3.4 An example with continuous \(X\): Economic stress among small-business owners

Here’s the estress data.

estress <- read_csv("data/estress/estress.csv")

glimpse(estress)## Observations: 262

## Variables: 7

## $ tenure <dbl> 1.67, 0.58, 0.58, 2.00, 5.00, 9.00, 0.00, 2.50, 0.50, 0.58, 9.00, 1.92, 2.00, 1.42, 0.92...

## $ estress <dbl> 6.0, 5.0, 5.5, 3.0, 4.5, 6.0, 5.5, 3.0, 5.5, 6.0, 5.5, 4.0, 3.0, 2.5, 3.5, 6.0, 4.0, 6.0...

## $ affect <dbl> 2.60, 1.00, 2.40, 1.16, 1.00, 1.50, 1.00, 1.16, 1.33, 3.00, 3.00, 2.00, 1.83, 1.16, 1.16...

## $ withdraw <dbl> 3.00, 1.00, 3.66, 4.66, 4.33, 3.00, 1.00, 1.00, 2.00, 4.00, 4.33, 1.00, 5.00, 1.66, 4.00...

## $ sex <int> 1, 0, 1, 1, 1, 1, 0, 0, 1, 1, 1, 1, 1, 1, 1, 1, 1, 1, 0, 0, 0, 1, 1, 1, 0, 1, 0, 0, 0, 1...

## $ age <int> 51, 45, 42, 50, 48, 48, 51, 47, 40, 43, 57, 36, 33, 29, 33, 48, 40, 45, 37, 42, 54, 57, ...

## $ ese <dbl> 5.33, 6.05, 5.26, 4.35, 4.86, 5.05, 3.66, 6.13, 5.26, 4.00, 2.53, 6.60, 5.20, 5.66, 5.66...The model set up is just like before. There are no complications switching from a binary \(X\) variable to a continuous one.

y_model <- bf(withdraw ~ 1 + estress + affect)

m_model <- bf(affect ~ 1 + estress)With our y_model and m_model defined, we’re ready to fit.

model2 <-

brm(data = estress, family = gaussian,

y_model + m_model + set_rescor(FALSE),

chains = 4, cores = 4)Let’s take a look.

print(model2, digits = 3)## Family: MV(gaussian, gaussian)

## Links: mu = identity; sigma = identity

## mu = identity; sigma = identity

## Formula: withdraw ~ 1 + estress + affect

## affect ~ 1 + estress

## Data: estress (Number of observations: 262)

## Samples: 4 chains, each with iter = 2000; warmup = 1000; thin = 1;

## total post-warmup samples = 4000

##

## Population-Level Effects:

## Estimate Est.Error l-95% CI u-95% CI Eff.Sample Rhat

## withdraw_Intercept 1.450 0.257 0.939 1.953 4000 1.000

## affect_Intercept 0.800 0.145 0.523 1.080 4000 0.999

## withdraw_estress -0.077 0.053 -0.181 0.025 4000 1.000

## withdraw_affect 0.766 0.104 0.561 0.969 4000 1.000

## affect_estress 0.173 0.030 0.113 0.230 4000 0.999

##

## Family Specific Parameters:

## Estimate Est.Error l-95% CI u-95% CI Eff.Sample Rhat

## sigma_withdraw 1.139 0.048 1.048 1.232 4000 0.999

## sigma_affect 0.686 0.031 0.628 0.750 4000 1.000

##

## Samples were drawn using sampling(NUTS). For each parameter, Eff.Sample

## is a crude measure of effective sample size, and Rhat is the potential

## scale reduction factor on split chains (at convergence, Rhat = 1).The ‘Eff.Sample’ and ‘Rhat’ values look great. Happily, the values in our summary cohere well with those Hayes reported in Table 3.5. Here are our \(R^2\) values.

bayes_R2(model2)## Estimate Est.Error Q2.5 Q97.5

## R2_withdraw 0.1815384 0.03849542 0.1044912 0.2572579

## R2_affect 0.1169312 0.03505706 0.0524473 0.1861113These are also quite similar to those in the text. Here’s our indirect effect.

# putting the posterior draws into a data frame

post <- posterior_samples(model2)

# computing the ab coefficient with multiplication

post <-

post %>%

mutate(ab = b_affect_estress*b_withdraw_affect)

# getting the posterior median and 95% intervals with `quantile()`

quantile(post$ab, probs = c(.5, .025, .975)) %>% round(digits = 3)## 50% 2.5% 97.5%

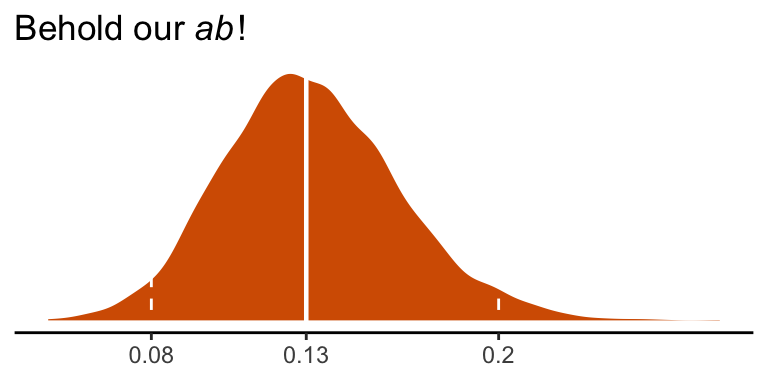

## 0.131 0.079 0.195We can visualize its shape, median, and 95% intervals in a density plot.

post %>%

ggplot(aes(x = ab)) +

geom_density(color = "transparent",

fill = colorblind_pal()(7)[7]) +

geom_vline(xintercept = quantile(post$ab, probs = c(.025, .5, .975)),

color = "white", linetype = c(2, 1, 2), size = c(.5, .8, .5)) +

scale_x_continuous(breaks = quantile(post$ab, probs = c(.025, .5, .975)),

labels = quantile(post$ab, probs = c(.025, .5, .975)) %>% round(2) %>% as.character()) +

scale_y_continuous(NULL, breaks = NULL) +

labs(title = expression(paste("Behold our ", italic("ab"), "!")),

x = NULL) +

theme_classic()

Here’s \(c'\), the direct effect of esterss predicting withdraw.

posterior_summary(model2)["b_withdraw_estress", ]## Estimate Est.Error Q2.5 Q97.5

## -0.07663292 0.05256371 -0.18050458 0.02503829It has wide flapping intervals which do straddle zero. A little addition will give us the direct effect, \(c\).

post <-

post %>%

mutate(c = b_withdraw_estress + ab)

quantile(post$c, probs = c(.5, .025, .975)) %>% round(digits = 3)## 50% 2.5% 97.5%

## 0.056 -0.053 0.165