Chapter 6 Multivariate Models

6.1 Constructing and sampling multivariate distributions

Illustrating the construction and sampling of several multivariate distributions (mostly elliptical).

Understanding the construction of multivariate normal distributions, normal variance mixtures, elliptical distributions etc.

6.1.1 Basic ‘ingredients’

Building a covariance/correlation matrix

Covariance matrix:

A = matrix(c(4, 0,

1, 1), ncol = 2, byrow = TRUE) # Cholesky factor of the ...

(Sigma = A %*% t(A)) # ... symmetric, positive definite (covariance) matrix Sigma## [,1] [,2]

## [1,] 16 4

## [2,] 4 2Corresponding correlation matrix:

(P = outer(1:2, 1:2, Vectorize(function(r, c)

Sigma[r,c]/(sqrt(Sigma[r,r])*sqrt(Sigma[c,c]))))) # construct the corresponding correlation matrix## [,1] [,2]

## [1,] 1.0000000000 0.7071067812

## [2,] 0.7071067812 1.0000000000(P. = cov2cor(Sigma)) # for a more elegant solution, see the source of cov2cor()## [,1] [,2]

## [1,] 1.0000000000 0.7071067812

## [2,] 0.7071067812 1.0000000000stopifnot(all.equal(P., P))Another option would be as.matrix(Matrix::nearPD(Sigma, corr = TRUE, maxit = 1000)$mat) which works differently, though (by finding a correlation matrix close to the given matrix in the Frobenius norm) and thus gives a different answer.

Decomposing a covariance/correlation matrix

We frequently need to decompose a covariance matrix \(\Sigma\) (or correlation matrix \(P\)) as \(\Sigma = A A^\top\). To this end there are several possibilities.

The Cholesky decomposition:

A. = t(chol(Sigma)) # the Cholesky factor (lower triangular with real entries > 0)

stopifnot(all.equal(A. %*% t(A.) , Sigma), # checking decomposition

all.equal(A., A)) # checking uniqueness of the Cholesky decompositionOther decompositions of \(\Sigma\) than A %*% t(A) are possible, too:

if(FALSE) {

## Eigendecomposition (or spectral decomposition)

eig = eigen(Sigma) # eigenvalues and eigenvectors

V = eig$vectors # matrix of eigenvectors

Lambda = diag(pmax(eig$values, 0))

stopifnot(all.equal(Sigma, V %*% Lambda %*% t(V))) # for real, symmetric matrices

A.eig = V %*% sqrt(Lambda) %*% t(V)

Sigma.eig = A.eig %*% t(A.eig)

stopifnot(all.equal(Sigma.eig, Sigma))

## ... but A.. (non-triangular) and A (triangular) are different

## Singular-value decomposition

sv = svd(Sigma) # singular values, U, V (left/right singular vectors) such that Sigma = U diag(<singular values>) V^T

A.sv = sv$u %*% sqrt(diag(pmax(sv$d, 0))) %*% t(sv$v)

Sigma.sv = A.sv %*% t(A.sv)

stopifnot(all.equal(Sigma.sv, Sigma))

}6.1.2 Sampling from the multivariate normal distribution

Sampling \(Z\) (\(\text{iid } \mathcal{N}(0,1)\))

n = 1000 # sample size

d = 2 # dimension

set.seed(271) # set a seed (for reproducibility)

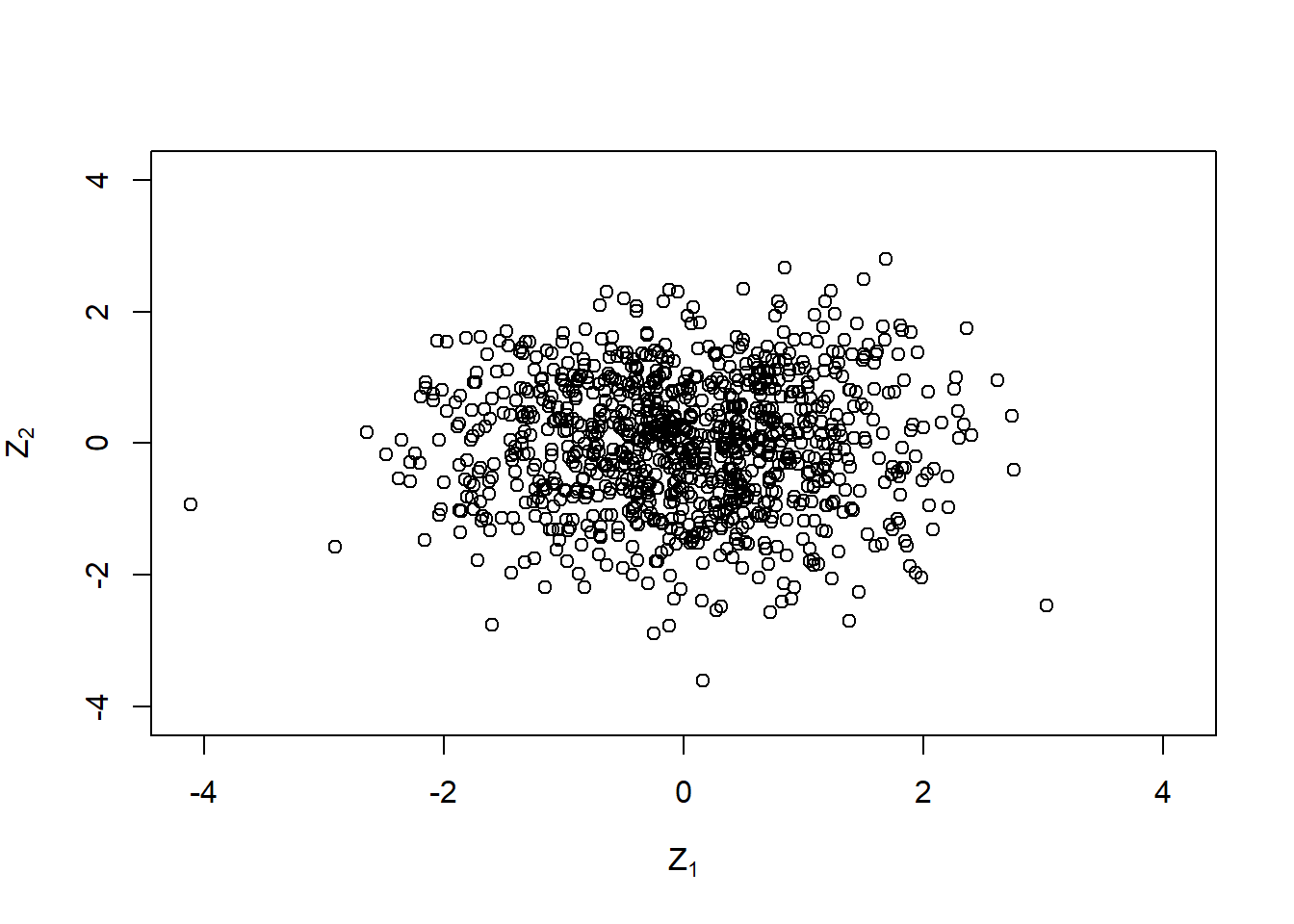

Z = matrix(rnorm(n * d), ncol = d) # sample iid N(0,1) random variates

mabs = max(abs(Z))

lim = c(-mabs, mabs)

plot(Z, xlim = lim, ylim = lim,

xlab = expression(Z[1]), ylab = expression(Z[2]))

Change the covariance matrix from identity to \(\Sigma\):

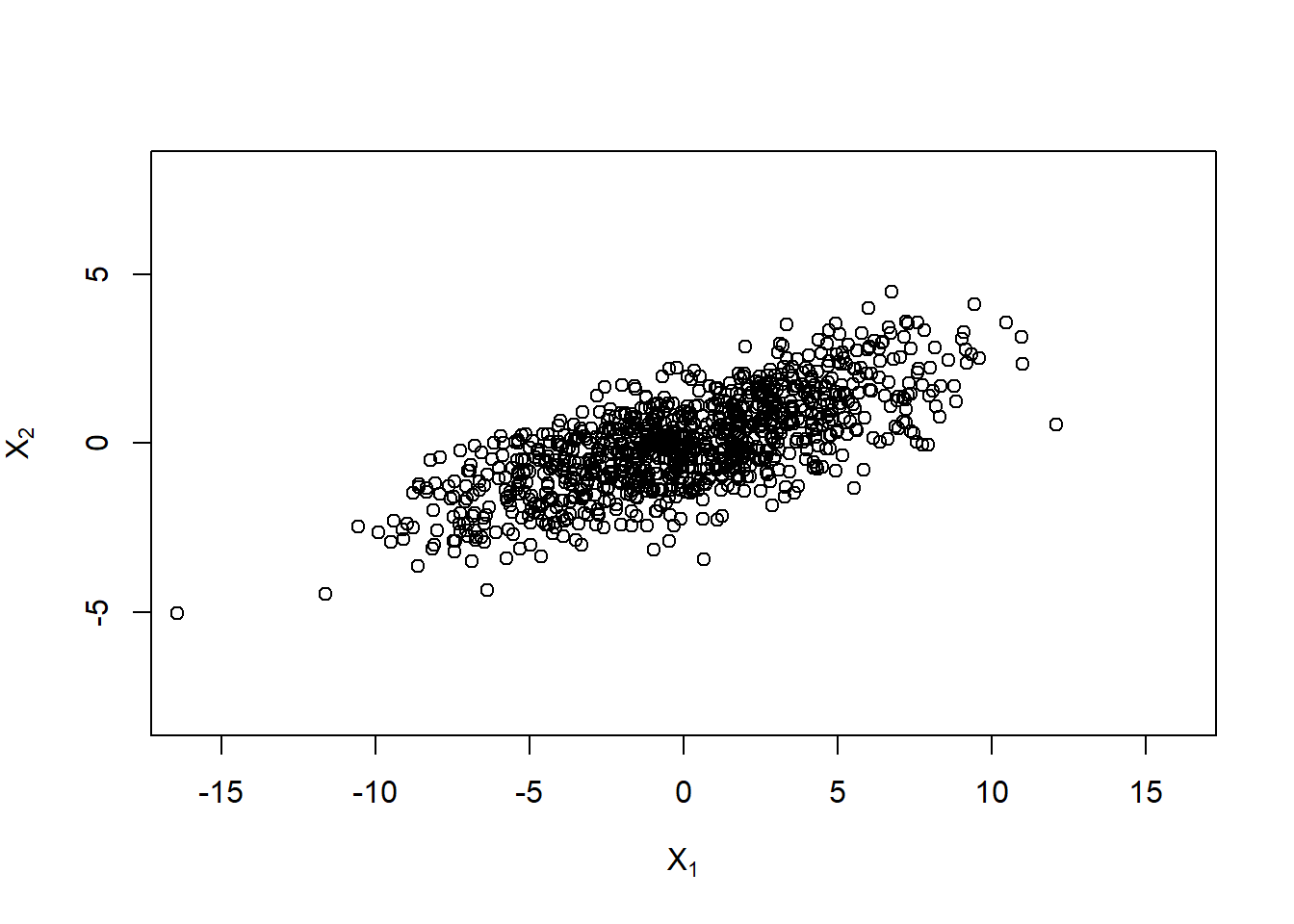

X. = t(A %*% t(Z)) # ~ N_d(0, Sigma)

xlim = c(-16, 16)

ylim = c(-8, 8)

plot(X., xlim = xlim, ylim = ylim,

xlab = expression(X[1]), ylab = expression(X[2]))

Use a shift to get \(X \sim \mathcal{N}_d(\mu, \Sigma)\):

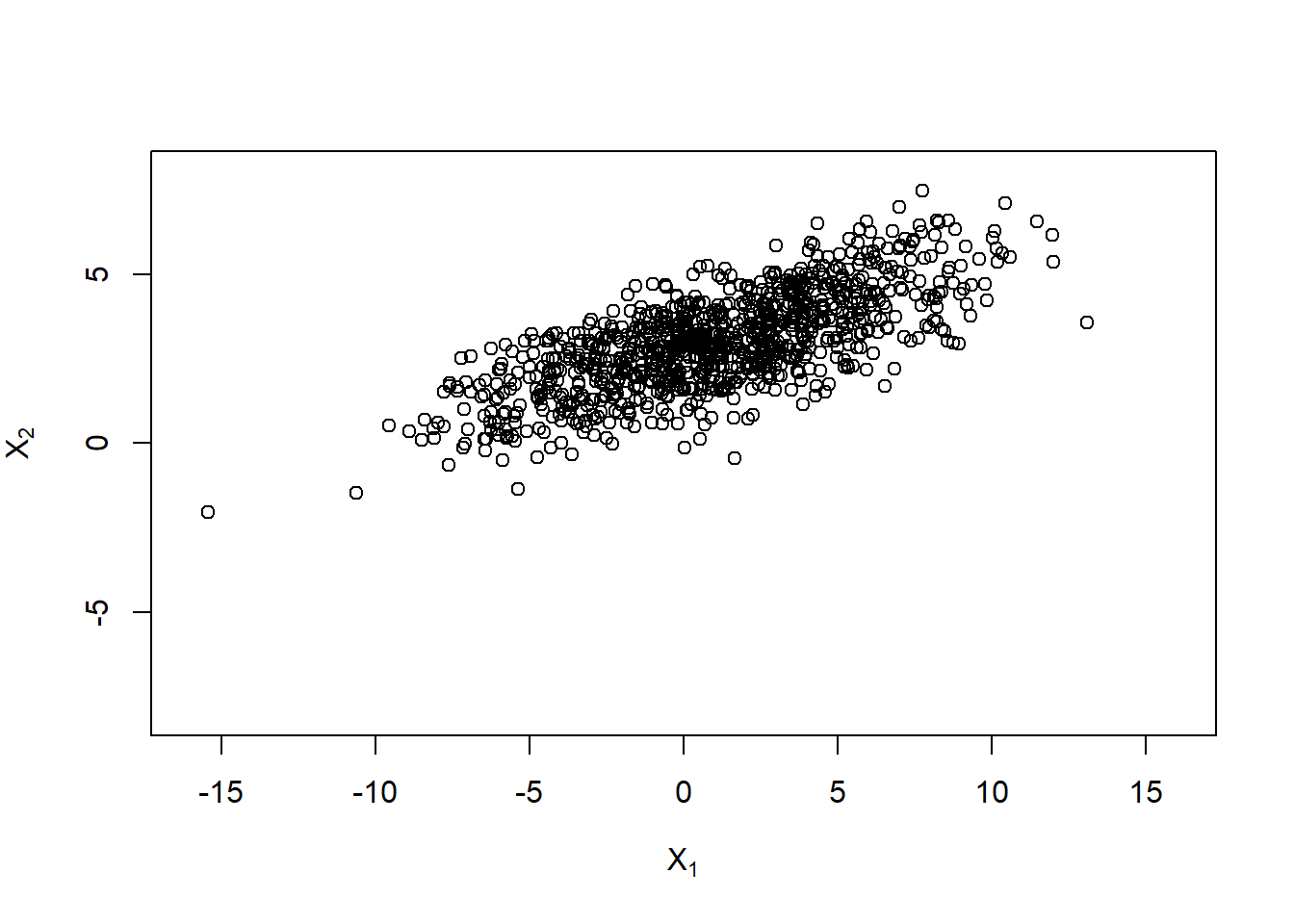

mu = c(1, 3)

X.norm = rep(mu, each = n) + X.

plot(X.norm, xlim = xlim, ylim = ylim,

xlab = expression(X[1]), ylab = expression(X[2]))

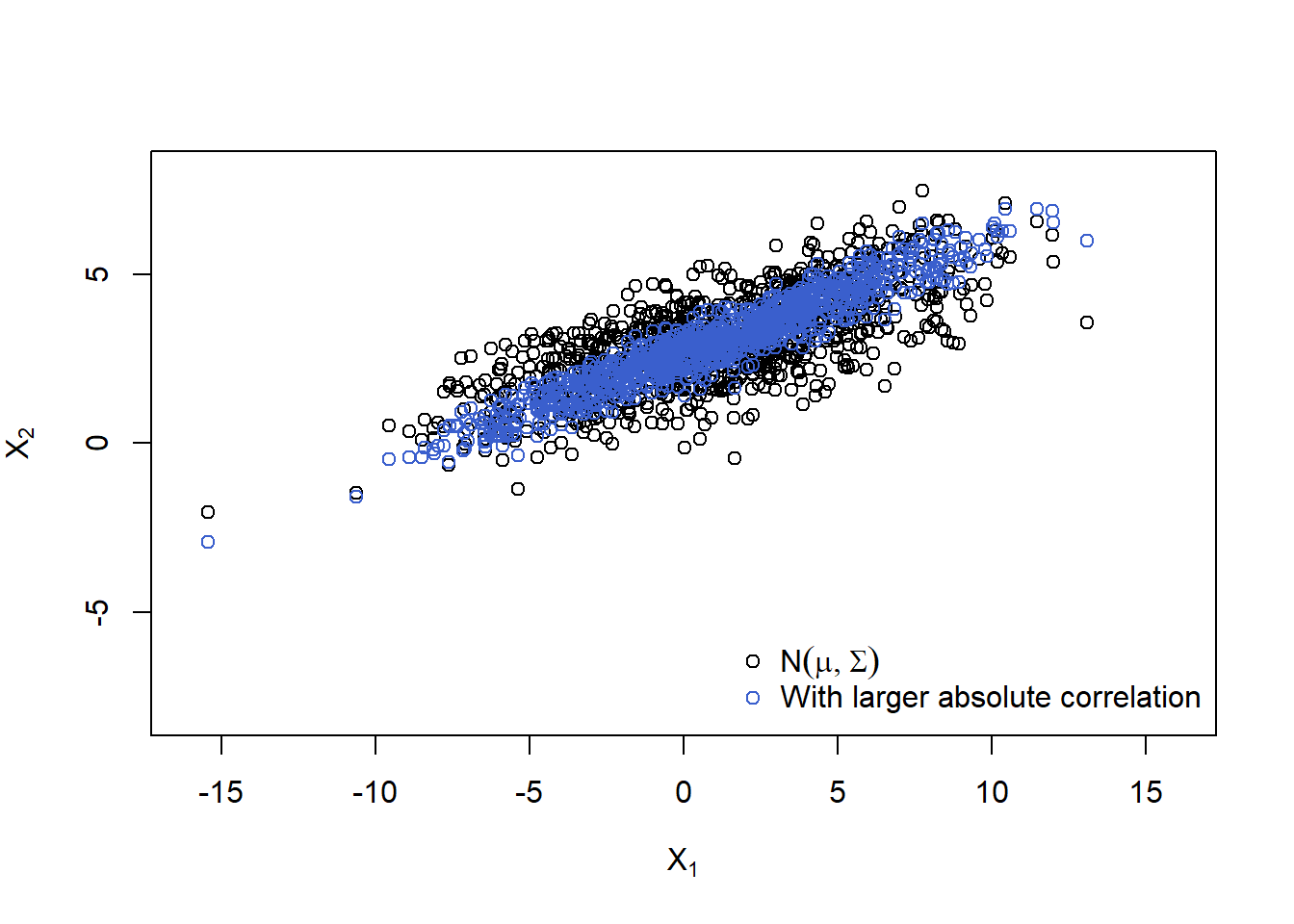

## Think about why the rep() and why the t()'s above!Plot (even larger correlation):

P. = matrix(c( 1, 0.95,

0.95, 1), ncol = d, byrow = TRUE)

Sigma. = outer(1:d, 1:d, Vectorize(function(r, c)

P.[r,c] * (sqrt(Sigma[r,r])*sqrt(Sigma[c,c])))) # construct the corresponding Sigma

## Note: When manually changing the off-diagonal entry of Sigma make sure that

## |Sigma.[1,2]| <= sqrt(Sigma.[1,1]) * sqrt(Sigma.[2,2]) still holds

A. = t(chol(Sigma.)) # new Cholesky factor

X.norm. = rep(mu, each = n) + t(A. %*% t(Z)) # generate the sample

plot(rbind(X.norm, X.norm.), xlim = xlim, ylim = ylim,

xlab = expression(X[1]), ylab = expression(X[2]),

col = rep(c("black", "royalblue3"), each = n))

legend("bottomright", bty = "n", pch = c(1,1), col = c("black", "royalblue3"),

legend = c(expression(N(mu,Sigma)),

expression("With larger absolute correlation")))

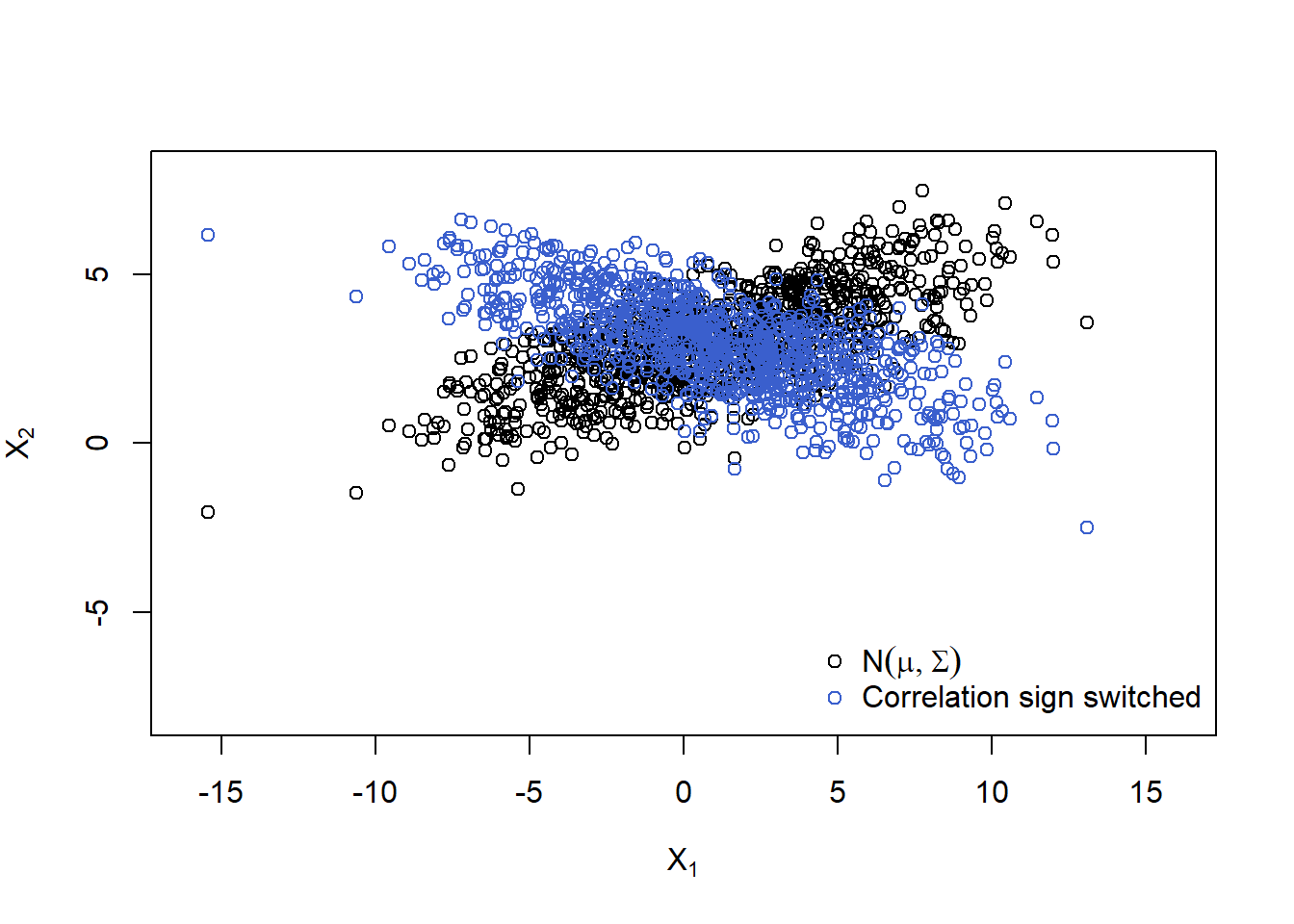

Plot (switch sign of correlation):

Sigma. = Sigma * matrix(c( 1, -1,

-1, 1), ncol = d, byrow = TRUE)

A. = t(chol(Sigma.))

X.norm. = rep(mu, each = n) + t(A. %*% t(Z))

plot(rbind(X.norm, X.norm.), xlim = xlim, ylim = ylim,

xlab = expression(X[1]), ylab = expression(X[2]),

col = rep(c("black", "royalblue3"), each = n))

legend("bottomright", bty = "n", pch = c(1,1), col = c("black", "royalblue3"),

legend = c(expression(N(mu,Sigma)),

expression("Correlation sign switched")))

## Note: This has all been done based on the same Z (and we also recycle it below)!6.1.3 Sampling from the multiv. \(t\) distribution (and other normal variance mixtures)

Definition 6.1 (multivariate normal variance mixture distribution) The random vector \(\boldsymbol{X}\) is said to have a (multivariate) normal variance mixture distribution if \[ \boldsymbol{X} \stackrel{d}{=} \boldsymbol{\mu} + \sqrt{W}A \boldsymbol{Z}, \] where

\(\boldsymbol{Z} \sim \mathcal{N}_k(\boldsymbol{0}, I_k)\) ;

\(W \geq 0\) is a non-negative, scalar-valued rv that is independent of \(\boldsymbol{Z}\), and

\(A \in \mathbb{R}^{d \times k}\) and \(\boldsymbol{\mu} \in \mathbb{R}^d\) are a matrix and a vector of constants, respectively.

\(\blacksquare\)

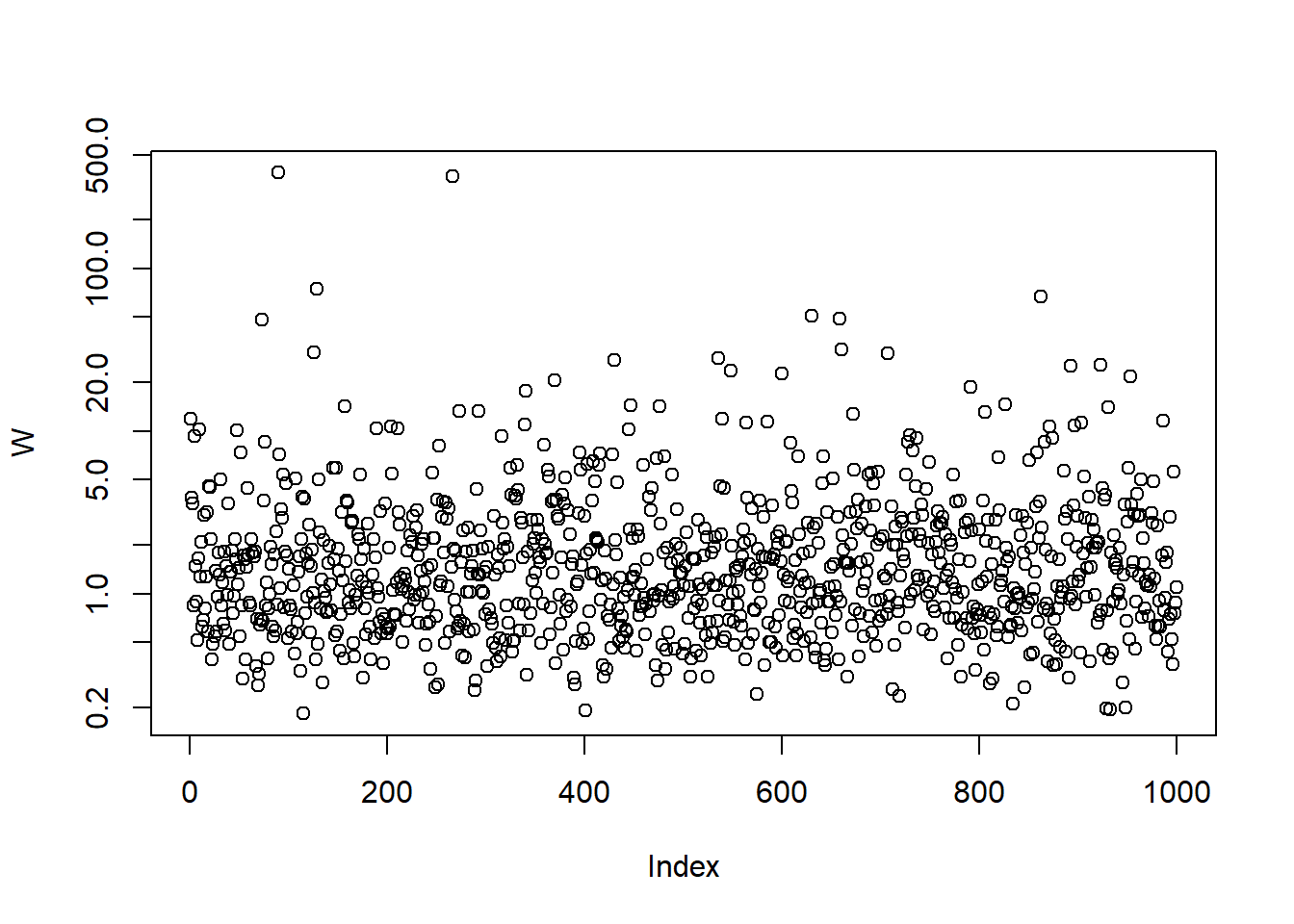

A sample from a multivariate \(t_\nu\) distribution

Example 6.1 (multivariate \(t\) distribution) If we take \(W\) to be an rv with an inverse gamma distribution \(W \sim \operatorname{Ig}\left(\frac{1}{2} \nu, \frac{1}{2} \nu \right)\) (which is equivalent to saying that \(\nu/W \sim \chi_{\nu}^{2}\)), then \(\boldsymbol{X}\) has a multivariate \(t\) distribution with \(\nu\) degrees of freedom. Our notation for the multivariate \(t\) is \(\boldsymbol{X} \sim t_{d}(\nu, \boldsymbol{\mu}, \Sigma)\), and we note that \(\Sigma\) is not the covariance matrix of \(\boldsymbol{X}\) in this definition of the multivariate \(t\). Since \(E(W)=\nu /(\nu-2)\) we have \(\operatorname{cov}(\boldsymbol{X})=(\nu /(\nu-2)) \Sigma\), and the covariance matrix (and correlation matrix ) of this distribution is only defined if \(\nu>2\).

MFE (2015, Example 6.7)\(\blacksquare\)

nu = 3 # degrees of freedom

set.seed(314)

W = 1/rgamma(n, shape = nu/2, rate = nu/2) # mixture variable for a multiv. t_nu distribution

plot(W, log = "y")

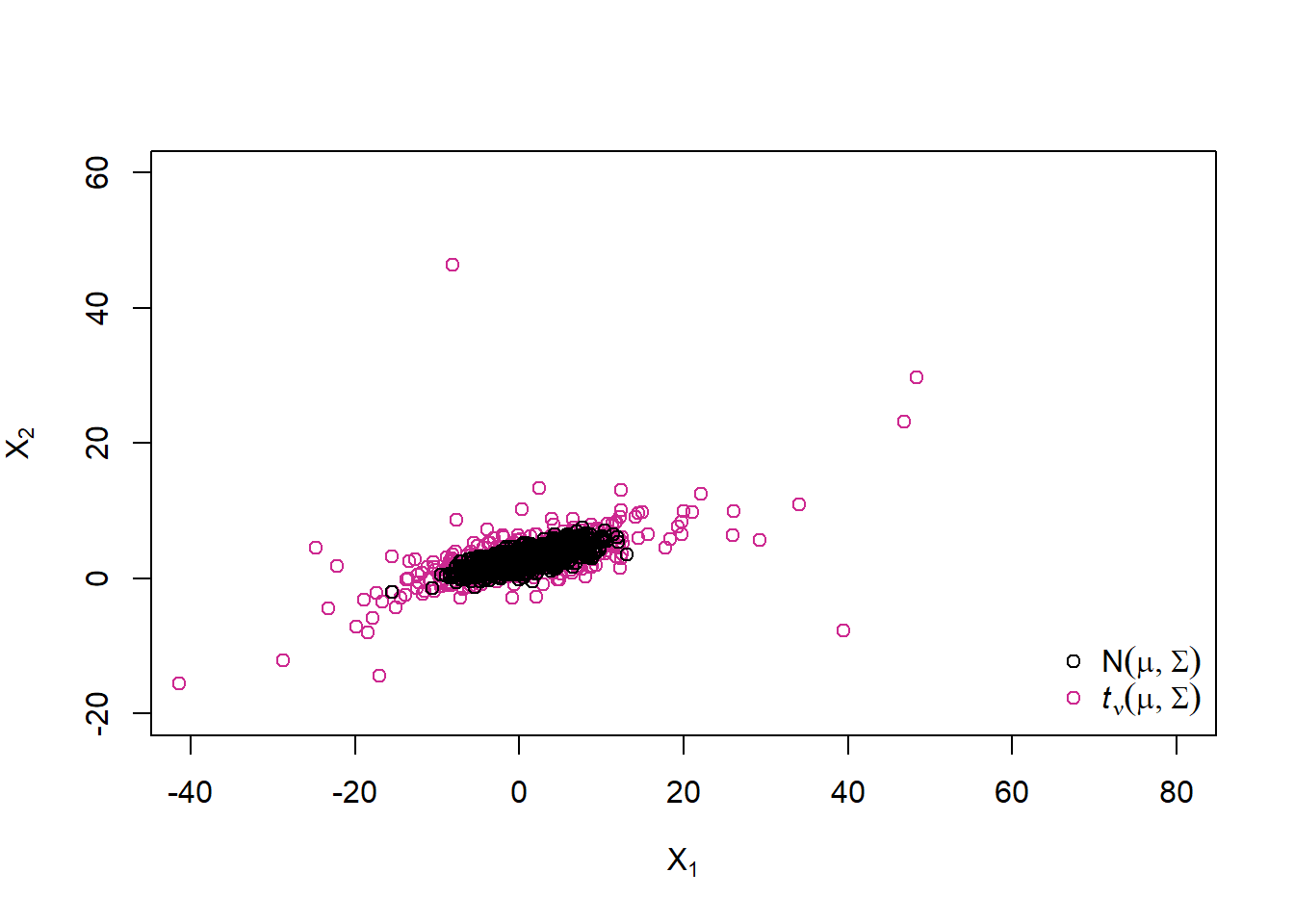

X.t = rep(mu, each = n) + sqrt(W) * t(A %*% t(Z))

xlim = c(-40, 80)

ylim = c(-20, 60)

plot(rbind(X.t, X.norm), xlim = xlim, ylim = ylim,

xlab = expression(X[1]), ylab = expression(X[2]),

col = rep(c("maroon3", "black"), each = n))

legend("bottomright", bty = "n", pch = c(1,1), col = c("black", "maroon3"),

legend = c(expression(N(mu,Sigma)),

expression(italic(t)[nu](mu,Sigma))))

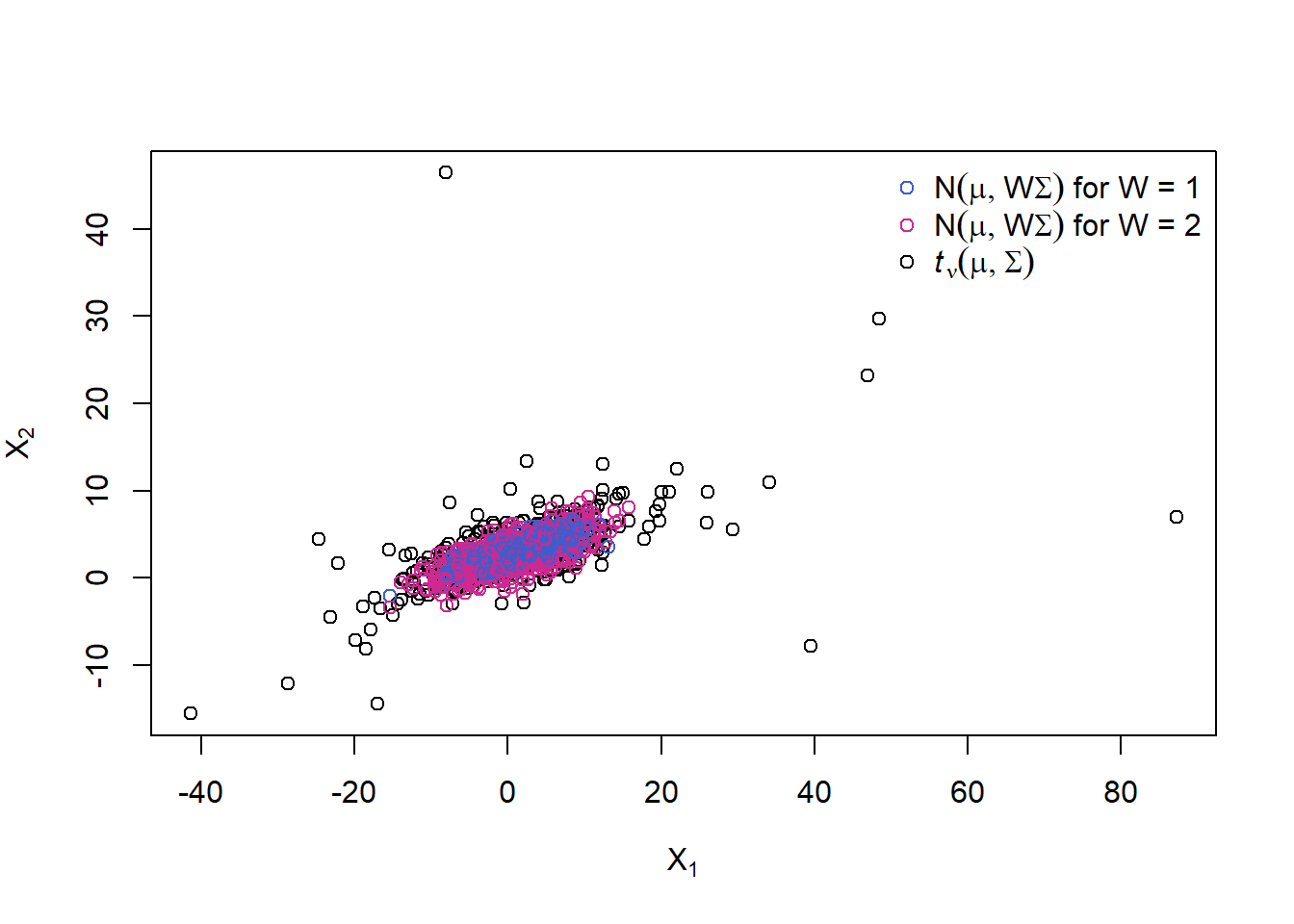

A 2-point distribution for \(W\) (= two ‘overlaid’ multiv. normals)

Let’s change the distribution of \(W\) to a 2-point distribution with \(W = 1\) with prob. \(0.5\) and \(W = 2\) with prob. \(0.5\). What we will see are two ‘overlaid’ normal distributions (as each of \(W = 1\) and \(W = 2\) corresponds to one).

W.binom = 1 + rbinom(n, size = 1, prob = 0.5)

cols = rep("royalblue3", n)

cols[W.binom == 2] = "maroon3"

X.W.binom = rep(mu, each = n) + sqrt(W.binom) * t(A %*% t(Z))

plot(rbind(X.t, X.W.binom), xlab = expression(X[1]), ylab = expression(X[2]),

col = c(rep("black", n), cols))

legend("topright", bty = "n", pch = rep(1, 3), col = c("royalblue3", "maroon3", "black"),

legend = c(expression(N(mu,W*Sigma)~"for W = 1"),

expression(N(mu,W*Sigma)~"for W = 2"),

expression(italic(t)[nu](mu,Sigma))))

With probability 0.5 we sample from a normal variance mixture with \(W = 1\) and with probability 0.5 we sample from one with \(W = 2\). By using a df for W with infinite upper endpoint, we can reach further out in the tails than with any multivariate normal distribution by overlaying normals with different (unbounded) covariance matrices (and this is what is creating heavier tails for the \(t\) distribution than the normal).

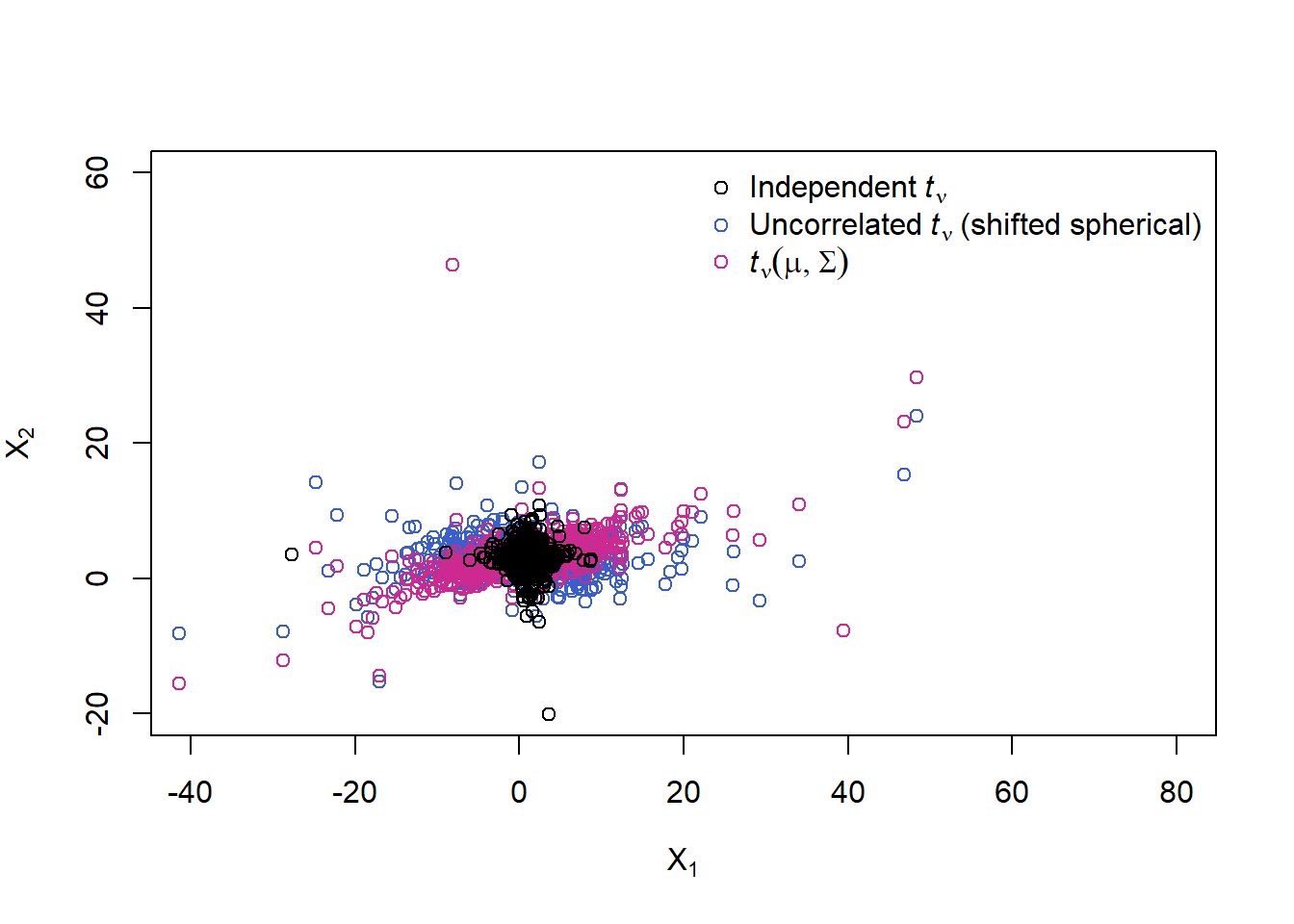

An uncorrelated multivariate \(t_\nu\) distribution vs an independent one

A. = diag(sqrt(diag(Sigma))) # Cholesky factor of the diagonal matrix containing the variances

X.t.uncor = rep(mu, each = n) + sqrt(W) * t(A. %*% t(Z)) # uncorrelated t samples

X.t.ind = rep(mu, each = n) + matrix(rt(n * d, df = nu), ncol = d) # independent t samples

plot(rbind(X.t.uncor, # uncorrelated t; dependence only introduced by sqrt(W) => shifted spherical distribution

X.t, # full t; dependence introduced by sqrt(W) *and* correlation

X.t.ind), # independence

xlim = xlim, ylim = ylim,

xlab = expression(X[1]), ylab = expression(X[2]),

col = rep(c("royalblue3", "maroon3", "black"), each = n))

legend("topright", bty = "n", pch = rep(1, 3), col = c("black", "royalblue3", "maroon3"),

legend = c(expression("Independent"~italic(t)[nu]),

expression("Uncorrelated"~italic(t)[nu]~"(shifted spherical)"),

expression(italic(t)[nu](mu,Sigma))))

The uncorrelated (but not independent) samples show more mass in the joint tails than the independent samples. The (neither uncorrelated nor independent) \(t\) samples show the most mass in the joint tails.

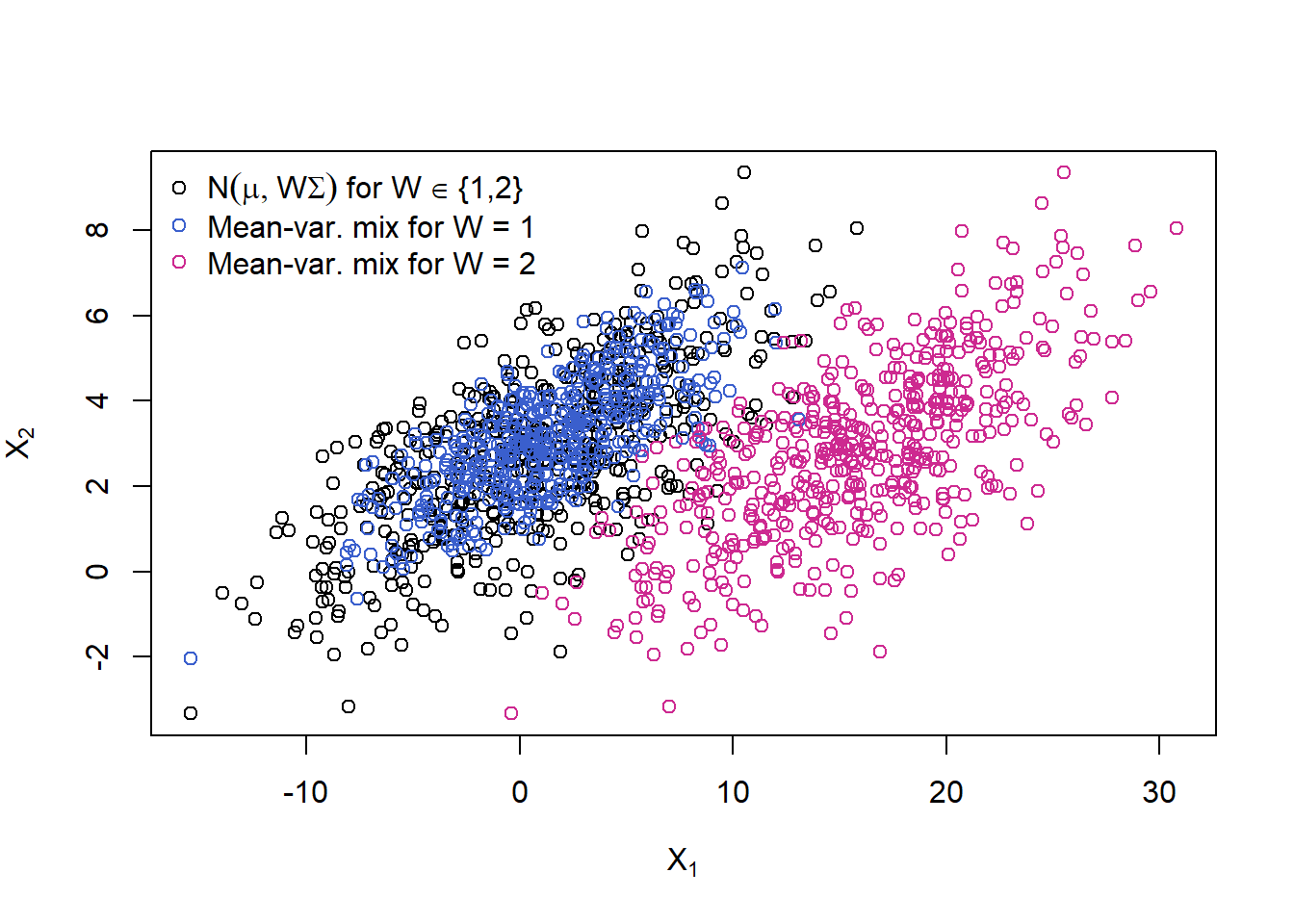

A normal mean-variance mixture

The models we now introduce attempt to add some asymmetry to the class of normal mixtures by mixing normal distributions with different means as well as different variances; this yields the class of multivariate normal mean–variance mixtures.

Definition 6.2 () The random vector \(\boldsymbol{X}\) is said to have a (multivariate) normal mean–variance mixture distribution if \[ \boldsymbol{X} \stackrel{d}{=} \boldsymbol{m}(W) + \sqrt{W}A \boldsymbol{Z}, \] where

\(\boldsymbol{Z} \sim \mathcal{N}_k(\boldsymbol{0}, I_k)\) ;

\(W \geq 0\) is a non-negative, scalar-valued rv that is independent of \(\boldsymbol{Z}\), and

\(A \in \mathbb{R}^{d \times k}\) is a matrix, and

\(\boldsymbol{m} : [0, \infty) \rightarrow \mathbb{R}^d\) is a measurable function.

In this case we have that \[ \boldsymbol{X} \mid W=w \sim \mathcal{N}_{d}(\boldsymbol{m}(w), w \Sigma) \] where \(\Sigma=A A^{\prime}\) and it is clear why such distributions are known as mean-variance mixtures of normals. In general, such distributions are not elliptical.

A possible concrete specification for the function \(\boldsymbol{m}(W)\) is \[ \boldsymbol{m}(W)=\boldsymbol{\mu}+W \boldsymbol{\gamma} \] where \(\boldsymbol{\mu}\) and \(\gamma\) are parameter vectors in \(\mathbb{R}^{d}\).

MFE (2015, Definition 6.11)\(\blacksquare\)

Now let’s also ‘mix’ the mean (replace \(\boldsymbol{\mu}\) by \(\boldsymbol{m}(W)\)), to get a normal mean-variance mixture; here: choosing between two different locations \(\boldsymbol{\mu}\) depending on \(W\).

mu. = t(sapply(W.binom, function(w) mu + if(w == 1) 0 else c(15, 0)))

X.mean.var = mu. + sqrt(W.binom) * t(A %*% t(Z))

plot(rbind(X.W.binom, X.mean.var), xlab = expression(X[1]), ylab = expression(X[2]),

col = c(rep("black", n), cols))

legend("topleft", bty = "n", pch = rep(1, 3), col = c("black", "royalblue3", "maroon3"),

legend = c(expression(N(mu,W*Sigma)~"for W"%in%"{1,2}"),

"Mean-var. mix for W = 1",

"Mean-var. mix for W = 2"))

Not only do the red points show more variation, they also have a different ocation; clearly, this sample (blue + red points together) is not elliptically distributed anymore.

6.2 Fitting a multivariate normal and \(t\)

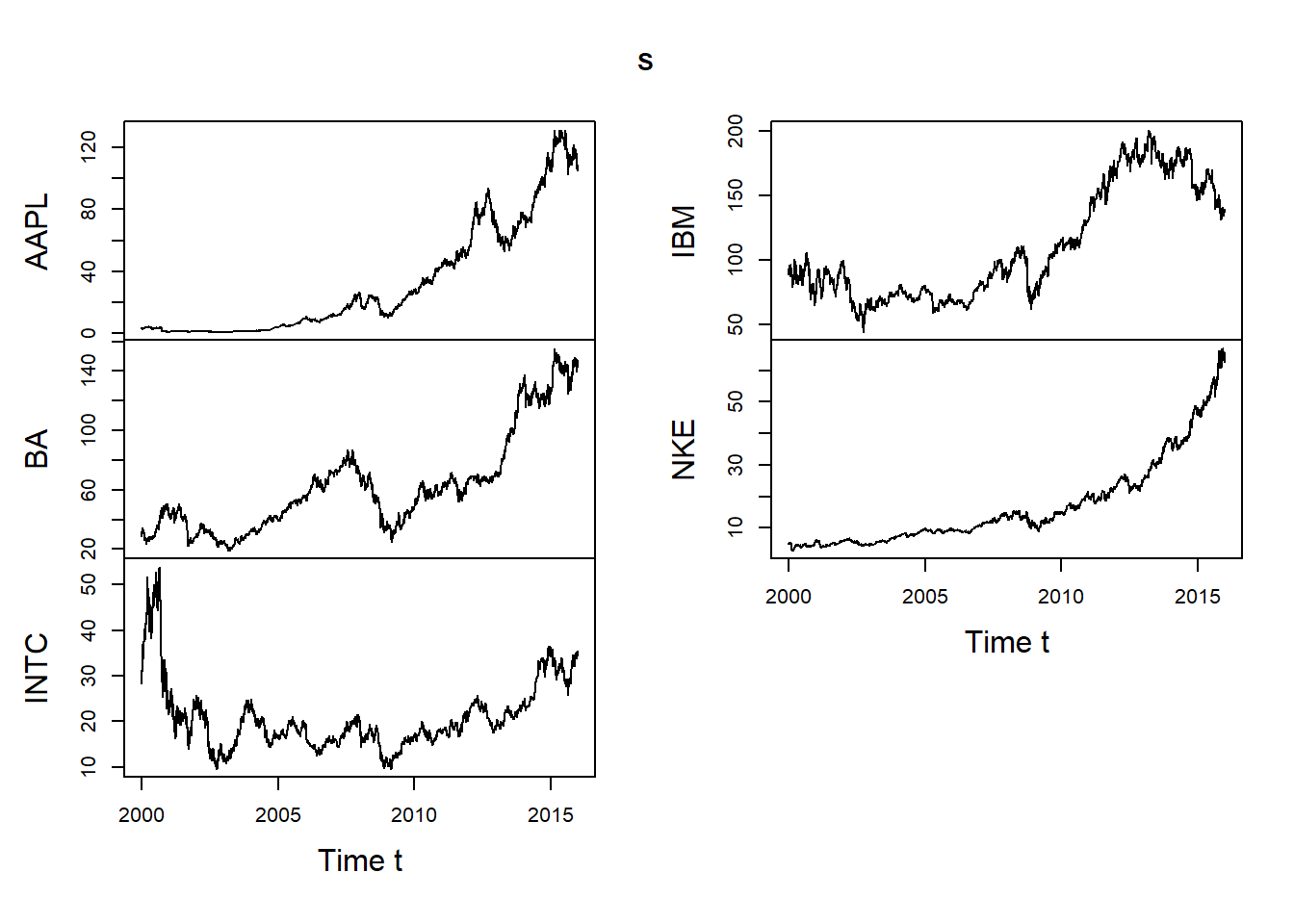

Fitting a multivariate normal and \(t\) distribution to negative log-returns of the five components of the Dow Jones index.

library(xts) # for time series manipulation

library(nvmix) # for rNorm(), fitStudent(), rStudent()

library(qrmdata) # for Dow Jones constituents data

library(qrmtools) # for returns()Load and extract the data we work with and plot:

data(DJ_const)

str(DJ_const)## An 'xts' object on 1962-01-02/2015-12-31 containing:

## Data: num [1:13595, 1:30] NA NA NA NA NA NA NA NA NA NA ...

## - attr(*, "dimnames")=List of 2

## ..$ : NULL

## ..$ : chr [1:30] "AAPL" "AXP" "BA" "CAT" ...

## Indexed by objects of class: [Date] TZ: UTC

## xts Attributes:

## List of 2

## $ src : chr "yahoo"

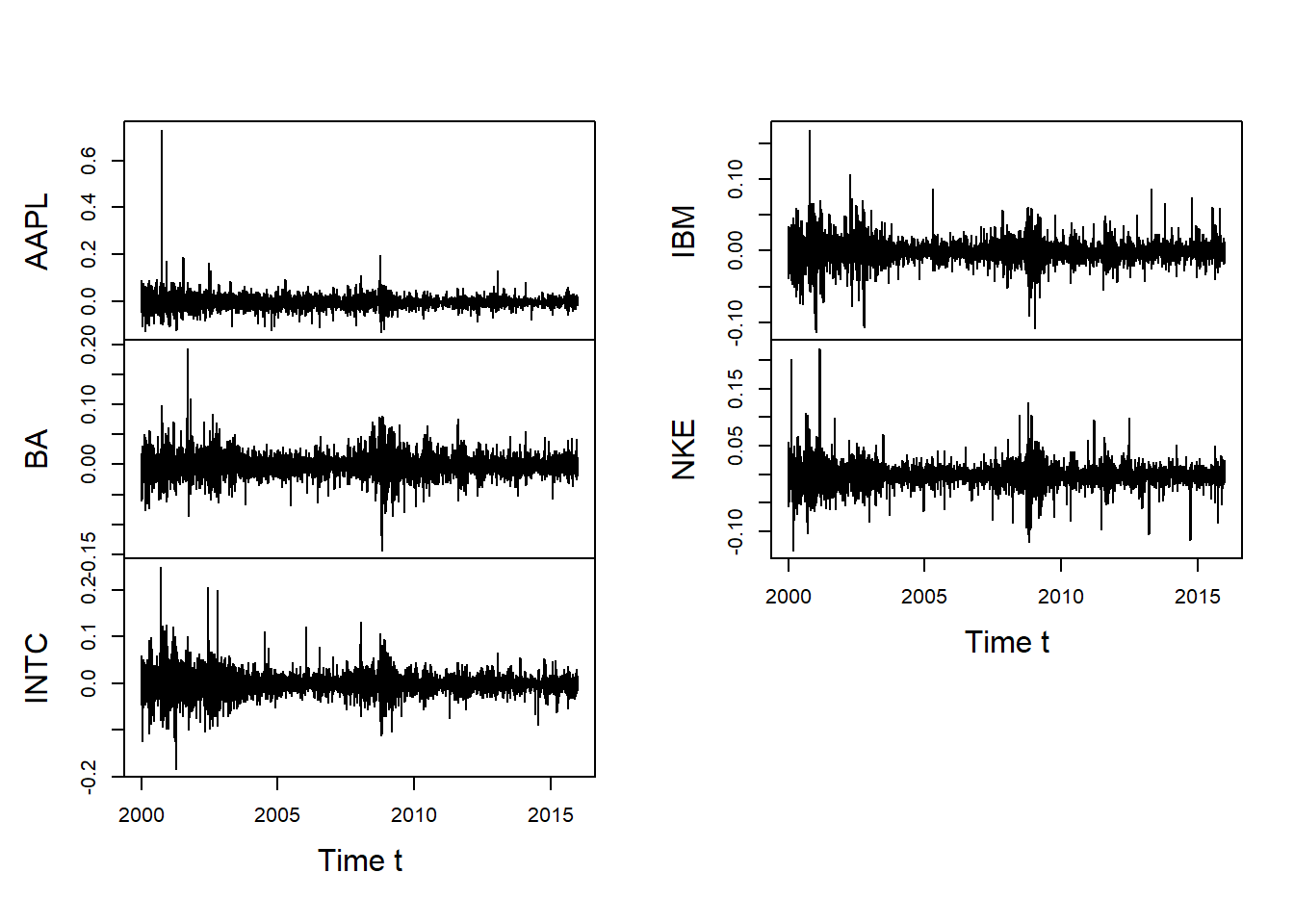

## $ updated: POSIXct[1:1], format: "2016-01-03 03:51:40"S = DJ_const['2000-01-01/', c("AAPL", "BA", "INTC", "IBM", "NKE")]

## => We work with Apple, Boeing, Intel, IBM, Nike since 2000-01-01 here

plot.zoo(S, xlab = "Time t")

Build and plot \(-\)log-returns:

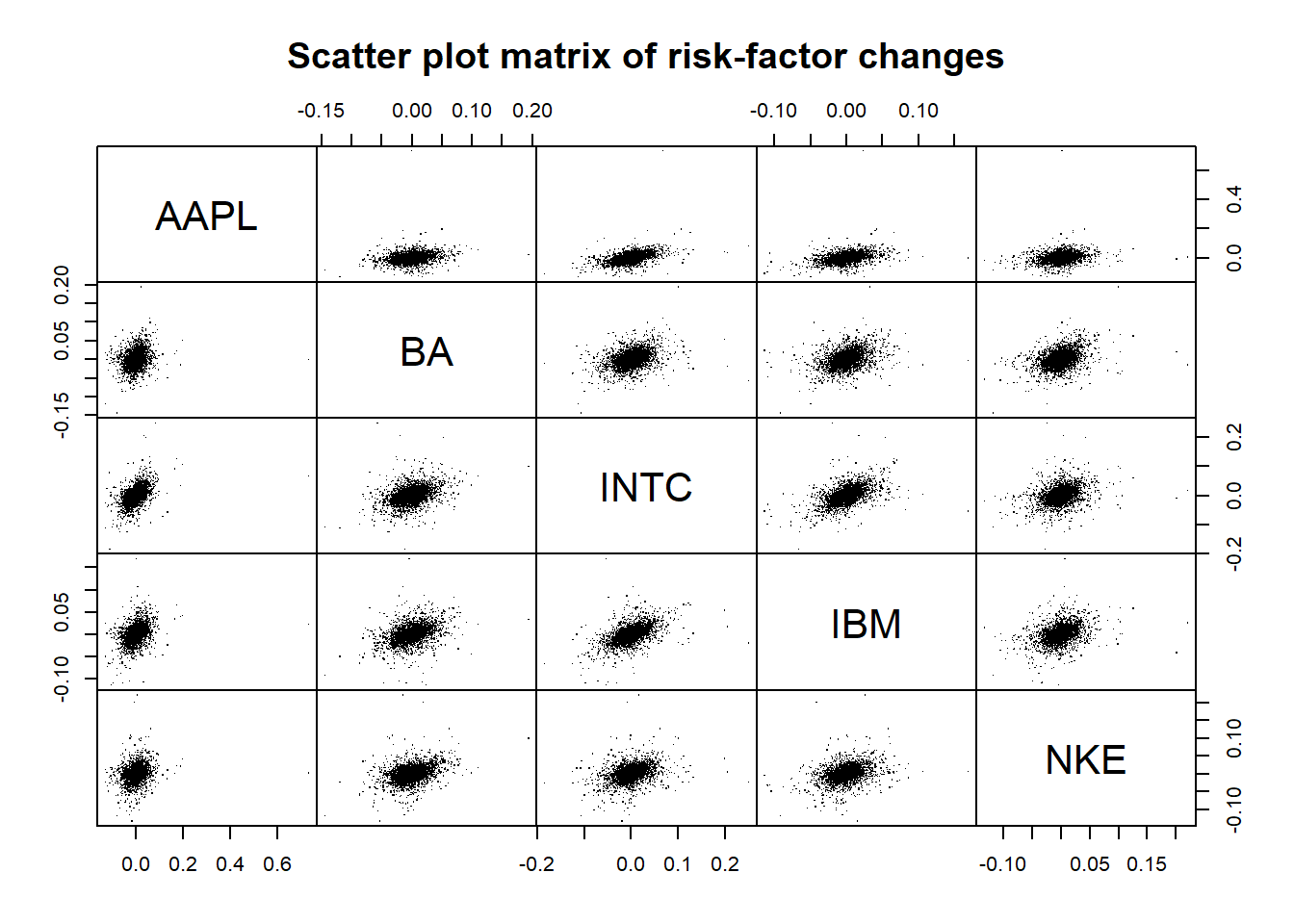

X = -returns(S) # compute -log-returns

pairs(as.matrix(X), main = "Scatter plot matrix of risk-factor changes", gap = 0, pch = ".")

plot.zoo(X, xlab = "Time t", main = "")

## For illustration purposes, we treat this data as realizations of iid

## five-dimensional random vectors.Fitting a multivariate normal distribution to \(\boldsymbol{X}\) and simulating from it:

mu = colMeans(X) # estimated location vector

Sigma = cov(X) # estimated scale matrix

stopifnot(all.equal(Sigma, var(X)))

P = cor(X) # estimated correlation matrix

stopifnot(all.equal(P, cov2cor(Sigma)))

n = nrow(X) # sample size

set.seed(271)

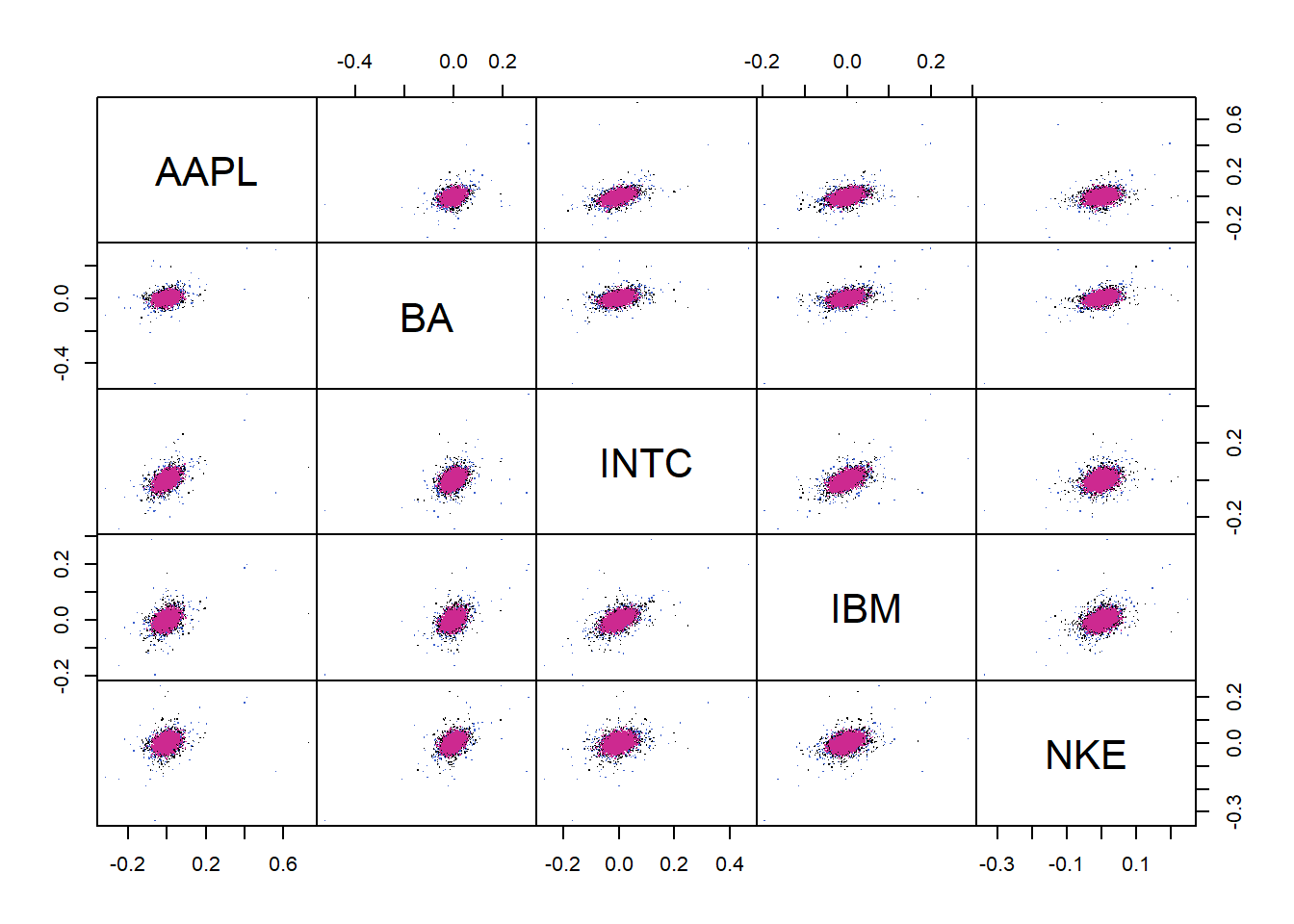

X.norm = rNorm(n, loc = mu, scale = Sigma) # N(mu, Sigma) samplesFitting a multivariate \(t\) distribution to \(\boldsymbol{X}\):

fit = fitStudent(X) # fit a multivariate t distribution

X.t = rStudent(n, df = fit$df, loc = fit$loc, scale = fit$scale) # t_nu samplesPlot (sample from fitted \(t\) (red), original sample (black), sample from fitted normal (blue)):

dat = rbind(t = X.t, original = as.matrix(X), norm = X.norm)

cols = rep(c("royalblue3", "black", "maroon3"), each = n)

pairs(dat, gap = 0, pch = ".", col = cols)

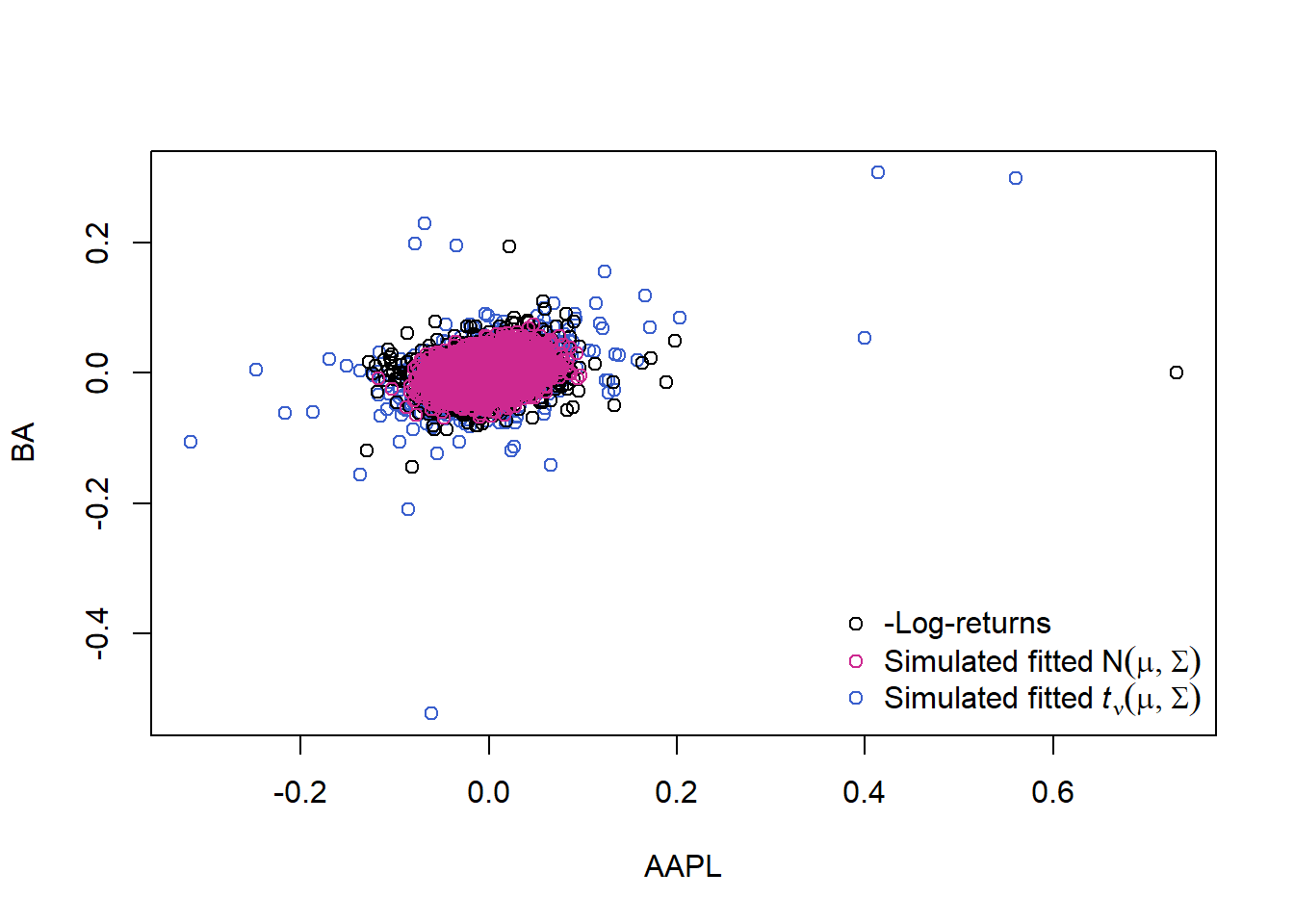

Pick out one pair (to better see that multivariate \(t\) fits better):

plot(dat[,1:2], col = cols) # => the multivariate normal generates too few extreme losses!

legend("bottomright", bty = "n", pch = rep(1, 3), col = c("black", "maroon3", "royalblue3"),

legend = c("-Log-returns", expression("Simulated fitted"~N(mu,Sigma)),

expression("Simulated fitted"~italic(t)[nu](mu,Sigma))))

6.3 Testing multivariate normality

library(qrmtools)

library(nvmix) # for rNorm() and rStudent()

library(moments) # for jarque.test()

library(xts) # for time-series related functions6.3.1 Generate data

n = 1000 # sample size

d = 3 # dimension

mu = 1:d # location vector

sd = sqrt(1:d) # standard deviations for scale matrix

tau = 0.5 # (homogeneous) Kendall's tau

rho = sin(tau * pi/2) # (homogeneous) correlation coefficient

Sigma = matrix(rho, nrow = d, ncol = d) # scale matrix

diag(Sigma) = rep(1, d) # => now Sigma is a correlation matrix

Sigma = Sigma * (sd %*% t(sd)) # covariance matrix

nu = 3 # degrees of freedom

set.seed(271) # set seed (for reproducibility)

X.N = rNorm(n, loc = mu, scale = Sigma) # sample from N(mu, Sigma)

X.t = rStudent(n, df = nu, loc = mu, scale = ((nu-2)/nu) * Sigma) # sample from t_d(nu, mu, ((nu-2)/nu) * Sigma) (same covariance as N(mu, Sigma))

X.t.N = sapply(1:d, function(j) qnorm(rank(X.t[,j]) / (nrow(X.t) + 1),

mean = mu[j], sd = sqrt(Sigma[j, j]))) # t dependence with normal margins; see Chapter 7

if(FALSE) {

cov(X.N)

cov(X.t)

## => quite apart, but closer for larger n

}6.3.2 Testing for \(\mathcal{N}(\boldsymbol{\mu}, \Sigma)\)

We treat \(\boldsymbol{\mu}\) and \(\Sigma\) as unknown and estimate them:

mu.N = mean(X.N)

mu.t = mean(X.t)

Sig.N = cov(X.N)

Sig.t = cov(X.t)6.3.3 For \(\mathcal{N}(\boldsymbol{\mu}, \Sigma)\) data

Formal tests

## Univariate normality

stopifnot(apply(X.N, 2, function(x) shapiro.test(x)$p.value) > 0.05) # Shapiro--Wilk

stopifnot(apply(X.N, 2, function(x) jarque.test(x) $p.value) > 0.05) # Jarque--Bera

## Note: Careful with 'multiple testing'## Joint normality

ADmaha2 = maha2_test(X.N) # Anderson--Darling test of squared Mahalanobis distances being chi_d^2

mardiaK = mardia_test(X.N) # Mardia's kurtosis test of joint normality based on squared Mahalanobis distances

mardiaS = mardia_test(X.N, type = "skewness") # Mardia's skewness test of joint normality based on Mahalanobis angles

stopifnot(mardiaS$p.value > 0.05, mardiaK$p.value > 0.05, ADmaha2$p.value > 0.05)Graphical tests

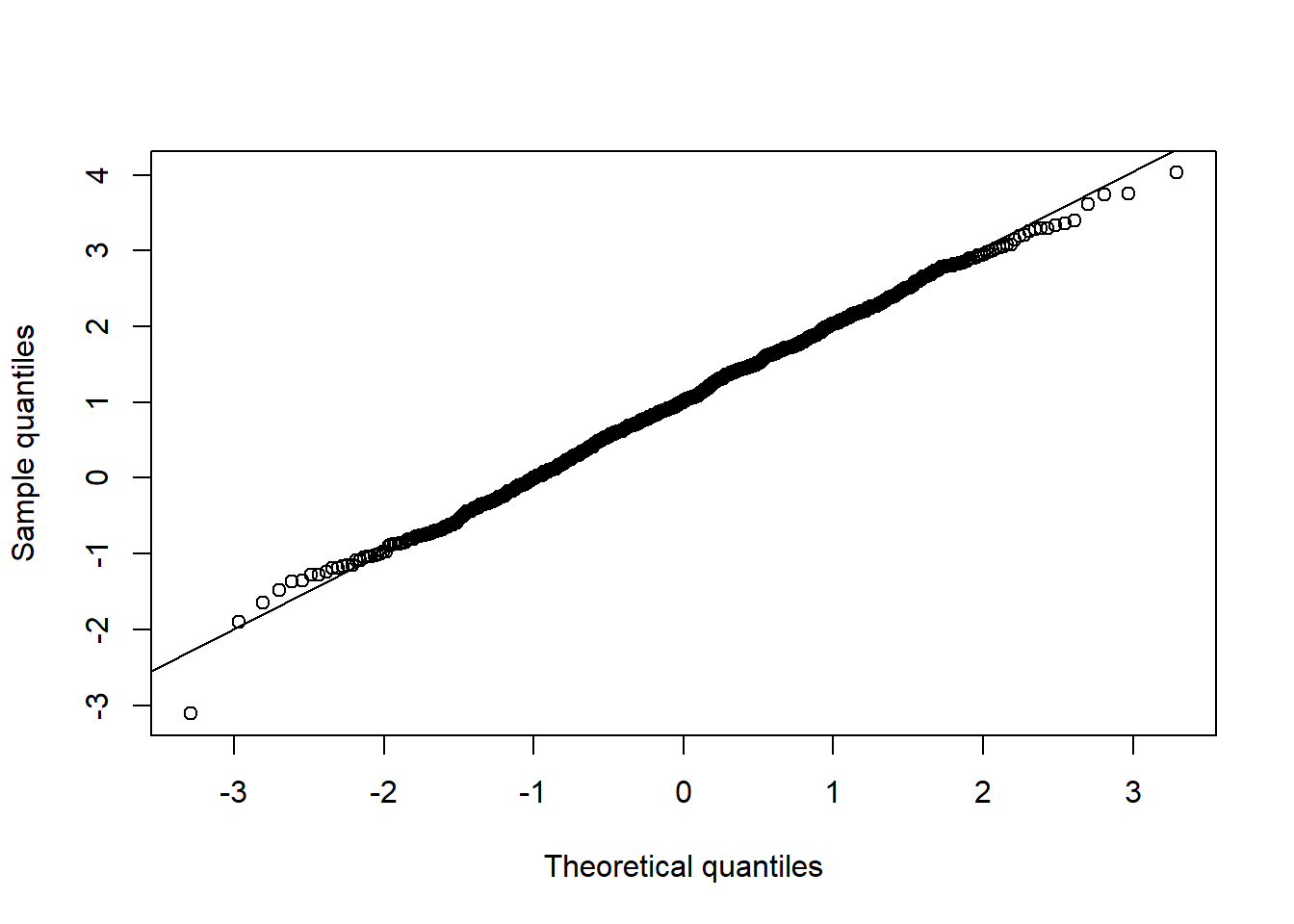

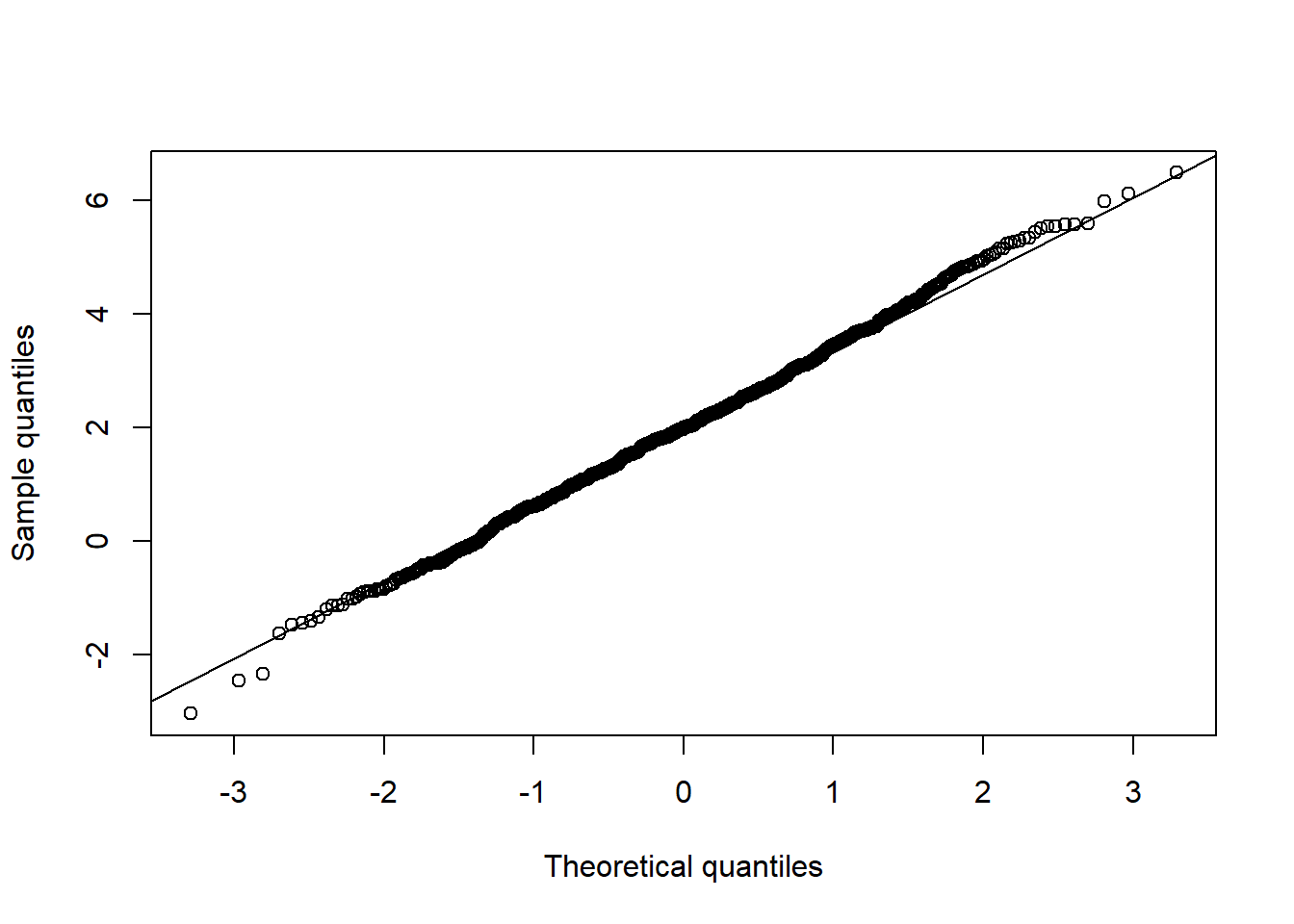

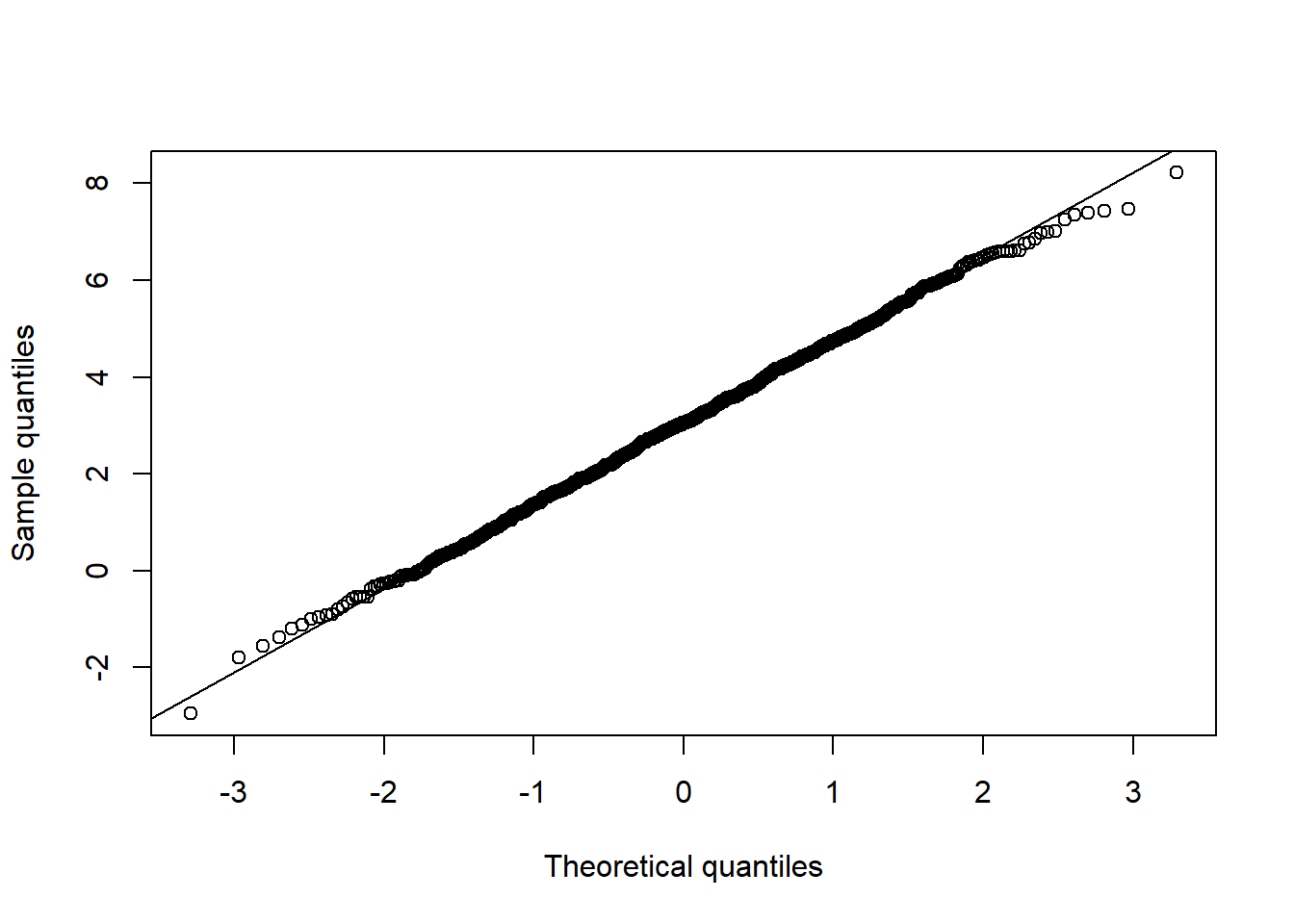

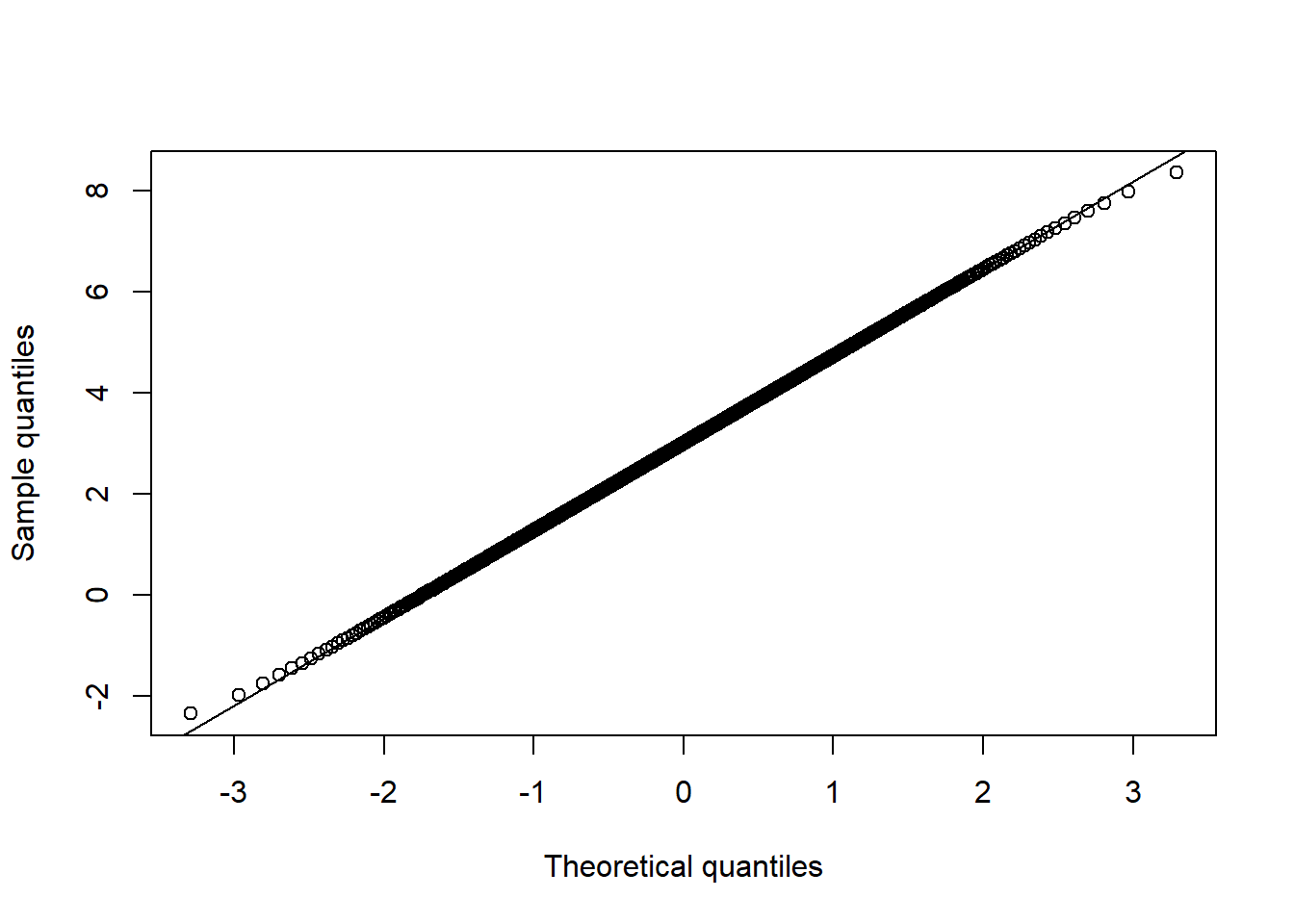

## Univariate normality

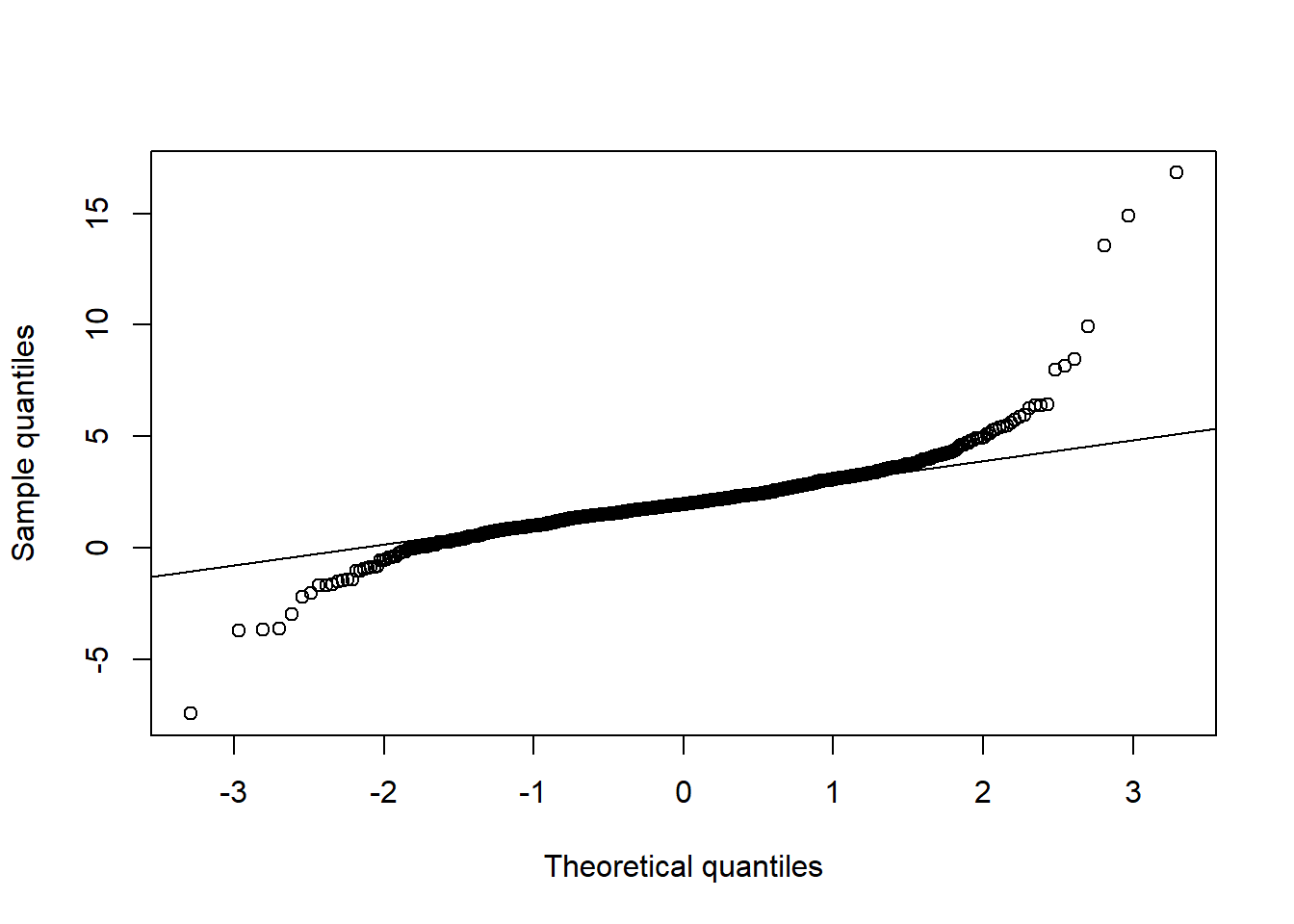

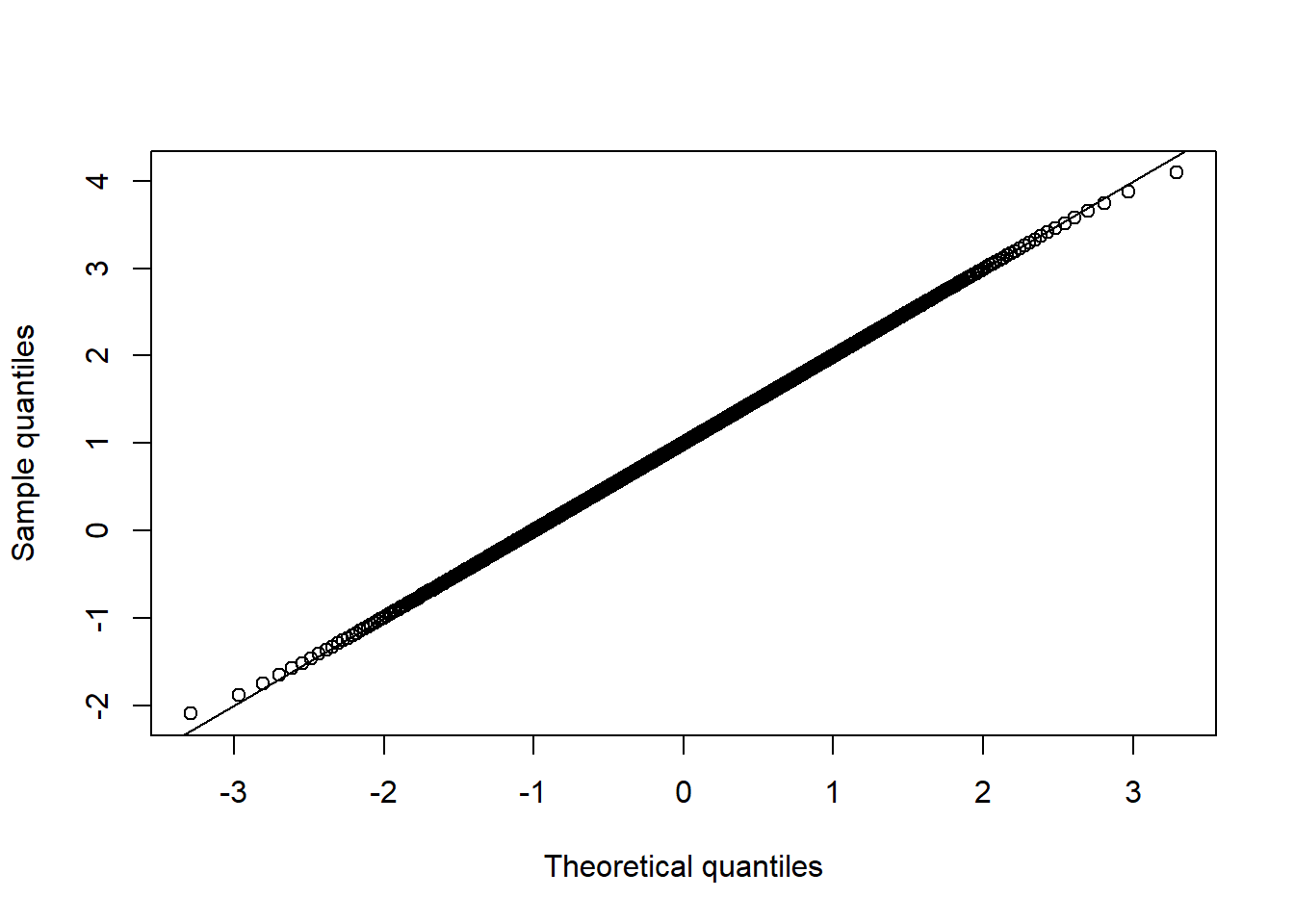

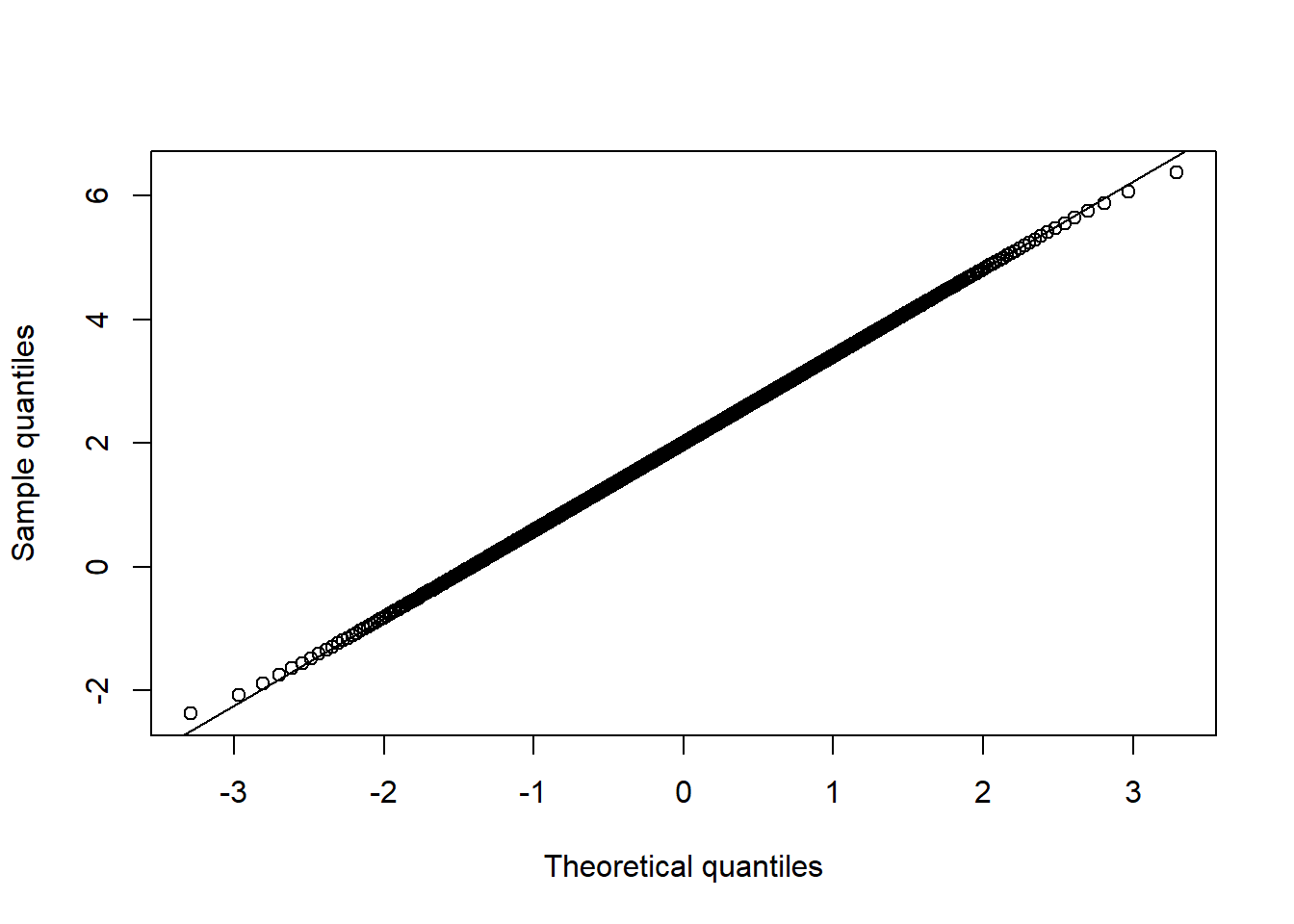

qq_plot(X.N[,1], FUN = qnorm, method = "empirical") # margin 1

qq_plot(X.N[,2], FUN = qnorm, method = "empirical") # margin 2

qq_plot(X.N[,3], FUN = qnorm, method = "empirical") # margin 3

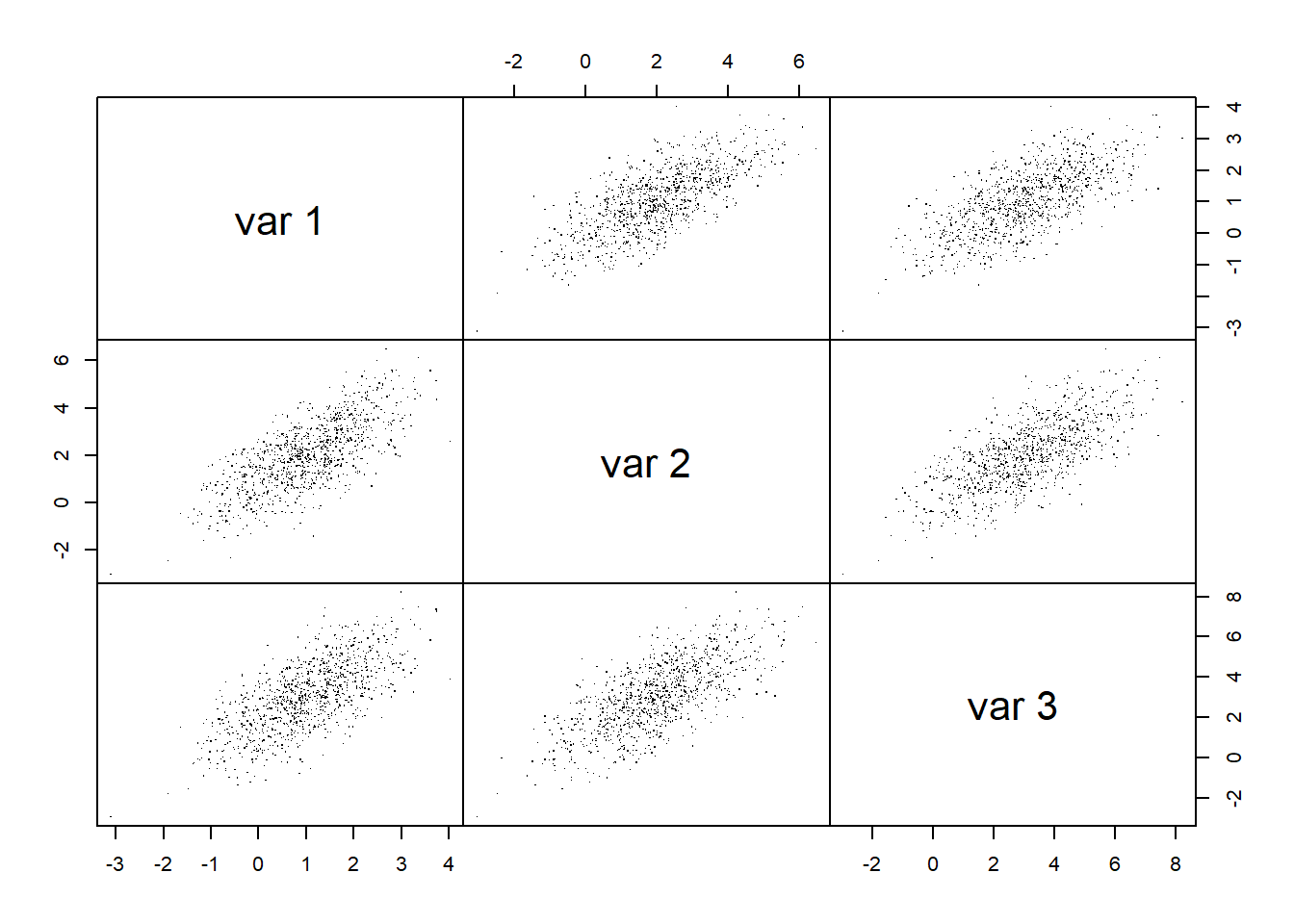

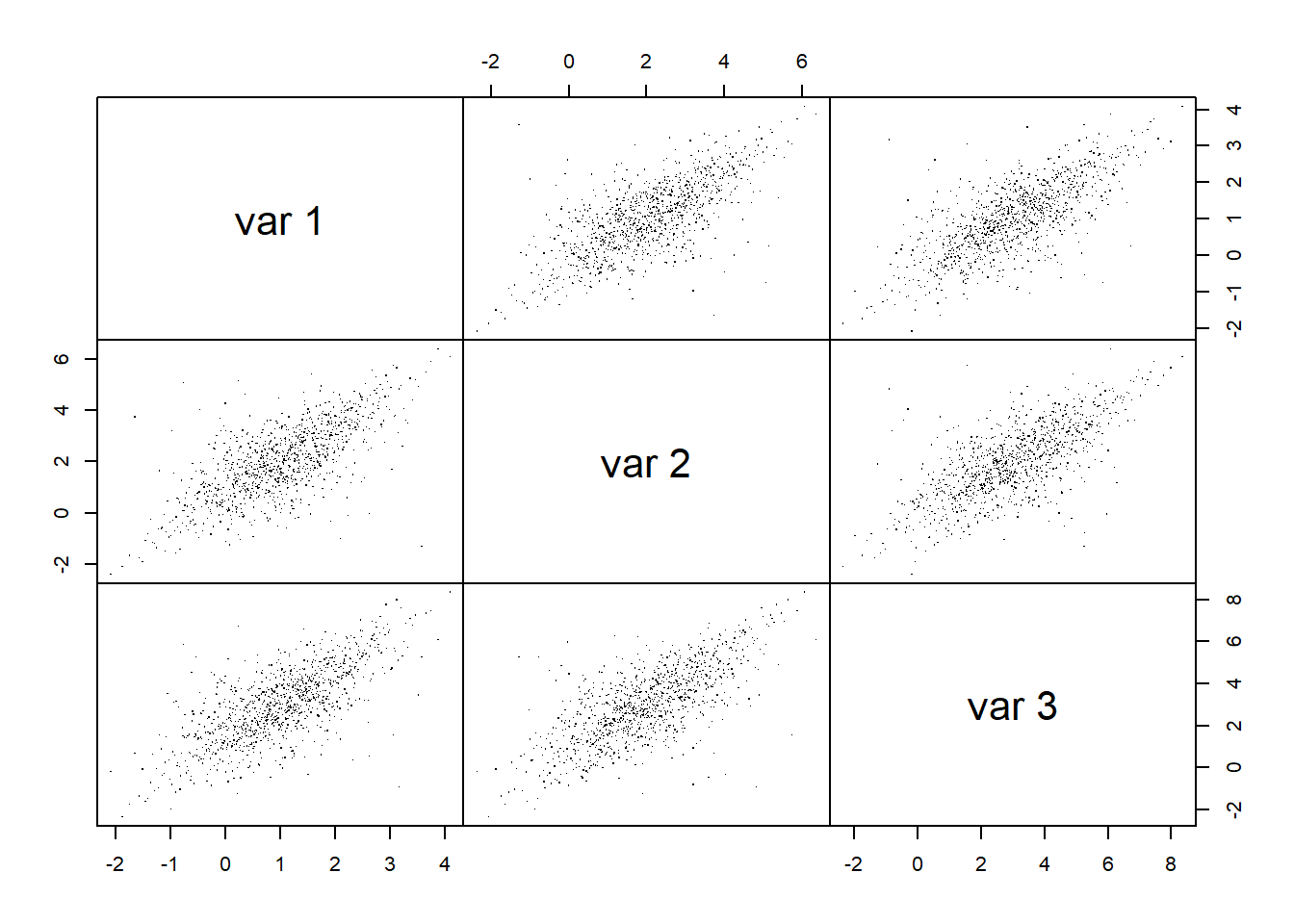

## Joint normality

pairs(X.N, gap = 0, pch = ".") # visual assessment

D2.d = mahalanobis(X.N, center = colMeans(X.N), cov = cov(X.N)) # squared Mahalanobis distances

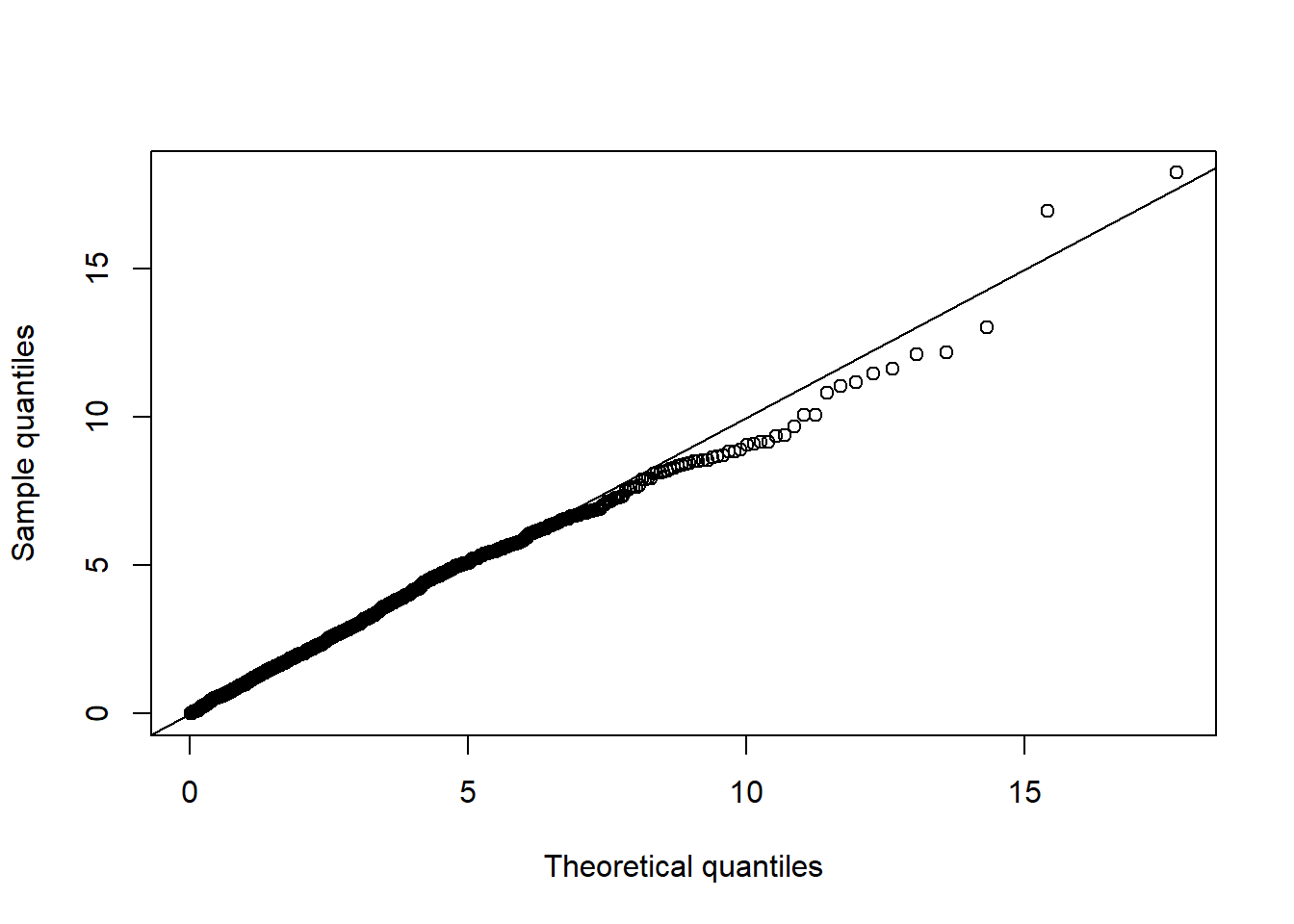

qq_plot(D2.d, FUN = function(p) qchisq(p, df = d)) # => no significant departure visible

6.3.4 For \(t_d(\nu, \boldsymbol{\mu}, \Sigma)\) data

Formal tests

## Univariate normality

stopifnot(apply(X.t, 2, function(x) shapiro.test(x)$p.value) <= 0.05) # Shapiro--Wilk

stopifnot(apply(X.t, 2, function(x) jarque.test(x) $p.value) <= 0.05) # Jarque--Bera

## Note: Careful with 'multiple testing'## Joint normality

ADmaha2 = maha2_test(X.t) # Anderson--Darling test of squared Mahalanobis distances being chi_d^2

mardiaK = mardia_test(X.t) # Mardia's kurtosis test of joint normality based on squared Mahalanobis distances

mardiaS = mardia_test(X.t, type = "skewness") # Mardia's skewness test of joint normality based on Mahalanobis angles

stopifnot(mardiaS$p.value <= 0.05, mardiaK$p.value <= 0.05, ADmaha2$p.value <= 0.05)Graphical tests

## Univariate normality

qq_plot(X.t[,1], FUN = qnorm, method = "empirical") # margin 1

qq_plot(X.t[,2], FUN = qnorm, method = "empirical") # margin 2

qq_plot(X.t[,3], FUN = qnorm, method = "empirical") # margin 3

## Joint normality

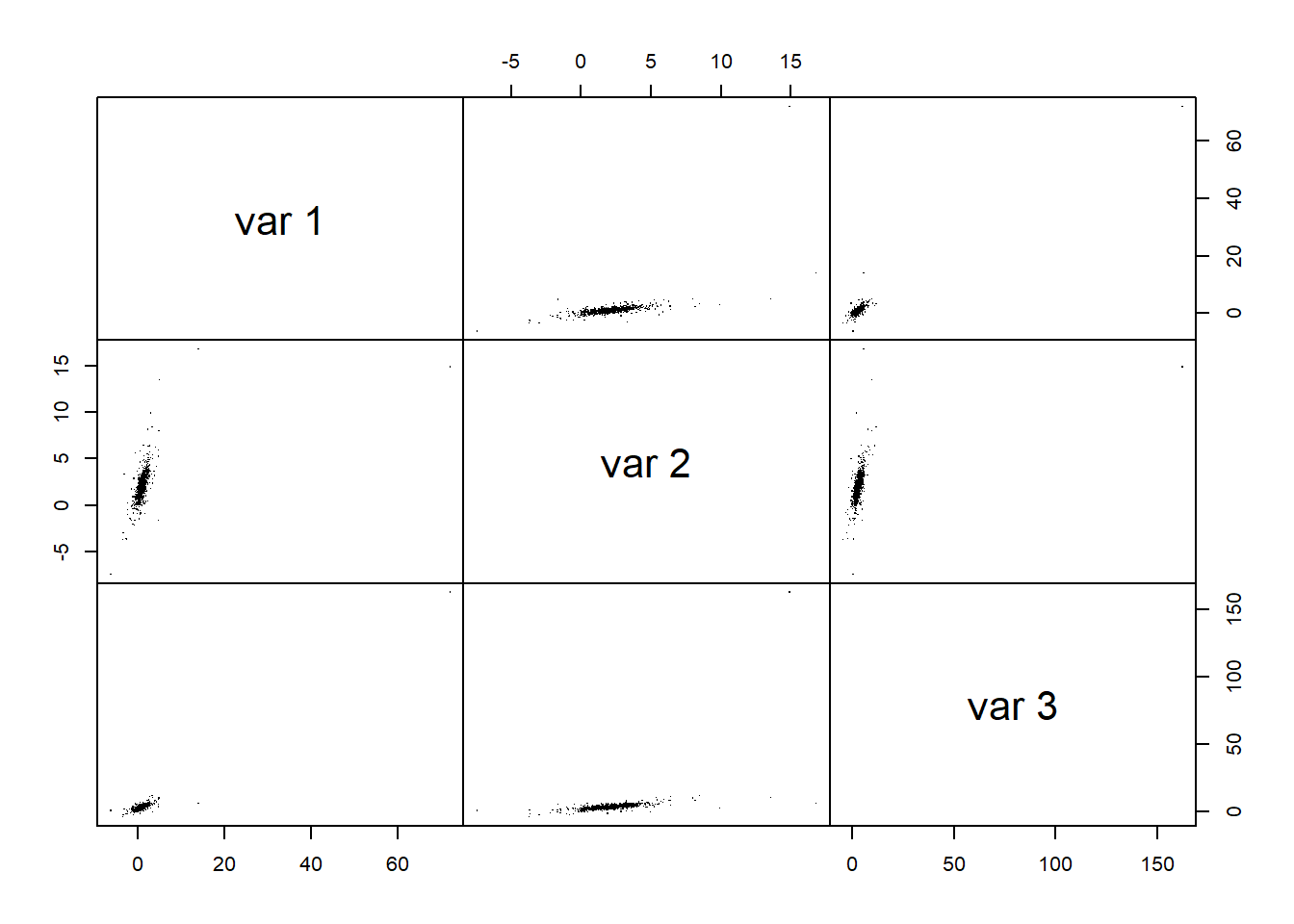

pairs(X.t, gap = 0, pch = ".") # visual assessment

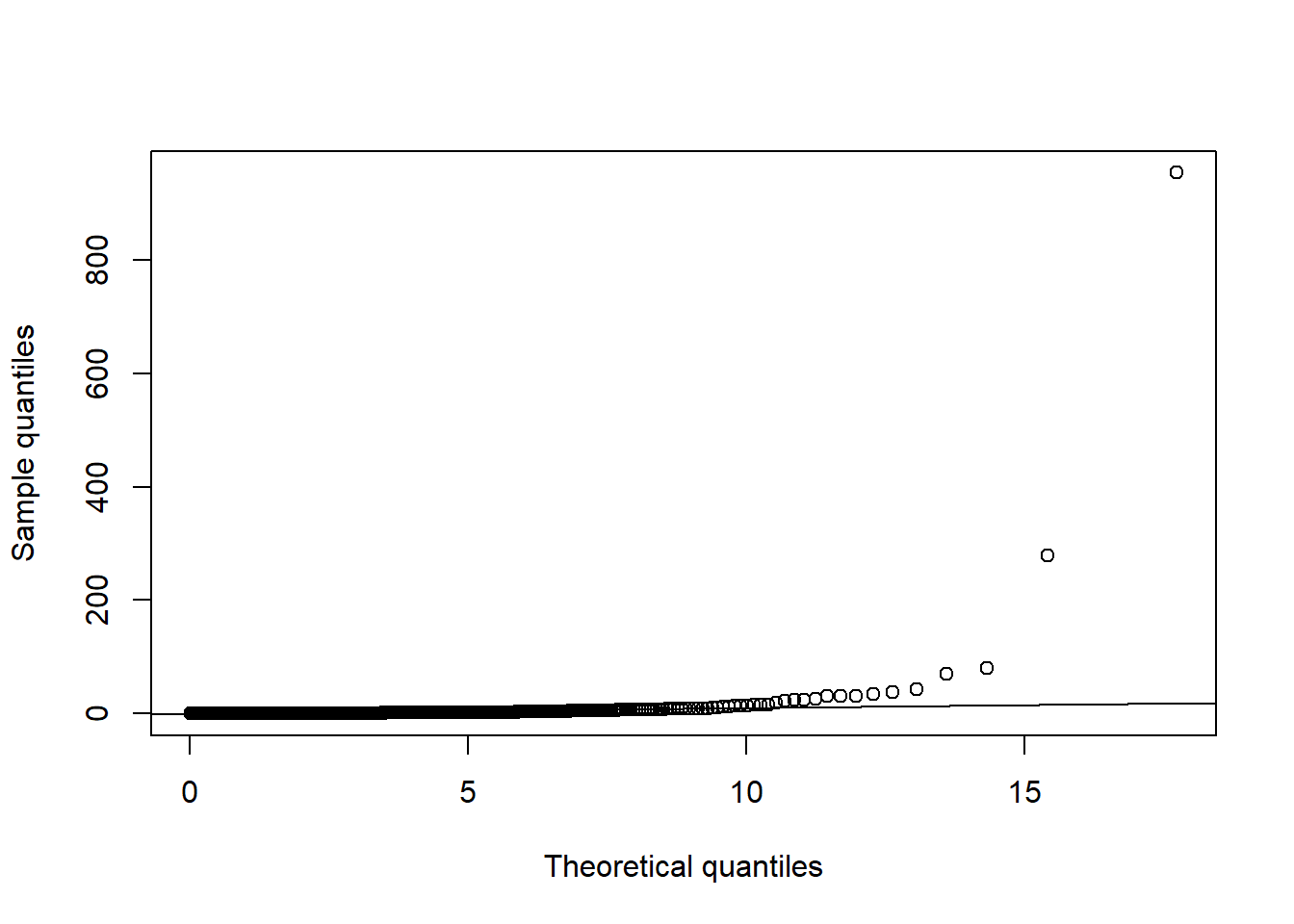

D2.d = mahalanobis(X.t, center = colMeans(X.t), cov = cov(X.t)) # squared Mahalanobis distances

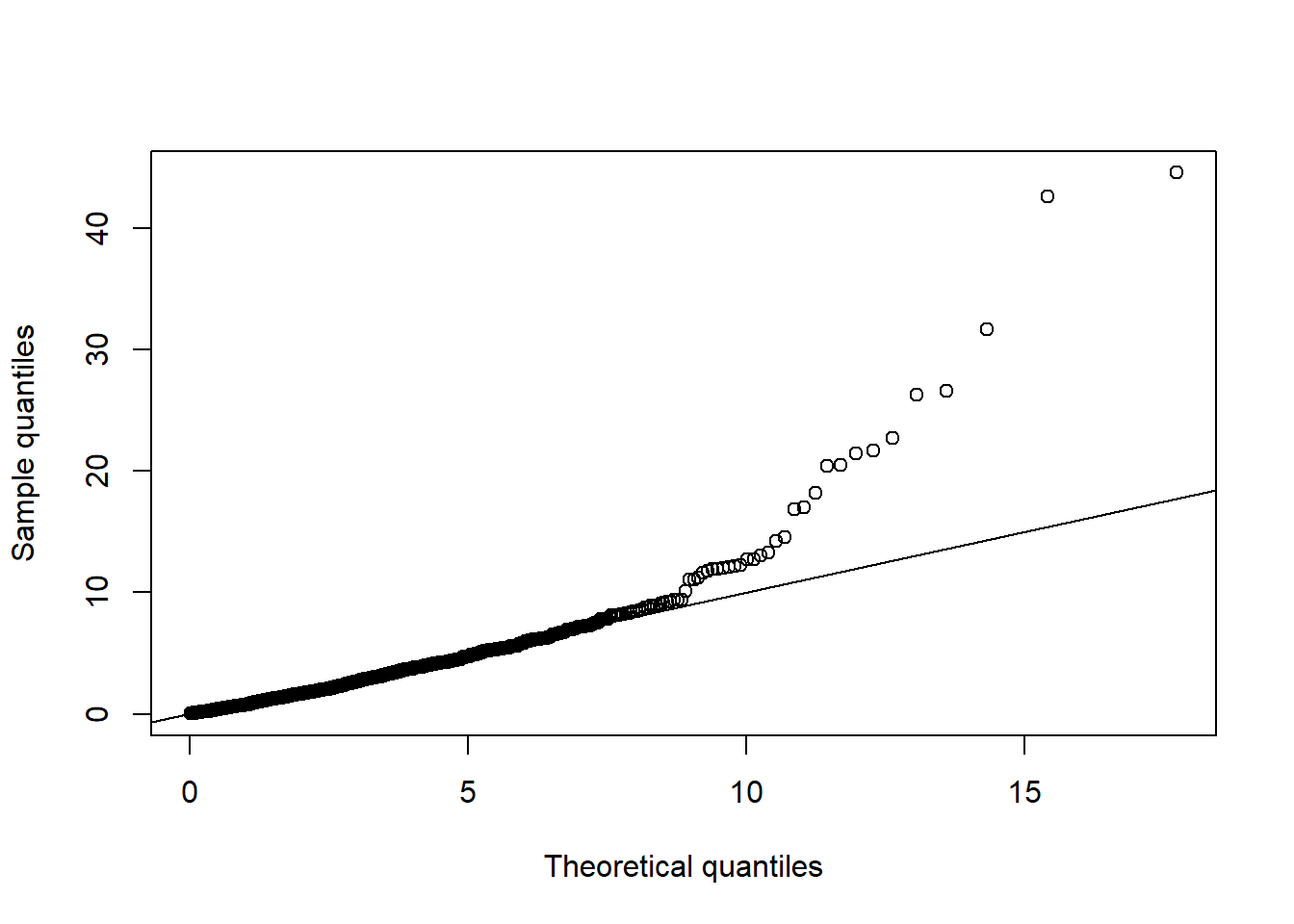

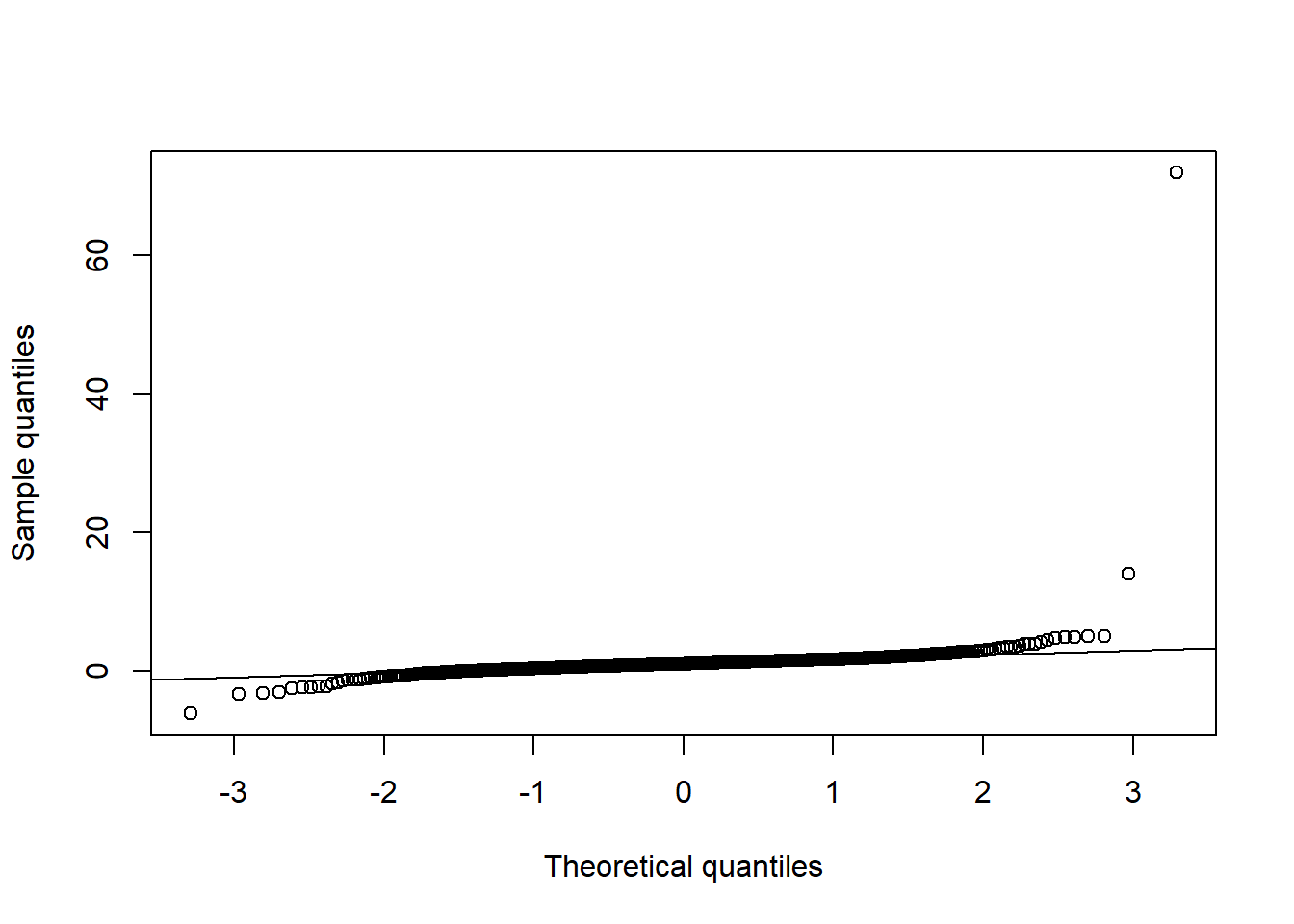

qq_plot(D2.d, FUN = function(p) qchisq(p, df = d)) # => departure clearly visible

6.3.5 For \(t_d(\nu, 0, P)\) dependence but \(\mathcal{N}(0, 1)\) margins

Formal tests

## Univariate normality

stopifnot(apply(X.t.N, 2, function(x) shapiro.test(x)$p.value) > 0.05) # Shapiro--Wilk

stopifnot(apply(X.t.N, 2, function(x) jarque.test(x) $p.value) > 0.05) # Jarque--Bera## Joint normality

ADmaha2 = maha2_test(X.t.N) # Anderson--Darling test of squared Mahalanobis distances being chi_d^2

mardiaK = mardia_test(X.t.N) # Mardia's kurtosis test of joint normality based on squared Mahalanobis distances

mardiaS = mardia_test(X.t.N, type = "skewness") # Mardia's skewness test of joint normality based on Mahalanobis angles

stopifnot(mardiaS$p.value <= 0.05, mardiaK$p.value <= 0.05, ADmaha2$p.value <= 0.05)Graphical tests

## Univariate normality

qq_plot(X.t.N[,1], FUN = qnorm, method = "empirical") # margin 1

qq_plot(X.t.N[,2], FUN = qnorm, method = "empirical") # margin 2

qq_plot(X.t.N[,3], FUN = qnorm, method = "empirical") # margin 3

## Joint normality

pairs(X.t.N, gap = 0, pch = ".") # visual assessment

D2.d = mahalanobis(X.t.N, center = colMeans(X.t.N), cov = cov(X.t.N)) # squared Mahalanobis distances

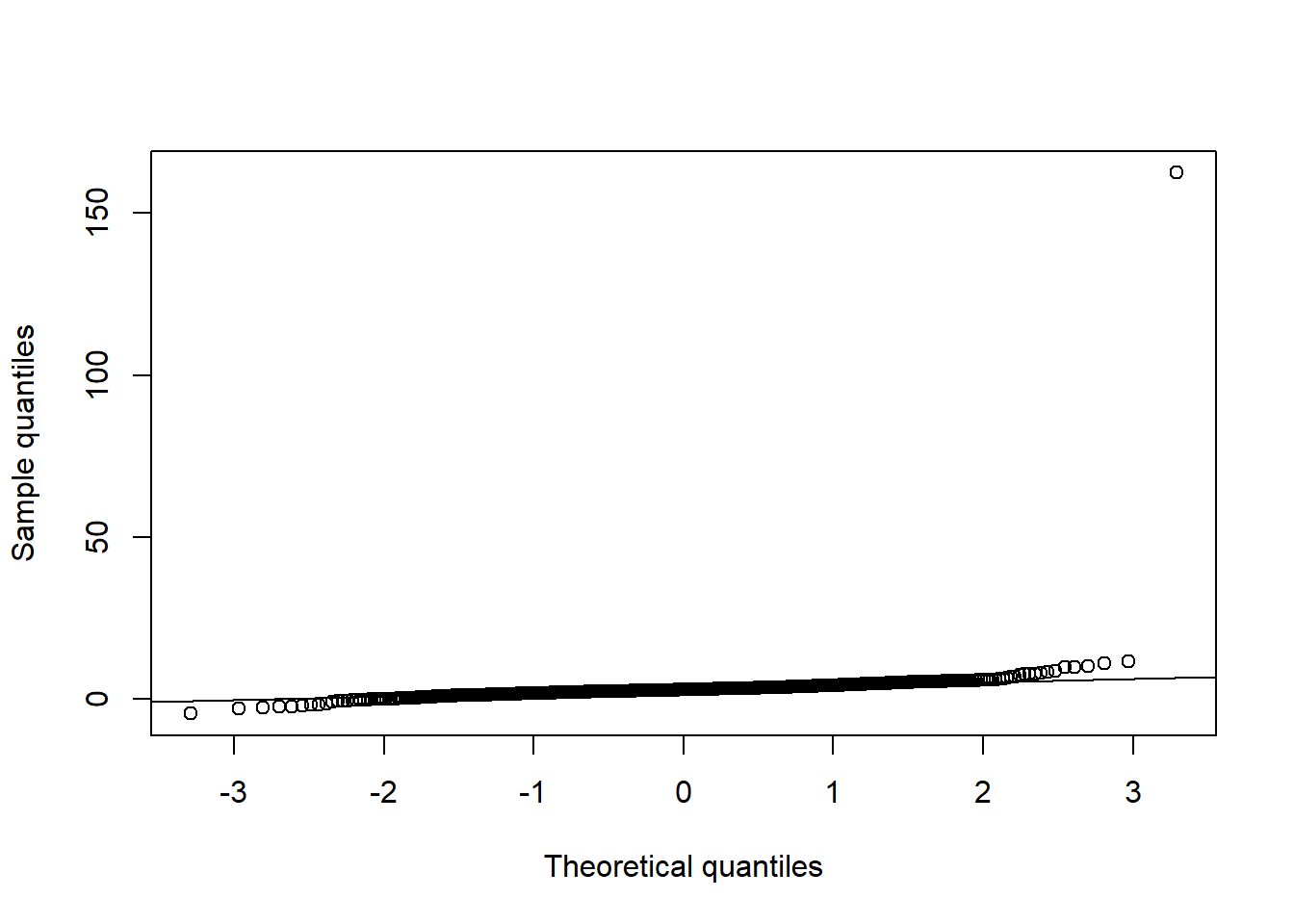

qq_plot(D2.d, FUN = function(p) qchisq(p, df = d)) # => departure clearly visible