Three ways to do it in program R

- Using scalar calculus and algebra (kind of)

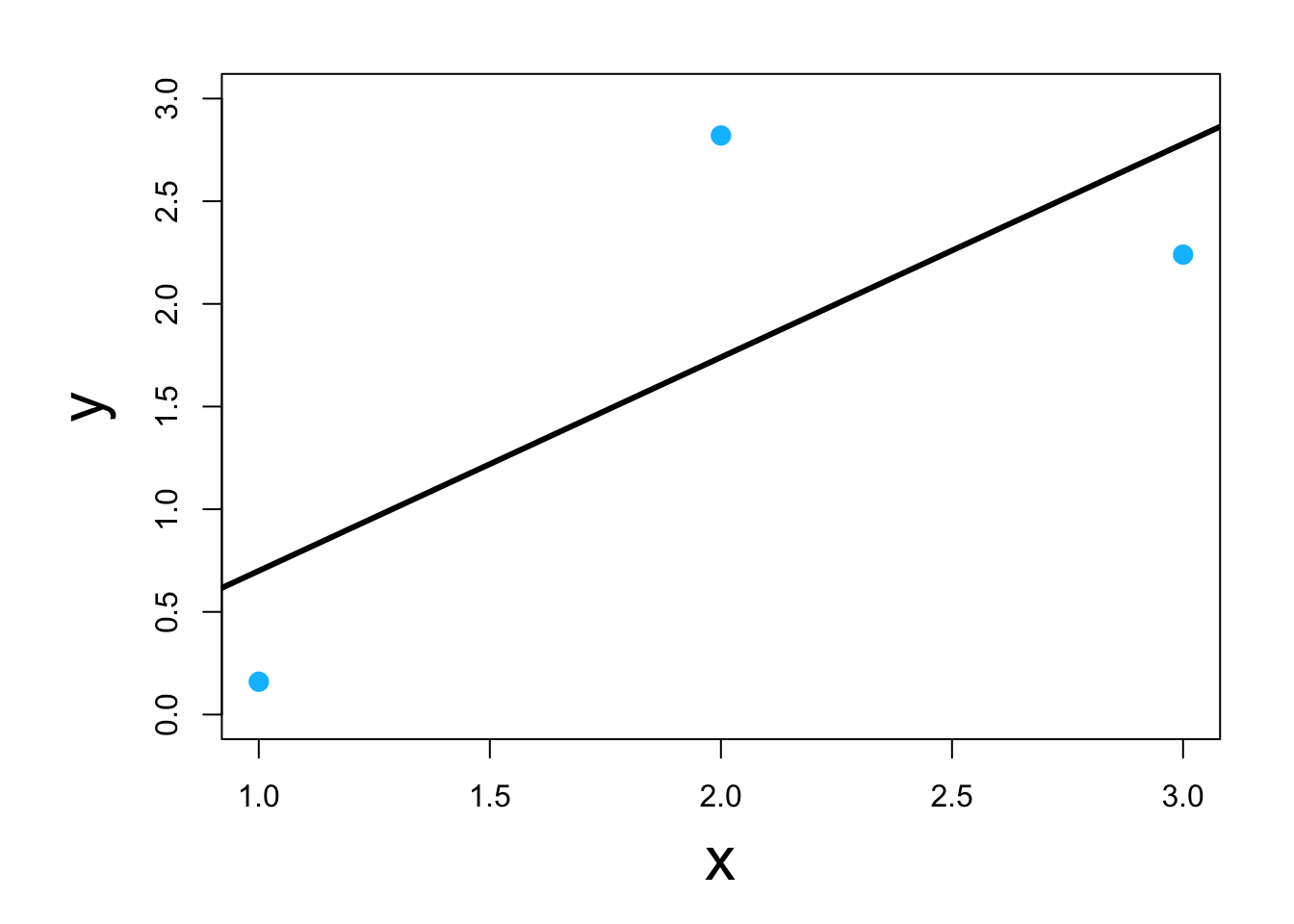

y <- c(0.16,2.82,2.24)

x <- c(1,2,3)

y.bar <- mean(y)

x.bar <- mean(x)

# Estimate the slope parameter

beta1.hat <- sum((x-x.bar)*(y-y.bar))/sum((x-x.bar)^2)

beta1.hat

## [1] 1.04

# Estimate the intercept parameter

beta0.hat <- y.bar - sum((x-x.bar)*(y-y.bar))/sum((x-x.bar)^2)*x.bar

beta0.hat

## [1] -0.34

- Using matrix calculus and algebra

y <- c(0.16,2.82,2.24)

X <- matrix(c(1,1,1,1,2,3),nrow=3,ncol=2,byrow=FALSE)

solve(t(X)%*%X)%*%t(X)%*%y

## [,1]

## [1,] -0.34

## [2,] 1.04

- Using modern (circa 1970’s) optimization techniques

y <- c(0.16,2.82,2.24)

x <- c(1,2,3)

optim(par=c(0,0),method = c("Nelder-Mead"),fn=function(beta){sum((y-(beta[1]+beta[2]*x))^2)})

## $par

## [1] -0.3399977 1.0399687

##

## $value

## [1] 1.7496

##

## $counts

## function gradient

## 61 NA

##

## $convergence

## [1] 0

##

## $message

## NULL

- Using modern and user friendly statistical computing software

df <- data.frame(y = c(0.16,2.82,2.24),x = c(1,2,3))

lm(y~x,data=df)

##

## Call:

## lm(formula = y ~ x, data = df)

##

## Coefficients:

## (Intercept) x

## -0.34 1.04