Lag structure: 3 lags on the dependent, and 4 lags on the independent (advertising)

-

Why there are lags of the dependent variable:

Algebraic: if didn’t have of the dependent, the independent lag would be infinite

Intuitive: separate the effect of carry over effect of advertising and inertia.

-

Error patterns:

\[ R_t = \alpha + v(\mathbf{B})A_t +N_t \]

where

\(R_t, A_t\) stationary

\(v(\mathbf{B})\) transfer function of advertising on referrals where \(v(\mathbf{B}) = Cw(B)B^b / \delta(B)\)

\(N_t = [\theta(B) / \phi(B)](1- B)^d a_t\) where \(a_t \sim N(0)\)

Advertising Effects (decay)

Total effects of advertising = sum of ad coefficients divided by (1 - sum of lag-referral coefficients)

\[ \text{Total Effect} = \frac{\sum_{l = 0}^n \beta_l }{(1- \sum_{j=1}^p \lambda_l)} \]

where \(l\) is the index for the time lag

and the partial advertising effect at each time period is

\[ TA_{t-l} = \beta_l A_{t-l} + \sum_{j=0}^l \lambda_j TA_{t-l+j} \]

Results

Advertising effect dissipate after 8 hours

Ad Effectiveness varies by station

Creatives also varies

36.4.2 (Tellis and Franses 2006) Optimal Data Interval for estimating ad response (on sales)

- Such a seminal paper

- This could also be applied to firm optimal interval for estimating announcement effect on stock performance.

Too disaggregate does not lead to disaggregate bias

Optimal interval is unit exposure time (not inter-purchase time)

To get the true estimates, it depends on the unit exposure time (instead of assumption of the advertising process)

Definition:

| Term | Definition |

|---|---|

| Data Interval | temporal level of the records |

| Inter purchase time | Smallest calendar time between any two consumer purchases |

| Duration Interval | Length of time that advertising effect lasts |

| Calendar time | Discrete time period |

| Exposure time | Moment a pulse of ad first hits a consumer |

| p% duration interval | length of time that accounts for \(p\)% of the advertising effect |

| Current effect of ad | portion of the total advertising effect that occurs in the same time period as the exposure |

| Duration interval bias | carryover effect estimated at the true interval - estimated on aggregate data |

Optimal interval balances between storage cost and estimate unbiasedness

Koyck model

- \(s_t, a_t\) are sales and ad at the true microdata interval

\[ s_t = \mu + \beta a_t + \beta \lambda a_{t-1} + \beta \lambda^2 a_{t-2} + \dots + \epsilon_t \]

where

\(\epsilon \sim N(0, \sigma^2_\epsilon)\)

\(\beta\) = current effect of advertising

\(\beta/(1- \lambda)\) = carryover effect

\(\lambda\) determines the duration interval (what do we call this term)

Using (Koyck 1954) transformation (i.e., multiply both sides by \(1 - \lambda L\) where \(L\) is the familiar lag operator \(L^k y_t = y_{t-k}\)) then

\[ s_t = \lambda s_{t-1} + \beta a_t + \epsilon_t - \lambda \epsilon_{t-1} \]

For aggregate data, denote \(S_T\) as the aggregate sales series from aggregating sales in the \(K\) periods from the current to the \(K-1\) prior period that are sampled at the current period

\[ \begin{aligned} S_T &= s_t + s_{t-1}+ s_{t-2}+ \dots + s_{t-(K-1)} \\ & = (1 + L + L^2 + \dots + L^{K-1})s_t \end{aligned} \]

Hence,

\[ A_T = (1 + L + L^2 + \dots + L^{K-1}) a_t \\ \epsilon_T = (1 + L + L^2 + \dots + L^{K-1}) \epsilon_t \\ S_{T-1} = (1 + L + L^2 + \dots + L^{K-1}) s_{t-K} \]

The true aggregate form of the micromodel

\[ S_T = \lambda^K S_{T-1} + \beta A_T + \beta \lambda (1 + \lambda L + \lambda^2 L^2 + \dots + \lambda^{K-1} L^{K-1}) \\ \times (1 + L + \dots + L_{K-1})a_{t-1} + \epsilon_T - \lambda^K \epsilon_{T-1} \]

The bias stem from the fact that

\[ A_{T-1} \neq (1 + \lambda L + \lambda^2 L^2 + \dots + \lambda^{K-1} L^{K-1}) \\ \times (1 + L + \dots + L_{K-1})a_{t-1} \]

because it was lost in aggregation

With optimal data interval (1 exposure pulse per interval), we can recover the carryover effect

\[ \frac{\beta_1 + \beta_2}{1 - \lambda^K} \]

and the true duration interval is

\[ \sqrt[K]{\hat{\lambda}^K} \]

the the current effect is \(\beta\)

When we have even more dis aggregate data than the optimal interval, we just have to adjust the formula to recover the true effects.

36.4.3 (T. S. Teixeira, Wedel, and Pieters 2010) Ad Pulsing to prevent consumer ad avoidance

Model: probit with MCMC

Data: eye-tracking on 31 commercials for 2000 participants.

New metric to predict attention dispersion based on eye-tracking data.

-

Optimization of ads:

problem: minimize avoidance subject to a given level of brand activity level

Solution: Pulsing

36.4.4 (Sethuraman, Tellis, and Briesch 2011) Advertising effectiveness meta-analysis

Data: 1960 - 2008, 56 studies.

Average short-term ad elasticity is .12

a decline in the advertising elasticity over time.

advertising elasticity is higher

for durable goods (vs. nondurables)

in the early stage than the mature stage of the life cycle

yearly data than quarterly data

ad is measured in gross rating points than monetary terms

Long-term ad elasticity is .24

36.4.5 (Liaukonyte, Teixeira, and Wilbur 2015) TV advertising on online shopping

Impression merging process: human coders

Data: $3.4 bil spending by 20 brands, consists of traffic and transactions and content measures for 1,2224 commercials.

Dif-n-dif: 2 mins pre/post windows of time. (similar to regression discontinuity)

Action-focus content increases direct website traffic and sales conditional on visitation

Info and emotion-focus content reduce web traffic while increases purchases, and positive net effect on sales for most brands.

Imagery-focus ad content decreases direct traffic to the website

-

After the tv ad

consumer choose whether to visit the website

consumer then determine whether to buy a product

-

Data:

-

Online traffic: comScore Media Metrix

Direct traffic

Search engine referrals

Transaction Count

TV Ad Data: Kantar Media

-

Argument for no endogeneity problem is that brands can’t manipulate the exact time the ad will air. (since hte ad will be placed in a 15-min window while the research design looks at the 4 minutes windows). For the case that the authors look at the 2-hour window, they use the dif-n-dif design where they pick the largest brands within each product category that did not advertise

36.4.6 (Tirunillai and Tellis 2017) TV ad on Online chatter: synthetic control

Raw metrics

- Reviews: from Amazon, Epinions, cnet, twitter, YouTube, Facebook

Volume of reviews

valence of the review (positive vs. negative)

Polarity (entropy)

- Blogs: from Spinn3r

Volume

In-degree (links) of the brand website

In-degree (links) of blog posts

Volume of blogs that gain/lose rank

Using Dynamic factor analysis

\[ Y_t = \xi f_t + \epsilon_t \\ f_t = \Psi f_{t-1} + \eta_t \]

where

\(Y_t\) raw measure of reviews and blogs

\(f_t\) is the underlying factors

\(\xi\) is the factors loadings

\(\epsilon\) idiosyncratic error

\(\eta\) = white noise where \(E(\epsilon_t \eta'_{t-k})=0\)

Dimension of chatter (using dynamic factor analysis)

-

Content-based dimensions:

Popularity: loads on volume of reviews and blogs

Negativity: loads positively on positive valence and polarity and negatively on positive valence

-

Information spread dimensions:

Visibility: loads on the volume of blogs and the in-degree links of the brand website

Virality: loads on volume of blogs that gained rank and in-degree of the blogs

TV ad causally increases a short positive effect on online chatter (info-spread > content-based)

Ad can reduce the negativity in online chatter in the short-term.

Ad can

simulate conversation online

trigger brand recall

Interpreting experience: give more favorable assessment toward the brand

Refute negatives: greater credibility and persuasiveness

Empirical Setting: A campaign: Let’s Do Amazing (ad duration). 20 days after the campaign date)>

Method:

Synthetic control (synthetic brand): the difference might already account for the spillover effect of the focal brands on other brands in the same industry (authors argue that there was no spillover effect).

No justification for 70 days before and 20 days after

To make sure YouTube did not affect much, the authors use data from Visible Measures to assess viewership, and TV viewership from https://tvlistings.zap2it.com/?aid=gapzap and Nielsen TV Ratings and Stradegy (need to ask about this company).

Authors also use Vector Auto-regressive model to examine the short-term and long-term dynamics between the dependent (chatter metrics) and independent variables (advertising).

36.5 Marketing Return

Event Analysis

Nature of series

- Continuous

Univariate: Class Bass, Classic FDA

Multivariate Unidirectional: functional regression, classic Koyck, ADL, ARIMA

Multivariate Multidirectional: VAR, VARX, PVAR, Simultaneous Equation

- Punctuated

Event is dependent: Hazard models, split hazard, bivariate hazard

Evident is independent: Event analysis, synthetic control, DID

Decreasing rigor of causal inference

- Lab Experiment

- Field Experiment

- Nature Experiment

- Instrumental Variables

- Granger causality (improves with shocks)

- Times series regression (improves with shocks)

- Cross-sectional regression

Levels of testing causality in field

Correlation

Multiple regression: control for other plausible causes

Times series model (use of current and past values: Koyck, ADL, ARIMA)

First differences (effect of changes)

Lag of first differences (Arellano & Bond)

Granger causality (use of only past values of independent variables + control of past values of dependent variables (VAR), preferably in differences).

Intervention or event analysis

Natural experiments

RCT

Concept of Abnormal Return:

Stock price (\(P_t\)) = random walk

Return = \(P_t - P_{t-1}\) = white noise

Panel Regression

Sample similar firms, \(j\)

Identify each of their similar events: First stage regression (WRDS)

Estimate abnormal returns of each of these firms associated with each of those events \(e_{jt}\)

2nd stage: equation

Pool abnormal returns

Estimate factors that may affect the distribution of \(e_{jt}\)

Strength of event analysis

Increases with clearly defined event, narrow window of treatment, removal of confounding events

Long time series for baseline

large number of firms

diverse contexts of treatments

Extraction effects of known predictors

temporal dependent series (returns)

punctuated independent series: event

Focus on effects of event on series of returns

simulates a natural experiment

Define: a natural or artificial shock

Types of natural experiments:

Compare treated vs. untreated

compared before and after

DiD

Synthetic control

Types of pre-temporal controls

One prior period

baseline of prior period

synthetic control

function of known factors (Fama-French 4)

Cross-over (treated becomes control and rev)

Time capsule in Marketing

| Event | Source |

|---|---|

| market Entry | Factiva, Lexis-Nexis |

| new product | Factiva, Thomson Reuters |

| Consumers satisfaction | CSI |

| Innovation activities | Factiva, Cap IQ |

| Acquisitions | Factiva, SDC platinum |

| Quality | Web chat, product reviews |

| Advertising | TNS Stradegy, YouTube |

| Recalls | Govt web, others |

| Sales | Yahoo fin, 10k GFK, euromonitor, Nielsen |

| Earnings | SEC Filings |

| Stock Prices | CRSP, WRDS |

36.5.1 (Fornell et al. 2006) Customer satisfaction and stock return

Historically, people understand that customer satisfaction affects firm economic performance. But we haven’t studied the relationship between customer satisfaction and stock performance.

People don’t incorporate the info about customer satisfaction into the stock price right away (market is not so efficient)

-

From the literature, we understand that there are 4 determinants of a company’s market value

Acceleration of cash flow: speed of buyer response marketing efforts

increase in cash cash flows: repeat business and low marginal costs of sales

reduction in cash flow risk: lower by satisfaction

increase in the residual value of the business

Data: Compsutat + American Customer Satisfaction Index

Regression (correlation) analysis

\[ \ln Market value = \alpha + \beta_1 \ln Book value \\ + \beta_2 \ln Bookvalueliability + \beta_3 \ln ACSI \]

There is evidence for a correlation market value and customer satisfaction.

However, investors don’t always respond positively to increased satisfaction news

The firms is giving away consumer surplus

firms that already have leads over competition

Why trade-off between satisfaction and productivity

reverse causality

timing expectation (i.e., measurement of satisfaction)

36.5.1.1 Event study

- Suing market model to estimate abnormal return

\[ AR_{jt} = R_{jt} - (\alpha_j + \beta_j R_{mt}) \]

where \(j\) = firm, and \(t\) = day

estimation period = 255 days ending 46 days before the event date (McWilliams and Siegel 1997)

one-day event period = day when Wall Street Journal publish ACSI announcement.

-

5 days before and after event to rule out other news (PR Newswire, Dow Jones, Business Wires)

M&A, Spin-offs, stock splits

CEO or CFO changes,

Layoffs, restructurings, earnings announcements, lawsuits

No evidence for the effect of ACSI on CAR

36.5.2 (S. Srinivasan and Hanssens 2009) Marketing and Firm Value

Marketing investments don’t always translate to firm value readily.

-

Marketing investments are typically intangible:

brand equity

customer equity

customer satisfaction

R&D

product quality

specific marketing-mix actions

-

Market is not so efficient: e.g.

- Intangible-intensive firms are usually undervalued (Lev 1989)

Market Valuation Modeling:

-

Fame-French factor explains excess returns come from

market risk factor: excess return on a broad market portfolio

size risk factor: difference in return between a large and small cap portfolio

value risk factor: difference in return between high and low book-to-market stocks

Momentum: Carhart (1997)

-

Metrics:

Top-line (revenue)

bottom-line (earnings) surprises

Methods: 4-factor model can still have omitted variables

Metrics on Marketing and Firm value

-

Market cap: need to

isolate the book value (using Tobin’s q)

Incorporate random-walk behavior in stock prices (first difference of log(stock price))

stock returns

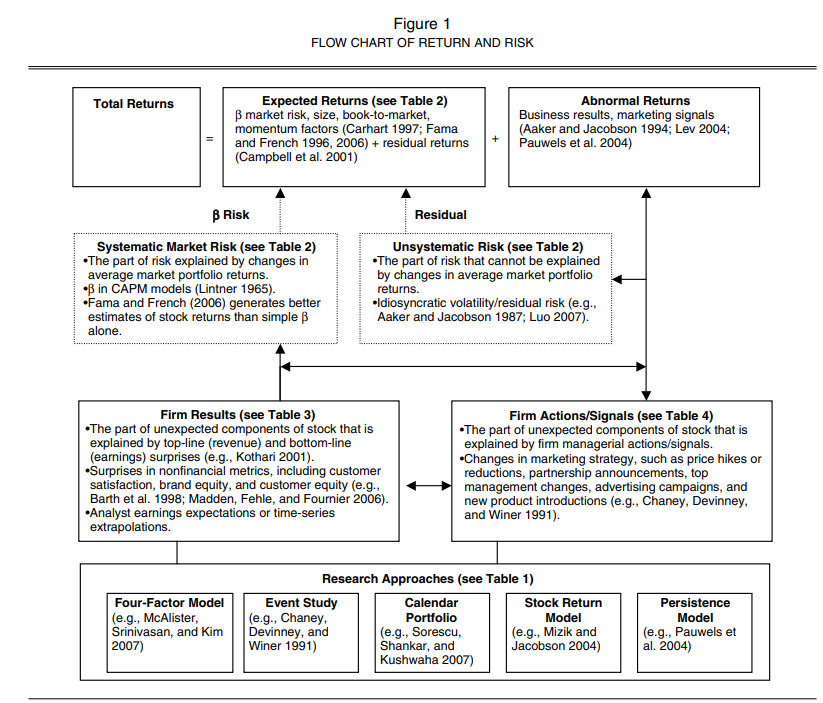

| Method | Characteristics | Litimations | Examples | Dependent/Independent |

|---|---|---|---|---|

| Four Factor Model | Assume efficient market theory |

sensitive to benchmark portfolio correlation analysis can contain omitted variable bias examine cross-sectional variation only |

Tobin’s q/ Branding strategy Firm val/ brand value estimates Stock returns/ brand valuation |

|

| Event Study |

Assume efficient market Causal Analysis |

can’t measure long-term effect |

(Horsky and Swyngedouw 1987): name change (Chaney, Devinney, and Winer 1991): new product intro (Lane and Jacobson 1995): brand extension |

Stock returns/ name events Stock returns/ new product intro Stock returns/ brand extensions Stock returns/ Internet channel |

| Calendar protfolio |

Include firms with certain to measure long-term impact more accurate than event studies |

Can’t measure per event effect might be sensitive to benchmark prtofolio |

(A. Sorescu, Shankar, and Kushwaha 2007) | Stock returns/ new product |

| Stock return response model |

based on Carhart (1997) and EMH account dynamic properties of stock returns incorporate continuous events |

detailed data at the brand so business unit level marketing info must be public single equation model without temporal chain |

(D. A. Aaker and Jacobson 1994) |

Stock returns/ perceived quality Stock return / brand attitude stock return/ strategic shifts Stock returns/ marketing actions |

| Persistence modeling |

system of equations: consumer (demand equation), manager (decision rule equation), competition, (competitive reaction equation), investor (stock price equation) VAR: examines both short-term and long-term robust to deviations from stationarity incorporate dynamic feedback loops |

detailed data at the business unit level time-series over a long horizon reduced-form models |

Firm value/ new product intro, sales promotions stock returns/ advertising |

4 factor model:

\[ R_{it} - R_{rf,t} = \alpha_i + \beta_i (R_{mt} - R_{rf,t}) + s_i SMB_t \\ h_i HML_t + u_i UMD_t + \epsilon-{it} \]

where

\(R_{it}\) = stock return for firm \(i\) at time \(t\)

\(R_{rf,t}\) = risk-free rate in period \(t\)

market factor = \(R_{mt}\) = market return in period \(t\)

Size factor = \(SMB_t\) = return on a value-weighted portfolio of small stocks - the return of big stocks

Value factor = \(HML_t\) = return on a vlaue-weighted portfolio of high book-to-market stocks - return on a value-wegihted portfolio of low book-to-market stocks

Momentum factor \(UMD_t\) = average return on 2 high prior-return portfolio - the average return on two low prior return portfolio

36.5.3 (Sood and Tellis 2009) Innovation and Stock Return

Innovation is important for firms

But firms are cautious when investing in R&D (long-term effect hard to justify)

Finding: innovations effect on stock prices is underestimated when events are distinct vs. aggregate

3 types of innovation activities

- Initiation: alliance, funding, expansions

- Development: Prototypes, patents

- Commercialization: Porudct Launch, awards

Takeaways

Total market returns to an innovation project: 643 mil (compared to 49 mil the return to an average event in the innovation project)

Positive events increase returns for all three types of events

Negative events decrease return for development and commercialization stages only

The absolute value of the market returns is higher for negative announcements than for positive announcements

36.5.4 (Jacobson and Mizik 2009b)

Disagreeing with previous research conclusion that there was a systemic mispricing of customer satisfaction into the stock price (Fornell et al. 2006) (Aksoy et al. 2008), the anomaly stem from only a small group of satisfaction leaders in the computer and internet sector. (i.e., sampling bias).

This study is consistent with (O’Sullivan, Hutchinson, and O’Connell 2009)

36.5.5 (Jacobson and Mizik 2009a)

36.5.6 (Borah and Tellis 2014) Choice of Payoff from announcements (Innovations)

- Whether a firm should make, buy or ally regarding new technologies

Innovation phases:

- Initiation

Make

Buy

Ally

- Development

- Commercialization

New product launch

initial shipments

new app and markets for the new products

awards

Models

- Model of returns

- Model of investment choice: multinomial logit model

- Model of payoffs:

36.5.7 (Tirunillai and Tellis 2012) Chatter effect on stock performance

Research questions:

Cor(UGC, stock performance)

What is the direction of causality

Among the UGC metrics, which best relates to stock performance

What are the dynamics of the relationship in terms of wear-in, war-out, and duration?

Data: 4 years, 6 markets , 15 firms

Findings:

Volume of chatter increases abnormal returns by a few day (using Granger causality tests) and trading volume

Positive UGC has no effect on abnormal returns

Negative UGC has negative effect on abnormal returns with a short “wear-in” and long “wear-out”

Interaction between chatter volume and negative chatter have a positive effect on trading volume

negative UGC positively correlates with idiosyncratic risk

Positive UGC has no effect on the idiosyncratic risk

Offline ad also increases the volume of chatter and decreases negative chatter

UGC:

- Product reviews + product ratings

Stock performance:

A measure of shareholder value

Available at the daily level

Assumption:

Market is not efficient: it takes time for the market to reflect info about UGC.

-

Asymmetric response across UGC metrics:

Losses loom larger than gain

investors discount positive info because it’s unreliable

Positive messages are usually influenced by the firms, but not negative

Sampling:

Product categories that have rich data on UGC (digital, high tech and popular consumer durable)

Product categories that reviews are related to sales

Public firm only

No M&A during the period

The sample markets should be representative of the whole market.

Time: June 2005 - Jan 2010

Media:

Product reviews instead of text or videos, etc because intuitively people use this form to express their opinion

Consumer reviews instead of evaluations, blogs, forums, because it’s more focused and greater signal-to-noise ratio

Consumer reviews instead of expert review because of wisdom of the crowds

3 popular websites: Amazon.com, Epinions.com, Yahoo! Shopping.

ratings + text reviews

Measures

UGC: ratings, volume chatter, positive valence, negative valence

-

Stock market performance

Abnormal returns: Fame-French (1993) three-factor + Carhart 1997 momentum factor.

Idiosyncratic risk: same model as abnormal returns

Trading volume: = daily turnover = volume of trade / shares outstanding at the end of the day

Using EGARCH specification:

\[ R_{i,t} - R_{f,t} = \alpha_i + \beta_{i, MKT} (R_{MKT, t} - R_{f,t}) + \beta_{i, SMB} SMB_t \\ + \beta_{i, HML} HML_t + \beta_{i, MOM} MOM_t + \epsilon_{i,t} \]

where

- \(\epsilon_{i,t} \sim N(0, \sigma_{i,t})\)

\[ \ln(\sigma^2_{i,t} ) = a_i + \sum_{j = 1}^p b_{i,j} \ln (\sigma^2_{i,t-j}) \\ + \sum_{k=1}^q c_{i,k}\{ \Theta (\frac{\epsilon_{i, t - k}}{\sigma_{i, t - k}}) + \Gamma (| \frac{\epsilon_{i, t-k}}{\sigma_{i, t-k}}| - (\frac{2}{\pi})^{1/2})\} \]

Control Variables

Analysts’ Forecasts: IBES Database

Advertising: TV ad from TNS media Intelligence

Media Citations: Number of articles in print media from LexisNexis (with relevancy score above 60%) and Factiva (using company tag)

New product Announcement: also LexisNexis and Factiva (following (Sood, James, and Tellis 2009))

Models

Vector Auto-regression (VAR)

can handle continuous events (instead of discrete events used in event studies)

account for immediate and lagged-term of the independent variables

capture the carryover effects over time with the generalized impulse response function

Controls for trends, seasonality, non-stationary, serial correlation, and reserve causality (Luo 2009)

Procedure

- Estimate the stationary (unit roots + co-integration) properties of stock performance and UGC

Stationarity test: Augmented Dickey-Fuller test + Kwiatkowski-Philips-Schmidt-Shin test

Co-integration: Johansen’s procedure (Johansen et al. 1992)

- Granger causality test

- Estimate dynamics of carryover effect using impulse response function

- Not sensitive to the causal ordering to the causal ordering of the variable in the system of equations

- Estimate the effect of UGC using variance decomposition: relative importance of metrics of UGC

36.6 Creativity

Implications of social media

- Wisdom of the Crowds

- Advertising almost free

36.6.1 (Bayus 2013) Crowdsourcing New Product Ideas over Time

from dell’s IdeaStorm community, serial ideators are more likely to have 1 idea that the organization will implement, but they don’t repeat this success.

-

Negative effect of past success can be mitigated for idators with more diverse commenting activity

- Fixation effect = unconscious plagiarism (or cryptomnesia) (R. L. Marsh and Landau 1995) (R. L. Marsh, Ward, and Landau 1999)

-

Good

First paper to study crowdfunding of ideas

Good theory: fixation effect

Good descriptive analysis

-

Cons

- Model: not taken into account rare events.

36.6.2 (Toubia and Netzer 2017) Idea generation, creativity, prototypicality

Creativity = balance(novelty , familiarity)

Beauty in avergeness effect

Automate read ideas to identify promising ones

Research questions

- How novelty and familiarity defined in the idea generation context? From literature using Geneplore

“novelty is the association of word stems that do not appear frequently together in text related to the topic under consideration” (p. 3)

“familiarity is the association of word stems that appear frequently together” (p. 3)

- How should novelty and familiarity be measured? semantic network co-word analysis (by the combinations of word stem instead of the word itself)

- What is the optimal balance between novelty and familiarity? beauty in averageness effect

idea = “a document made of words that attempts to add value given a particular idea generation topic” p. 2

Automatically recommend words to improve idea

Baseline for semantic network:

Pre-test idea: consumers generate initial set of ideas on a topic

Google results: top search (might be biased to high-quality contents)

Used Jaccard index for edge weights

Control variables: (Barrat, Barthélemy, and Vespignani 2007)

Frequencies of nodes in the network: average edge weight, coefficient of variation of edge weights, minimum edge weight, maximum edge weight, average node frequency, coefficient of variation of node frequencies, minimum node frequency, maximum node frequency, and the number of nodes in the subnetwork, length of the idea using number of characters

Clustering coefficients of the nodes in the network; average node clustering coefficient, coefficient of variation of node clustering coefficients, minimum node clustering coefficient, and maximum node clustering coefficient.

Prototypical distribution of edge weights using mean of the prototypical distribution

Measure distance between two distributions - The Kolmogorov-Smirnov statistics (2 cdfs). Alternatively could use Kullback-Leibler divergence

Idea evaluation: manual with 4 dimension: creativity, purchase interest, predicted popularity, writing quality

Alternative measure to edge weight distributions: Info retrieval literature: vector space representation: each document as a vector with dimensionality equal to the number of word stems in our dictionary (i.e., number of nodes in our semantic network

Specification of the baseline semantic network is dangerous to the sub-network distribution.

Robust to synonyms

Strengths:

Good way to measure a complex and highly qualitative construct

Good connection between the theory and method

-

Robust

- Different measures, ideas, evaluators, baseline networks.

Cons

- With other representations, the results do not hold

36.6.3 (Y. “Max”. Wei, Hong, and Tellis 2021) Machine leaning creativity

Crowdfunding: for both finance and marketing (market reaction, advertise ideas)

Combinatorial theory:

measure novelty, overshooting and undershooting, measure styles of imitation

-

Research questions

How to measure the similarity between all the projects on crowdfunding sites in an objective and automated way?

-

The relationship between the similarity pattern and funding performance

Can previous successful projects that are similar product a new project’s success?

Do people value novelty?

whether to overshoot or undershoot the funds raised?

Do people value atypicality?

Recommendation from the similarity measure

Data: 98,058 Kickstarter projects from 2009 - 2017 (from 3 categories: Film & Video, Music and publishing. only English.

-

Techniques: Semantic Similarity

Word2vec: word-level similarity

Word Mover’s Distance (WMD): Document-level similarity \(w_{ij} = \delta^{|t_i - t_j|} \times L(\gamma_0 - \gamma_1 d_{ij})\) where \(0 < \delta \le 1\) is the decay factor, \(d_{ij}\) is the WMD between 2 projects and \(L\) is the logistic function and \(\gamma\) are chosen based

-

Similarity network where each node is a project,and the strength of a link

Increases with degree of similarity

decreases with the time lapse between 2 projects

-

Funding performance

Whether the funding is successful

How much money is raised

-

Findings

The average level of success by prior projects is a good predictor of the current project’s funding performance