B Solutions to practice problems

2 Basic data cleaning with Excel

Click here to see the problems

- Table (b) shows a tidy data set.

- Characteristic (a) is necessary for a variable to function as an ID variable.

- Cell E15 is 2 columns and 3 rows away from cell C12. So we change all relative

references from column B to column D, and all relative references from row 2 to

row 5, and all relative references from row 10 to row 13. Absolute references

are not changed.

=D5=$B$2=$B5=D$2=SUM(D5:D13)=SUM($B$2:$B$10)=SUM($B5,$B13)=SUM(D$2,D$10)

- The formulas are:

=SQRT(A2)=MIN(A2:A100)=ABS(A2-B2)

- The formulas are:

=IF(A2<0.05,"Reject","Fail to reject")=CONCAT("A2 = ",A2)=LEFT(A2,2)

- The formulas are:

=MONTH(TODAY())=TODAY()+100=TODAY()-DATE(1969,11,20)- using my birthday; yours will obviously be different.

3 Probability and random events

Click here to see the problems

- The sample space is the set of all possible outcomes for \((r,w)\), and its cardinality

is just the number of elements it has.

- The sample space is: \[\begin{align} \Omega &= \left\{ \begin{aligned} & (1,1),(1,2),(1,3),(1,4),(1,5),(1,6), \\ & (2,1),(2,2),(2,3),(2,4),(2,5),(2,6), \\ & (3,1),(3,2),(3,3),(3,4),(3,5),(3,6), \\ & (4,1),(4,2),(4,3),(4,4),(4,5),(4,6), \\ & (5,1),(5,2),(5,3),(5,4),(5,5),(5,6), \\ & (6,1),(6,2),(6,3),(6,4),(6,5),(6,6) \\ \end{aligned} \right\} \end{align}\]

- Counting up the number of elements in the set, we get \(|\Omega| = 36\).

- Each event is just a set listing the \((r,w)\) outcomes that satisfy the relevant

conditions.

- Yo wins whenever \(r+w = 11\). \[\begin{align} Yo &= \{(5,6),(6,5)\} \end{align}\]

- Snake eyes wins when \(r+w = 2\): \[\begin{align} SnakeEyes = \{(1,1)\} \end{align}\]

- Boxcars wins when \(r+w = 12\): \[\begin{align} Boxcars = \{(6,6)\} \end{align}\]

- Field wins when \(r+w \in \{2,3,4,9,10,11,12\}\): \[\begin{align} Field &= \left\{\begin{aligned} & (1,1),(1,2),(1,3), \\ & (2,1),(2,2), \\ & (3,1),(3,6), \\ & (4,5),(4,6), \\ & (5,4),(5,5),(5,6), \\ & (6,3),(6,4),(6,5),(6,6) \\ \end{aligned}\right\} \end{align}\]

- Statements (b) and (c) are true.

- Statements (a) and (d) are true.

- Statements (b) and (c) are true.

- Event (c) is an elementary event.

- All three elementary events have probability \(1/36 \approx 0.028\)

- The probability of each event can be calculated by adding up the probabilities

of its elementary events:

- The probability a bet on Yo wins is: \[\begin{align} \Pr(Yo) &= \Pr(\{(5,6),(6,5)\}) \\ &= \Pr(\{(5,6)\}) + \Pr(\{(6,5)\}) \\ &= 2/36 \\ &\approx 0.056 \end{align}\]

- The probability a bet on Snake eyes wins is: \[\begin{align} \Pr(SnakeEyes) &= \Pr(\{(1,1)\}) \\ &= 1/36 \\ &\approx 0.028 \end{align}\]

- The probability a bet on Boxcars wins is: \[\begin{align} \Pr(Boxcars) &= \Pr(\{(6,6)\}) \\ &= 1/36 \\ &\approx 0.028 \end{align}\]

- The probability a bet on Field wins is: \[\begin{align} \Pr(Field) &= \Pr\left(\left\{\begin{aligned} & (1,1),(1,2),(1,3), \\ & (2,1),(2,2), \\ & (3,1),(3,6), \\ & (4,5),(4,6), \\ & (5,4),(5,5),(5,6), \\ & (6,3),(6,4),(6,5),(6,6) \\ \end{aligned}\right\}\right) \\ &= \Pr(\{(1,1)\}) + \Pr(\{(1,2)\}) + \cdots + \Pr(\{(6,6)\}) \\ &= 16/36 \\ &\approx 0.444 \end{align}\]

- To calculate the joint probability, start by calculating the intersection

of the two events:

- The joint probability is: \[\begin{align} \Pr(Yo \cap Boxcars) &= \Pr(\{(5,6),(6,5)\} \cap \{(6,6)\}) \\ &= \Pr(\emptyset) \\ &= 0 \end{align}\]

- The joint probability is: \[\begin{align} \Pr(Yo \cap Field) &= \Pr\left(\{(5,6),(6,5)\} \cap \left\{\begin{aligned} & (1,1),(1,2),(1,3), \\ & (2,1),(2,2), \\ & (3,1),(3,6), \\ & (4,5),(4,6), \\ & (5,4),(5,5),(5,6), \\ & (6,3),(6,4),(6,5),(6,6) \\ \end{aligned}\right\}\right) \\ &= \Pr(\{(5,6),(6,5)\}) \\ &= 2/36 \\ &\approx 0.056 \end{align}\]

- The joint probability is: \[\begin{align} \Pr(Yo \cap Boxcars^C) &= \Pr(\{(5,6),(6,5)\} \cap \{(6,6)\}^C) \\ &= \Pr(\{(5,6),(6,5)\}) \\ &= 2/36 \\ &\approx 0.056 \end{align}\]

- The conditional probability is just the ratio of the joint probability to

the probability of the event we are conditioning on:

- The conditional probability is: \[\begin{align} \Pr(Yo | Boxcars) &= \frac{Pr(Yo \cap Boxcars)}{\Pr(Boxcars)} \\ &= \frac{0}{1/36} \\ &= 0 \end{align}\]

- The conditional probability is: \[\begin{align} \Pr(Yo | Field) &= \frac{Pr(Yo \cap Field)}{\Pr(Field)} \\ &= \frac{2/36}{16/36} \\ &= 0.125 \end{align}\]

- The conditional probability is: \[\begin{align} \Pr(Yo | Boxcars^C) &= \frac{Pr(Yo \cap Boxcars^C)}{\Pr(Boxcars^C)} \\ &= \frac{2/36}{1-1/36} \\ &\approx 0.057 \end{align}\]

- The conditional probability is: \[\begin{align} \Pr(Field | Yo) &= \frac{Pr(Field \cap Yo)}{\Pr(Yo)} \\ &= \frac{2/36}{2/36} \\ &= 1 \end{align}\]

- The conditional probability is: \[\begin{align} \Pr(Boxcars | Yo) &= \frac{Pr(Boxcars \cap Yo)}{\Pr(Yo)} \\ &= \frac{0}{2/36} \\ &= 0 \end{align}\]

- The events in (e) are independent.

- Statements (a), (c), (e), (g), and (i) are true.

- Statements (b) and (c) are true.

- Statements (a), (d), (e), (f), and (h) are true.

- Statements (a) and (b) are true.

- Statements (b) and (c) are true.

4 Introduction to random variables

Click here to see the problems

- We can define \(t = r+w\).

- We can define \(y = I(r+w = 11)\).

- The support of a random variable is the set of all values with positive probability.

- The support of \(r\) is \(S_r = \{1,2,3,4,5,6\}\).

- The support of \(t\) is \(S_t = \{2,3,4,5,6,7,8,9,10,11,12\}\).

- The support of \(y\) is \(S_y = \{0,1\}\).

- The range of a random variable is just the interval defined by the support’s minimum and maximum values.

- The range of \(r\) is \([1,6]\).

- The range of \(t\) is \([2,12]\).

- The range of \(y\) is \([0,1]\).

- The PDF can be derived from the probability distribution of the underlying outcome

\((r,w)\), which was calculated in the previous chapter.

- The PDF of \(r\) is: \[\begin{align} f_r(a) &= \begin{cases} 1/6 & a \in \{1,2,3,4,5,6\} \\ 0 & \textrm{otherwise} \\ \end{cases} \end{align}\]

- The PDF of \(t\) is: \[\begin{align} f_t(a) &= \begin{cases} 1/36 & a \in \{2,12\} \\ 2/36 \textrm{ (or $1/18$)} & a \in \{3,11\} \\ 3/36 \textrm{ (or $1/12$)} & a \in \{4,10\} \\ 4/36 \textrm{ (or $1/9$)} & a \in \{5,9\} \\ 5/36 & a \in \{6,8\} \\ 6/36 \textrm{ (or $1/6$)} & a = 7 \\ 0 & \textrm{otherwise} \\ \end{cases} \end{align}\]

- The PDF of \(y\) is: \[\begin{align} f_y(a) &= \begin{cases} 17/18 & a = 0 \\ 1/18 & a = 1 \\ 0 & \textrm{otherwise} \\ \end{cases} \end{align}\]

- We can construct the CDF by cumulatively summing up the PDF:

- The CDF of \(r\) is: \[\begin{align} F_r(a) &= \begin{cases} 0 & a < 1 \\ 1/6 & 1 \leq a < 2 \\ 1/3 & 2 \leq a < 3 \\ 1/2 & 3 \leq a < 4 \\ 2/3 & 4 \leq a < 5 \\ 5/6 & 5 \leq a < 6 \\ 1 & a \geq 6 \\ \end{cases} \end{align}\]

- The CDF of \(y\) is: \[\begin{align} F_y(a) &= \begin{cases} 0 & a < 0 \\ 17/18 & 0 \leq a < 1 \\ 1 & a \geq 1 \\ \end{cases} \end{align}\]

- We find the expected value by applying the definition:

- The expected value is \[\begin{align} E(r) &= \sum_{a \in S_r} a\Pr(r=a) \\ &= 1*\frac{1}{6} + 2*\frac{1}{6} + 3*\frac{1}{6} + 4*\frac{1}{6} + 5*\frac{1}{6} + 6*\frac{1}{6} \\ &= 21/6 \\ &= 3.5 \end{align}\]

- The expected value is \[\begin{align} E(r^2) &= \sum_{a \in S_r} a^2\Pr(r=a) \\ &= 1^2*\frac{1}{6} + 2^2*\frac{1}{6} + 3^2*\frac{1}{6} + 4^2*\frac{1}{6} + 5^2*\frac{1}{6} + 6^2*\frac{1}{6} \\ &= 91/6 \\ &= 15.17 \end{align}\]

- The key here is to write down the definition of the specific quantile you are

looking for, then substitute the CDF you derived earlier.

- The median of \(r\) is: \[\begin{align} F_r^{-1}(0.5) &= \min \{a: \Pr(r \leq a) \geq 0.5\} \\ &= \min \{a: F_r(a) \geq 0.5\} \\ &= \min \{a: a \geq 3\} \\ &= 3 \end{align}\]

- The 0.25 quantile of \(r\) is \[\begin{align} F_r^{-1}(0.25) &= \min \{a: \Pr(r \leq a) \geq 0.25\} \\ &= \min \{a: F_r(a) \geq 0.25\} \\ &= \min \{a: a \geq 2\} \\ &= 2 \end{align}\]

- The 75th percentile of \(r\) is just its 0.75 quantile: \[\begin{align} F_r^{-1}(0.75) &= \min \{a: \Pr(r \leq a) \geq 0.75\} \\ &= \min \{a: F_r(a) \geq 0.75\} \\ &= \min \{a: a \geq 5\} \\ &= 5 \end{align}\]

- Let \(d = (y - E(y))^2\)

- We can derive the PDF of \(d\) from the PDF of \(y\): \[\begin{align} f_{d}(a) &= \begin{cases} 17/18 & a = (0-1/18)^2 \\ 1/18 & a = (1-1/18)^2 \\ 0 & \textrm{otherwise} \\ \end{cases} \end{align}\]

- The expected value is: \[\begin{align} E(d) &= (0-1/18)^2 * \frac{17}{18} + (1-1/18)^2 *\frac{1}{18} \\ &\approx 0.0525 \end{align}\]

- The variance is: \[\begin{align} var(y) &= E(d) \\ &\approx 0.0525 \end{align}\]

- The standard deviation is \[sd(y) = \sqrt{var(y)} \approx \sqrt{0.0525} \approx 0.229\]

- Earlier, you found \(E(r) = 3.5\) and \(E(r^2) = 15.17\). So we can apply

our result that \(var(x) = E(x^2) - E(x)^2\) for a simpler way of calculating

the variance.

- The variance is: \[\begin{align} var(r) &= E(r^2) - E(r)^2 \\ &= 15.17 - 3.5^2 \\ &= 2.92 \end{align}\]

- The standard deviation is: \[\begin{align}2 sd(r) &= \sqrt{var(r)} = \sqrt{2.92} \approx 1.71 \end{align}\]

- The Bernoulli distribution describes any random variable (like \(y\)) that

has a binary \(\{0,1\}\) support.

- \(y\) has the \(Bernouili(p)\) distribution with \(p=1/18\), or \[y \sim Bernoulli(1/18)\]

- In the Bernoulli distribution \(E(y)=p =1/18\).

- In the Bernoulli distribution, \(var(y) = p*(1-p) = 1/18 * 17/18 \approx 0.525\).

- The binomial distribution describes any random variable that describes the

number of times an event happens in a fixed number of independent trials.

- \(Y_{10}\) has the binomial distribution with \(n=10\) and \(p=1/18\). We can also write that as \[Y_{10} \sim Binomial(10,1/18)\]

- For the Binomial distribution we have \[E(Y_{10}) = np = 10*1/18 \approx 0.556\]

- For the binomial distribution we have \[var(Y_{10}) = np(1-p) = 10*1/18*17/18 \approx 0.525\]

- The Excel formula for \(\Pr(Y_{10} = 0)\) would be

=BINOM.DIST(0,10,1/18,FALSE)which produces the result \[\Pr(Y_{10} = 0) \approx 0.565\] - The Excel formula for \(\Pr(Y_{10} \leq 10/16)\) would be

=BINOM.DIST(10/16,10,1/18,TRUE)which produces the result \[\Pr(Y_{10} \leq 10/16) \approx 0.565\] - The Excel formula for \(\Pr(Y_{10} > 10/16)\) would be

=1-BINOM.DIST(10/16,10,1/18,TRUE)which produces the result \[\Pr(Y_{10} > 10/16) \approx 0.435\]

- The key here is to apply the formulas for the expected value and variance

of a linear function of a random variable.

- The expected value is: \[\begin{align} E(W) &= E(160*y - 10) \\ &= 160*E(y) - 10 \\ &= 160*1/18 - 10 \\ &\approx -1.11 \end{align}\]

- The variance is: \[\begin{align} var(W) &= var(160*y - 10) \\ &= 160^2*var(y) \\ &= 160^2*1/18*17/18 \\ &\approx 1343.2 \end{align}\]

- The event probability is \[\begin{align} \Pr(W > 0) &= \Pr(y=1) = 1/18 \approx 0.056 \end{align}\]

- Applying the formulas for a linear function:

- The expected value is: \[\begin{align} E(W_{10}) &= E(16*Y_{10} - 10) \\ &= 16*E(Y_{10}) - 10 \\ &= 16*10*1/18 - 10 \\ &\approx -1.11 \end{align}\]

- The variance is: \[\begin{align} var(W_{10}) &= var(16*Y_{10} - 10) \\ &= 16^2var(Y_10) \\ &= 16^2 * 10*1/18*17/18 \\ &\approx 134.32 \end{align}\]

- The event probability is \[\begin{align} \Pr(W_{10} > 0) &= \Pr(Y_{10} > 10/16) \approx 0.435 \end{align}\]

- If you care mostly about expected net winnings, you should just keep your $10 and not bet at all. This strategy has an expected net winnings of zero, while the others both have negative expected net winnings.

- Betting $1 on ten rolls produces the highest probability of walking away from the table with more money than you started with.

- Betting $10 on one roll produces more variable net winnings.

5 More on random variables

Click here to see the problems

- The key here is to redefine joint events for \(y\) and \(b\) as

events for the single random variable \(t\).

- The joint PDF is: \[\begin{align} f_{y,b}(1,1) &= \Pr(y = 1 \cap b = 1) \\ &= \Pr(t = 11 \cap t = 12) \\ &= \Pr(\emptyset) \\ &= 0 \end{align}\]

- The joint PDF is: \[\begin{align} f_{y,b}(0,1) &= \Pr(y \neq 1 \cap b = 1) \\ &= \Pr(t \neq 11 \cap t = 12) \\ &= \Pr(t = 12) \\ &= f_t(12) \\ &= 1/36 \end{align}\]

- The joint PDF is: \[\begin{align} f_{y,b}(1,0) &= \Pr(y = 1 \cap b = 0) \\ &= \Pr(t = 11 \cap t \neq 12) \\ &= \Pr(t = 11) \\ &= f_t(11) \\ &= 1/18 \end{align}\]

- The joint PDF is: \[\begin{align} f_{y,b}(0,0) &= \Pr(y = 0 \cap b = 0) \\ &= \Pr(t \neq 11 \cap t \neq 12) \\ &= \Pr(t \notin \{11,12\}) \\ &= 1 - \Pr(t \in \{11,12\}) \\ &= 1 - 1/36 - 1/18 \\ &= 11/12 \end{align}\]

- The marginal PDF is constructed by adding together the joint PDFs.

- The marginal PDF is: \[\begin{align} f_b(0) &= f_{y,b}(0,0) + f_{y,b}(1,0) \\ &= 11/12 + 1/18 \\ &= 35/36 \end{align}\]

- The marginal PDF is: \[\begin{align} f_b(1) &= f_{y,b}(0,1) + f_{y,b}(1,1) \\ &= 1/36 + 0 \\ &= 1/36 \end{align}\]

- The expected value is: \[\begin{align} E(b) &= 0*f_b(0) + 1*f_b(1) \\ &= f_b(1) \\ &= 1/36 \end{align}\]

- The conditional PDF is the ratio of the joint PDF to the marginal PDF:

- The conditional PDF is: \[\begin{align} f_{y|b}(1,1) &= \Pr(y=1|b=1) \\ &= \frac{f_{y,b}(1,1)}{f_b(1)} \\ &= \frac{0}{1/36} \\ &= 0 \end{align}\]

- The conditional PDF is: \[\begin{align} f_{y|b}(0,1) &= \Pr(y=0|b=1) \\ &= \frac{f_{y,b}(0,1)}{f_b(1)} \\ &= \frac{1/36}{1/36} \\ &= 1 \end{align}\]

- The conditional PDF is: \[\begin{align} f_{y|b}(1,0) &= \Pr(y=1|b=0) \\ &= \frac{f_{y,b}(1,0)}{f_b(0)} \\ &= \frac{1/18}{35/36} \\ &\approx 0.057 \end{align}\]

- The conditional PDF is: \[\begin{align} f_{y|b}(0,0) &= \Pr(y=0|b=0) \\ &= \frac{f_{y,b}(0,0)}{f_b(0)} \\ &= \frac{11/12}{35/36} \\ &\approx 0.943 \end{align}\]

- \(r\) and \(w\) are independent.

- Since \(E(y) = 1/18\) and \(E(b) = 1/36\) we have \[\begin{align} cov(y,b) &= E((y-E(y))(b-E(b))) \\ &= \begin{aligned}[t] & (0-E(y))*(0-E(b))*f_{y,b}(0,0) \\ &+ (1-E(y))*(0-E(b))*f_{y,b}(1,0) \\ &+ (0-E(y))*(1-E(b))*f_{y,b}(0,1) \\ &+ (1-E(y))*(1-E(b))*f_{y,b}(1,1) \\ \end{aligned} \\ &= \begin{aligned}[t] & (0-1/18)*(0-1/36)*(11/12) \\ &+ (1-1/18)*(0-1/36)*(1/18) \\ &+ (0-1/18)*(1-1/36)*(1/36) \\ &+ (1-1/18)*(1-1/36)*(0) \\ \end{aligned} \\ &\approx -0.00154 \end{align}\]

- The alternate formula for the covariance is \(cov(y,b) = E(yb) - E(y)E(b)\).

- The expected value is: \[\begin{align} E(yb) &= \begin{aligned} & 0*0*f_{y,b}(0,0) \\ &+ 1*0*f_{y,b}(1,0) \\ &+ 0*1*f_{y,b}(0,1) \\ &+ 1*1*f_{y,b}(1,1) \\ \end{aligned} \\ &= f_{y,b}(1,1) \\ &= 0 \end{align}\]

- The covariance is: \[\begin{align} cov(y,b) &= E(yb) - E(y)E(b) \\ &= 0 - (1/18)*(1/36) \\ &\approx -0.00154 \end{align}\]

- Yes, if you have done it right you should get the same answer.

- The correlation is: \[\begin{align} corr(y,b) &= \frac{cov(y,b)}{\sqrt{var(y)var(b)}} \\ &\approx \frac{-0.00154}{\sqrt{ 0.0525*0.027}} \\ &\approx -0.04 \end{align}\]

- In this question we know the correlation and several values of the formula

defining it, and we use this to solve for the missing value.

- We know that \(corr(b,t) = \frac{cov(b,t)}{\sqrt{var(b)var(t)}}\), so we can substitute known values to get: \[\begin{align} 0.35 &= \frac{cov(b,t)}{\sqrt{0.027*5.83}} \end{align}\] Solving for \(cov(b,t)\) we get \[\begin{align} cov(b,t) &= 0.35*\sqrt{0.027*5.83} \\ &= 0.139 \end{align}\]

- We know that \(cov(b,t) = E(bt) - E(b)E(t)\), so we can substitute known values to get: \[\begin{align} 0.139 &= E(bt) - (1/36)*7 \end{align}\] Solving for \(E(bt)\) we get: \[\begin{align} E(bt) &= 0.139 + (1/36)*7 \\ &= 0.333 \end{align}\]

- Remember that independent events are also uncorrelated. So:

- The covariance is \(cov(r,w) = 0\).

- The correlation is \(corr(r,w) = 0\).

- This question uses the formulas for the mean of a linear function of

two random variables.

- The expected value is: \[\begin{align} E(y+b) &= E(y) + E(b) \\ &= 1/18 + 1/36 \\ &= 3/36 \\ &= 1/12 \end{align}\]

- The expected value is: \[\begin{align} E(16y + 31b - 2) &= 16 E(y) + 31 E(b) - 2 \\ &= 16/18 + 31/36 - 2 \\ &= -9/36 \end{align}\]

- This question uses the formulas for the variance and covariance of

a linear function of two random variables.

- The covariance is: \[\begin{align} cov(16y,31b) &= 16 * 31 * cov(y,b) \\ &\approx 16 * 31 * (-0.00154) \\ &\approx -0.7638 \end{align}\]

- The variance is: \[\begin{align} var(y+b) &= var(y) + var(b) + 2 cov(y,b) \\ &\approx 0.0525 + 0.027 + 2*(-0.00154) \\ &\approx 0.07642 \end{align}\]

- The result of a bet on Boxcars is negatively related to the result of a bet on Yo.

- This question uses various formulas for the uniform distribution.

- The PDF is: \[\begin{align} f_x(a) &= \begin{cases} 0 & a < -1 \\ 0.5 & -1 \leq a \leq 1 \\ 0 & a > 1 \\ \end{cases} \end{align}\]

- The CDF is: \[\begin{align} f_x(a) &= \begin{cases} 0 & a < -1 \\ \frac{a+1}{2} & -1 \leq a \leq 1 \\ 1 & a > 1 \\ \end{cases} \end{align}\]

- \(x\) is a continuous random variable so \(\Pr(x = 0) = 0\)

- \(x\) is a continuous random variable so \[\begin{align} \Pr(0 < x < 0.5) &= F_x(0.5) - F_x(0) \\ &= \frac{0.5+1}{2} - \frac{1}{2} \\ &= 0.25 \end{align}\]

- \(x\) is a continuous random variable so \[\begin{align} \Pr(0 \leq x \leq 0.5) &= F_x(0.5) - F_x(0) \\ &= \frac{0.5+1}{2} - \frac{1}{2} \\ &= 0.25 \end{align}\]

- The median is: \[\begin{align} F_x^{-1}(0.5) &= \min \{a: \Pr(x \leq a) \geq 0.5\} \\ &= \min \{a: F_x(a) \geq 0.5\} \\ &= \min \{a: \frac{a+1}{2} \geq 0.5\} \\ &= \textrm{the $a$ that solves the equation $\frac{a+1}{2} = 0.5$} \\ &= 0 \end{align}\]

- The 75th percentile is \[\begin{align} F_x^{-1}(0.75) &= \min \{a: \Pr(x \leq a) \geq 0.75\} \\ &= \min \{a: F_x(a) \geq 0.75\} \\ &= \min \{a: \frac{a+1}{2} \geq 0.75\} \\ &= \textrm{the $a$ that solves the equation $\frac{a+1}{2} = 0.75$} \\ &= 0.5 \end{align}\]

- The mean of a \(Uniform(a,b)\) random variable is \((a+b)/2\), so \[\begin{align} E(x) &= \frac{1 + (-1)}{2} \\ &= 0 \end{align}\]

- The variance of a \(Uniform(a,b)\) random variable is \((b-a)^2/12\), so \[\begin{align} var(x) &= (b-a)^2/12 \\ &= \frac{(1 - (-1))^2}{12} \\ &\approx 0.33 \end{align}\]

- A linear function of a uniform random variable is also uniform.

- When \(x = -1\), we have \(y = 3*(-1)+5 = 2\). When \(x = 1\), we have \(y = 3*(1)+5 = 8\). Therefore \(y \sim U(2,8)\)

- The expected value is \(E(y) = (2+8)/2 = 5\).

- This question applies various formulas for the normal distribution.

- The expected value of a \(N(\mu,\sigma^2)\) random variable is \(\mu\), so \(E(x) = 10\)

- The median of a \(N(\mu,\sigma^2)\) random variable is \(\mu\), so \(Median(x) = 10\).

- The variance of a \(N(\mu,\sigma^2)\) random variable is \(\sigma^2\), so \(var(x) = 4\).

- The standard deviation is \(sd(x) = \sqrt{var(x)} = \sqrt{4} = 2\)

- The Excel formula would be

=NORM.DIST(11,10,2,TRUE)which yields the result \(\Pr(x \leq 11) \approx 0.691\)

- A linear function of a normal random variable is also normal.

- The distribution of \(y\) will be normal with mean \(3E(x) + 5 = 35\) and variance \(3^2 var(x) = 36\), so \(y \sim N(35,36)\)

- If \(x \sim N(10,4)\) then \(z = \frac{x - 10}{2} \sim N(0,1)\).

- Solving for \(x\) in terms of \(z\) we get \(x = 2z + 10\) \[\begin{align} \Pr(x \leq 11) &= \Pr(2z + 10 \leq 11) \\ &= \Pr(z \leq (11-10)/2) \\ &= \Pr(z \leq 0.5) \\ &= \Phi(0.5) \end{align}\]

- The correct Excel formula would be

=NORM.S.DIST(0.5,TRUE)which yields the result \(\Pr(x \leq 11) \approx 0.691\).

6 Basic data analysis with Excel

Click here to see the problems

The answers are:

- Sample size is 3

- Sample average age is 45.

- Sample median of age is 32.

- Sample 25th percentile of age is 28.5.

- Sample variance of age is 829.

- Sample standard deviation of age is 28.8.

The numerical answers are the same as in question 1. Assuming the table starts in cell A1, the Excel formulas are:

=COUNT(B2:B4)=AVERAGE(B2:B4)=MEDIAN(B2:B4)=PERCENTILE.INC(B2:B4,0.25)=VAR.S(B2:B4)=STDEV.S(B2:B4)

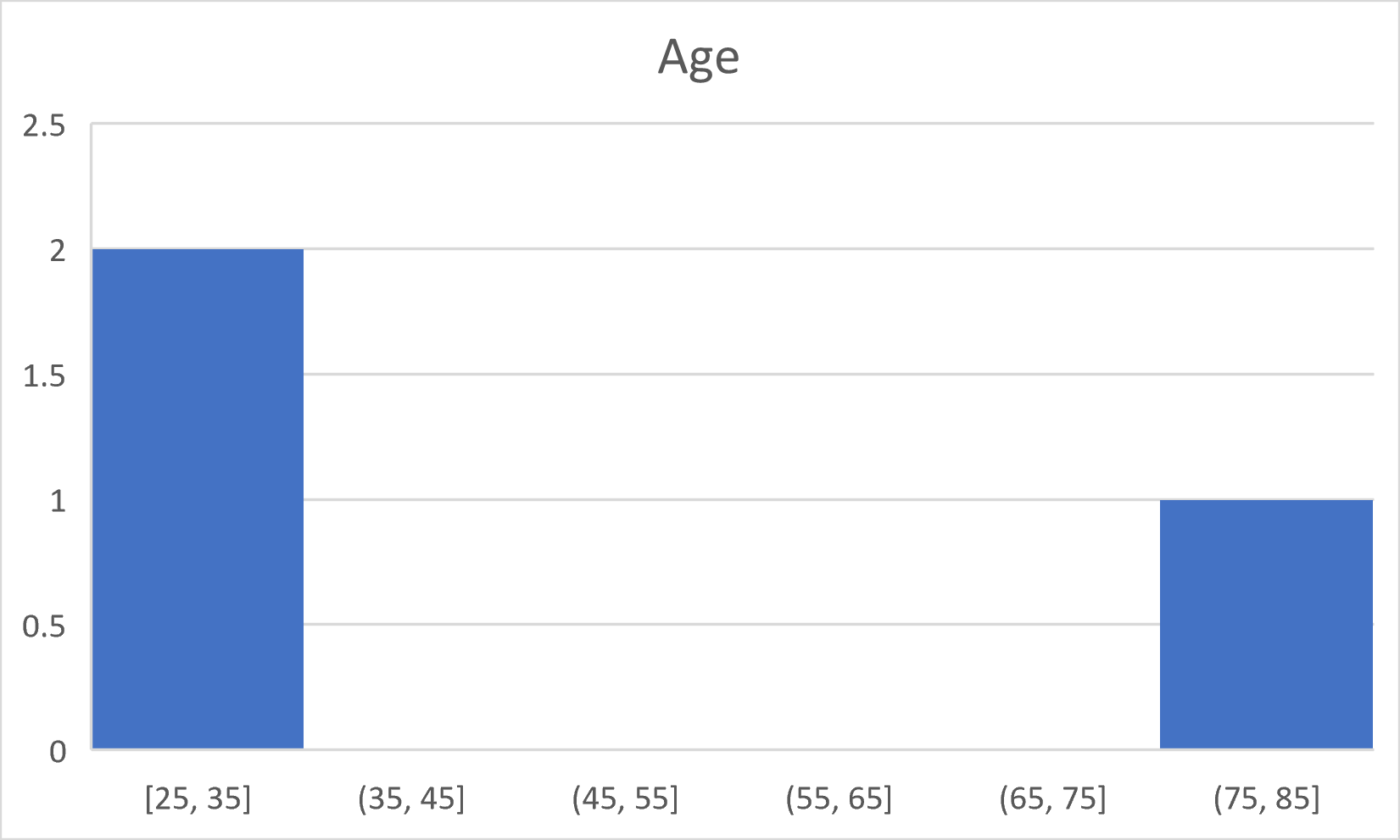

The binned frequency table should look something like this:

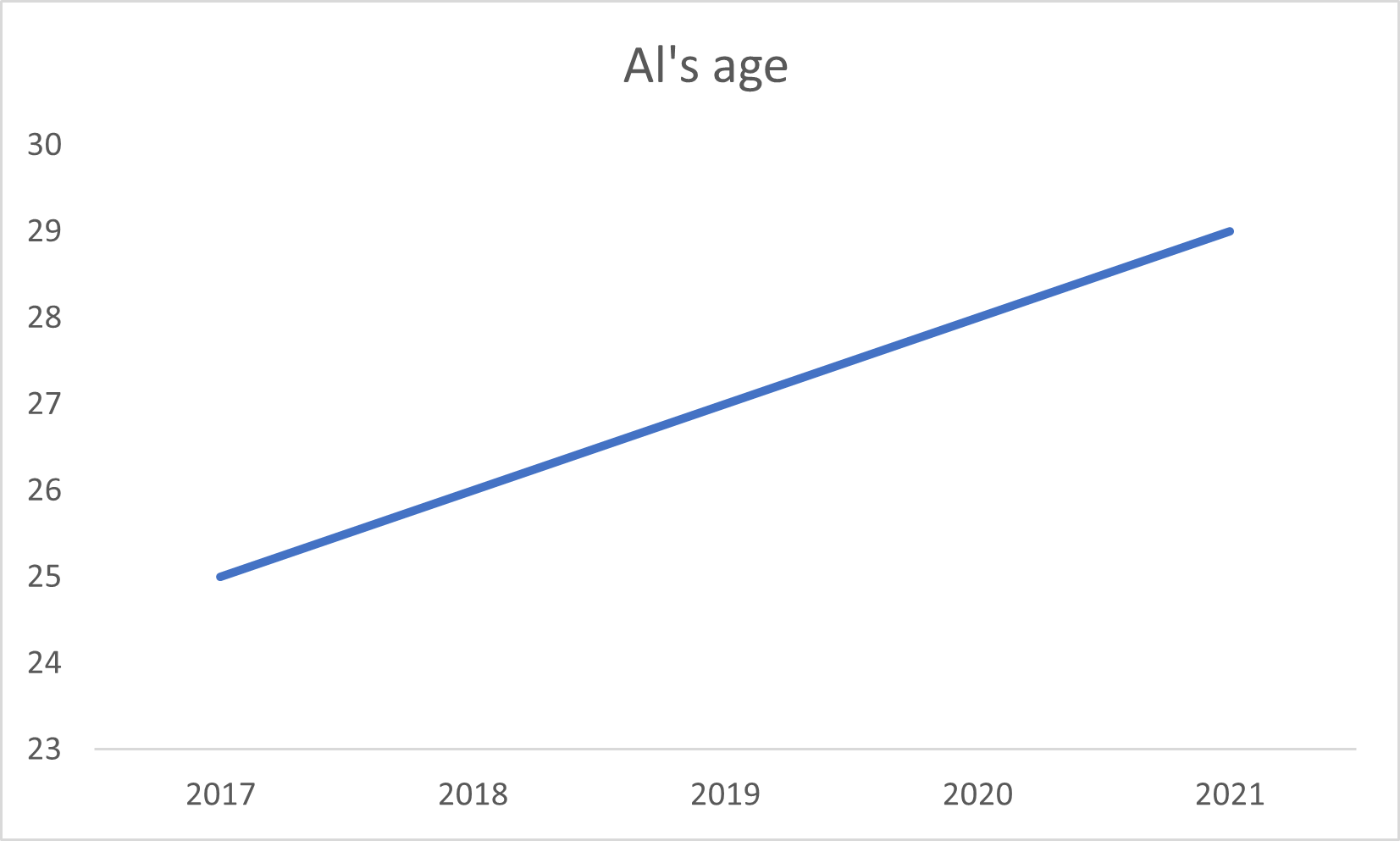

Range Frequency % Freq 0-10 0 0 11-20 0 0 21-30 1 33 31-40 1 33 41-50 0 0 51-60 0 0 61-70 0 0 71-80 1 33 The time series graph should look something like this:

The histogram should look something like this:

7 Statistics

Click here to see the problems

A random sample needs to be independent (not just uncorrelated) and identically distributed (not just the same mean and variance).

- Possibly a random sample.

- Possibly a random sample.

- Not a random sample.

- Definitely a random sample.

- Possibly a random sample.

- Not a random sample.

Identify the sampling type (random sample, time series, stratified sample, cluster sample, census, convenience sample) for each of the following data sets.

- This is a convenience sample.

- This is a random sample.

- This is a stratified sample.

- This is a time series.

- This is a census.

Since we have a random sample, the joint PDF is just a product of the marginal PDFs.

- The support is just the set of all possible combinations: \[S_{D_n} = \{(1,1),(1,2),(2,1),(2,2)\}\]

- Since we have a random sample, the joint PDF is the product of the marginal PDFs: \[\begin{align} f_{D_n}(1,1) &= f_x(1)f_x(1) \\ &= 0.4*0.4 \\ &= 0.16 \end{align}\]

- Since we have a random sample, the joint PDF is the product of the marginal PDFs: \[\begin{align} f_{D_n}(2,1) &= f_x(2)f_x(1) \\ &= 0.6*0.4 \\ &= 0.24 \end{align}\]

- Since we have a random sample, the joint PDF is the product of the marginal PDFs: \[\begin{align} f_{D_n}(1,2) &= f_x(1)f_x(2) \\ &= 0.4*0.6 \\ &= 0.24 \end{align}\]

- Since we have a random sample, the joint PDF is the product of the marginal PDFs: \[\begin{align} f_{D_n}(2,2) &= f_x(2)f_x(2) \\ &= 0.6*0.6 \\ &= 0.36 \end{align}\]

This is a long question but we can make it easier by preparing a simple table mapping each of the four possible values of \(D_n\) into a value for each statistic:

\(x_1\) \(x_2\) \(f_{D_n}(\cdot)\) \(\hat{f}_1\) \(\bar{x}\) \(\hat{\sigma}_x^2\) \(\hat{\sigma}_x\) \(xmin\) \(xmax\) 1 1 0.16 1 1 0 0 1 1 2 1 0.24 0.5 1.5 0.5 0.71 1 2 1 2 0.24 0.5 1.5 0.5 0.71 1 2 2 2 0.36 0 2 0 0 2 2 This will make our lives much easier.

- The support is \(S_{\hat{f}_1} = \{0,0.5,1\}\) and the sampling distribution is: \[\begin{align} f_{\hat{f}_1}(0) &= \Pr(\hat{f}_1 = 0) \\ &= f_{D_n}(2,2) \\ &= 0.36 \\ f_{\hat{f}_1}(0.5) &= \Pr(\hat{f}_1 = 0.5) \\ &= f_{D_n}(2,1) + f_{D_n}(1,2) \\ &= 0.24 + 0.24 \\ &= 0.48 \\ f_{\hat{f}_1}(1) &= \Pr(\hat{f}_1 = 1) \\ &= f_{D_n}(1,1) \\ &= 0.16 \end{align}\]

- The support is \(S_{\bar{x}} = \{1,1.5,2\}\) and the sampling distribution is: \[\begin{align} f_{\bar{x}}(1) &= \Pr(\bar{x} = 1) \\ &= f_{D_n}(1,1) \\ &= 0.16 \\ f_{\bar{x}}(1.5) &= \Pr(\bar{x} = 1.5) \\ &= f_{D_n}(2,1) + f_{D_n}(1,2) \\ &= 0.24 + 0.24 \\ &= 0.48 \\ f_{\bar{x}}(2) &= \Pr(\bar{x} = 2) \\ &= f_{D_n}(2,2) \\ &= 0.36 \end{align}\]

- The support is \(S_{\hat{\sigma}_x^2} = \{0,0.5\}\) and the sampling distribution is: \[\begin{align} f_{\hat{\sigma}_x^2}(0) &= \Pr(\hat{\sigma}_x^2 = 0) \\ &= f_{D_n}(1,1) + f_{D_n}(2,2)\\ &= 0.16 + 0.36 \\ &= 0.52 \\ f_{\hat{\sigma}_x^2}(0.5) &= \Pr(\hat{\sigma}_x^2 = 0.5) \\ &= f_{D_n}(2,1) + f_{D_n}(1,2) \\ &= 0.24 + 0.24 \\ &= 0.48 \end{align}\]

- The support is \(S_{\hat{\sigma}_x} = \{0,0.71\}\) and the sampling distribution is: \[\begin{align} f_{\hat{\sigma}_x^2}(0) &= \Pr(\hat{\sigma}_x = 0) \\ &= f_{D_n}(1,1) + f_{D_n}(2,2)\\ &= 0.16 + 0.36 \\ &= 0.52 \\ f_{\hat{\sigma}_x^2}(0.71) &= \Pr(\hat{\sigma}_x = 0.71) \\ &= f_{D_n}(2,1) + f_{D_n}(1,2) \\ &= 0.24 + 0.24 \\ &= 0.48 \end{align}\]

- The support is \(S_{xmin} = \{1,2\}\) and the sampling distribution is: \[\begin{align} f_{xmin}(1) &= \Pr(xmin = 1) \\ &= f_{D_n}(1,1) + f_{D_n}(2,1) + f_{D_n}(1,2) \\ &= 0.16 + 0.24 + 0.24 \\ &= 0.64 \\ f_{xmin}(2) &= \Pr(xmin = 2) \\ &= f_{D_n}(2,2) \\ &= 0.36 \end{align}\]

- The support is \(S_{xmax} = \{1,2\}\) and the sampling distribution is: \[\begin{align} f_{xmax}(1) &= \Pr(xmax = 1) \\ &= f_{D_n}(1,1) \\ &= 0.16 \\ f_{xmax}(2) &= \Pr(xmax = 2) \\ &= f_{D_n}(2,2) + f_{D_n}(2,1) + f_{D_n}(1,2) \\ &= 0.36 + 0.24 + 0.24 \\ &= 0.84 \end{align}\]

The mean can be calculated from each statistic’s PDF:

- The mean is: \[\begin{align} E(\hat{f}_1) &= 0*f_{\hat{f}_1}(0) + 0.5*f_{\hat{f}_1}(0) + 1*f_{\hat{f}_1}(1) \\ &= 0*0.36 + 0.5*0.48 + 1*0.16 \\ &= 0.4 \end{align}\]

- The mean is: \[\begin{align} E(\bar{x}) &= 1*f_{\bar{x}}(1) +1.5*f_{\bar{x}}(1.5) + 2*f_{\bar{x}}(2) \\ &= 1*0.16 +1.5*0.48 + 2*0.36 \\ &= 1.6 \end{align}\]

- The mean is: \[\begin{align} E(\hat{\sigma}_x^2) &= 0*f_{\hat{\sigma}_x^2}(0) + 0.5*f_{\hat{\sigma}_x^2}(0.5) \\ &= 0*0.52 + 0.5*0.48 \\ &= 0.24 \end{align}\]

- The mean is: \[\begin{align} E(\hat{\sigma}_x) &= 0*f_{\hat{\sigma}_x}(0) + 0.71*f_{\hat{\sigma}_x}(0.71) \\ &= 0*0.52 + 0.71*0.48 \\ &= 0.34 \end{align}\]

- The mean is: \[\begin{align} E(xmin) &= 1*f_{xmin}(1) + 2*f_{xmin}(2) \\ &= 1*0.64 + 2*0.36 \\ &= 1.36 \end{align}\]

- The mean is: \[\begin{align} E(xmax) &= 1*f_{xmax}(1) + 2*f_{xmax}(2) \\ &= 1*0.16 + 2*0.84 \\ &= 1.84 \end{align}\]

We have already found the mean of each statistic, so we can calculate the variance using the alternative formula \(var(x) = E(x^2) - E(x)^2\)

- To calculate the variance, we can use the alternative formula: \[\begin{align} E(\hat{f}_1^2) &= 0^2*f_{\hat{f}_1}(0) + 0.5^2*f_{\hat{f}_1}(0) + 1^2*f_{\hat{f}_1}(1) \\ &= 0*0.36 + 0.25*0.48 + 1*0.16 \\ &= 0.28 \\ var(\hat{f}_1) &= E(\hat{f}_1^2) - E(\hat{f}_1)^2 \\ &= 0.28 - 0.4^2 \\ &= 0.12 \end{align}\]

- To calculate the variance, we can use the alternative formula: \[\begin{align} E(\bar{x}^2) &= 1^2*f_{\bar{x}}(1) +1.5^2*f_{\bar{x}}(1.5) + 2^2*f_{\bar{x}}(2) \\ &= 1*0.16 +2.25*0.48 + 4*0.36 \\ &= 2.68 \\ var(\bar{x}) &= E(\bar{x}^2) - E(\bar{x})^2 \\ &= 2.68 - 1.6^2 \\ &= 0.12 \end{align}\]

- To calculate the variance, we can use the alternative formula: \[\begin{align} E(xmin^2) &= 1^2*f_{xmin}(1) + 2^2*f_{xmin}(2) \\ &= 1*0.64 + 4*0.36 \\ &= 2.08 \\ var(xmin) &= E(xmin^2) - E(xmin)^2 \\ &= 2.08 - 1.36^2 \\ &= 0.23 \end{align}\]

- To calculate the variance, we can use the alternative formula: \[\begin{align} E(xmax^2) &= 1^2*f_{xmax}(1) + 2^2*f_{xmax}(2) \\ &= 1*0.16 + 4*0.84 \\ &= 3.52 \\ var(xmax) &= E(xmax^2) - E(xmax)^2 \\ &= 3.52 - 1.84^2 \\ &= 0.134 \end{align}\]

All three of these statistics are simple linear functions of the data, so their mean and variance can be calculated without using the PDF:

- The mean and variance are already given to us: \[\begin{align} E(x_1) &= 1.6 \\ var(x_1) &= 0.24 \end{align}\]

- The mean and variance can be found using the standard formulas for the sample average: \[\begin{align} E(\bar{x}) &= E(x_i) \\ &= 1.6 \\ var(\bar{x}) &= var(x_i)/2 \\ &= 0.24/2 \\ &= 0.12 \end{align}\]

- The mean and variance can be found using the standard formula for a linear function of two random variables: \[\begin{align} E(w) &= E(0.2*x_1 + 0.8*x_2) \\ &= 0.2*E(x_1) + 0.8*E(x_2) \\ &= 0.2*1.6 + 0.8*1.6 \\ &= 1.6 \\ var(w) &= var(0.2*x_1 + 0.8*x_2) \\ &= 0.2^2*var(x_1) + 0.8^2*var(x_2) + 2*0.2*0.8*cov(x_1,x_2)\\ &= 0.2^2*0.24 + 0.8^2*0.24 + 2*0.2*0.8*0 \\ &= 0.16 \end{align}\]

Unknown parameters: \(\mu\),\(\sigma^2\), \(E(x_i)\), \(E(x_i^3)\), \(var(x_i)\), and \(sd(x_i)/\sqrt{n}\).

Statistics: \(D_n\), \(\bar{x}\).We can find the true values directly from the PDF \(f_x(\cdot)\):

- The true probability is: \(\Pr(x_i = 1) = 0.4\)

- The population mean is: \(E(x_i) = 1*0.4 + 2*0.6 = 1.6\)

- The population variance is: \(var(x_i) = (1-1.6)^2*0.4 + (2-1.6)^2*0.6 = 0.24\)

- The population standard deviation is: \(sd(x_i) = \sqrt{var(x_i)} = \sqrt{0.24} = 0.49\)

- The population minimum is: \(min(S_x) = 1\)

- The population maximum is: \(max(S_x) = 2\)

Since \(\max(S_x) = 2\), the error is either \(err = 1 -2 = -1\) or \(err = 2 - 2 = 0\).

- The sampling error has support \(S_{err} = \{-1,0\}\)

- The sampling error has PDF: \[\begin{align} f_{err}(-1) &= f_{D_n}(1,1) \\ &= 0.16 \\ f_{err}(0) &= f_{D_n}(2,1) + f_{D_n}(1,2) + f_{D_n}(2,2) \\ &= 0.24 + 0.24 + 0.36 \\ &= 0.84 \end{align}\]

We have already calculated the mean of each statistic and the true value of each parameter, so we can calculate the bias and then use the result to classify each estimator:

- Unbiased \[\begin{align} bias(\hat{f}_1) &= E(\hat{f}_1) - \Pr(x_i=1) \\ &= 0.4 - 0.4 \\ &= 0 \end{align}\]

- Unbiased \[\begin{align} bias(\bar{x}) &= E(\bar{x}) - E(x_i) \\ &= 1.6 - 1.6 \\ &= 0 \end{align}\]

- Unbiased \[\begin{align} bias(\hat{\sigma}_x^2) &= E(\hat{\sigma}_x^2) - var(x_i) \\ &= 0.24 - 0.24 \\ &= 0 \end{align}\]

- Biased \[\begin{align} bias(\hat{\sigma}_x) &= E(\hat{\sigma}_x) - sd(x_i) \\ &= 0.34 - 0.49 \\ &= -0.15 \end{align}\]

- Biased \[\begin{align} bias(xmin) &= E(xmin) - \min(S_x) \\ &= 1.36 - 1 \\ &= 0.36 \end{align}\]

- Biased \[\begin{align} bias(xmax) &= E(xmax) - \max(S_x) \\ &= 1.84 - 2 \\ &= -0.16 \end{align}\]

Remember that the expected value passes through linear functions, but not nonlinear functions:

- It is unbiased, as \(E(\bar{y}_M - \bar{y}_W) = E(\bar{y}_M) - E(\bar{y}_W) = \mu_M - \mu_W\).

- It is biased, as \(E(\bar{y}_M/\bar{y}_W) \neq E(\bar{y}_M)/E(\bar{y}_W) = \mu_M/\mu_W\).

We have already calculated the variance and bias, so we can apply the formula \(MSE = var + bias^2\):

- The MSE is: \[\begin{align} MSE(\hat{f}_1) &= var(\hat{f}_1) + bias(\hat{f}_1)^2 \\ &= 0.12 + 0^2 \\ &= 0.12 \end{align}\]

- The MSE is: \[\begin{align} MSE(\bar{x}) &= var(\bar{x}) + bias(\bar{x})^2 \\ &= 0.12 + 0^2 \\ &= 0.12 \end{align}\]

- The MSE is: \[\begin{align} MSE(xmin) &= var(xmin) + bias(xmin)^2 \\ &= 0.23 + 0.36^2 \\ &= 0.36 \end{align}\]

- The MSE is: \[\begin{align} MSE(xmax) &= var(xmax) + bias(xmax)^2 \\ &= 0.13 + (-0.16)^2 \\ &= 0.16 \end{align}\]

Again, these estimators are both linear functions of the data, so their mean and variance are easy to calculate.

- Both estimators are unbiased.

- The variance is \(var(\bar{x}) = \sigma^2/2\)

- The variance is \(var(x_2) = \sigma^2\)

- The MSE is \(MSE(\bar{x}) = \sigma^2/2\)

- The MSE is \(MSE(x_2)= \sigma^2\)

- The estimator \(\bar{x}\) is preferred under the MVUE criterion.

- The estimator \(\bar{x}\) is preferred under the MSE criterion.

The standard error is: \[\begin{align} se(\bar{x}) &= \hat{\sigma}/\sqrt{n} \\ &= \sqrt{4}/\sqrt{100} \\ &= 0.2 \end{align}\]

Both the sample average (a) and the average of all even numbered observations (d) are consistent estimators of \(\mu\), because they keep using more and more information as the sample size increases. In contrast the estimators based on the first observation, and on the first 100 observations are both unbiased, but they do not change as the sample size increases. So the LLN does not apply, and the estimators are not consistent. The LLN does apply to the sample median because of Slutsky’s theorem, but that makes it a consistent estimator of the population median, which may or may not be equal to the population mean.

8 Statistical inference

Click here to see the problems

- The null is: \[H_0: \beta = 0\] and the alternative is: \[H_w: \beta \neq 0\]

- Test statistics need to possess characteristics (a), (d), and (e).

- In this setting:

- \(x_i\) must have a normal distribution.

- The asymptotic distribution is \(N(0,1)\)

- The expression is: \[t = \frac{\bar{x}-\mu_1}{\hat{\sigma}_x/\sqrt{n}} + \frac{\mu_1-\mu_0}{\hat{\sigma}_x/\sqrt{n}}\]

- This question is about calculating the size given the critical values.

- The size is:

\[\begin{align}

size &= F_{T_{13}}(-1.96) + 1 - F_{T_{13}}(1.96) \\

&= 0.035894296 + 1 - 0.964105704 \\

&\approx 0.07

\end{align}\]

and the formula for calculating this in Excel is

=T.DIST(-1.96,13,TRUE) +1 - T.DIST(1.96,13,TRUE). - The size is:

\[\begin{align}

size &= \Phi(-1.96) + 1 - \Phi(1.96) \\

&= 0.024997895 + 1 - 0.975002105 \\

&\approx 0.05

\end{align}\]

and the formula for calculating this in Excel is

=NORM.S.DIST(-1.96,TRUE) +1 - NORM.S.DIST(1.96,TRUE). - The size is:

\[\begin{align}

size &= F_{T_{13}}(-3) + 1 - F_{T_{13}}(2) \\

&\approx 0.005119449 + 1 - 0.966579821 \\

&\approx 0.04

\end{align}\]

and the formula for calculating this in Excel is

=T.DIST(-3,13,TRUE) +1 - T.DIST(1.96,13,TRUE). - The size is:

\[\begin{align}

size &= \Phi(-3) + 1 - \Phi(2) \\

&\approx 0.001349898 + 1 - 0.977249868 \\

&\approx 0.02

\end{align}\]

and the formula for calculating this in Excel is

=NORM.S.DIST(-3,TRUE) +1 - NORM.S.DIST(2,TRUE). - The size is:

\[\begin{align}

size &= F_{T_{13}}(-\infty) + 1 - F_{T_{13}}(2) \\

&\approx 0 + 1 - 0.966579821 \\

&\approx 0.03

\end{align}\]

and the formula for calculating this in Excel is

=1 - T.DIST(2,13,TRUE). - The size is:

\[\begin{align}

size &= \Phi(-\infty) + 1 - \Phi(2) \\

&\approx 0 + 1 - 0.977249868 \\

&\approx 0.02

\end{align}\]

and the formula for calculating this in Excel is

=1 - NORM.S.DIST(2,TRUE).

- The size is:

\[\begin{align}

size &= F_{T_{13}}(-1.96) + 1 - F_{T_{13}}(1.96) \\

&= 0.035894296 + 1 - 0.964105704 \\

&\approx 0.07

\end{align}\]

and the formula for calculating this in Excel is

- This problem asks you to find the critical values that deliver a given size.

- The critical values are:

\[\begin{align}

c_L &= F^{-1}_{T_{17}}(0.005) \\

&\approx -2.90 \\

c_H &= F^{-1}_{T_{17}}(0.995) \\

&\approx 2.90

\end{align}\]

and the formulas for calculating this in Excel are

=T.INV(0.005,17)and=T.INV(0.995,17). - The critical values are:

\[\begin{align}

c_L &= F^{-1}_{T_{17}}(0.025) \\

&\approx -2.11 \\

c_H &= F^{-1}_{T_{17}}(0.975) \\

&\approx 2.11

\end{align}\]

and the formulas for calculating this in Excel are

=T.INV(0.025,17)and=T.INV(0.975,17). - The critical values are:

\[\begin{align}

c_L &= F^{-1}_{T_{17}}(0.05) \\

&\approx -1.74 \\

c_H &= F^{-1}_{T_{17}}(0.95) \\

&\approx 1.74

\end{align}\]

and the formulas for calculating this in Excel are

=T.INV(0.05,17)and=T.INV(0.95,17). - The critical values are:

\[\begin{align}

c_L &= \Phi^{-1}(0.005) \\

&\approx -2.58 \\

c_H &= \Phi^{-1}(0.995) \\

&\approx 2.58

\end{align}\]

and the formulas for calculating this in Excel are

=NORM.S.INV(0.005)and=NORM.S.INV(0.995). - The critical values are:

\[\begin{align}

c_L &= \Phi^{-1}(0.025) \\

&\approx -1.96 \\

c_H &= \Phi^{-1}(0.975) \\

&\approx 1.96

\end{align}\]

and the formulas for calculating this in Excel are

=NORM.S.INV(0.025)and=NORM.S.INV(0.975). - The critical values are:

\[\begin{align}

c_L &= \Phi^{-1}(0.05) \\

&\approx -1.65 \\

c_H &= \Phi^{-1}(0.95) \\

&\approx 1.65

\end{align}\]

and the formulas for calculating this in Excel are

=NORM.S.INV(0.05)and=NORM.S.INV(0.95).

- The critical values are:

\[\begin{align}

c_L &= F^{-1}_{T_{17}}(0.005) \\

&\approx -2.90 \\

c_H &= F^{-1}_{T_{17}}(0.995) \\

&\approx 2.90

\end{align}\]

and the formulas for calculating this in Excel are

- The confidence interval for a mean always follows the same formula

- The confidence interval is:

\[\begin{align}

CI^{95} &= \bar{x} \pm F_{T_{15}}^{-1}(0.975)*\hat{\sigma}/\sqrt{n} \\

&\approx 4 \pm 2.13*0.3/\sqrt{16} \\

&\approx (3.84, 4.16)

\end{align}\]

and the formulas for calculating these numbers in Excel are

=4-T.INV(0.975,15)*0.3/SQRT(16)and=4+T.INV(0.975,15)*0.3/SQRT(16) - The confidence interval is:

\[\begin{align}

CI^{90} &= \bar{x} \pm F_{T_{15}}^{-1}(0.95)*\hat{\sigma}/\sqrt{n} \\

&\approx 4 \pm 1.75*0.3/\sqrt{16} \\

&\approx (3.87, 4.13)

\end{align}\]

and the formulas for calculating these numbers in Excel are

=4-T.INV(0.95,15)*0.3/SQRT(16)and=4+T.INV(0.95,15)*0.3/SQRT(16) - The confidence interval is:

\[\begin{align}

CI^{99} &= \bar{x} \pm F_{T_{15}}^{-1}(0.995)*\hat{\sigma}/\sqrt{n} \\

&\approx 4 \pm 2.95*0.3/\sqrt{16} \\

&\approx (3.77, 4.22)

\end{align}\]

and the formulas for calculating these numbers in Excel are

=4-T.INV(0.995,15)*0.3/SQRT(16)and=4+T.INV(0.995,15)*0.3/SQRT(16) - The confidence interval is:

\[\begin{align}

CI^{95} &= \bar{x} \pm \Phi^{-1}(0.975)*\hat{\sigma}/\sqrt{n} \\

&\approx 4 \pm 1.96*0.3/\sqrt{16} \\

&\approx (3.85, 4.15)

\end{align}\]

and the formulas for calculating these numbers in Excel are

=4-NORM.S.INV(0.975)*0.3/SQRT(16)and=4+NORM.S.INV(0.975)*0.3/SQRT(16) - The confidence interval is:

\[\begin{align}

CI^{90} &= \bar{x} \pm \Phi^{-1}(0.95)*\hat{\sigma}/\sqrt{n} \\

&\approx 4 \pm 1.64*0.3/\sqrt{16} \\

&\approx (3.88, 4.12)

\end{align}\]

and the formulas for calculating these numbers in Excel are

=4-NORM.S.INV(0.95)*0.3/SQRT(16)and=4+NORM.S.INV(0.95)*0.3/SQRT(16) - The confidence interval is:

\[\begin{align}

CI^{99} &= \bar{x} \pm \Phi^{-1}(0.995)*\hat{\sigma}/\sqrt{n} \\

&\approx 4 \pm 2.58*0.3/\sqrt{16} \\

&\approx (3.81, 4.19)

\end{align}\]

and the formulas for calculating these numbers in Excel are

=4-NORM.S.INV(0.995)*0.3/SQRT(16)and=4+NORM.S.INV(0.995)*0.3/SQRT(16)

- The confidence interval is:

\[\begin{align}

CI^{95} &= \bar{x} \pm F_{T_{15}}^{-1}(0.975)*\hat{\sigma}/\sqrt{n} \\

&\approx 4 \pm 2.13*0.3/\sqrt{16} \\

&\approx (3.84, 4.16)

\end{align}\]

and the formulas for calculating these numbers in Excel are

- The only thing we have tested here is whether there is no effect. We rejected that null,

so we can rule out the possibility that there is no effect. But that does not tell us whether the

effect is small or large - in order to say anything about that question we need to test

other nulls, or construct a confidence interval.

- Probably false.

- Probably true.

- Possibly true.

- The only thing we have tested here is whether there is no effect, and we haven’t been

able to rule out that possibility. So we can’t really rule anything out.

- Possibly true.

- Possibly true.

- Possibly true.

- In effect, the confidence interval simultaneously reports the results of every possible

null hypothesis. So anything in the range \((0.10,0.40)\) cannot be ruled out but anything

outside of that range can be ruled out.

- Probably false.

- Probably true.

- Probably true.

- Probably false.

9 An introduction to R

Click here to see the problems

- The chapter describes how to do each of these.

- Items (a), (b), (d), and (e) are valid R expressions.

- Write the R code to perform the following actions:

cookies <- c("oatmeal", "chocolate chip", "shortbread")threes <- seq(3,100,by=3)threes[5]threecookies <- list(cookies = cookies, threes = threes).

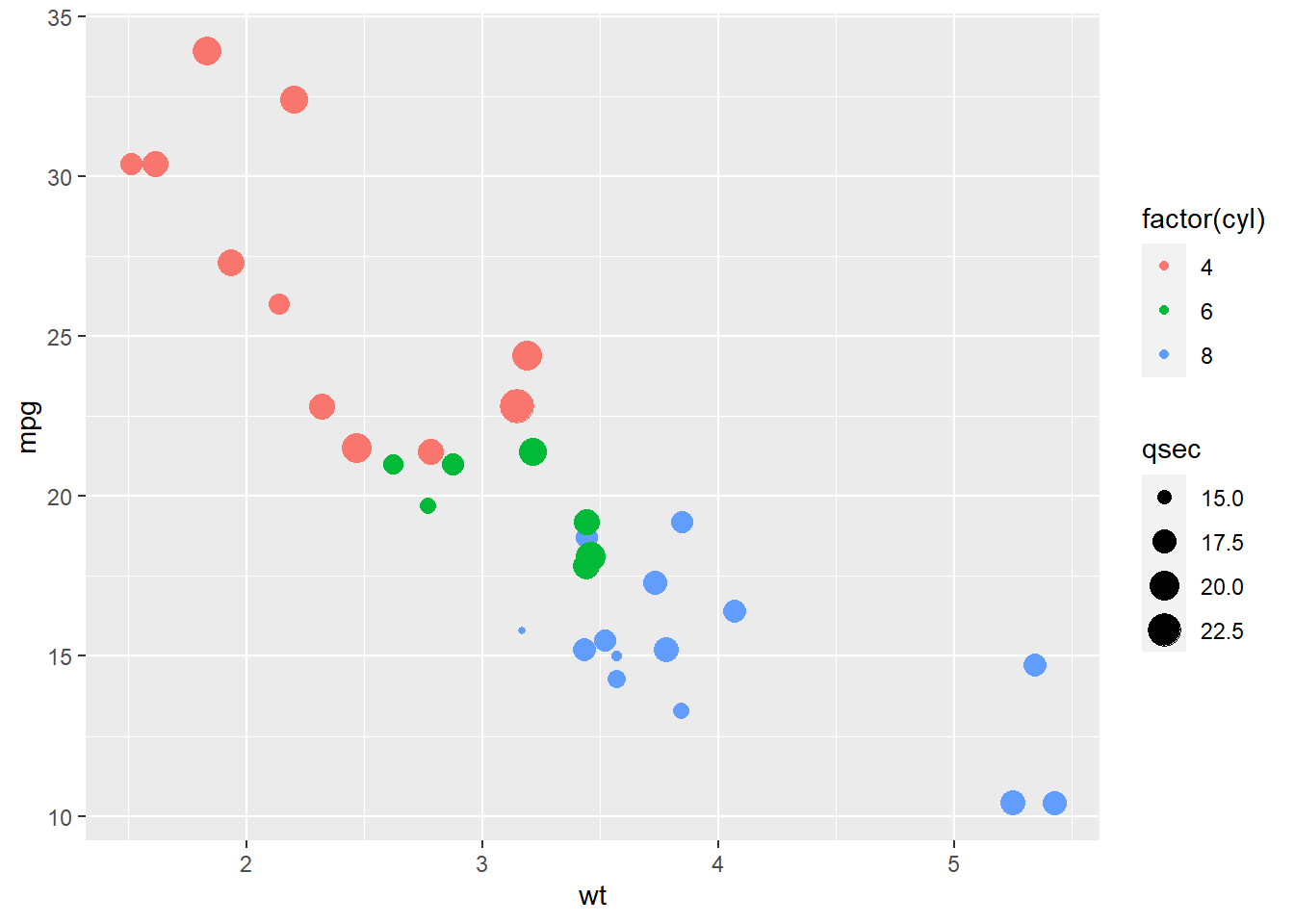

- This code will load a built-in data set of automobile gas mileage, and produce a graph that depicts the relationship between weight and miles per gallon:

data("mtcars") # load data

ggplot(mtcars, aes(wt, mpg)) + geom_point(aes(colour = factor(cyl), size = qsec))

10 Advanced data cleaning

Click here to see the problems

- The file formats are:

- Fixed width

- Space or tab delimited

- CSV

- Here are my descriptions, yours may be somewhat different:

- A crosswalk table is a data table we can use to translate variables that are expressed in one way into another way. For example, we might use a crosswalk table to translate country names into standardized country codes, or to translate postal codes into provinces.

- When we have two data tables that contain information on related cross-sectional

units, we can combine their information into a single table by matching observations based on a variable that (a) exists in both tables and (b) connects the observations in some way. - Aggregating data by groups allows us to group observations according to a common characteristic, and describe those groups using data calculated from the individual observations.

- You can edit cell A1 under scenarios (a) and (c).

- If you do this:

- Nothing will happen, but you can ask Excel to mark invalid data.

- Excel will not allow you to enter invalid data.

- The R code will be something like this.

library("tidyverse")

deniro <- read_csv("https://people.sc.fsu.edu/~jburkardt/data/csv/deniro.csv")

## Rows: 87 Columns: 3

## -- Column specification --------------------------------------------------------

## Delimiter: ","

## chr (1): Title

## dbl (2): Year, Score

##

## i Use `spec()` to retrieve the full column specification for this data.

## i Specify the column types or set `show_col_types = FALSE` to quiet this message.

nrow(deniro)

## [1] 87

ncol(deniro)

## [1] 311 Using R

Click here to see the problems

- The R code to create this data table is as follows:

PPData <- EmpData %>%

mutate(Year = format(MonthYr, "%Y")) %>%

mutate(EmpRate = Employed/Population) %>%

filter(Year >= 2010) %>%

select(MonthYr, Year, EmpRate, UnempRate, AnnPopGrowth) %>%

arrange(EmpRate)

print(PPData)## # A tibble: 133 x 5

## MonthYr Year EmpRate UnempRate AnnPopGrowth

## <date> <chr> <dbl> <dbl> <dbl>

## 1 2020-04-01 2020 0.521 0.131 0.0132

## 2 2020-05-01 2020 0.530 0.137 0.0124

## 3 2020-06-01 2020 0.560 0.125 0.0118

## 4 2020-07-01 2020 0.573 0.109 0.0109

## 5 2020-08-01 2020 0.580 0.102 0.0104

## 6 2020-03-01 2020 0.585 0.0789 0.0143

## 7 2021-01-01 2021 0.586 0.0941 0.00863

## 8 2020-09-01 2020 0.591 0.0918 0.00992

## 9 2020-12-01 2020 0.593 0.0876 0.00905

## 10 2020-10-01 2020 0.594 0.0902 0.00961

## # ... with 123 more rows- The R code is as follows. None of the variables have missing data.

### A: Mean employment rate

mean(PPData$EmpRate)## [1] 0.610809### B: Table of medians

PPData %>%

select(where(is.numeric)) %>%

lapply(median)## $EmpRate

## [1] 0.6139724

##

## $UnempRate

## [1] 0.07082771

##

## $AnnPopGrowth

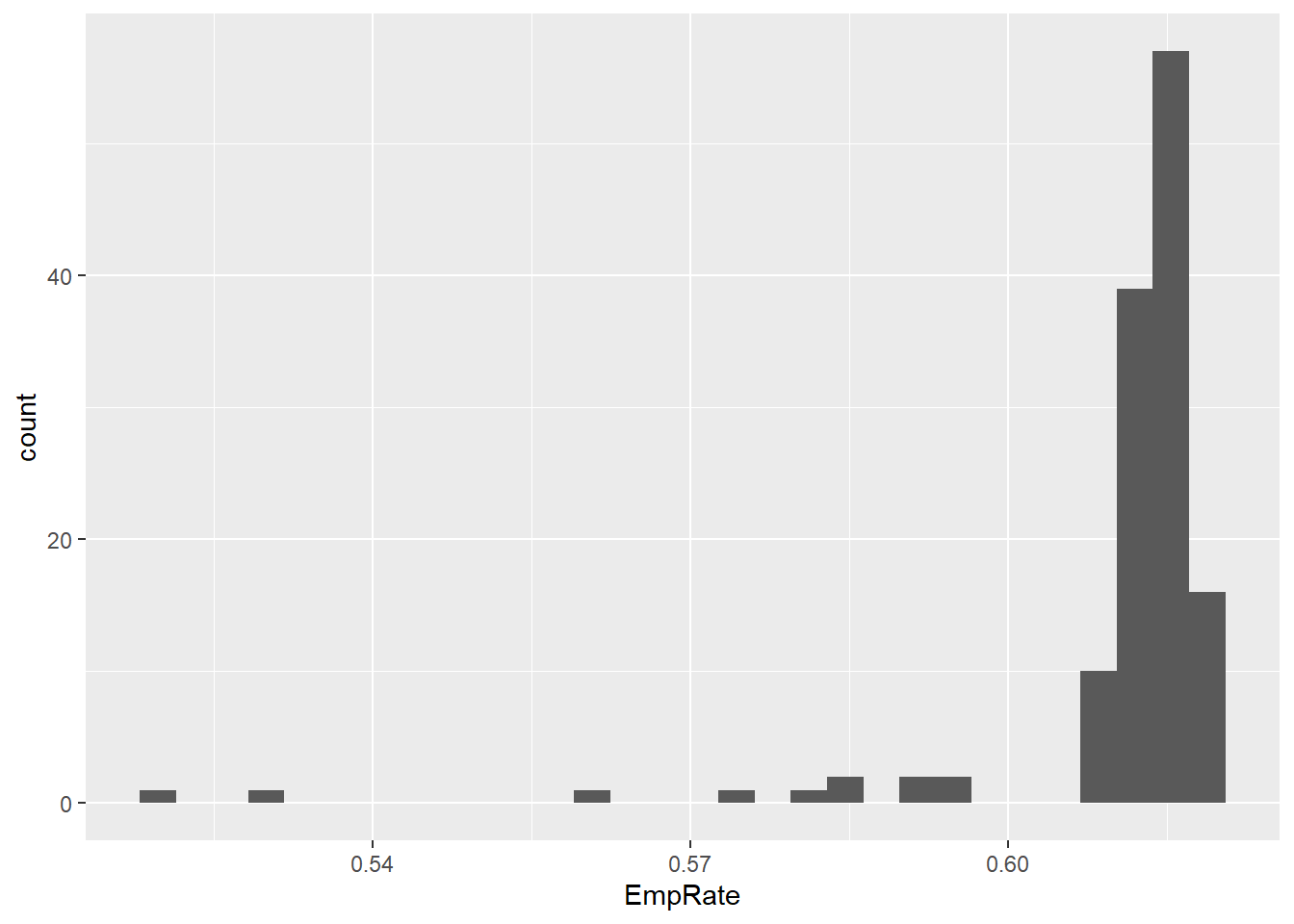

## [1] 0.01171851- The employment rate is a continuous variable, so the appropriate kind of frequency table here is a binned frequency table.

PPData %>%

count(cut_interval(EmpRate, 6))## # A tibble: 5 x 2

## `cut_interval(EmpRate, 6)` n

## <fct> <int>

## 1 [0.521,0.537] 2

## 2 (0.554,0.57] 1

## 3 (0.57,0.587] 4

## 4 (0.587,0.603] 4

## 5 (0.603,0.62] 122- The R code for these calculations is as follows:

qnorm(0.45, mean = 4, sd = 6)## [1] 3.246032qt(0.975, df = 8)## [1] 2.306004pnorm(0.75)## [1] 0.7733726rbinom(5, size = 10, prob = 0.5)## [1] 6 6 3 5 5- The code below is the minimal code needed to create the histogram using the default options. You could improve on the graph quite easily by adjusting some of these options.

ggplot(data = PPData, mapping = aes(x = EmpRate)) + geom_histogram()

## `stat_bin()` using `bins = 30`. Pick better value with `binwidth`.

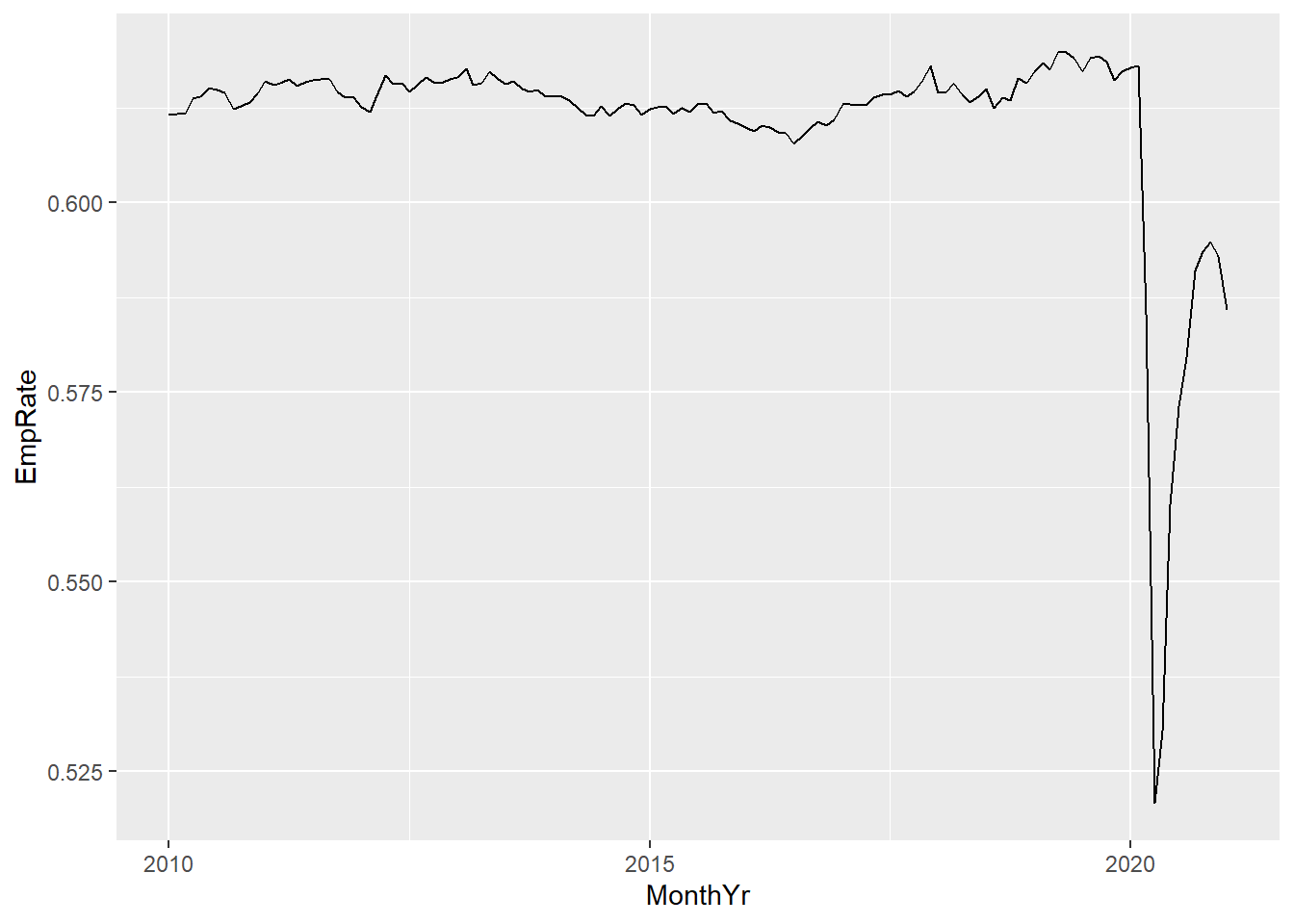

- The code below is the minimal code needed to create the graph using the default options. You could improve on the graph quite easily by adjusting some of these options.

ggplot(data = PPData, mapping = aes(x = MonthYr, y = EmpRate)) + geom_line()

12 Multivariate data analysis

Click here to see the problems

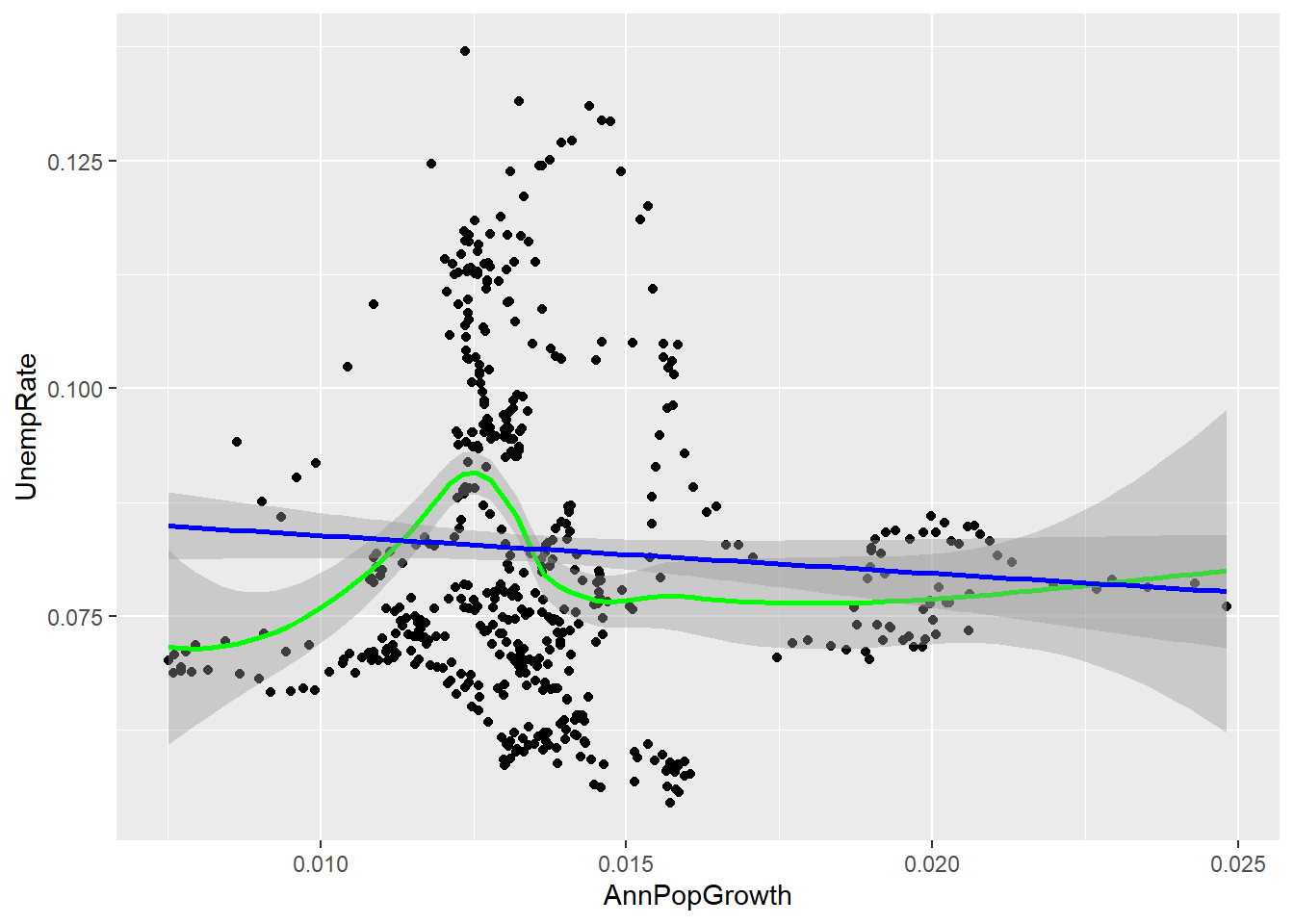

- The covariance and correlation is negative here, so periods of high population growth tend to be periods of low unemployment.

cov(EmpData$UnempPct, EmpData$AnnPopGrowth, use = "complete.obs")

## [1] -0.0003017825

cor(EmpData$UnempPct, EmpData$AnnPopGrowth, use = "complete.obs")

## [1] -0.06513125- I used casewise deletion but it does not matter. It only matters when you add a third variable.

- The tables are

- Simple frequency table

- Conditional average

- Crosstab

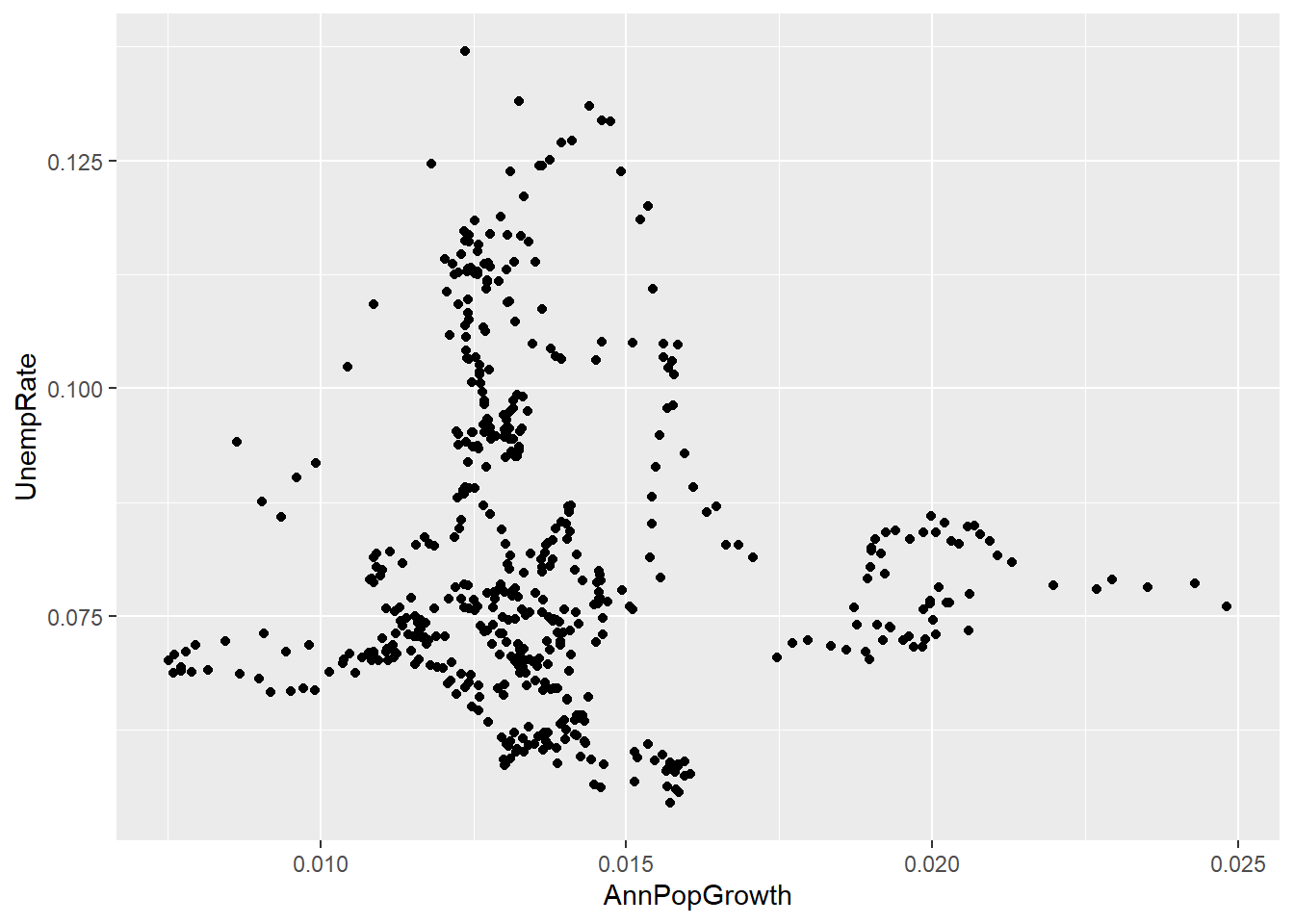

- The scatter plot should look something like this:

ggplot(data = EmpData, mapping = aes(x = AnnPopGrowth, y = UnempRate)) + geom_point()

## Warning: Removed 12 rows containing missing values (geom_point).

- The plot should look something like this:

ggplot(data = EmpData, mapping = aes(x = AnnPopGrowth, y = UnempRate)) + geom_point() +

geom_smooth(col = "green") + geom_smooth(method = "lm", col = "blue")

## `geom_smooth()` using method = 'loess' and formula 'y ~ x'

## Warning: Removed 12 rows containing non-finite values (stat_smooth).

## `geom_smooth()` using formula 'y ~ x'

## Warning: Removed 12 rows containing non-finite values (stat_smooth).

## Warning: Removed 12 rows containing missing values (geom_point).

Appendix A Math review

Click here to see the problems

- In my case it would be \(A = (Brian, Charlie, Hazel, Sue)\).

- This would be \(B = \{x \in Z: 1 \leq x \leq 1000\}\)

- The cardinality is \(|A| = 4\) (in my case, yours may be different) and \(|B| = 1000\).

- Remember that sets are subsets of themselves.

- \(B\) and \(D\) are identical (\(B = D\))

- \(C\) is disjoint with \(A\)

- All four sets are subsets of \(A\) (\(A \subset A\), \(B \subset A\), \(C \subset A\), and \(D \subset A\))

- \(C\) and \(D\) are subsets of \(B\).

- Remember that \(\cap\) means “and,” \(\cup\) means “or,” and \({}^C\) means “not”

- \(A \cap B = \{2\}\)

- \(A \cup B = \{1,2,3,4\}\)

- \(A \cap D = \{2\}\)

- \(A \cup D = \{1,2,3\}\)

- \(B^C = \{1,3,5\}\)

- Enumeration is not an option here, so we use set-builder notation: \(B^C = \{x \in \mathbb{Z}: x \notin \{2,4\}\}\)

- Remember that the indicator function \(I(\cdot)\) returns one for true

statements and zero for false statements.

- \(I(x < 5) = I(4 < 5) =1\)

- \(I(x \textrm{ is an odd number}) = I(4 \textrm{ is an odd number}) = 0\)

- \(I(x < 5) - I(\sqrt{x} \textrm{ is an integer}) = I(4 < 5) - I(\sqrt{4} \textrm{ is an integer}) = 1 - 1 = 0\)

- The limits are:

- The limit of this sequence is \(0\)

- This sequence has no limit.

- The limit of this sequence is \(5\)

- The limit of this sequence is \(0\)

- The limit of this sequence is \(\infty\)

- The summation values are:

- \(\sum_{x = 1}^5 x^2 = 1^2 + 2^2 + 3^2 + 4^2 + 5^2 = 55\)

- \(\sum_{i \in \{1,3,5\}} \ln(i) = \ln(1) + \ln(3) + \ln(5) \approx 2.708\)

- \(\sum_{i \in 1}^\infty x_i I(i < 4) = x_1 + x_2 + x_3\)

- Statements (a) and (c) are true.