6.3 Kernel regression with mixed multivariate data

Until now, we have studied the simplest situation for performing nonparametric estimation of the regression function: a single, continuous, predictor \(X\) is available for explaining \(Y,\) a continuous response. This served for introducing the main concepts without the additional technicalities associated to more complex predictors. We now extend the study to the case in which there are

- multiple predictors \(X_1,\ldots,X_p\) and

- possible non-continuous predictors, namely categorical predictors and discrete predictors.

The first point is how to extend the local polynomial estimator \(\hat{m}(\cdot;q,h)\;\)228 to deal with \(p\) continuous predictors. Although this can be done for \(q\geq0,\) we focus on the local constant and linear estimators (\(q=0,1\)) for avoiding excessive technical complications.229 Also, to avoid a quickly escalation of the number of smoothing bandwidths, it is customary to consider product kernels. With these two restrictions, the estimators for \(m\) based on a sample \(\{(\mathbf{X}_i,Y_i)\}_{i=1}^n\) extend easily from the developments in Sections 6.2.1 and 6.2.2:

Local constant estimator. We can replicate the argument in (6.13) with a multivariate kde for \(f_{\mathbf{X}}\) based on product kernels with bandwidth vector \(\mathbf{h},\) which gives

\[\begin{align*} \hat{m}(\mathbf{x};0,\mathbf{h}):=\sum_{i=1}^n\frac{K_\mathbf{h}(\mathbf{x}-\mathbf{X}_i)}{\sum_{i=1}^nK_\mathbf{h}(\mathbf{x}-\mathbf{X}_i)}Y_i=\sum_{i=1}^nW^0_{i}(\mathbf{x})Y_i \end{align*}\]

where

\[\begin{align*} K_\mathbf{h}(\mathbf{x}-\mathbf{X}_i)&:=K_{h_1}(x_1-X_{i1})\times\stackrel{p}{\cdots}\times K_{h_p}(x_p-X_{ip}),\\ W^0_{i}(\mathbf{x})&:=\frac{K_\mathbf{h}(\mathbf{x}-\mathbf{X}_i)}{\sum_{i=1}^nK_\mathbf{h}(\mathbf{x}-\mathbf{X}_i)}. \end{align*}\]

Local linear estimator. Considering the Taylor expansion \(m(\mathbf{X}_i)\approx m(\mathbf{x})+\nabla m(\mathbf{x})(\mathbf{X}_i-\mathbf{x})\;\)230 instead of (6.18) it is possible to arrive to the analogous of (6.21),

\[\begin{align*} \hat{\boldsymbol{\beta}}_\mathbf{h}:=\arg\min_{\boldsymbol{\beta}\in\mathbb{R}^{p+1}}\sum_{i=1}^n\left(Y_i-\boldsymbol{\beta}'(1,(\mathbf{X}_i-\mathbf{x})')'\right)^2K_\mathbf{h}(\mathbf{x}-\mathbf{X}_i), \end{align*}\]

and then solve the problem in the exact same way but now considering

\[\begin{align*} \mathbf{X}:=\begin{pmatrix} 1 & (\mathbf{X}_1-\mathbf{x})'\\ \vdots & \vdots\\ 1 & (\mathbf{X}_n-\mathbf{x})'\\ \end{pmatrix}_{n\times(p+1)} \end{align*}\]

and

\[\begin{align*} \mathbf{W}:=\mathrm{diag}(K_{\mathbf{h}}(\mathbf{X}_1-\mathbf{x}),\ldots, K_\mathbf{h}(\mathbf{X}_n-\mathbf{x})). \end{align*}\]

The estimate231 for \(m(x)\) is therefore computed as

\[\begin{align*} \hat{m}(\mathbf{x};1,h):=&\,\hat{\beta}_{\mathbf{h},0}\\ =&\,\mathbf{e}_1'(\mathbf{X}'\mathbf{W}\mathbf{X})^{-1}\mathbf{X}'\mathbf{W}\mathbf{Y}\\ =&\,\sum_{i=1}^nW^1_{i}(\mathbf{x})Y_i \end{align*}\]

where

\[\begin{align*} W^1_{i}(\mathbf{x}):=\mathbf{e}_1'(\mathbf{X}'\mathbf{W}\mathbf{X})^{-1}\mathbf{X}'\mathbf{W}\mathbf{e}_i. \end{align*}\]

The cross-validation bandwidth selection rule studied on Section 6.2.4 extends neatly to the multivariate case:

\[\begin{align*} \mathrm{CV}(\mathbf{h})&:=\frac{1}{n}\sum_{i=1}^n(Y_i-\hat{m}_{-i}(\mathbf{X}_i;p,\mathbf{h}))^2,\\ \hat{\mathbf{h}}_\mathrm{CV}&:=\arg\min_{h_1,\ldots,h_p>0}\mathrm{CV}(\mathbf{h}). \end{align*}\]

Obvious complications appear in the optimization of \(\mathrm{CV}(\mathbf{h}),\) which now is a \(\mathbb{R}^p\rightarrow\mathbb{R}\) function. Importantly, the trick described in Proposition 6.1 also holds with obvious modifications.

Let’s see an application of multivariate kernel regression for the wine dataset.

# Bandwidth by CV for local linear estimator -- a product kernel with 4

# bandwidths. Employs 4 random starts for minimizing the CV surface

bwWine <- np::npregbw(formula = Price ~ Age + WinterRain + AGST + HarvestRain,

data = wine, regtype = "ll")

bwWine

##

## Regression Data (27 observations, 4 variable(s)):

##

## Age WinterRain AGST HarvestRain

## Bandwidth(s): 3616691 290170218 0.8725243 106.5079

##

## Regression Type: Local-Linear

## Bandwidth Selection Method: Least Squares Cross-Validation

## Formula: Price ~ Age + WinterRain + AGST + HarvestRain

## Bandwidth Type: Fixed

## Objective Function Value: 0.0873955 (achieved on multistart 4)

##

## Continuous Kernel Type: Second-Order Gaussian

## No. Continuous Explanatory Vars.: 4

# Regression

fitWine <- np::npreg(bwWine)

summary(fitWine)

##

## Regression Data: 27 training points, in 4 variable(s)

## Age WinterRain AGST HarvestRain

## Bandwidth(s): 3616691 290170218 0.8725243 106.5079

##

## Kernel Regression Estimator: Local-Linear

## Bandwidth Type: Fixed

## Residual standard error: 0.2079691

## R-squared: 0.8889649

##

## Continuous Kernel Type: Second-Order Gaussian

## No. Continuous Explanatory Vars.: 4

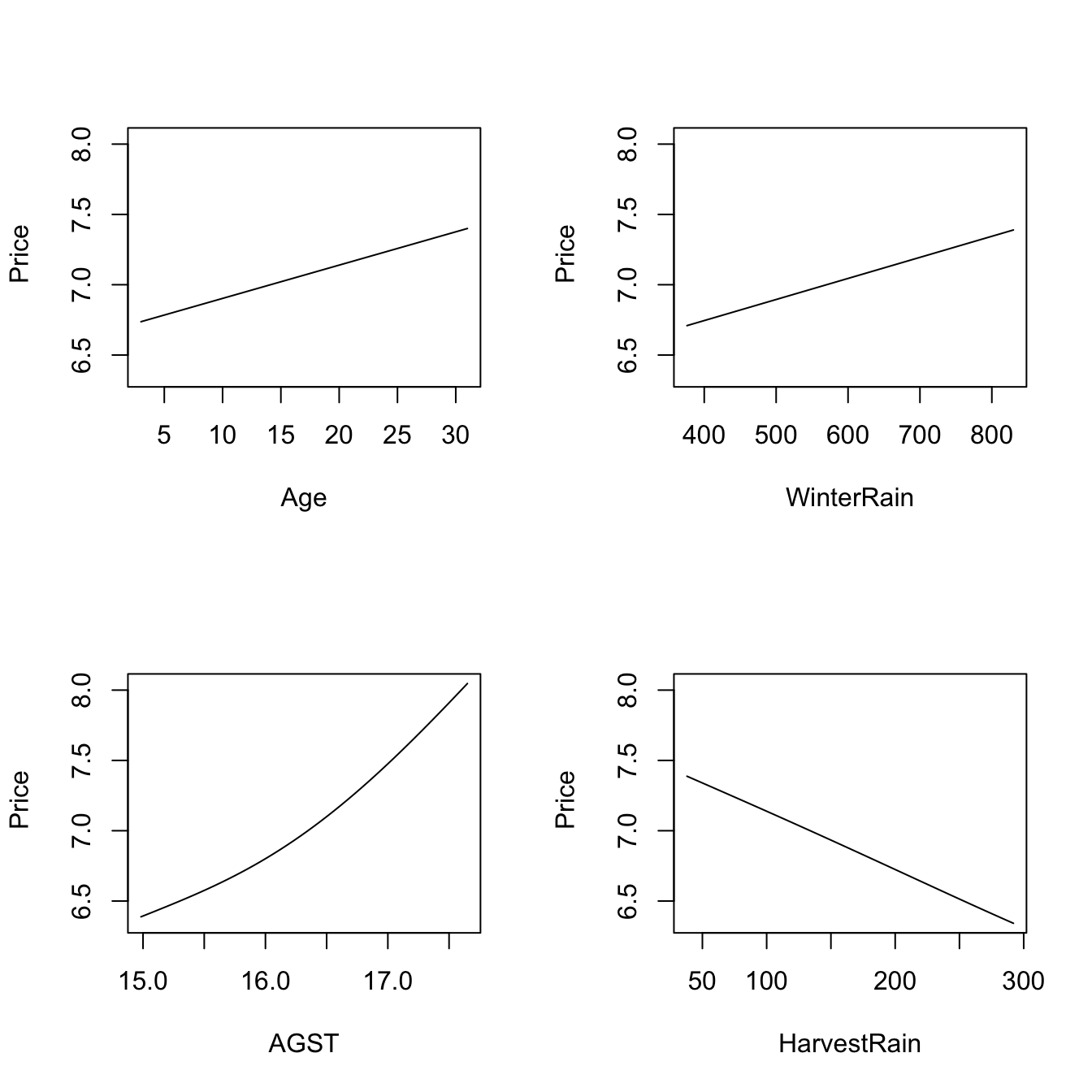

# Plot marginal effects of each predictor on the response (the rest of

# predictors are fixed to their marginal medians)

plot(fitWine)

# Therefore:

# - Age is positively related with Price (almost linearly)

# - WinterRain is positively related with Price (with a subtle nonlinearity)

# - AGST is positively related with Price, but now we see what it looks like a

# quadratic pattern

# - HarvestRain is negatively related with Price (almost linearly)

The \(R^2\) outputted by the

summary of np::npreg is defined as

\[\begin{align*} R^2:=\frac{(\sum_{i=1}^n(Y_i-\bar{Y})(\hat{Y}_i-\bar{Y}))^2}{(\sum_{i=1}^n(Y_i-\bar{Y})^2)(\sum_{i=1}^n(\hat{Y}_i-\bar{Y})^2)} \end{align*}\]

and is neither the \(r^2_{y\hat{y}}\) (because it is not guaranteed that \(\bar{Y}=\bar{\hat{Y}}\)!) nor “the percentage of variance explained” by the model – this interpretation only makes sense within the linear model context. It is however a quantity in \([0,1]\) that attains \(R^2=1\) when the fit is perfect.

Non-continuous variables can be taken into account by defining suitably adapted kernels. The two main possibilities for non-continuous data are:

Categorical or unordered discrete variables. For example,

iris$speciesis a categorical variable in which ordering does not make sense. These variables are specified in R byfactor. Due to the lack of ordering, the basic mathematical operation behind a kernel, a distance computation,232 is senseless. That motivates the Aitchison and Aitken (1976) kernel.Assume that the categorical random variable \(X_d\) has \(c_d\) different levels. Then, it can be represented as \(X_d\in C_d:=\{0,1,\ldots,c_d-1\}.\) For \(x_d,X_d\in C_d,\) the Aitchison and Aitken (1976) unordered discrete kernel is

\[\begin{align*} l(x_d,X_d;\lambda)=\begin{cases} 1-\lambda,&\text{ if }x_d=X_d,\\ \frac{\lambda}{c_d-1},&\text{ if }x_d\neq X_d, \end{cases} \end{align*}\]

where \(\lambda\in[0,(c_d-1)/c_d]\) is the bandwidth.

Ordinal or ordered discrete variables. For example,

wine$Yearis a discrete variable with a clear order, but it is not continuous. These variables are specified byordered(an orderedfactor). In these variables there is ordering, but distances are discrete.If the ordered discrete random variable \(X_d\) can take \(c_d\) different ordered values, then it can be represented as \(X_d\in C_d:=\{0,1,\ldots,c_d-1\}.\) For \(x_d,X_d\in C_d,\) a possible (Li and Racine 2007) ordered discrete kernel is

\[\begin{align*} l(x_d,X_d;\lambda)=\lambda^{|x_d-X_d|}, \end{align*}\]

where \(\lambda\in[0,1]\) is the bandwidth.

The np package employs a variation of the previous kernels. The following examples illustrate their use.

# Bandwidth by CV for local linear estimator

# Recall that Species is a factor!

bwIris <- np::npregbw(formula = Petal.Length ~ Sepal.Width + Species,

data = iris, regtype = "ll")

bwIris

##

## Regression Data (150 observations, 2 variable(s)):

##

## Sepal.Width Species

## Bandwidth(s): 898696.6 2.357536e-07

##

## Regression Type: Local-Linear

## Bandwidth Selection Method: Least Squares Cross-Validation

## Formula: Petal.Length ~ Sepal.Width + Species

## Bandwidth Type: Fixed

## Objective Function Value: 0.1541057 (achieved on multistart 1)

##

## Continuous Kernel Type: Second-Order Gaussian

## No. Continuous Explanatory Vars.: 1

##

## Unordered Categorical Kernel Type: Aitchison and Aitken

## No. Unordered Categorical Explanatory Vars.: 1

# Product kernel with 2 bandwidths

# Regression

fitIris <- np::npreg(bwIris)

summary(fitIris)

##

## Regression Data: 150 training points, in 2 variable(s)

## Sepal.Width Species

## Bandwidth(s): 898696.6 2.357536e-07

##

## Kernel Regression Estimator: Local-Linear

## Bandwidth Type: Fixed

## Residual standard error: 0.3775005

## R-squared: 0.9539633

##

## Continuous Kernel Type: Second-Order Gaussian

## No. Continuous Explanatory Vars.: 1

##

## Unordered Categorical Kernel Type: Aitchison and Aitken

## No. Unordered Categorical Explanatory Vars.: 1

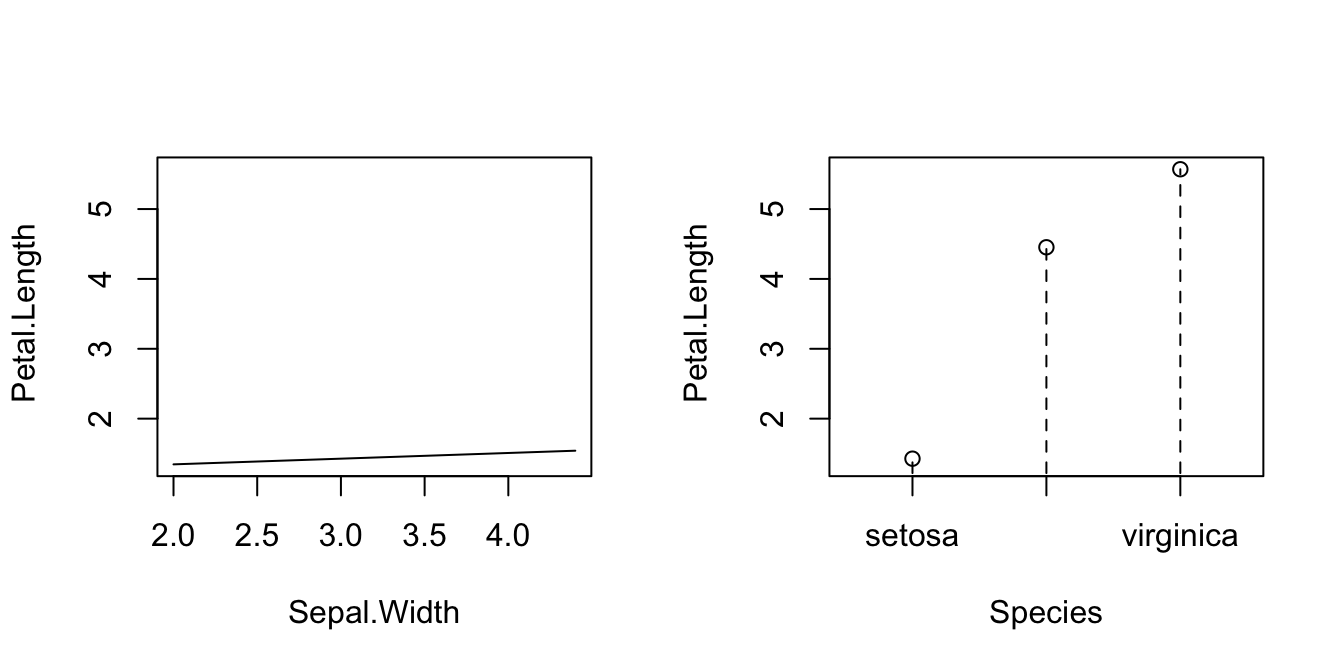

# Plot marginal effects of each predictor on the response

par(mfrow = c(1, 2))

plot(fitIris, plot.par.mfrow = FALSE)

# Options for the plot method for np::npreg available at ?np::npplot

# For example, xq = 0.5 (default) indicates that all the predictors are set to

# their medians for computing the marginal effects# Example from ?np::npreg: modeling of the GDP growth of a country from

# economic indicators of the country

# The predictors contain a mix of unordered, ordered, and continuous variables

# Load data

data(oecdpanel, package = "np")

# Bandwidth by CV for local constant -- use only two starts to reduce the

# computation time

bwOECD <- np::npregbw(formula = growth ~ factor(oecd) + ordered(year) +

initgdp + popgro + inv + humancap, data = oecdpanel,

regtype = "lc", nmulti = 2)

bwOECD

##

## Regression Data (616 observations, 6 variable(s)):

##

## factor(oecd) ordered(year) initgdp popgro inv humancap

## Bandwidth(s): 0.02413475 0.8944088 0.1940763 9672508 0.09140376 1.223202

##

## Regression Type: Local-Constant

## Bandwidth Selection Method: Least Squares Cross-Validation

## Formula: growth ~ factor(oecd) + ordered(year) + initgdp + popgro + inv +

## humancap

## Bandwidth Type: Fixed

## Objective Function Value: 0.0006545946 (achieved on multistart 2)

##

## Continuous Kernel Type: Second-Order Gaussian

## No. Continuous Explanatory Vars.: 4

##

## Unordered Categorical Kernel Type: Aitchison and Aitken

## No. Unordered Categorical Explanatory Vars.: 1

##

## Ordered Categorical Kernel Type: Li and Racine

## No. Ordered Categorical Explanatory Vars.: 1

# Regression

fitOECD <- np::npreg(bwOECD)

summary(fitOECD)

##

## Regression Data: 616 training points, in 6 variable(s)

## factor(oecd) ordered(year) initgdp popgro inv humancap

## Bandwidth(s): 0.02413475 0.8944088 0.1940763 9672508 0.09140376 1.223202

##

## Kernel Regression Estimator: Local-Constant

## Bandwidth Type: Fixed

## Residual standard error: 0.01814086

## R-squared: 0.6768302

##

## Continuous Kernel Type: Second-Order Gaussian

## No. Continuous Explanatory Vars.: 4

##

## Unordered Categorical Kernel Type: Aitchison and Aitken

## No. Unordered Categorical Explanatory Vars.: 1

##

## Ordered Categorical Kernel Type: Li and Racine

## No. Ordered Categorical Explanatory Vars.: 1

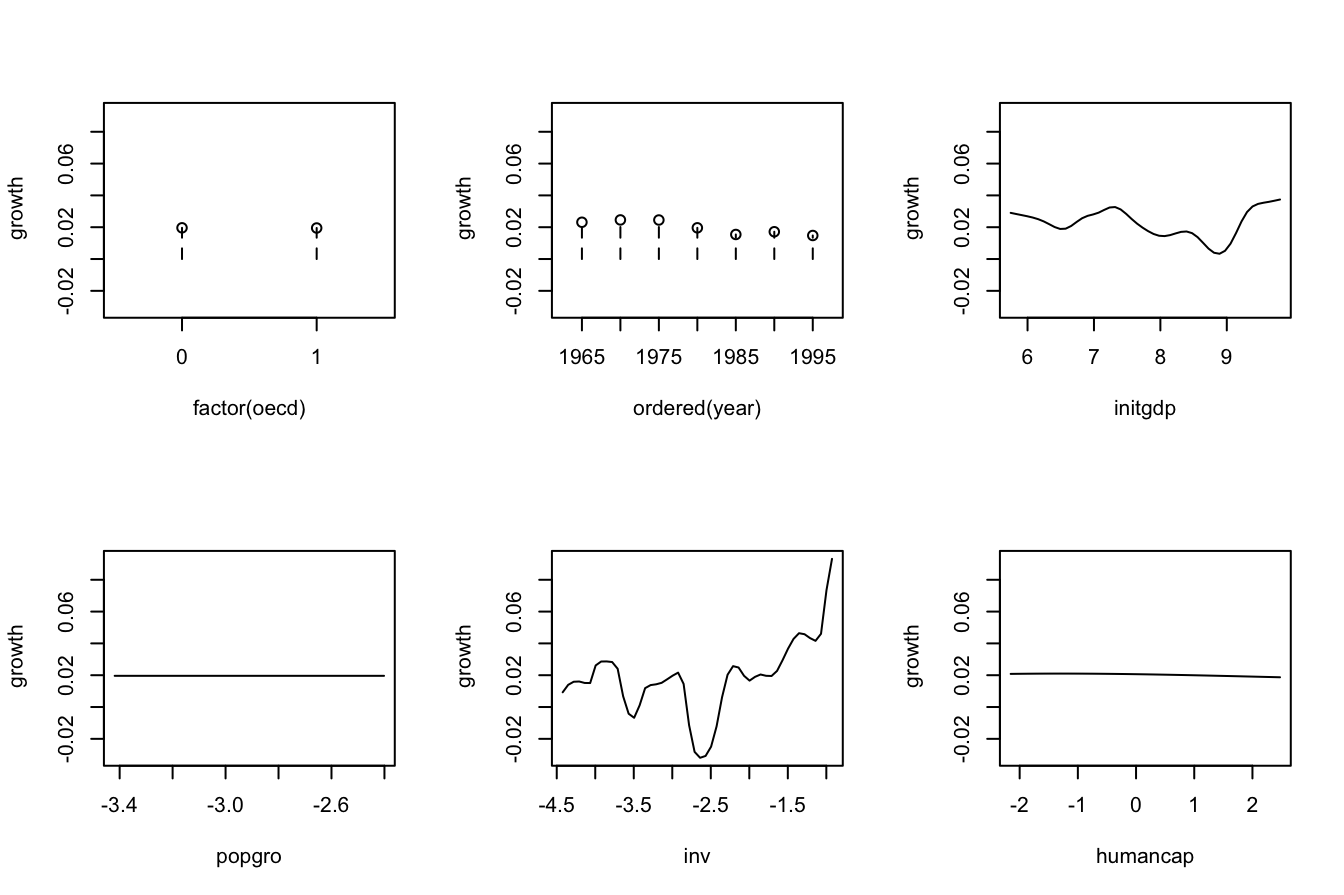

# Plot marginal effects of each predictor

par(mfrow = c(2, 3))

plot(fitOECD, plot.par.mfrow = FALSE)

References

Now \(q\) denotes the order of the polynomial fit since \(p\) stands for the number of predictors.↩︎

In particular, the consideration of Taylor expansions of \(m:\mathbb{R}^p\rightarrow\mathbb{R}\) of more than two orders that involve the consideration of the vector of partial derivatives \(\mathrm{D}^{\otimes s}m(\mathbf{x})\) formed by \(\frac{\partial^s m(\mathbf{x})}{\partial x_1^{s_1}\cdots \partial x_p^{s_1}},\) where \(s=s_1+\cdots+s_p.\) For example: if \(s=1,\) then \(\mathrm{D}^{\otimes 1}m(\mathbf{x})\) is just the transpose of the gradient \(\nabla m(\mathbf{x})';\) if \(s=2,\) then \(\mathrm{D}^{\otimes 2}m(\mathbf{x})\) is the column stacking of the Hessian matrix \(\mathcal{H}m(\mathbf{x});\) and if \(s\geq3\) the arrangement of derivatives is made in terms of tensors containing the derivatives \(\frac{\partial^s m(\mathbf{x})}{\partial x_1^{s_1}\cdots \partial x_p^{s_1}}.\)↩︎

The gradient \(\nabla m(\mathbf{x})=\left(\frac{\partial m(\mathbf{x})}{\partial x_1},\ldots,\frac{\partial m(\mathbf{x})}{\partial x_p}\right)\) is a row vector.↩︎

Recall that now the entries of \(\hat{\boldsymbol{\beta}}_\mathbf{h}\) are estimating \(\boldsymbol{\beta}=\left(m(\mathbf{x}), \nabla m(\mathbf{x})\right)'.\)↩︎

Recall \(K_h(x-X_i).\)↩︎