7.7 Combining two indicators: EMA and RSI

Test the following strategy using EMA and RSI based on day trading:

Buy signal based on EMA rule.

Sell signal based on RSI rule.

Tie-breaking: buy-signal has priority

We use 14-day RSI and use 70 as threshold for selling.

We will use MSFT to illustrate. We use the closing price and calculate the daily return.

price <- Cl(MSFT)

returnMSFT <- (Cl(MSFT) - Op(MSFT))/Op(MSFT)Then we calculate the indicator for filter rule and rsi.

delta<-0.005

r <- price/Lag(price) - 1

n <- 14

rsi <- RSI(price, n) We calculate the signal based on the trading rule. Note that the trading rule cannot be started until all information is ready. Hence, the first n day have signal value of zero.

signal <-c()

signal[1:n] <-0

for (i in (n+1):length(price)){

if (r[i] > delta){

signal[i]<- 1

} else if (rsi[i] > 70){

signal[i]<- -1

} else

signal[i]<- 0

}

signal<-reclass(signal,price)Finally, we evaluate trading rule based on day trading.

EMA.RSI.trade <- Lag(signal)

EMA.RSI.ret<- returnMSFT*EMA.RSI.trade

names(EMA.RSI.ret) <- 'Combined'

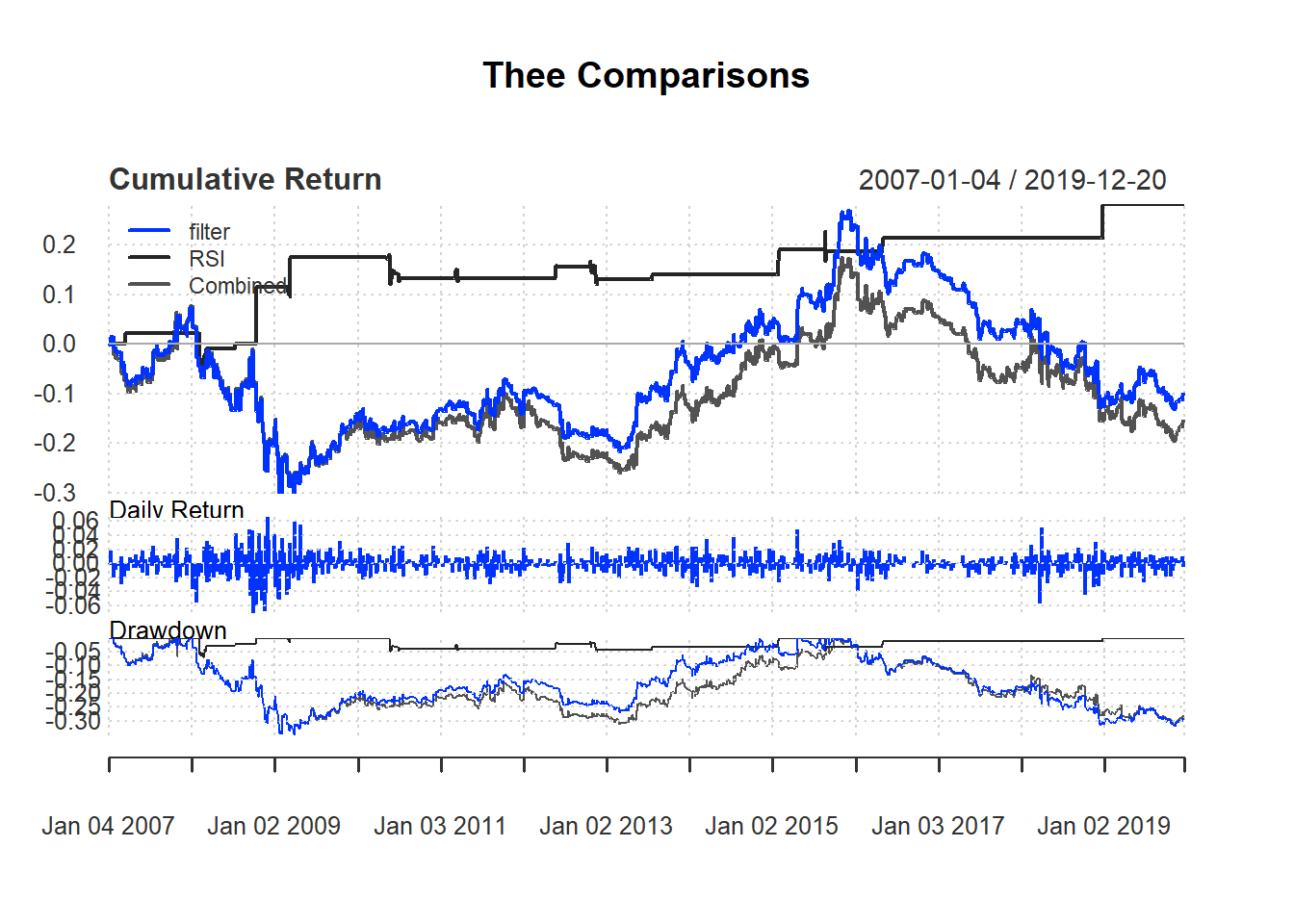

retall <- cbind(filter.ret, RSI.ret, EMA.RSI.ret)To draw trade performance summary with different colors, we use the option colorset. Common options includes redfocus, bluefocus, greenfocus, rainbow4equal andrich12equal.

charts.PerformanceSummary(retall,

main="Thee Comparisons",

colorset=bluefocus)