6 Additional Models

This final chapter will cover additional models from the remaining chapters we have not covered in Introduction to Time Series Analysis and Forecasting as well as notable models from Forecasting: Principles and Practice past Chapter 9: ARIMA Models. Many of these models are either variants or extensions of ARIMA models covered in chapter 5 or are more recently developed models designed to handle very high frequency data (daily, sub-daily).

6.1 Chapter 6 Code

Chapter 6 contains material on intervention models and transfer function noise models. These models are in the same class as ARIMA models, but introduce other inputs that reflect changes in the process.40

6.1.1 Example 6.5 Intervention Model for Weekly Cereal Sales Data

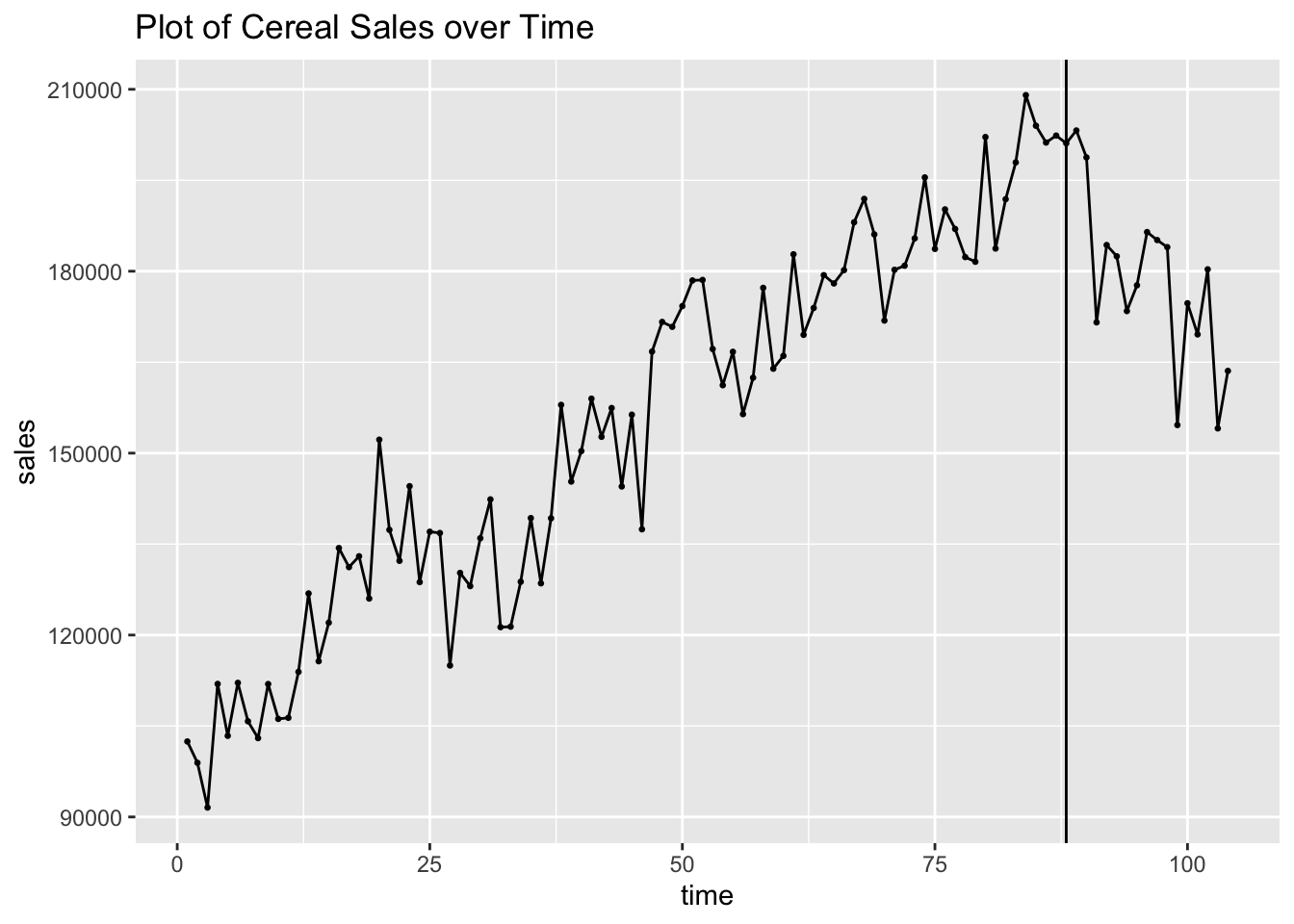

For the examples on intervention models we will use weekly cereal sales data from CerealSales.csv. First, I read in cereal sales data, rename the variables, and declare it as a tsibble. The time variable does not need to be modified to be used as an index, as time is kept periodically. In this data, at week 88 a rival company introduces a similar product into the market.

(cereal <- read_csv("data/CerealSales.csv") |>

rename(time = 1, sales = 2) |>

as_tsibble(index = time))## Rows: 104 Columns: 2

## ── Column specification ───────────────────────────────────────

## Delimiter: ","

## dbl (2): Week, Sales

##

## ℹ Use `spec()` to retrieve the full column specification for this data.

## ℹ Specify the column types or set `show_col_types = FALSE` to quiet this message.## # A tsibble: 104 x 2 [1]

## time sales

## <dbl> <dbl>

## 1 1 102450

## 2 2 98930

## 3 3 91550

## 4 4 111940

## 5 5 103380

## 6 6 112120

## 7 7 105780

## 8 8 103000

## 9 9 111920

## 10 10 106170

## # ℹ 94 more rowsI then plot the data and mark week 88, when the rival product hits the market. The data before week 88 has a clear upward trend. This changes after week 88. Often, data can have a point where a significant event not captured within the data changes the trend and/or seasonality of the data. A good example of this is housing sales data from 2000 to 2019. In this middle of this data the housing market crash and resulting economic effects can be reasonably expected to have a large impact on the data after this event.

cereal |>

ggplot(aes(x = time, y = sales)) +

geom_point(size = 0.5) +

geom_line() +

geom_vline(aes(xintercept = 88)) +

labs(title = "Plot of Cereal Sales over Time")

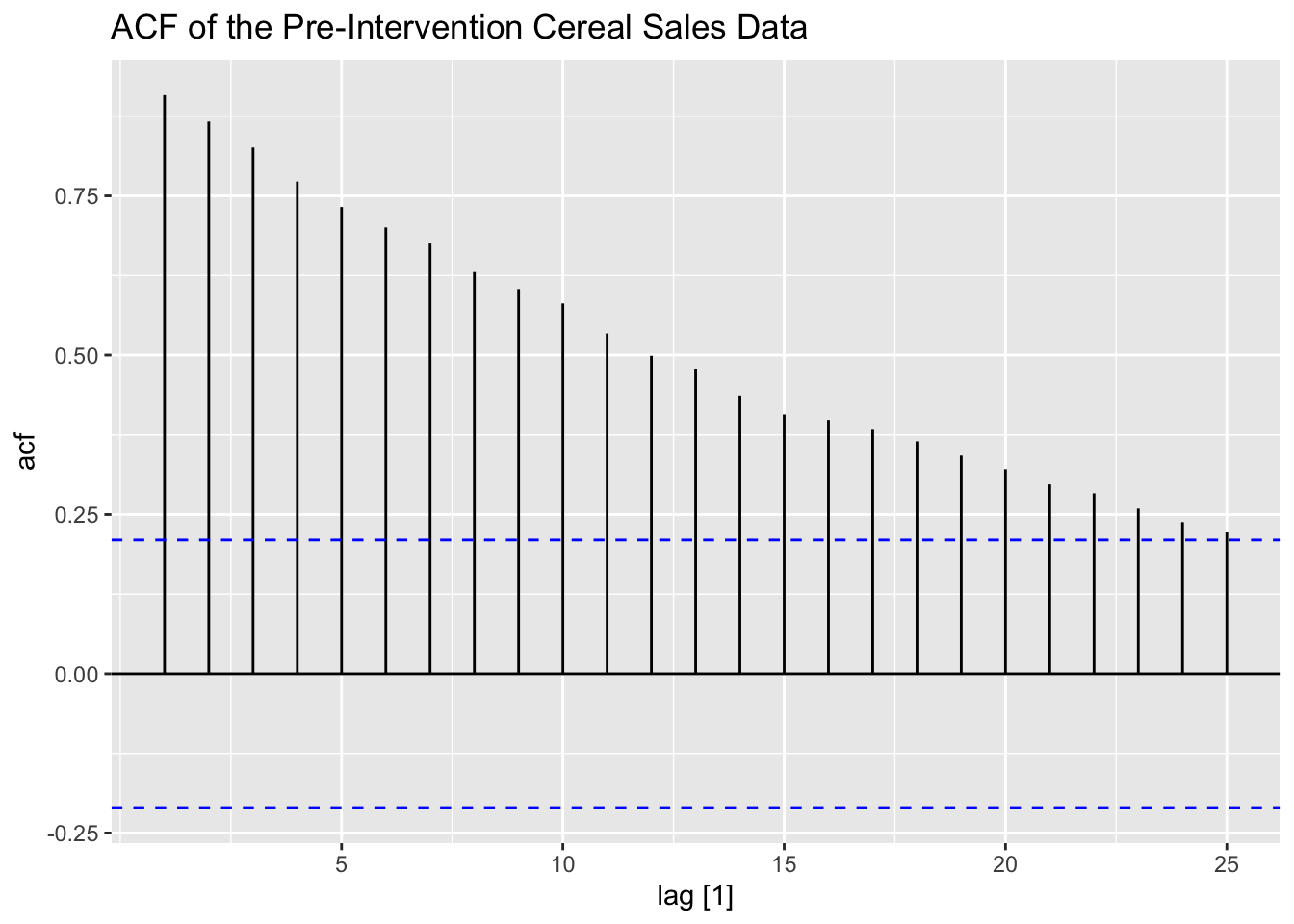

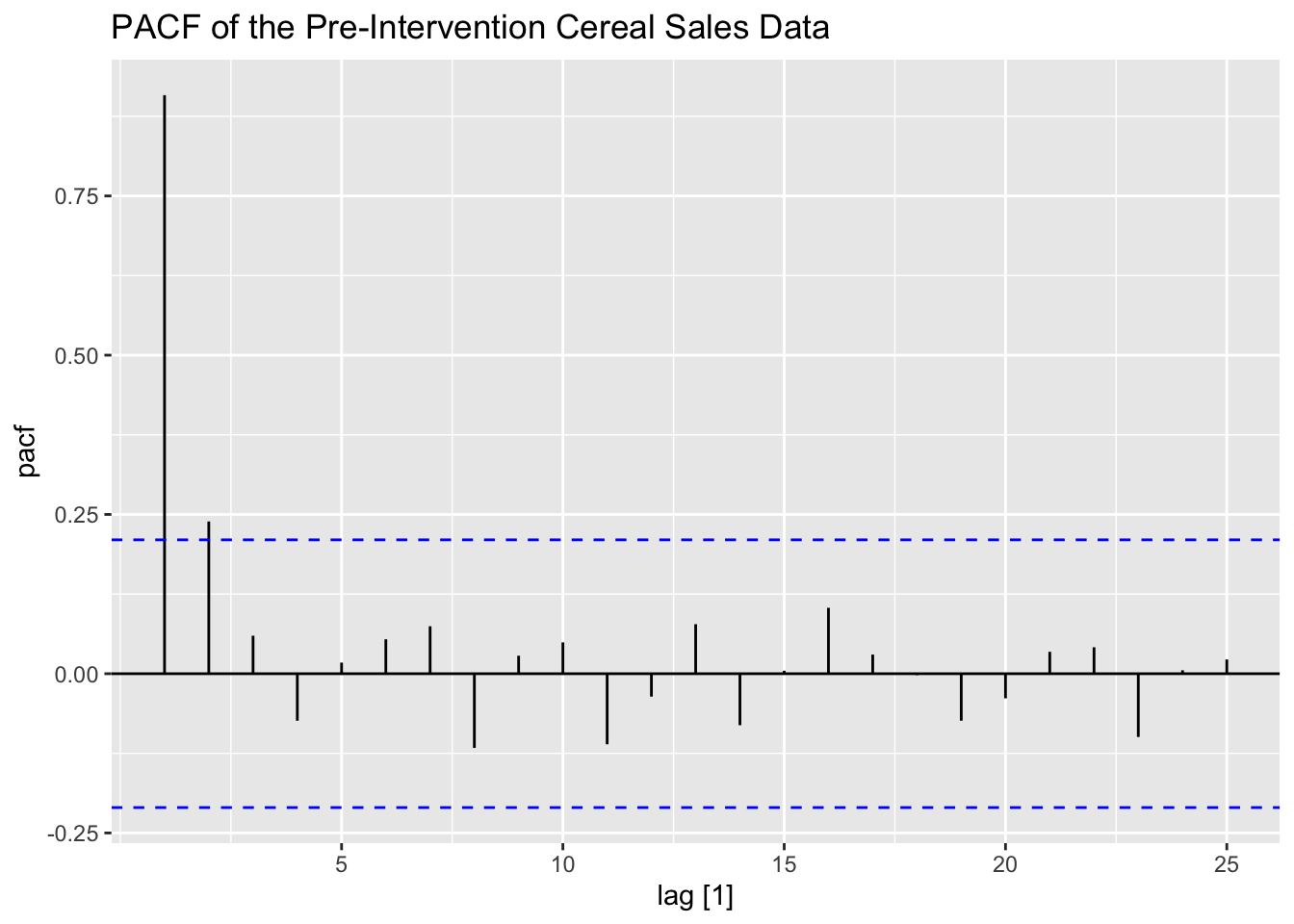

To identify the ARMA for pre-intervention data, I plot the ACF and PACF of the data. The ACF and PACF show that there is clearly lingering autocorrelation and that the data could possibly benefit from differencing.

cereal |>

filter(time <= 87) |>

ACF(sales, lag_max = 25) |>

autoplot() +

labs(title = "ACF of the Pre-Intervention Cereal Sales Data")

cereal |>

filter(time <= 87) |>

PACF(sales, lag_max = 25) |>

autoplot() +

labs(title = "PACF of the Pre-Intervention Cereal Sales Data")

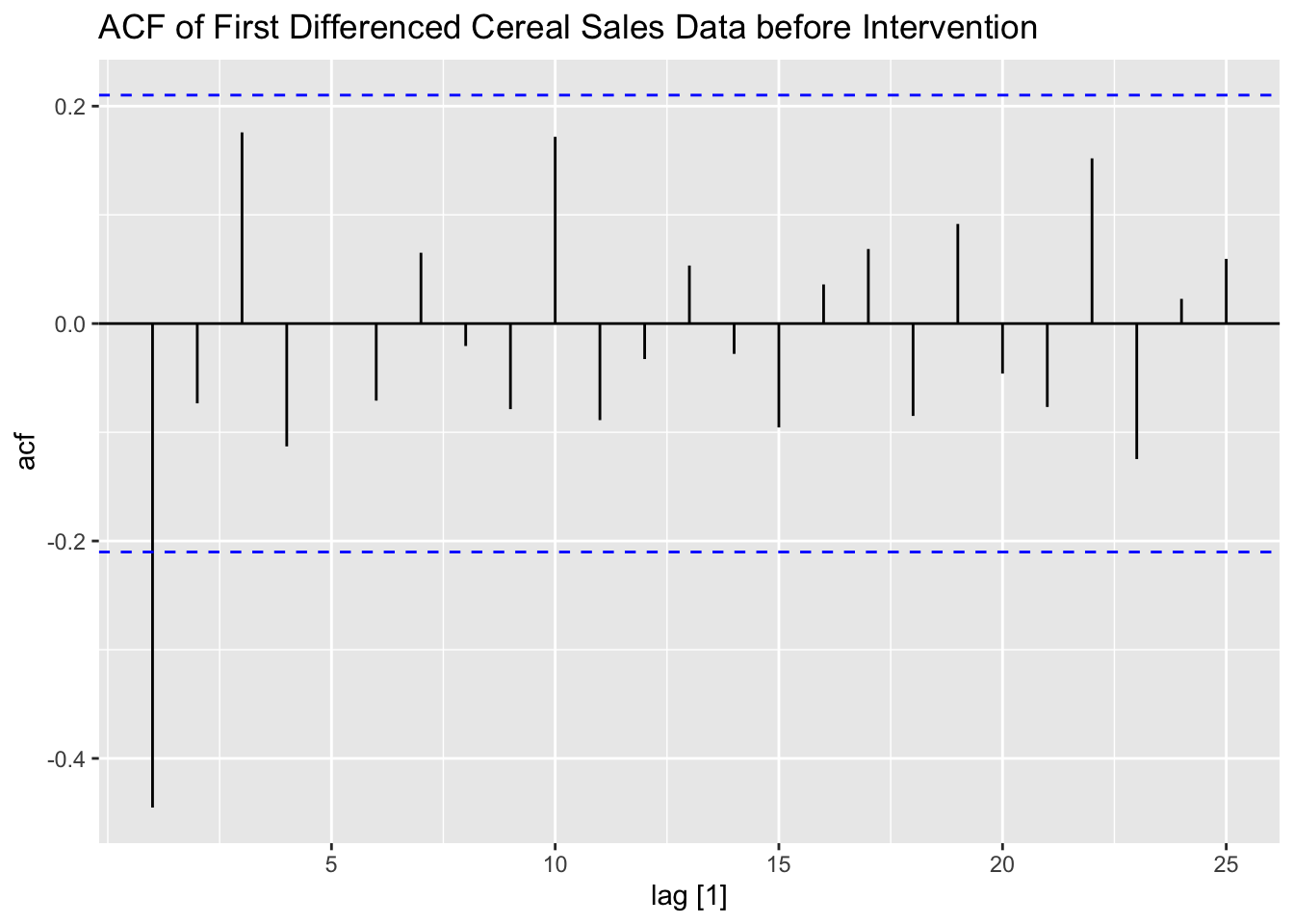

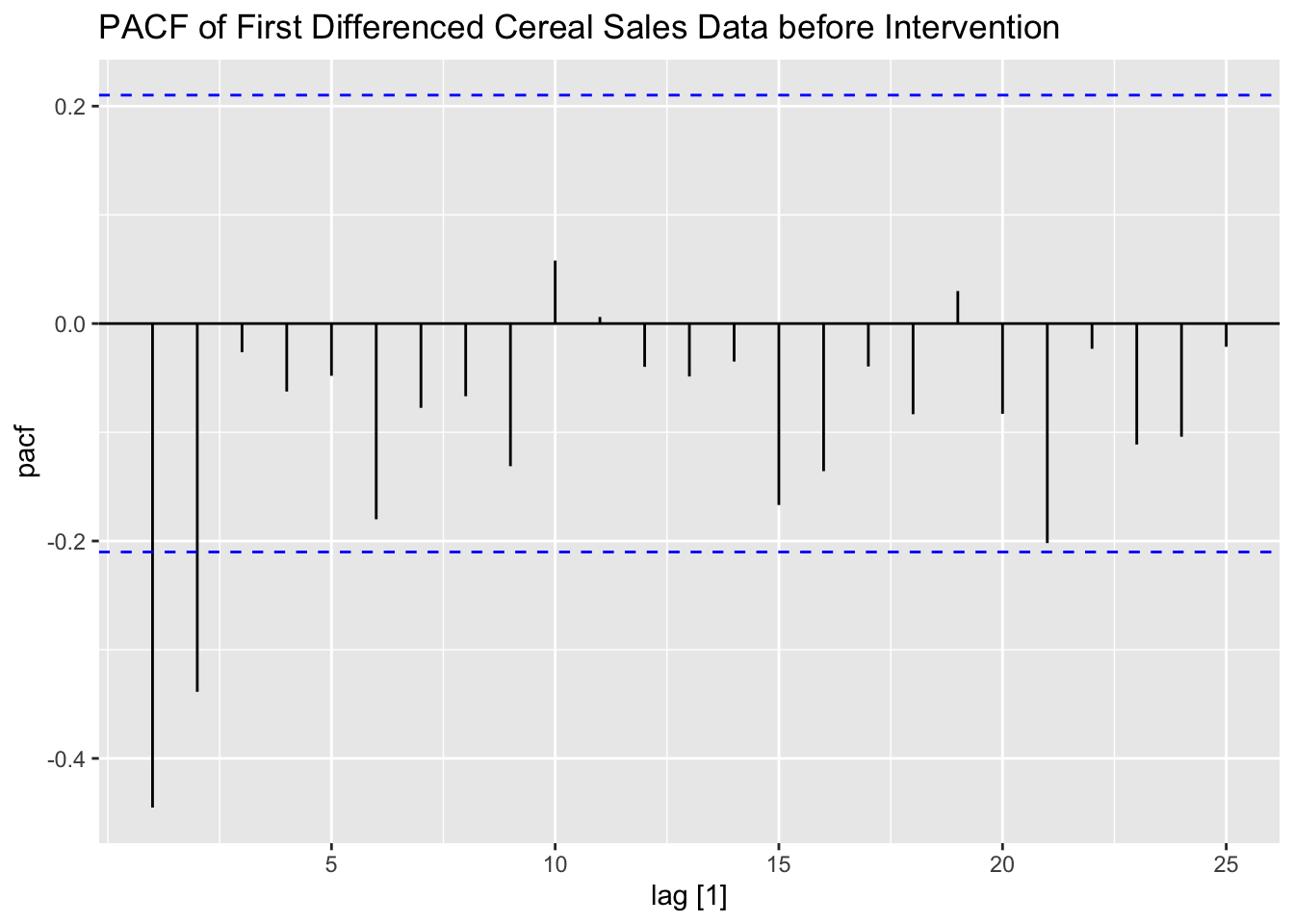

I then take the first difference of the data and examine the pre-intervention first differenced ACF and PACF of the data. I also create an indicator variable, which equals zero before week 88 and equals one after. This will serve as a dummy variable indicating if the competitor has entered the market yet.

#create the difference variable and intervention variable

(cereal <- cereal |>

mutate(diff = difference(sales, 1),

ind = case_when(time <= 87 ~ 0,

time > 87 ~ 1)))## # A tsibble: 104 x 4 [1]

## time sales diff ind

## <dbl> <dbl> <dbl> <dbl>

## 1 1 102450 NA 0

## 2 2 98930 -3520 0

## 3 3 91550 -7380 0

## 4 4 111940 20390 0

## 5 5 103380 -8560 0

## 6 6 112120 8740 0

## 7 7 105780 -6340 0

## 8 8 103000 -2780 0

## 9 9 111920 8920 0

## 10 10 106170 -5750 0

## # ℹ 94 more rowscereal |>

filter(time <= 87) |>

ACF(diff, lag_max = 25) |>

autoplot() +

labs(title = "ACF of First Differenced Cereal Sales Data before Intervention")

cereal |>

filter(time <= 87) |>

PACF(diff, lag_max = 25) |>

autoplot() +

labs(title = "PACF of First Differenced Cereal Sales Data before Intervention")

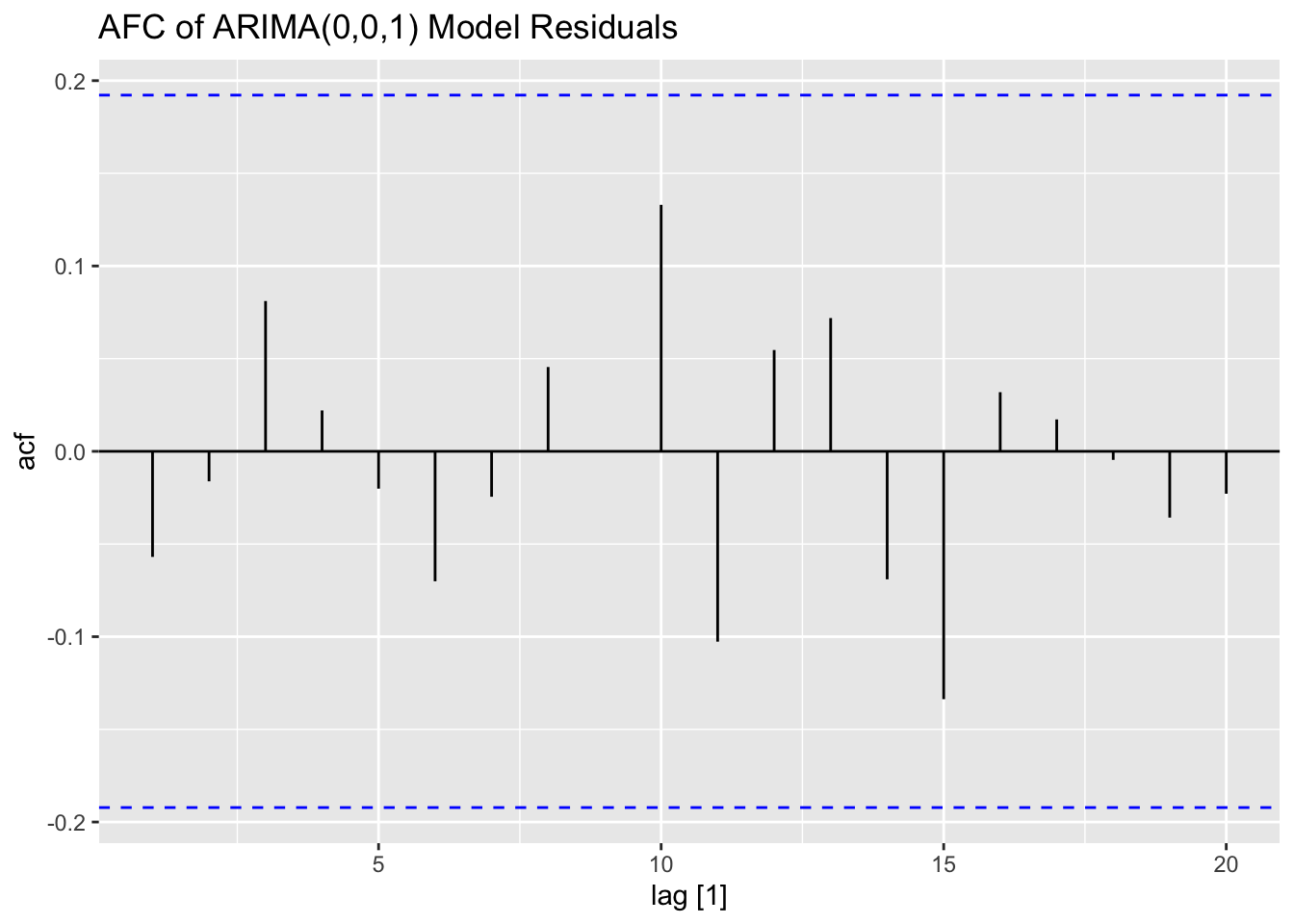

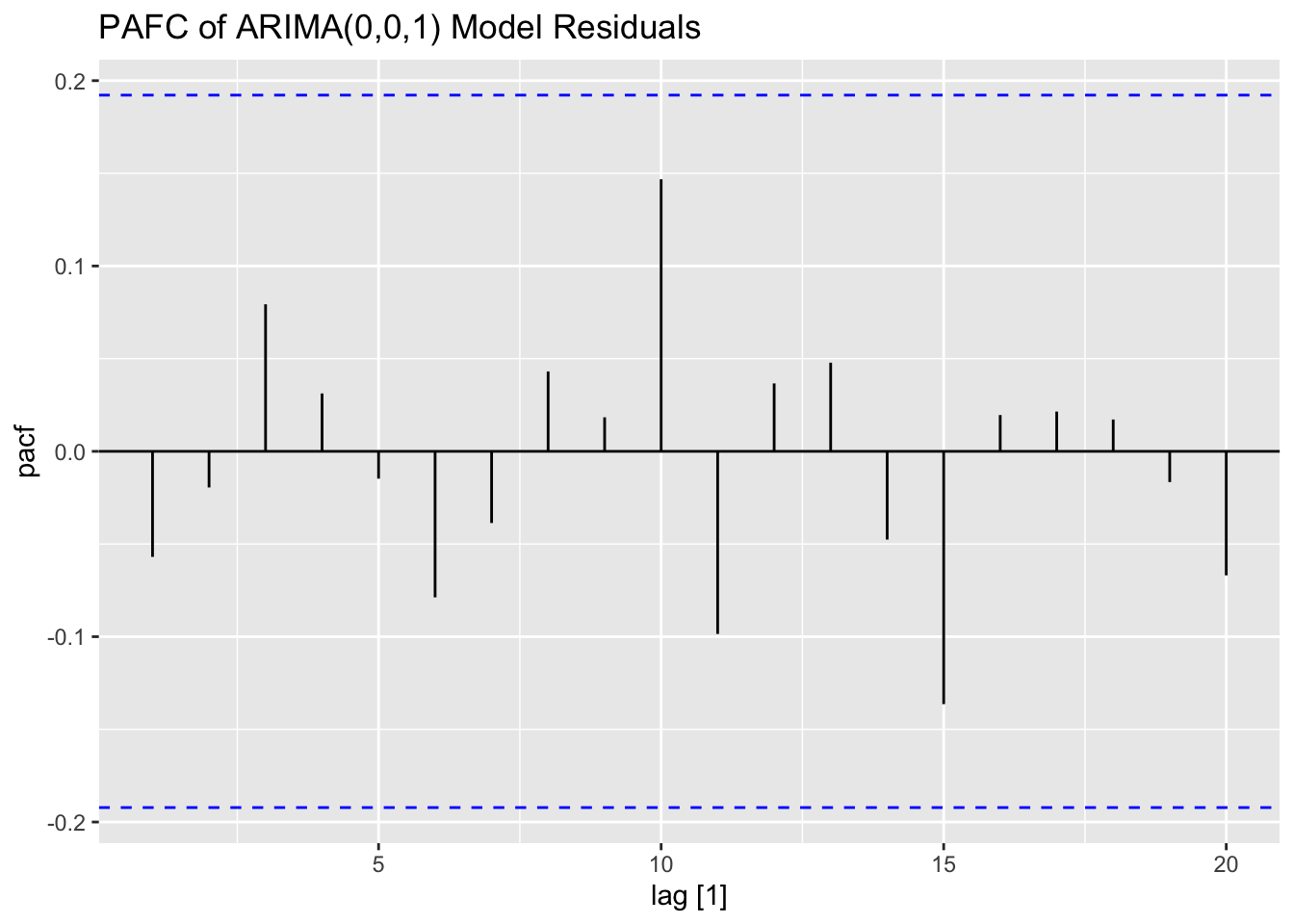

After examining the ACF and PACF, I create an linear model regressing the differenced data on the indicator variable with ARIMA(0,0,1) errors. For comparison, I allow the algorithm to select the best ARIMA model for the differenced data according to AICc. The linear model with ARIMA errors performs slightly better than the ARIMA model selected by the algorithm.

cereal.fit <- cereal |>

model(int = ARIMA(diff ~ 0 + pdq(0,0,1) + ind),

best = ARIMA(diff, stepwise = FALSE))

cereal.fit |> select(best) |> report()## Series: diff

## Model: ARIMA(0,0,1)

##

## Coefficients:

## ma1

## -0.5144

## s.e. 0.0772

##

## sigma^2 estimated as 96667735: log likelihood=-1093.22

## AIC=2190.45 AICc=2190.57 BIC=2195.74## Series: diff

## Model: LM w/ ARIMA(0,0,1) errors

##

## Coefficients:

## ma1 ind

## -0.5571 -2369.901

## s.e. 0.0757 1104.530

##

## sigma^2 estimated as 93672303: log likelihood=-1091.13

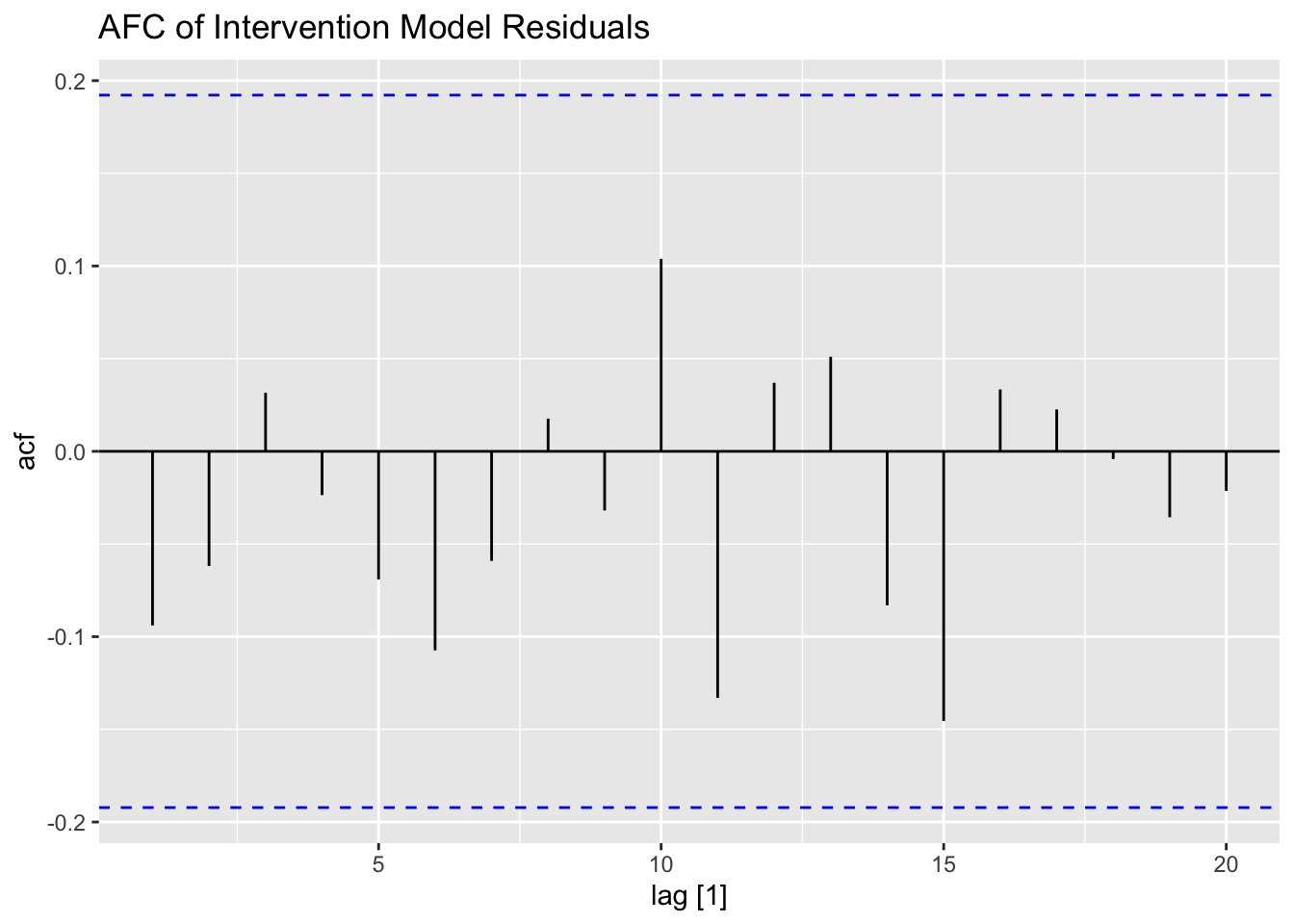

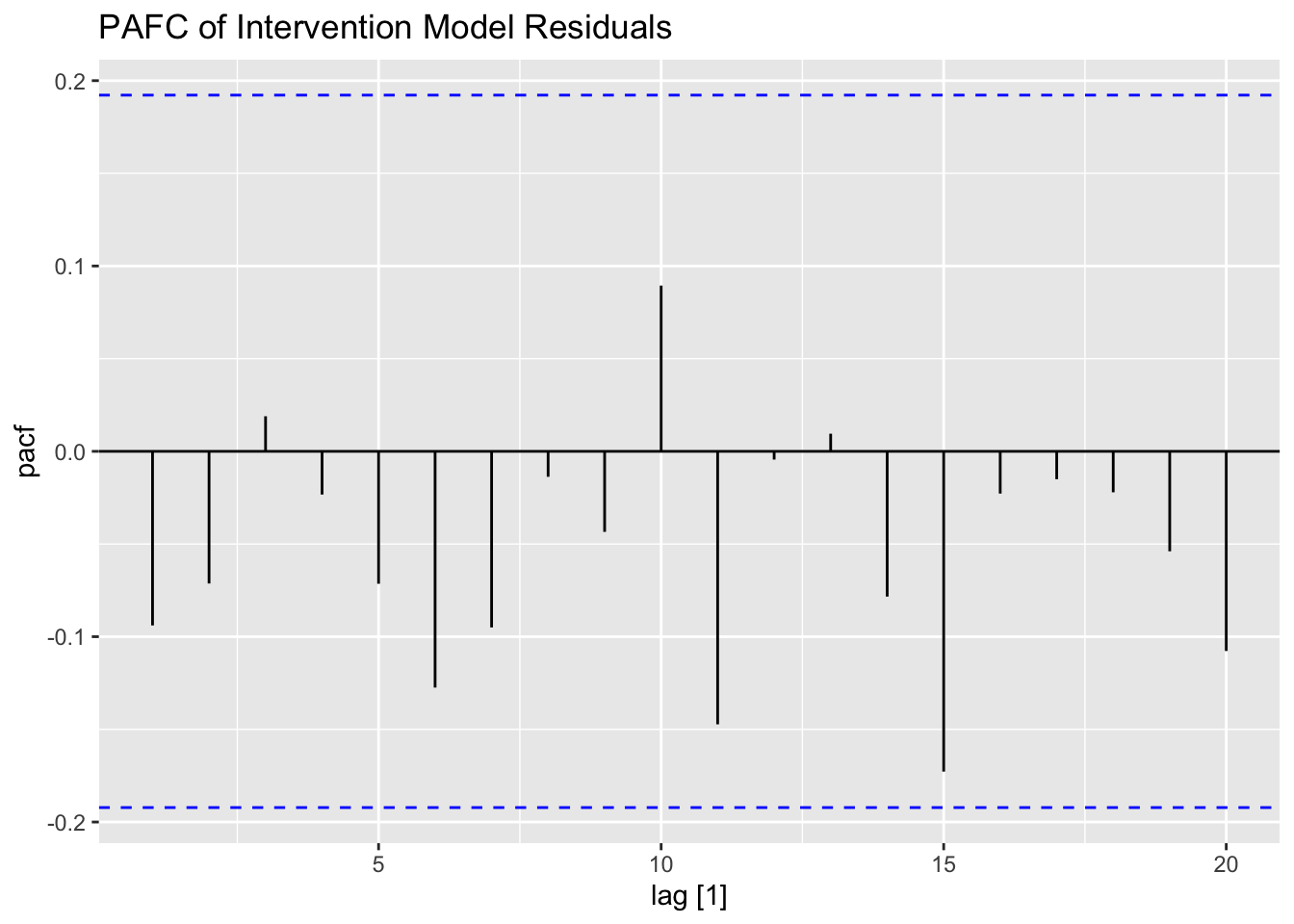

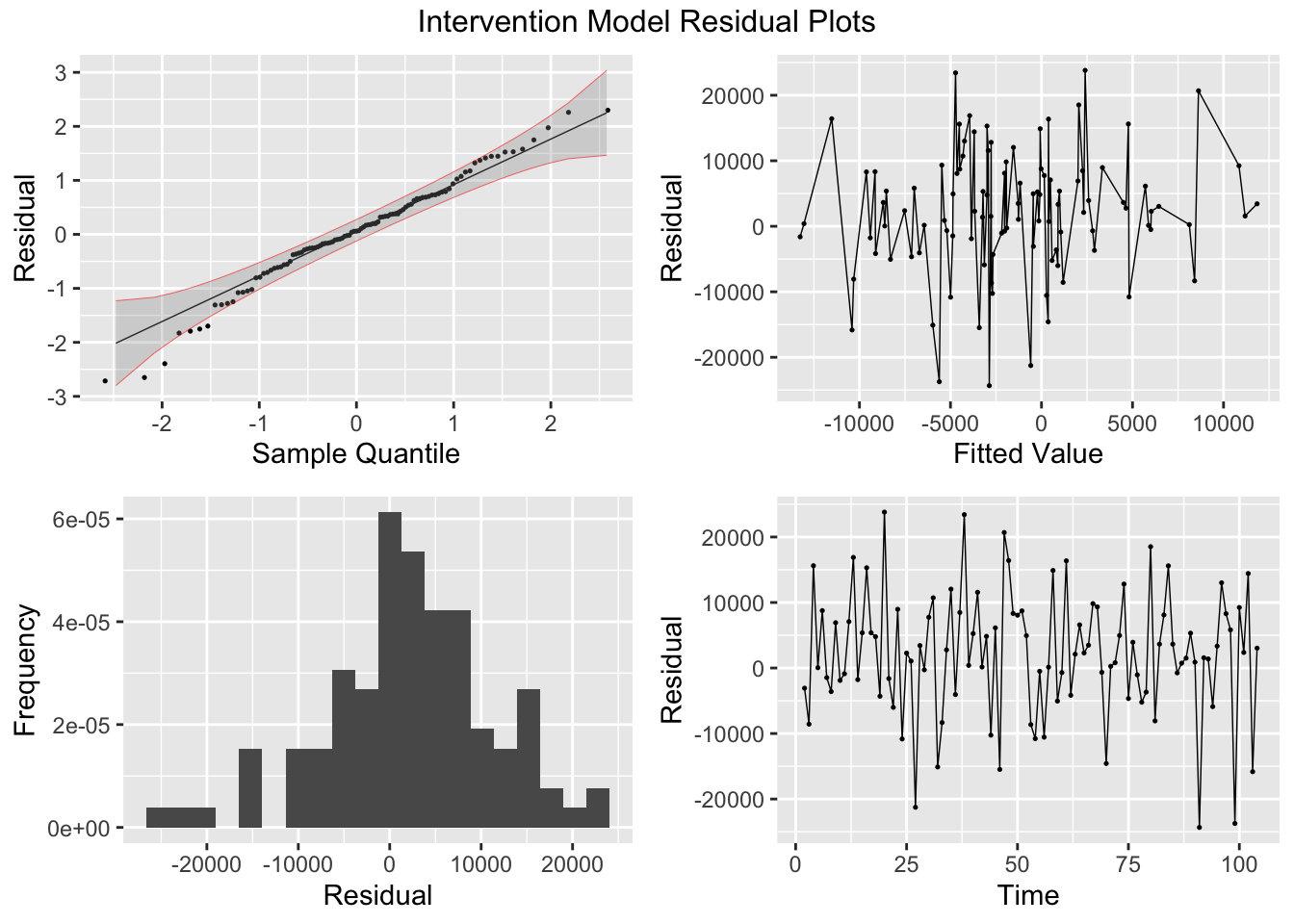

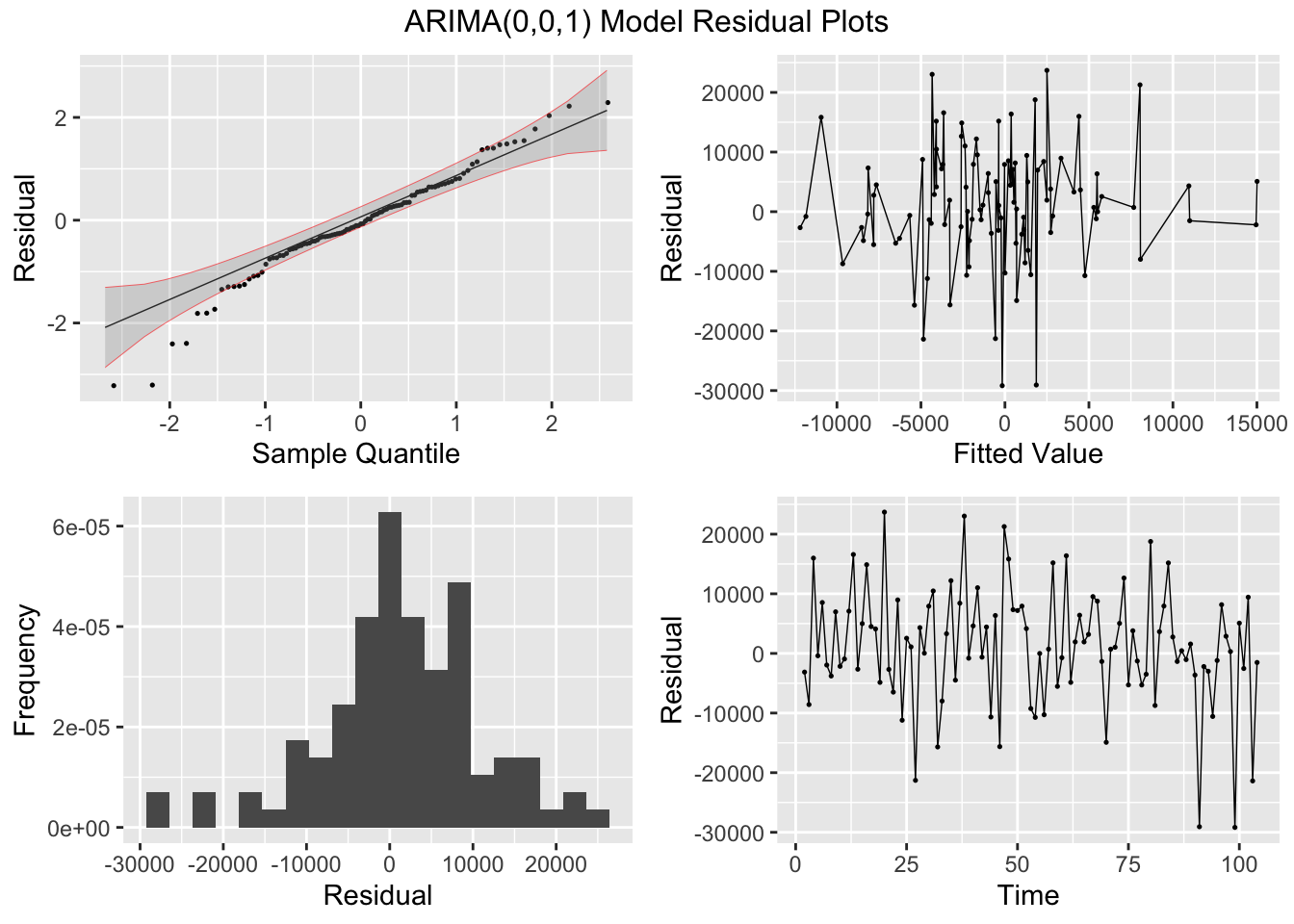

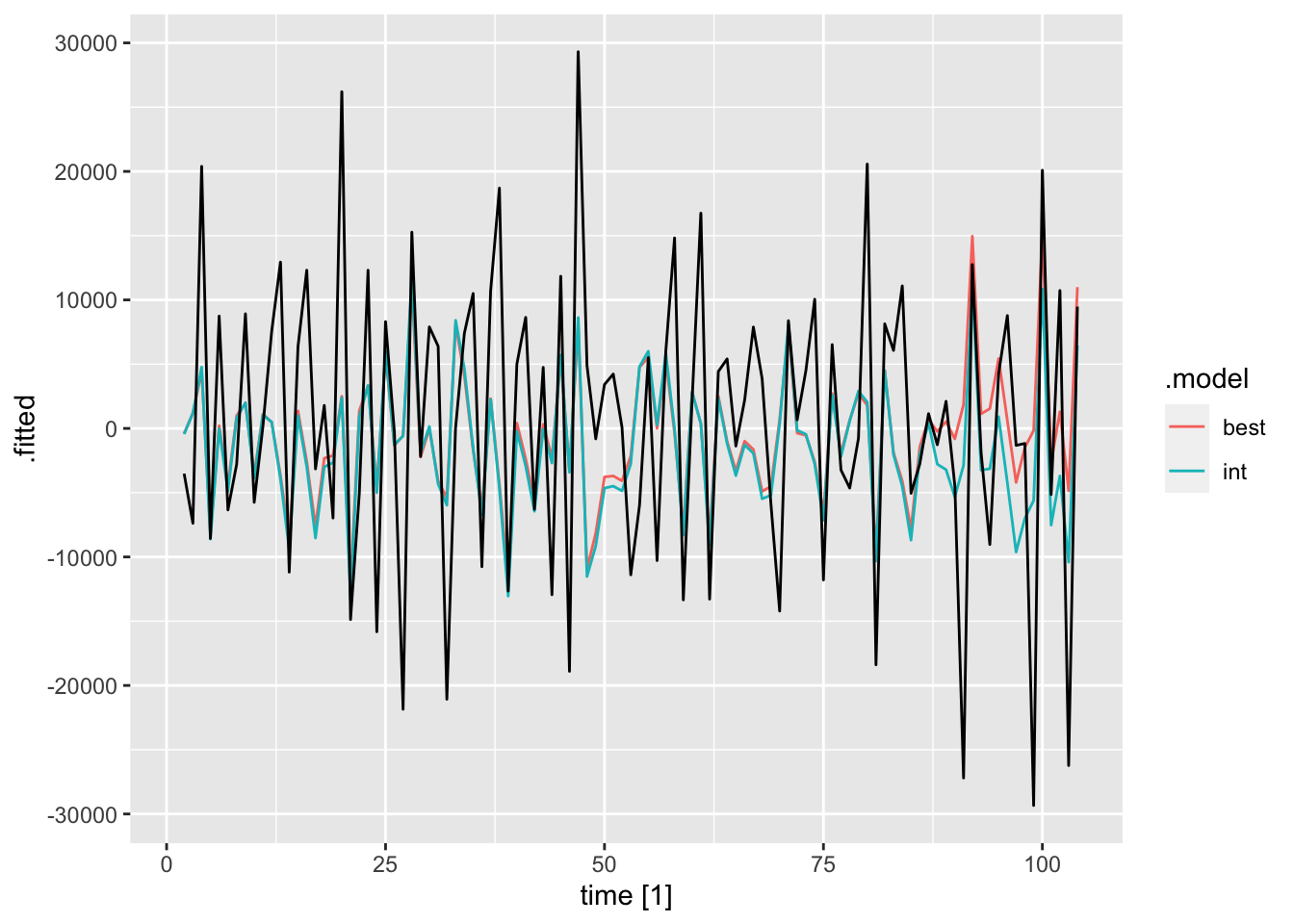

## AIC=2188.27 AICc=2188.51 BIC=2196.2I then plot and examine the residuals of the model using plot_residuals() and plot both of the models with the original data. I look at the measures of accuracy using the accuracy function as well. The residuals from both models do not have any lingering autocorrelation. The intervention model appears to perform slightly better than the straight ARIMA model.

## # A tibble: 2 × 3

## .model lb_stat lb_pvalue

## <chr> <dbl> <dbl>

## 1 best 0.344 0.558

## 2 int 0.935 0.333

## # A tibble: 2 × 3

## .model kpss_stat kpss_pvalue

## <chr> <dbl> <dbl>

## 1 best 0.360 0.0942

## 2 int 0.0841 0.1

## NULL## Warning: Removed 2 rows containing missing values (`geom_line()`).## Warning: Removed 1 row containing missing values (`geom_line()`).

dig <- function(x){round(x, digits = 3)} # function for mutate if to round digits to 3 decimals

accuracy(cereal.fit) |> mutate_if(is.numeric, dig) |> gt()| .model | .type | ME | RMSE | MAE | MPE | MAPE | MASE | RMSSE | ACF1 |

|---|---|---|---|---|---|---|---|---|---|

| int | Training | 2204.559 | 9631.348 | 7399.349 | 0.301 | 277.564 | 0.484 | 0.504 | -0.094 |

| best | Training | 1252.384 | 9831.975 | 7355.590 | 7.420 | 252.298 | 0.481 | 0.515 | -0.057 |

6.1.2 Example 6.2: Transfer Function Noise Model for Chemical Process Viscosity

For this example, I will be using the chemical process viscocity data from ChemicalViscocity.csv. I use row_number() to create a periodic time variable and then assign that variable as the index when making it into a tsibble.

(visc <- read_csv("data/ChemicalViscosity.csv") |>

rename(temp = 1, visc = 2) |>

mutate(time = row_number()) |>

as_tsibble(index = time))## Rows: 100 Columns: 2

## ── Column specification ───────────────────────────────────────

## Delimiter: ","

## dbl (2): temperature, viscosity

##

## ℹ Use `spec()` to retrieve the full column specification for this data.

## ℹ Specify the column types or set `show_col_types = FALSE` to quiet this message.## # A tsibble: 100 x 3 [1]

## temp visc time

## <dbl> <dbl> <int>

## 1 0.17 0.3 1

## 2 0.13 0.18 2

## 3 0.19 0.09 3

## 4 0.09 0.06 4

## 5 0.03 0.3 5

## 6 0.11 0.44 6

## 7 0.15 0.46 7

## 8 -0.02 0.44 8

## 9 0.07 0.34 9

## 10 0 0.23 10

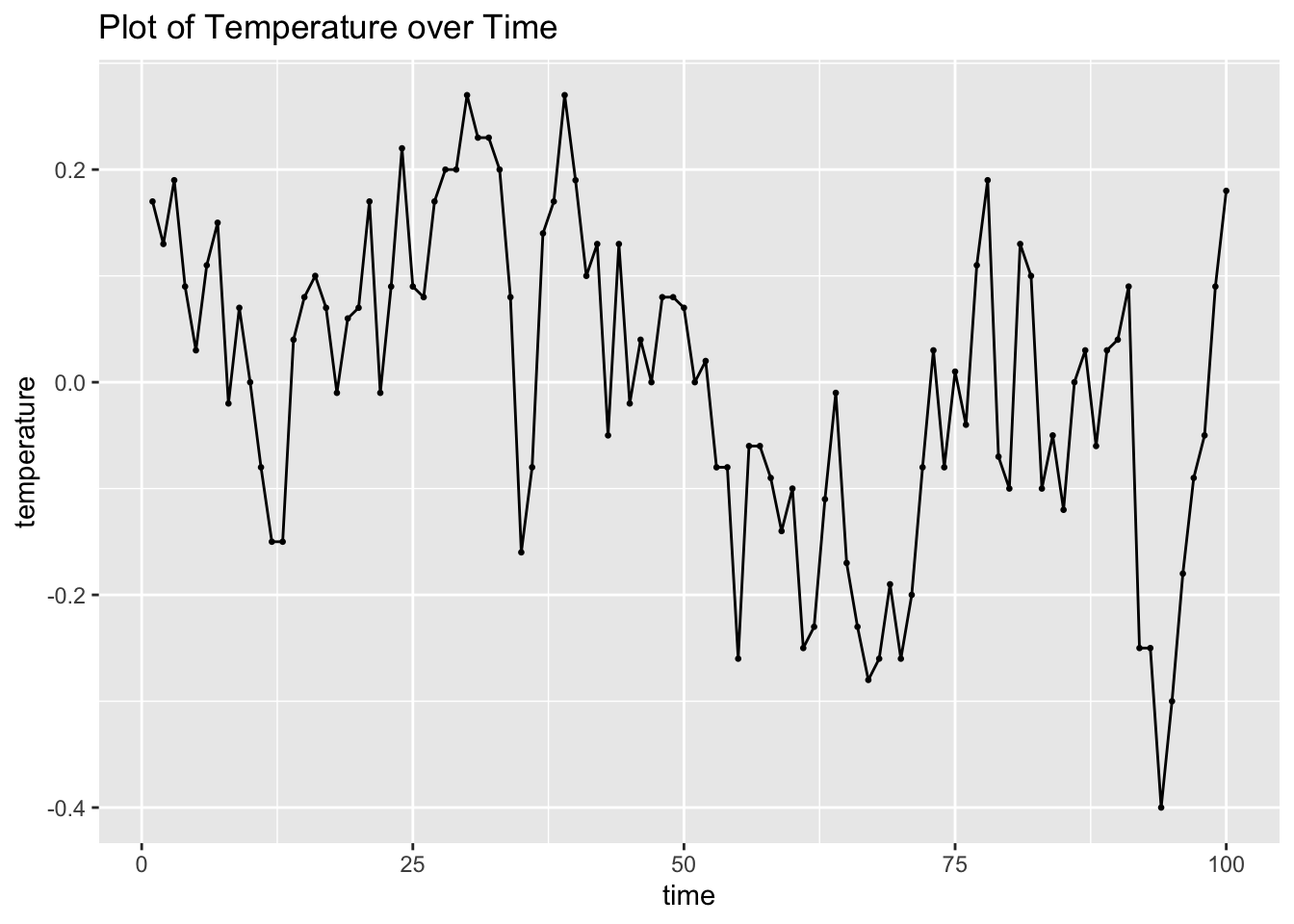

## # ℹ 90 more rowsI then plot both the temperature and viscosity variables over time for visual analysis.

visc |>

ggplot(aes(x = time, y = temp)) +

geom_point(size = 0.5) +

geom_line() +

labs(title = "Plot of Temperature over Time",

y = "temperature")

visc |>

ggplot(aes(x = time, y = visc)) +

geom_point(size = 0.5) +

geom_line() +

labs(title = "Plot of Chemical Viscocity over Time",

y = "viscocity")

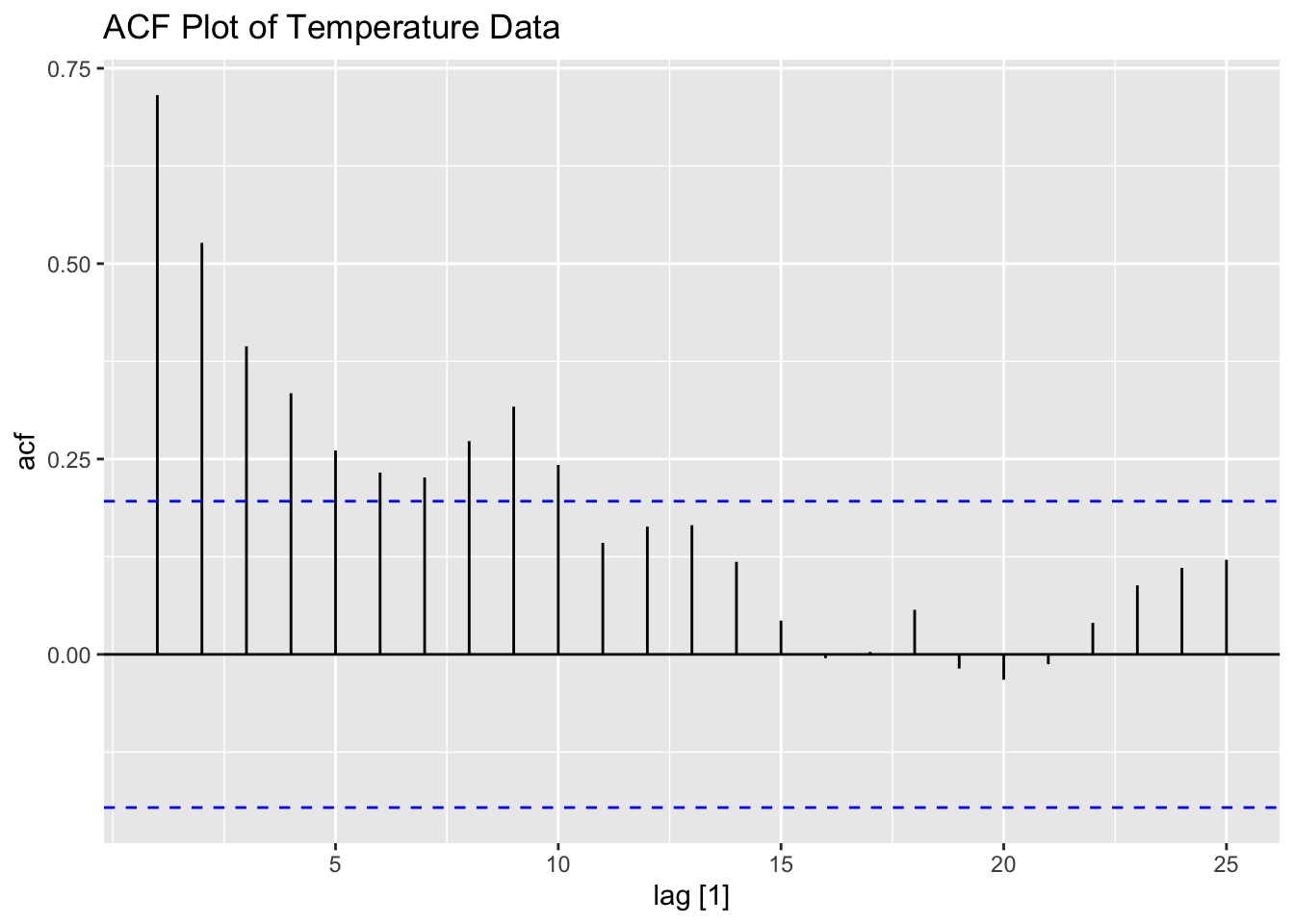

Next is prewhitening. To identify a model for temperature, I plot its ACF and PACF below.

I then fit an AR(1) model to temperature. Recall, to make sure a model is exactly as specified, you must include all components (constant, pdq, and PDQ). The coefficient in the AR(1) model is statistically significant.

visc.temp.fit <- visc |>

model(ar1 = ARIMA(temp ~ 0 + pdq(1,0,0) + PDQ(0,0,0)))

visc.temp.fit |> tidy() |> mutate_if(is.numeric, dig) |> gt()| .model | term | estimate | std.error | statistic | p.value |

|---|---|---|---|---|---|

| ar1 | ar1 | 0.729 | 0.069 | 10.633 | 0 |

I then examine the ACF, PACF, and residuals of the AR(1) model of temperature. The residuals do not have any lingering autocorrelation.

## # A tibble: 1 × 3

## .model lb_stat lb_pvalue

## <chr> <dbl> <dbl>

## 1 ar1 0.0468 0.829

## # A tibble: 1 × 3

## .model kpss_stat kpss_pvalue

## <chr> <dbl> <dbl>

## 1 ar1 0.335 0.1

## NULLNext, I prewhiten both series using an AR(1) coefficient of 0.73 from the model of temperature above. I calculate \(\alpha_{t}\) and \(\beta_{t}\) within mutate() and use lag() to multiply the previous observation by the coefficient. Finally, I plot the CCF of \(\alpha_{t}\) and \(\beta_{t}\).

## # A tsibble: 100 x 5 [1]

## temp visc time alpha beta

## <dbl> <dbl> <int> <dbl> <dbl>

## 1 0.17 0.3 1 NA NA

## 2 0.13 0.18 2 0.0059 -0.039

## 3 0.19 0.09 3 0.0951 -0.0414

## 4 0.09 0.06 4 -0.0487 -0.00570

## 5 0.03 0.3 5 -0.0357 0.256

## 6 0.11 0.44 6 0.0881 0.221

## 7 0.15 0.46 7 0.0697 0.139

## 8 -0.02 0.44 8 -0.130 0.104

## 9 0.07 0.34 9 0.0846 0.0188

## 10 0 0.23 10 -0.0511 -0.0182

## # ℹ 90 more rowsralbe <- visc |>

CCF(alpha, beta)

ralbe |>

autoplot() +

geom_vline(aes(xintercept = 0), color = "blue") +

labs(title = "CCF of alpha(t) and beta(t)")

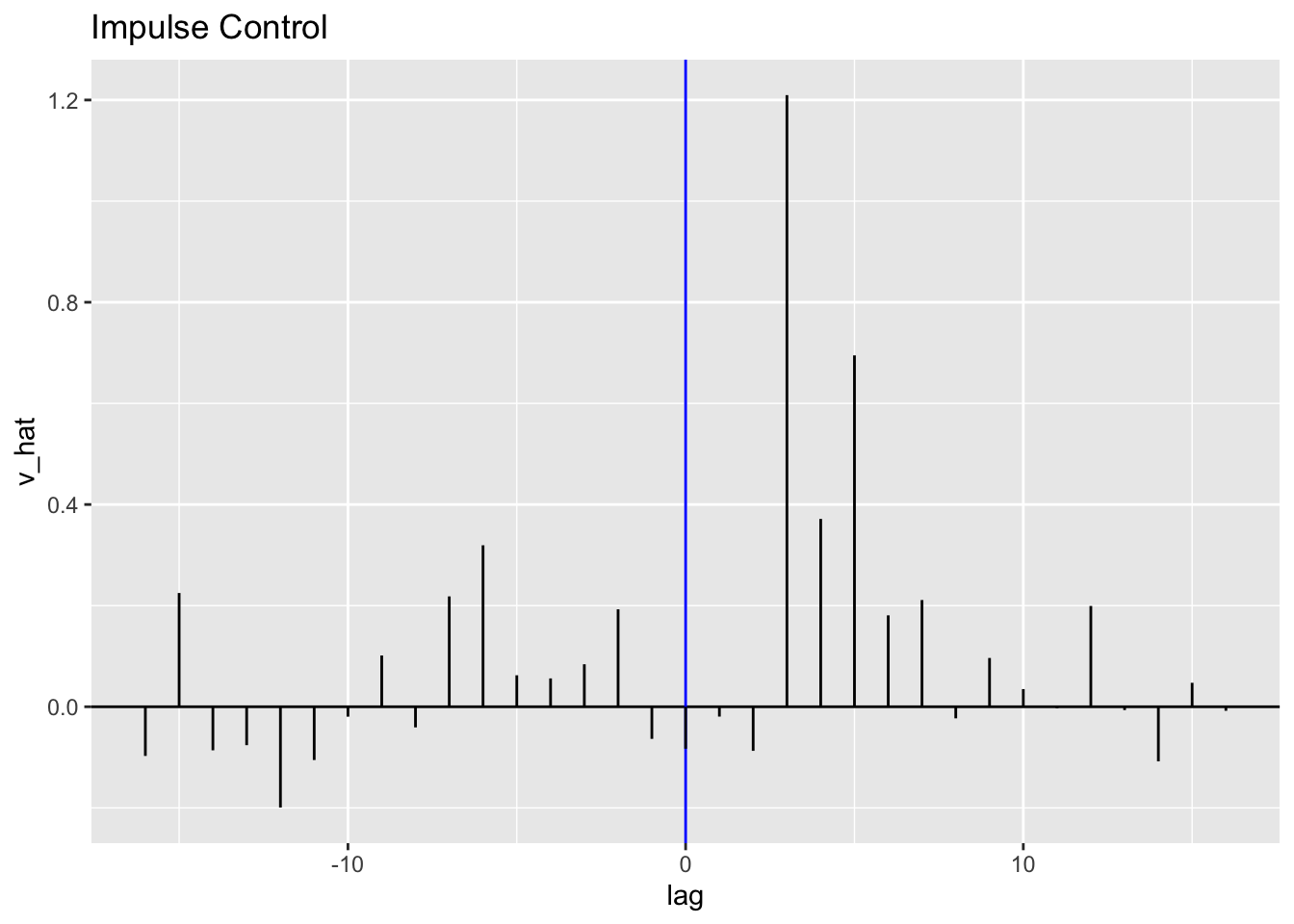

To obtain estimates of \(\hat v_{t}\), I use mutate() to create a vhat variable in the CCF data frame saved as ralbe. I then plot \(\hat v_{t}\) in a similar style as an ACF, PACF, or CCF. The blue line indicates the competitor entering the market. It looks very similar in shape to the CCF above because \(\hat v_{t}\) is a function of the CCF.

library(latex2exp)

(ralbe <- ralbe |>

mutate(vhat = sqrt(var(visc$beta[2:100])/var(visc$alpha[2:100]))*ccf))## # A tsibble: 33 x 3 [1]

## lag ccf vhat

## <cf_lag> <dbl> <dbl>

## 1 -16 -0.0521 -0.0972

## 2 -15 0.121 0.225

## 3 -14 -0.0461 -0.0861

## 4 -13 -0.0407 -0.0760

## 5 -12 -0.107 -0.199

## 6 -11 -0.0564 -0.105

## 7 -10 -0.0105 -0.0196

## 8 -9 0.0543 0.101

## 9 -8 -0.0219 -0.0408

## 10 -7 0.117 0.218

## # ℹ 23 more rowsralbe |>

ggplot(aes(x = lag, y = vhat)) +

geom_hline(aes(yintercept = 0)) +

geom_vline(aes(xintercept = 0), color = "blue") +

geom_segment(aes(xend = lag, yend = 0)) +

labs(title = "Impulse Control", y = "v_hat")

I then model the noise using the estimates given in the example. To do this, I create a vector of zeros, and then loop from the 4th element to the end, calculating Nhat. After calculations, I change the first three element from 0 to NA and then append the vector to the visc data frame.

T <-length(visc$temp)

Nhat <- vector(mode = "numeric", length = T)

for (i in 4:T){

Nhat[i] <- visc$visc[i] + 0.31*(Nhat[i-1]-visc$visc[i-1]) + 0.48*(Nhat[i-2]-visc$visc[i-2]) + 1.21*visc$temp[i-3]

}

Nhat[1:3] <- NA # 1:3 must be 0 in for loop for calculations

#must make those NA so then can mutate into visc

(visc <- visc |>

mutate(Nhat = Nhat))## # A tsibble: 100 x 6 [1]

## temp visc time alpha beta Nhat

## <dbl> <dbl> <int> <dbl> <dbl> <dbl>

## 1 0.17 0.3 1 NA NA NA

## 2 0.13 0.18 2 0.0059 -0.039 NA

## 3 0.19 0.09 3 0.0951 -0.0414 NA

## 4 0.09 0.06 4 -0.0487 -0.00570 0.151

## 5 0.03 0.3 5 -0.0357 0.256 0.442

## 6 0.11 0.44 6 0.0881 0.221 0.758

## 7 0.15 0.46 7 0.0697 0.139 0.736

## 8 -0.02 0.44 8 -0.130 0.104 0.714

## 9 0.07 0.34 9 0.0846 0.0188 0.691

## 10 0 0.23 10 -0.0511 -0.0182 0.652

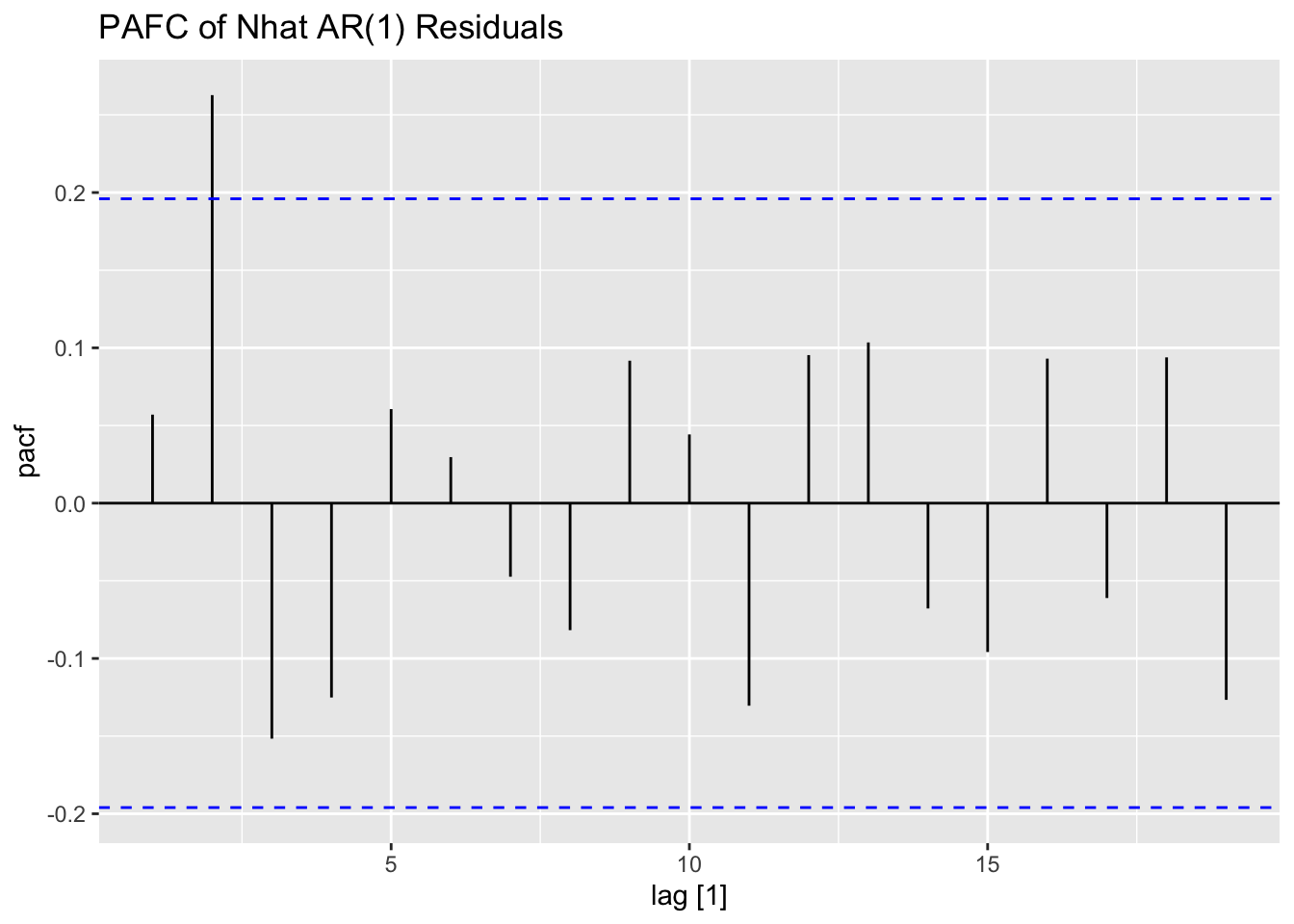

## # ℹ 90 more rowsI look at the ACF and PACF of the newly calculated Nhat to determine possible models.

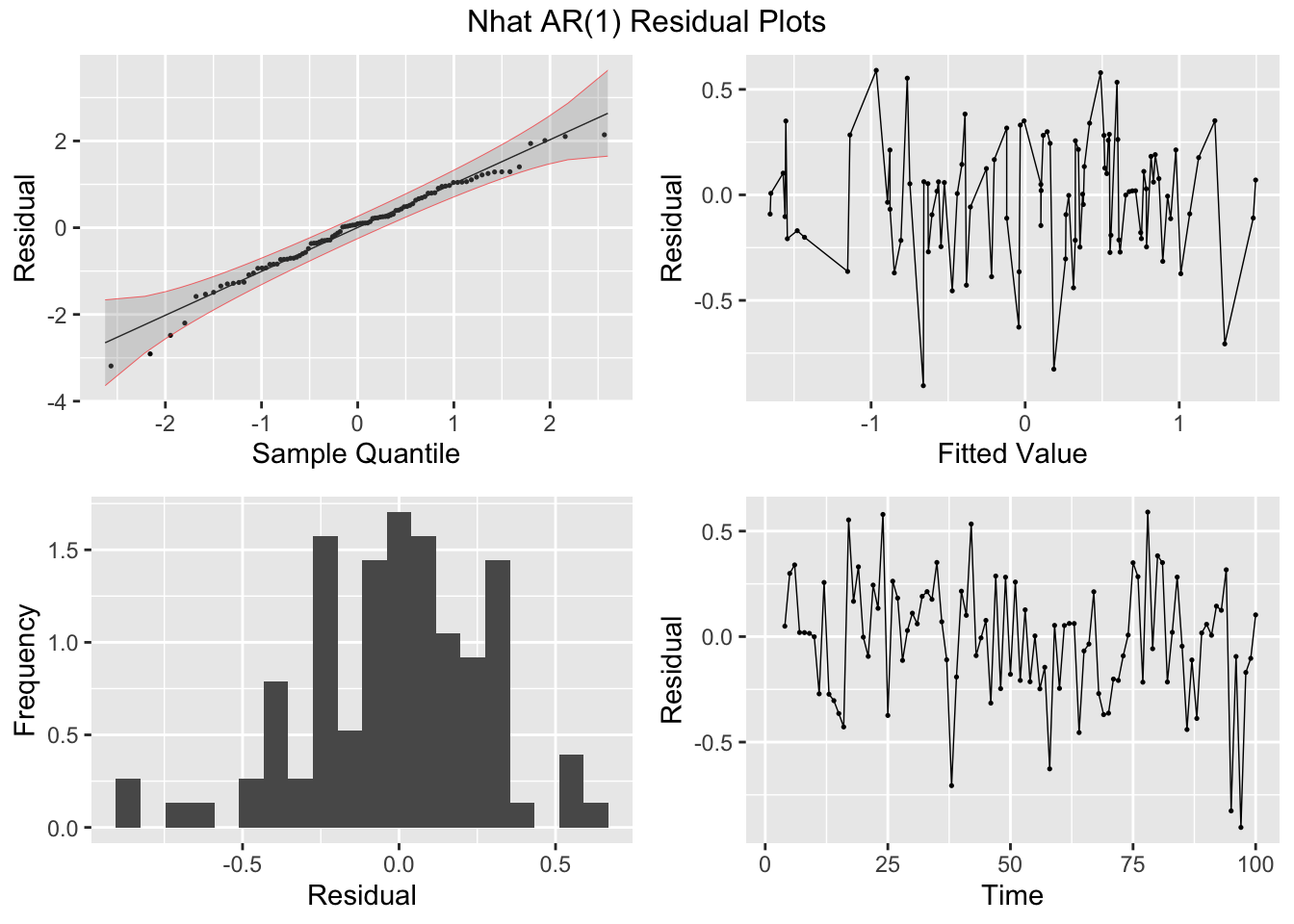

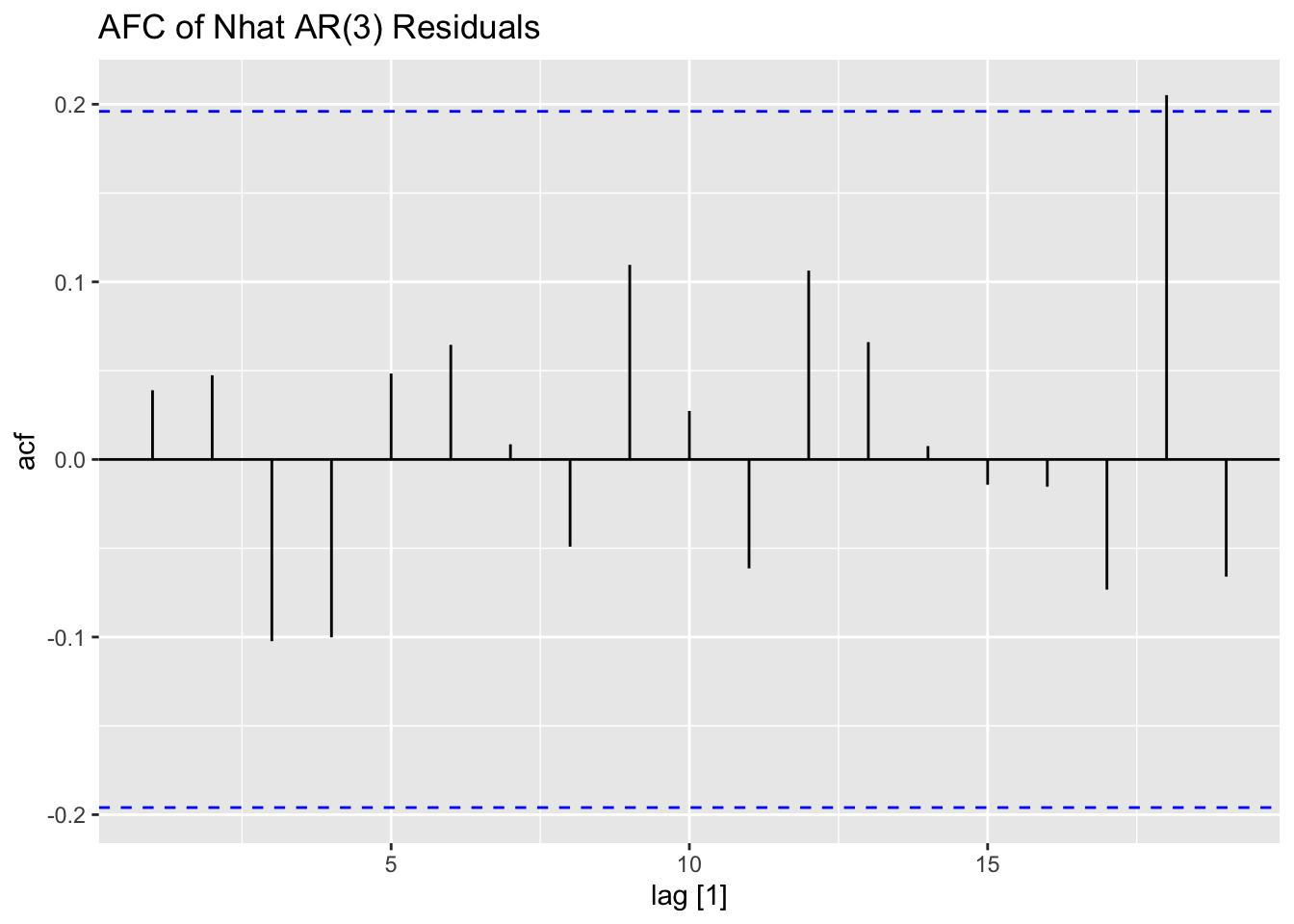

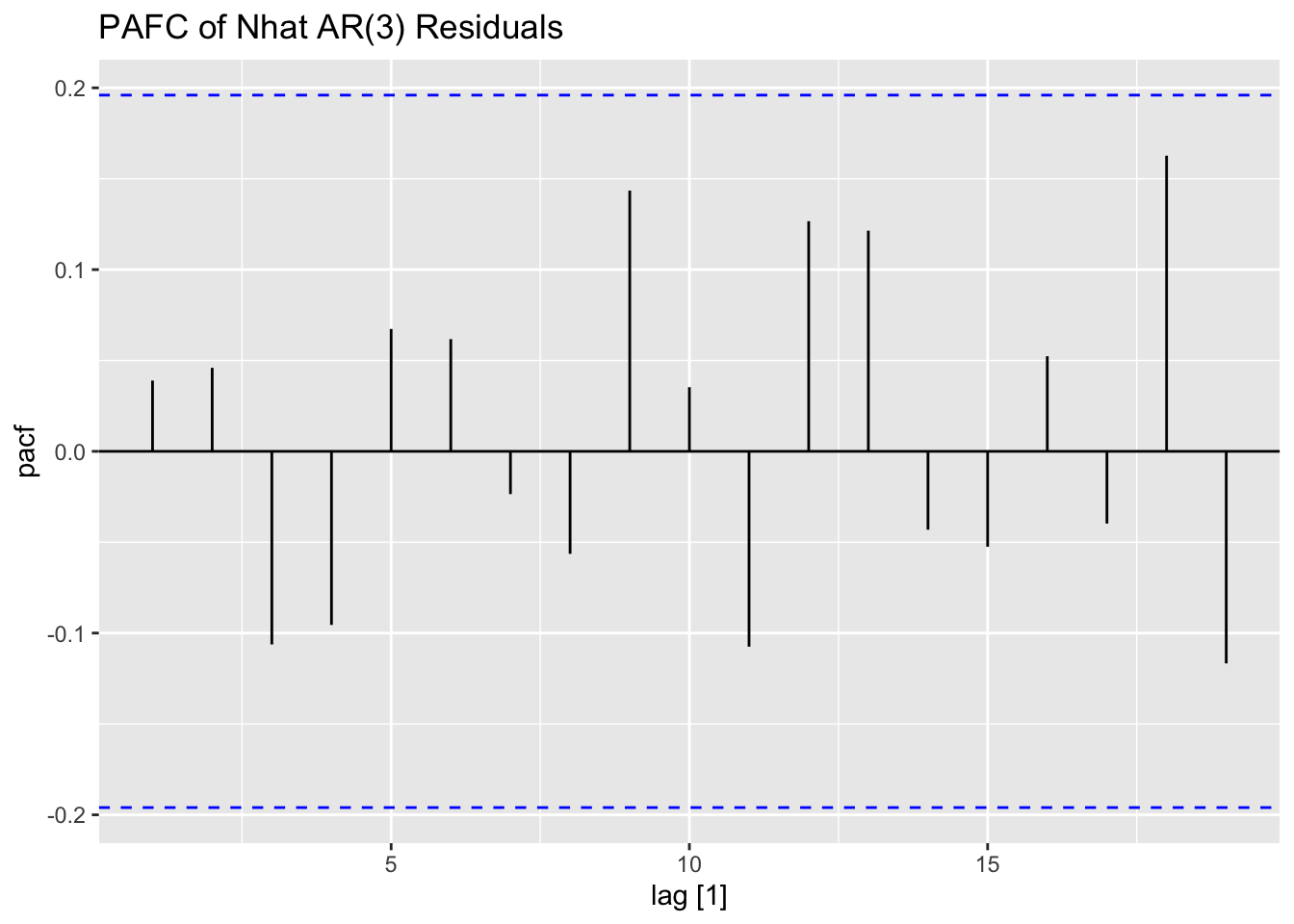

Next, I fit AR(1) and AR(3) models (without constants) to Nhat and plot the residuals of both models for analysis. The AR(1) model has lingering autocorrelation but the coefficients of the AR(3) model are not siginificant, so the AR(1) model is deemed to be the appropriate model.41

nhat.models <- visc |>

model(ar1 = ARIMA(Nhat ~ 0 + pdq(1,0,0) + PDQ(0,0,0)),

ar3 = ARIMA(Nhat ~ 0 + pdq(3,0,0) + PDQ(0,0,0)))

nhat.models |> select(ar1) |> report()## Series: Nhat

## Model: ARIMA(1,0,0)

##

## Coefficients:

## ar1

## 0.9452

## s.e. 0.0319

##

## sigma^2 estimated as 0.08013: log likelihood=-17.33

## AIC=38.66 AICc=38.78 BIC=43.87## Series: Nhat

## Model: ARIMA(3,0,0)

##

## Coefficients:

## ar1 ar2 ar3

## 0.9838 0.2249 -0.2893

## s.e. 0.0964 0.1369 0.0989

##

## sigma^2 estimated as 0.07483: log likelihood=-13.12

## AIC=34.24 AICc=34.66 BIC=44.66## # A tibble: 2 × 3

## .model lb_stat lb_pvalue

## <chr> <dbl> <dbl>

## 1 ar1 0.325 0.569

## 2 ar3 0.152 0.697

## # A tibble: 2 × 3

## .model kpss_stat kpss_pvalue

## <chr> <dbl> <dbl>

## 1 ar1 0.287 0.1

## 2 ar3 0.410 0.0727

## NULLThe transfer function noise model is not included in fable, so I will be using functions from the TSA package to create this model. The tentative overall model is shown in the equation below:

\[ y_{t} = \frac{w_{0}}{1 - \delta_{1}B - \delta_{2}B^{2}}x_{t-3} + \frac{1}{1 - \phi_{1}B} \epsilon_{t} \]42

Below, I define the components of the model and bind them together in a data frame before using arimax() to create the model.

ts.xt <- ts(visc$temp)

lag3.x <- stats::lag(ts.xt, -3)

ts.yt <- ts(visc$visc)

dat3 <- cbind(ts.xt,lag3.x,ts.yt)

dimnames(dat3)[[2]] <- c("xt","lag3x","yt")

data2 <- na.omit(as.data.frame(dat3))

#Input arguments

#order: determines the model for the error component,

# i.e. the order of the ARIMA model for y(t) if there were no x(t)

#xtransf: x(t)

#transfer: the orders (r and s) of the transfer function

visc.tf<-TSA::arimax(data2$yt,

order=c(1,0,0),

xtransf=data.frame(data2$lag3x),

transfer=list(c(2,0)),

include.mean = FALSE)

visc.tf##

## Call:

## TSA::arimax(x = data2$yt, order = c(1, 0, 0), include.mean = FALSE, xtransf = data.frame(data2$lag3x),

## transfer = list(c(2, 0)))

##

## Coefficients:

## ar1 data2.lag3x-AR1 data2.lag3x-AR2 data2.lag3x-MA0

## 0.8295 0.3414 0.2667 1.3276

## s.e. 0.0642 0.0979 0.0934 0.1104

##

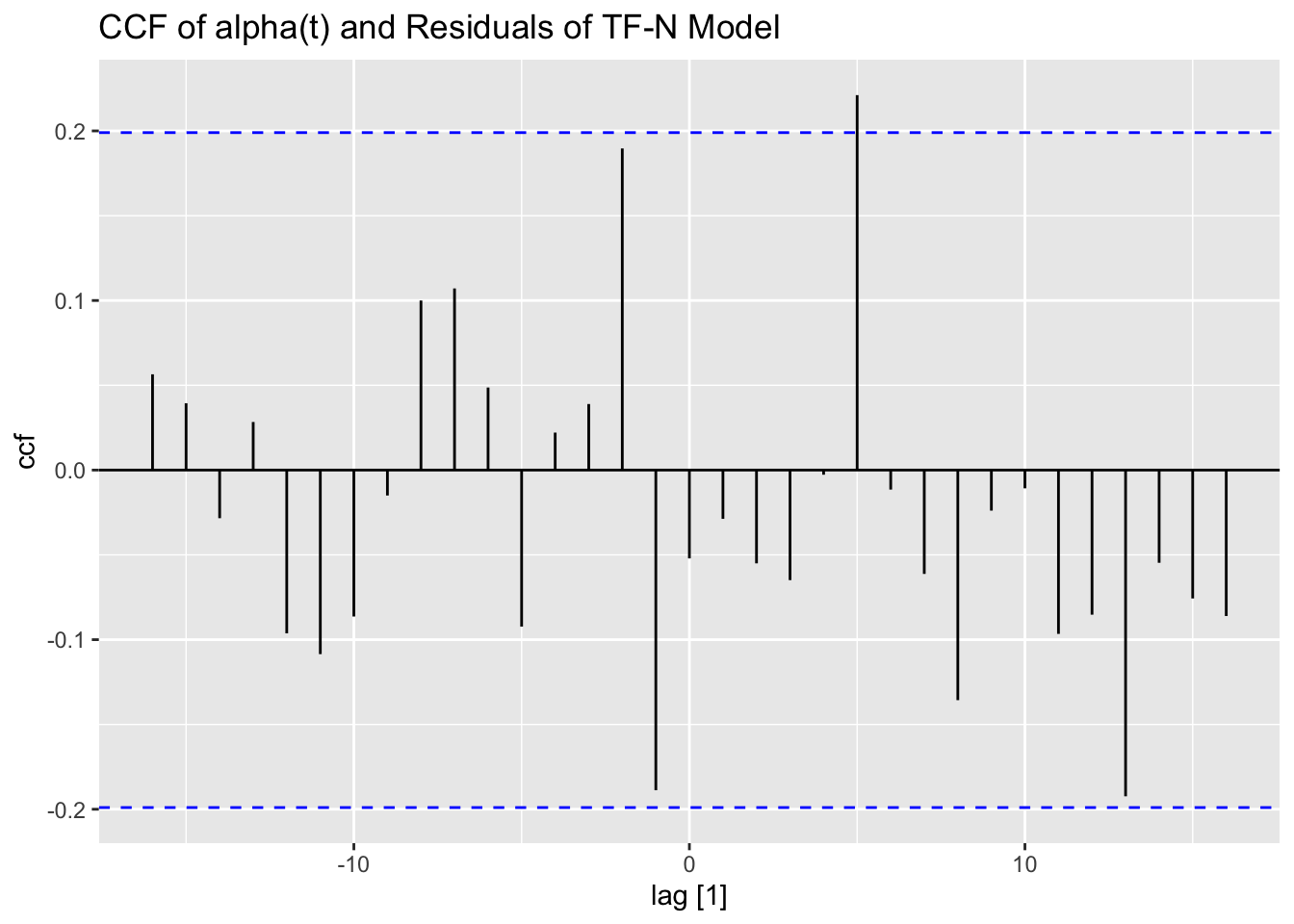

## sigma^2 estimated as 0.0123: log likelihood = 75.09, aic = -142.18To analyze the residuals of a model outside of fable using plot_residuals(), the residuals must be organized similarly to the results of augment(). After creating a tsibble containing the necessary information, I run the function. I also create a CCF of the residuals and alpha as well.

(resid <- tsibble(

.model = "TR-N",

time = visc$time[4:100],

.fitted = fitted(visc.tf),

.resid = residuals(visc.tf),

index = time

))## # A tsibble: 97 x 4 [1]

## .model time .fitted .resid

## <chr> <int> <dbl> <dbl>

## 1 TR-N 4 0.153 -0.0925

## 2 TR-N 5 0.112 0.188

## 3 TR-N 6 0.439 0.000552

## 4 TR-N 7 0.357 0.103

## 5 TR-N 8 0.370 0.0696

## 6 TR-N 9 0.472 -0.132

## 7 TR-N 10 0.394 -0.164

## 8 TR-N 11 0.0657 0.00431

## 9 TR-N 12 0.160 0.0499

## 10 TR-N 13 0.0986 -0.0686

## # ℹ 87 more rows## # A tibble: 1 × 2

## lb_stat lb_pvalue

## <dbl> <dbl>

## 1 0.865 0.352

## # A tibble: 1 × 2

## kpss_stat kpss_pvalue

## <dbl> <dbl>

## 1 0.0632 0.1

## NULLresid |>

left_join(visc, by = join_by(time)) |>

CCF(alpha, .resid) |>

autoplot() +

labs(title = "CCF of alpha(t) and Residuals of TF-N Model")

6.2 GARCH Models

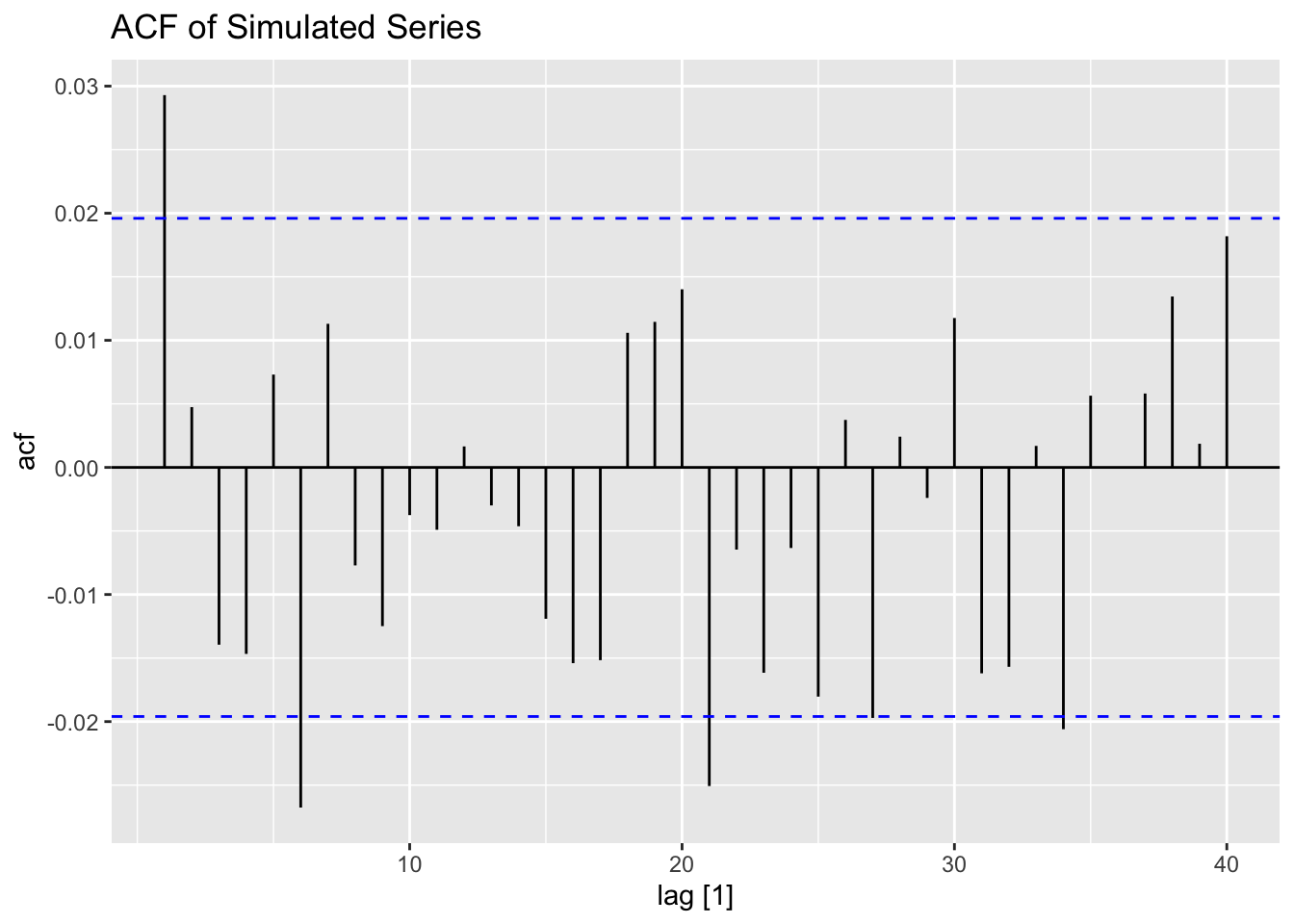

Generalized Autoregressive Conditional Heteroskedastic models relax the assumption of a constant variance for the residuals. In the code chunk below, I demonstrate a simulated GARCH Model. The garch() function, used to create these models, is part of the tseries package as GARCH models are not included in fable.

## Registered S3 method overwritten by 'quantmod':

## method from

## as.zoo.data.frame zooset.seed(1)

alpha0 <- 0.1

alpha1 <- 0.4

beta1 <- 0.2

w <- rnorm(10000)

a <- rep(0, 10000)

h <- rep(0, 10000)

for (i in 2:10000) {

h[i] <- alpha0 + alpha1 * (a[i - 1]^2) + beta1 * h[i - 1] # this is the data generating process

a[i] <- w[i] * sqrt(h[i])

}

ACF(ts(a) |> as_tsibble()) |>

autoplot() +

labs(title = "ACF of Simulated Series")## Response variable not specified, automatically selected `var = value`

## Response variable not specified, automatically selected `var = value`

##

## Call:

## garch(x = a, grad = "numerical", trace = FALSE)

##

## Coefficient(s):

## a0 a1 b1

## 0.09876 0.36659 0.24415## 2.5 % 97.5 %

## a0 0.0882393 0.1092903

## a1 0.3307897 0.4023932

## b1 0.1928344 0.29546606.2.1 S&P500 Example

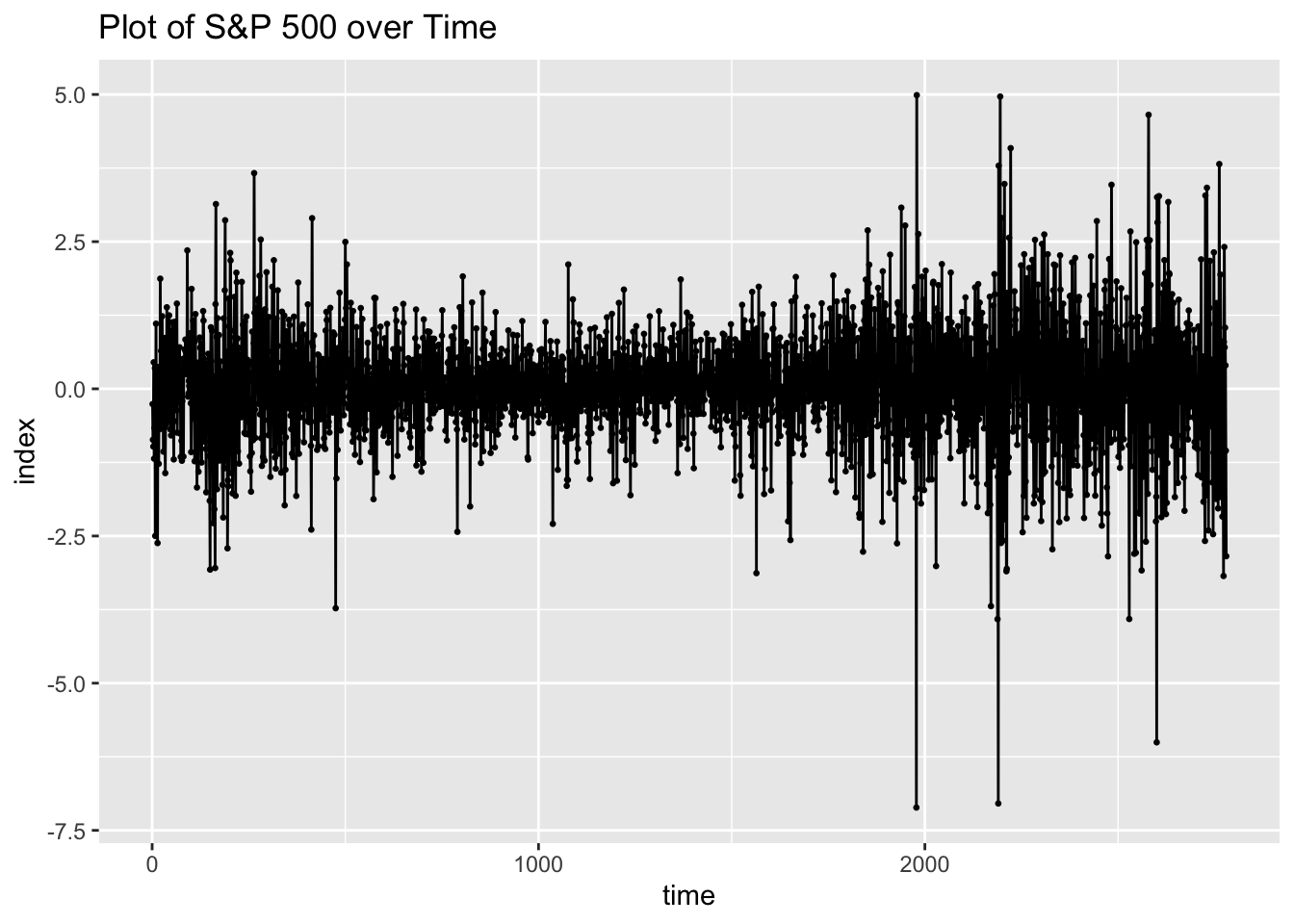

In this example we will be using the daily S&P 500 index data from 1990 to 1999 included in the MASS package. Note the data only includes trading days not all days. I read in the datato a tibble, create a periodic time variable, and make that variable the index of a tsibble containing the data. I also create a version of the data as a time series, as the functions for garch models are not part of fable and require a time series object instead of a tsibble.

#library(MASS)

(sp <- tibble(sp500 = MASS::SP500) |>

mutate(time = row_number()) |>

as_tsibble(index = time))## # A tsibble: 2,780 x 2 [1]

## sp500 time

## <dbl> <int>

## 1 -0.259 1

## 2 -0.865 2

## 3 -0.980 3

## 4 0.450 4

## 5 -1.19 5

## 6 -0.663 6

## 7 0.351 7

## 8 -2.50 8

## 9 -0.866 9

## 10 1.11 10

## # ℹ 2,770 more rowsNext, I plot the S&P 500 data. The data has 2,780 observations, so the plot is very overcrowded with points.

sp |>

ggplot(aes(x = time, y = sp500)) +

geom_point(size = 0.5) +

geom_line() +

labs(title = "Plot of S&P 500 over Time",

y = "index")

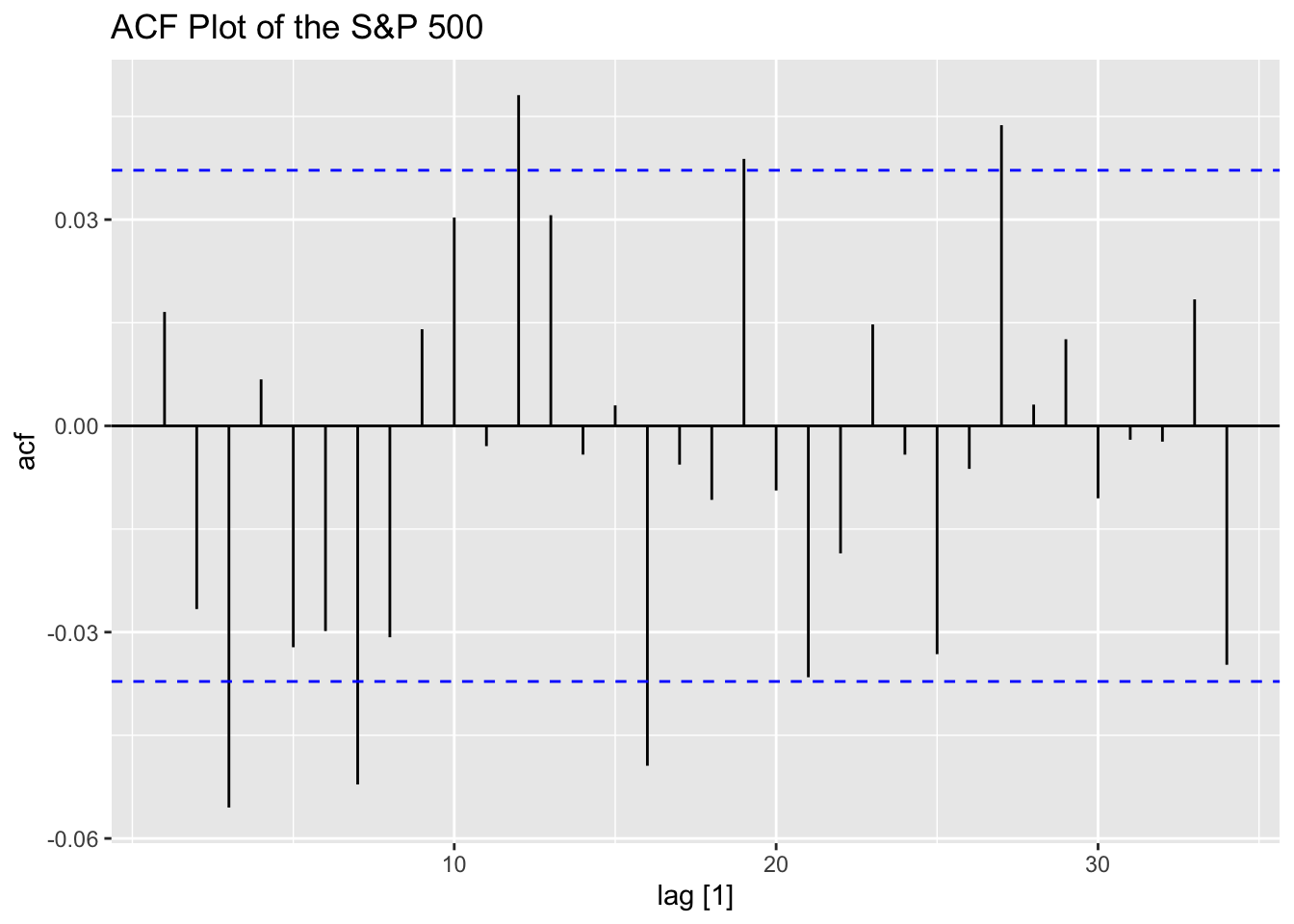

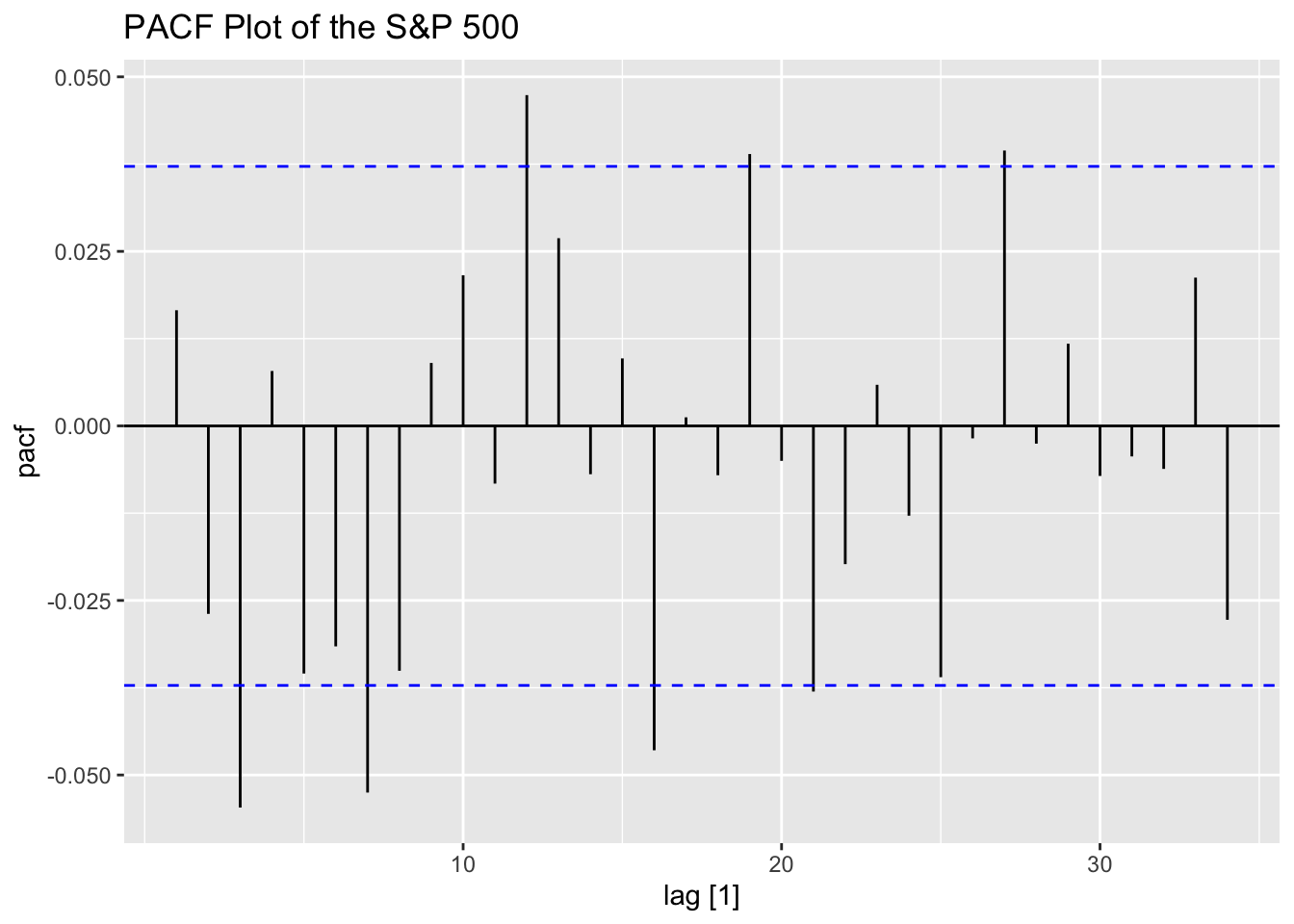

Looking at the ACF and PACF of the data, the data clearly has lingering autocorrelation.

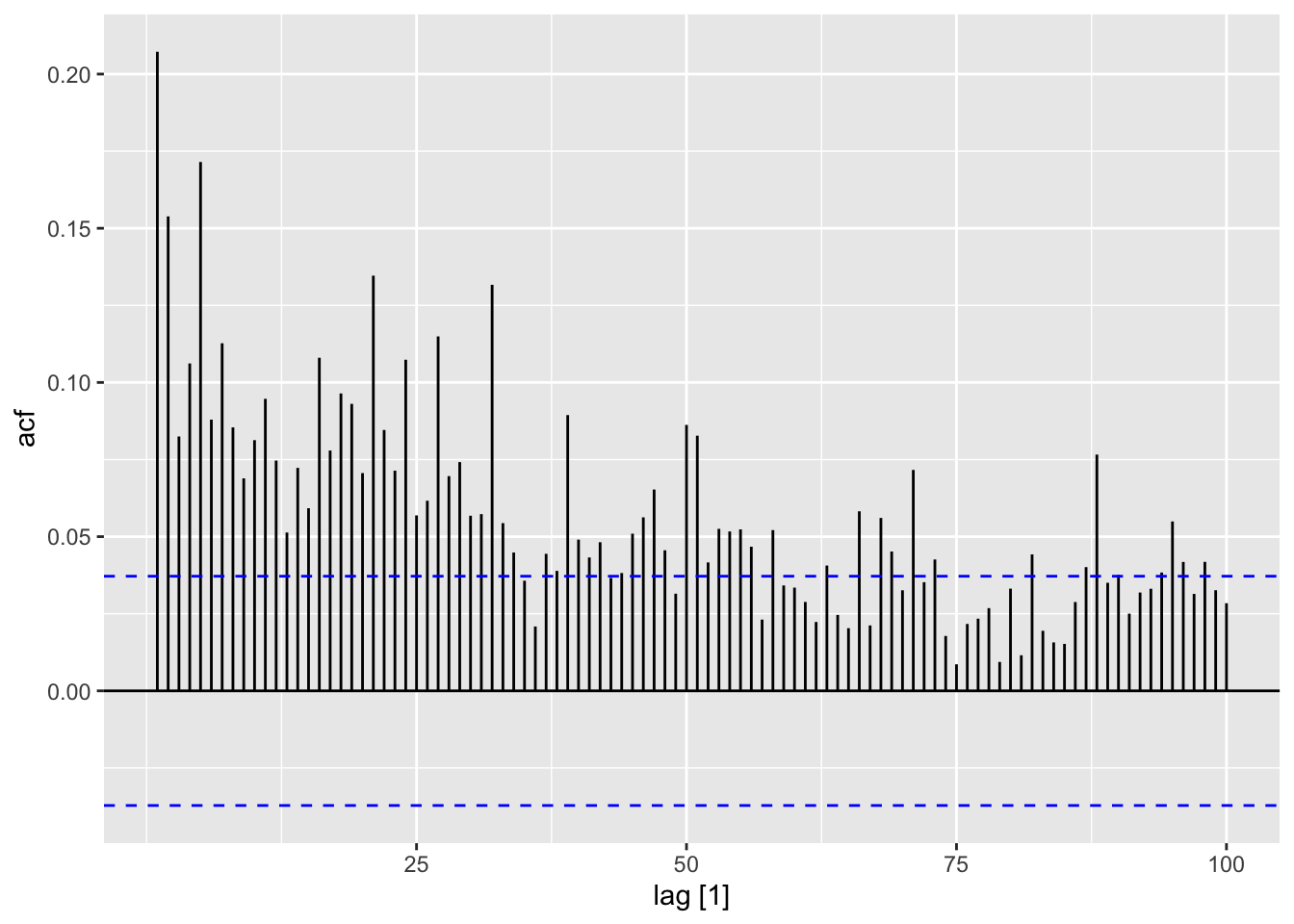

Next, I take the ACF of the squared residuals of the mean.

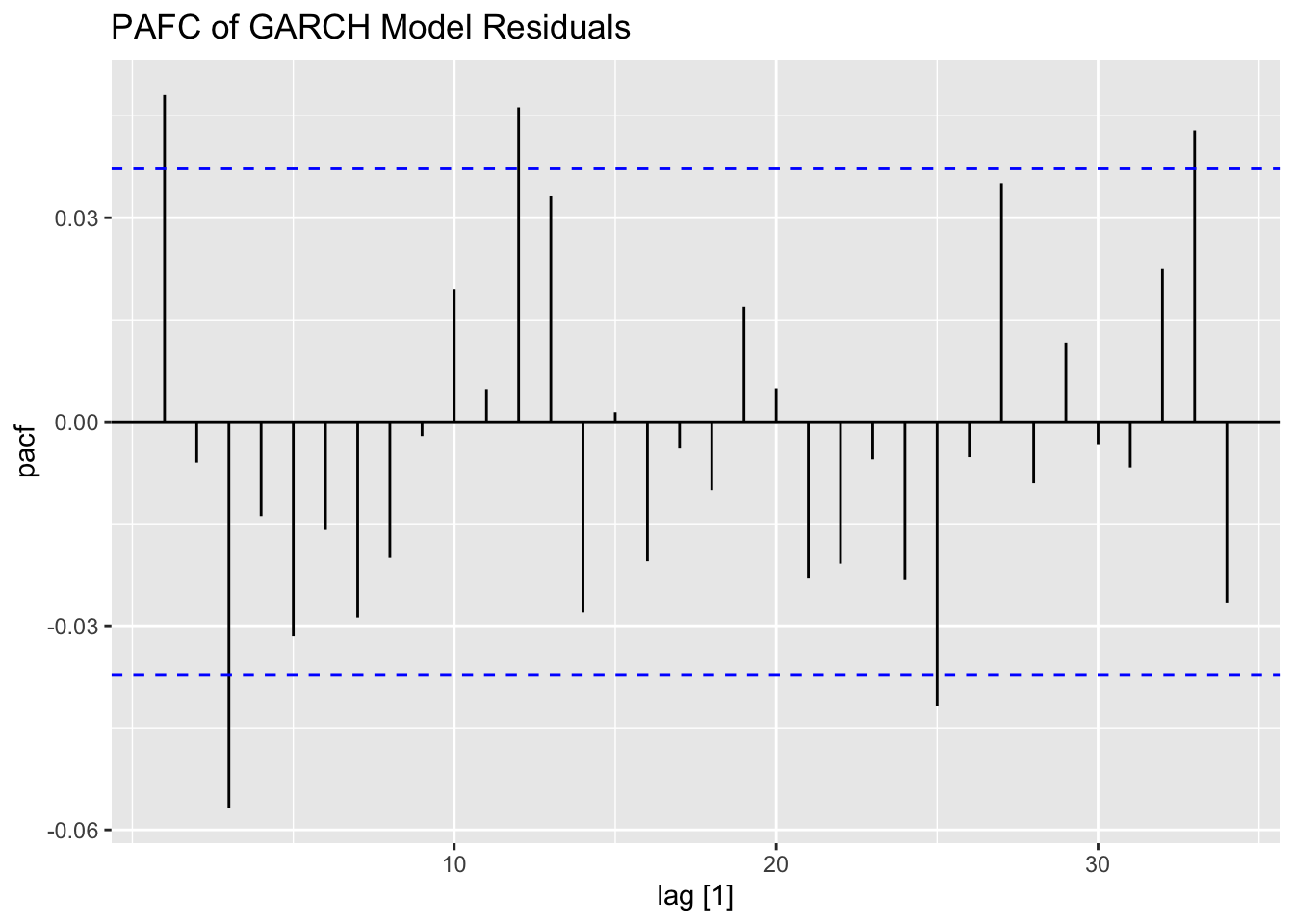

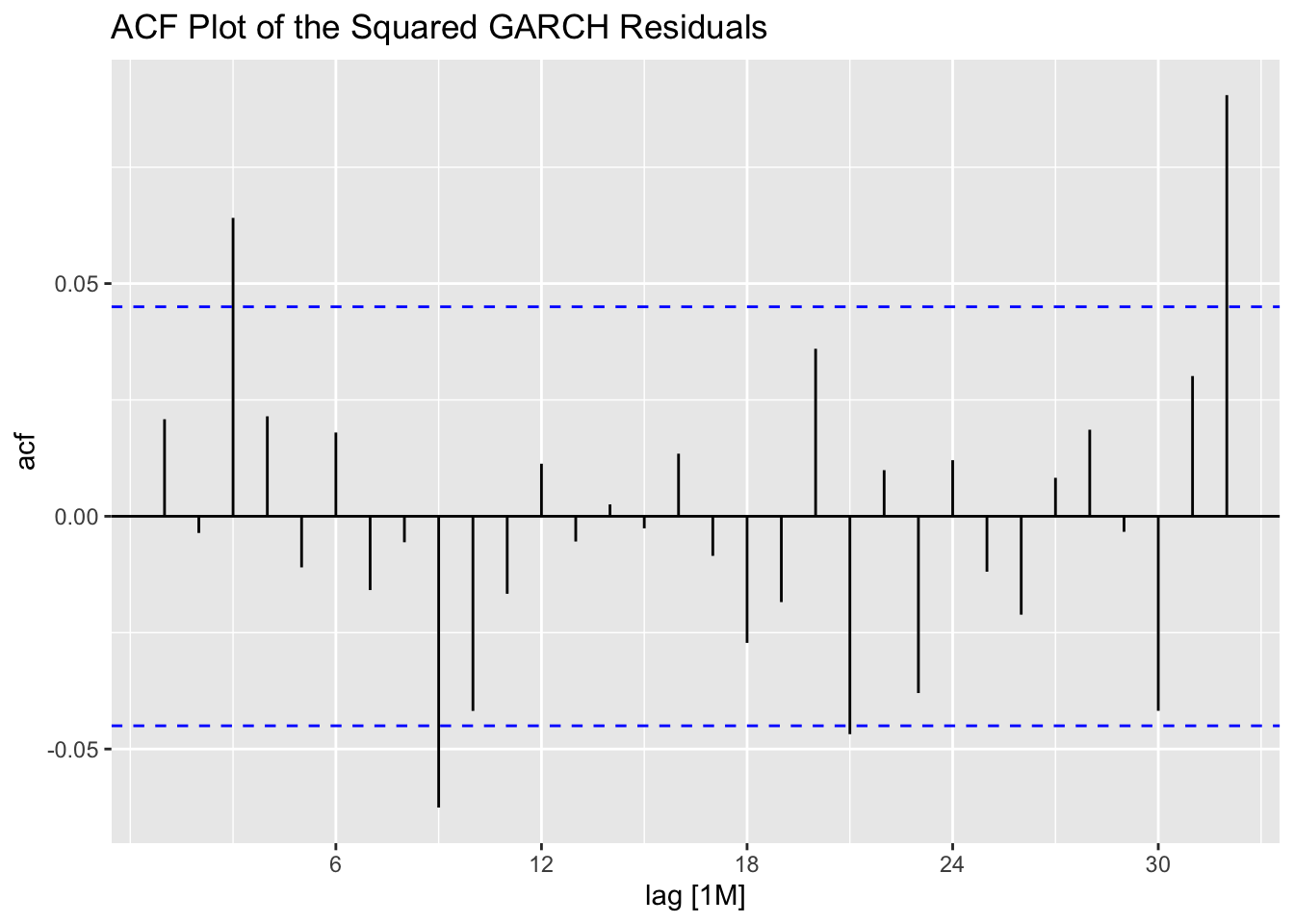

To fit a GARCH model to the data I use the garch() function. I then take the residuals and fitted values and make a tsibble that can be used with plot_residuals() to analyze the residuals. I additionally create an ACF plot of the square of the residuals.

##

## Call:

## garch(x = sp500, trace = F)

##

## Coefficient(s):

## a0 a1 b1

## 0.004292 0.050054 0.946773(sp.garch.resid <- tibble(.model = "garch",

.resid = as.vector(sp.garch[["residuals"]]),

.fitted = as.vector(sp.garch[["fitted.values"]][,1])) |>

mutate(time = row_number()) |>

filter(time != 1) |>

as_tsibble(index = time))## # A tsibble: 2,779 x 4 [1]

## .model .resid .fitted time

## <chr> <dbl> <dbl> <int>

## 1 garch -0.762 1.14 2

## 2 garch -0.873 1.12 3

## 3 garch 0.403 1.12 4

## 4 garch -1.08 1.09 5

## 5 garch -0.604 1.10 6

## 6 garch 0.324 1.08 7

## 7 garch -2.36 1.06 8

## 8 garch -0.739 1.17 9

## 9 garch 0.955 1.16 10

## 10 garch -0.855 1.16 11

## # ℹ 2,769 more rows## # A tibble: 1 × 2

## lb_stat lb_pvalue

## <dbl> <dbl>

## 1 6.42 0.0113

## # A tibble: 1 × 2

## kpss_stat kpss_pvalue

## <dbl> <dbl>

## 1 0.184 0.1

## NULL

6.2.2 Climate Series Example

For this example, we will be using the data from stemp.csv. This data contains monthly observations of temperature from 1850 to 2007 for the southern hemisphere. The data is from the database maintained by the University of East Anglia Climatic Research Unit. In the code chunk below, I read in the data, create an appropriate time variable, and declare the data as a tsibble.

(stemp <- read_csv("data/stemp.csv") |>

pivot_longer(-year, names_to = "month", values_to = "anomaly") |>

mutate(time = yearmonth(str_c(year, "-", month))) |>

select(time, anomaly) |>

as_tsibble(index = time))## Rows: 158 Columns: 13

## ── Column specification ───────────────────────────────────────

## Delimiter: ","

## dbl (13): year, jan, feb, mar, apr, may, jun, jul, aug, sep, oct, nov, dec

##

## ℹ Use `spec()` to retrieve the full column specification for this data.

## ℹ Specify the column types or set `show_col_types = FALSE` to quiet this message.## # A tsibble: 1,896 x 2 [1M]

## time anomaly

## <mth> <dbl>

## 1 1850 Jan -0.625

## 2 1850 Feb -0.598

## 3 1850 Mar -0.841

## 4 1850 Apr -0.632

## 5 1850 May -0.326

## 6 1850 Jun -0.528

## 7 1850 Jul -0.296

## 8 1850 Aug -0.503

## 9 1850 Sep -0.602

## 10 1850 Oct -0.42

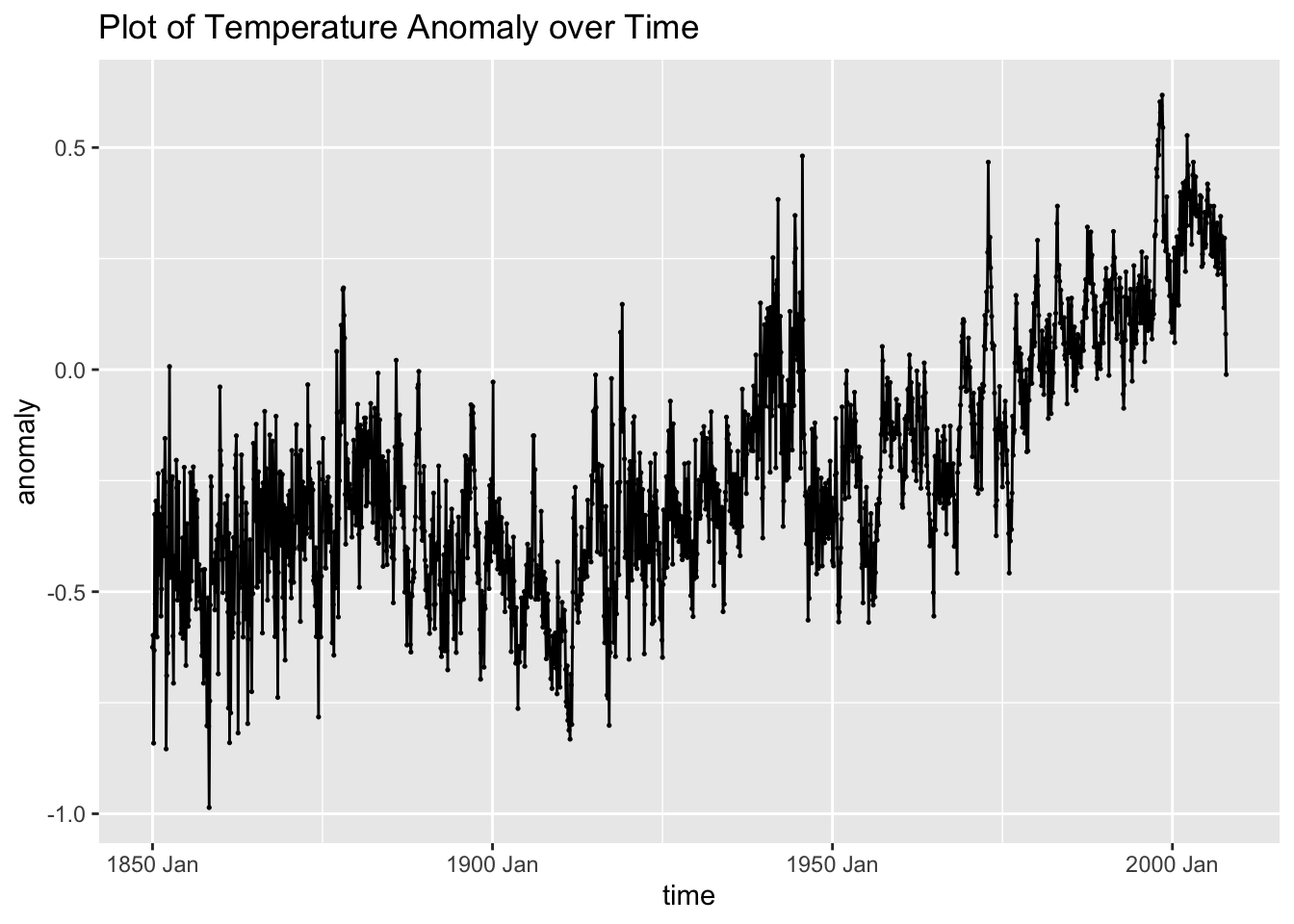

## # ℹ 1,886 more rowsAs always the first step is to plot the new time series we are working with. The data appears to be very volatile at first glance. It also appears to have a slight upward trend over time.

stemp |>

ggplot(aes(x = time, y = anomaly)) +

geom_point(size = 0.25) +

geom_line() +

labs(title = "Plot of Temperature Anomaly over Time")

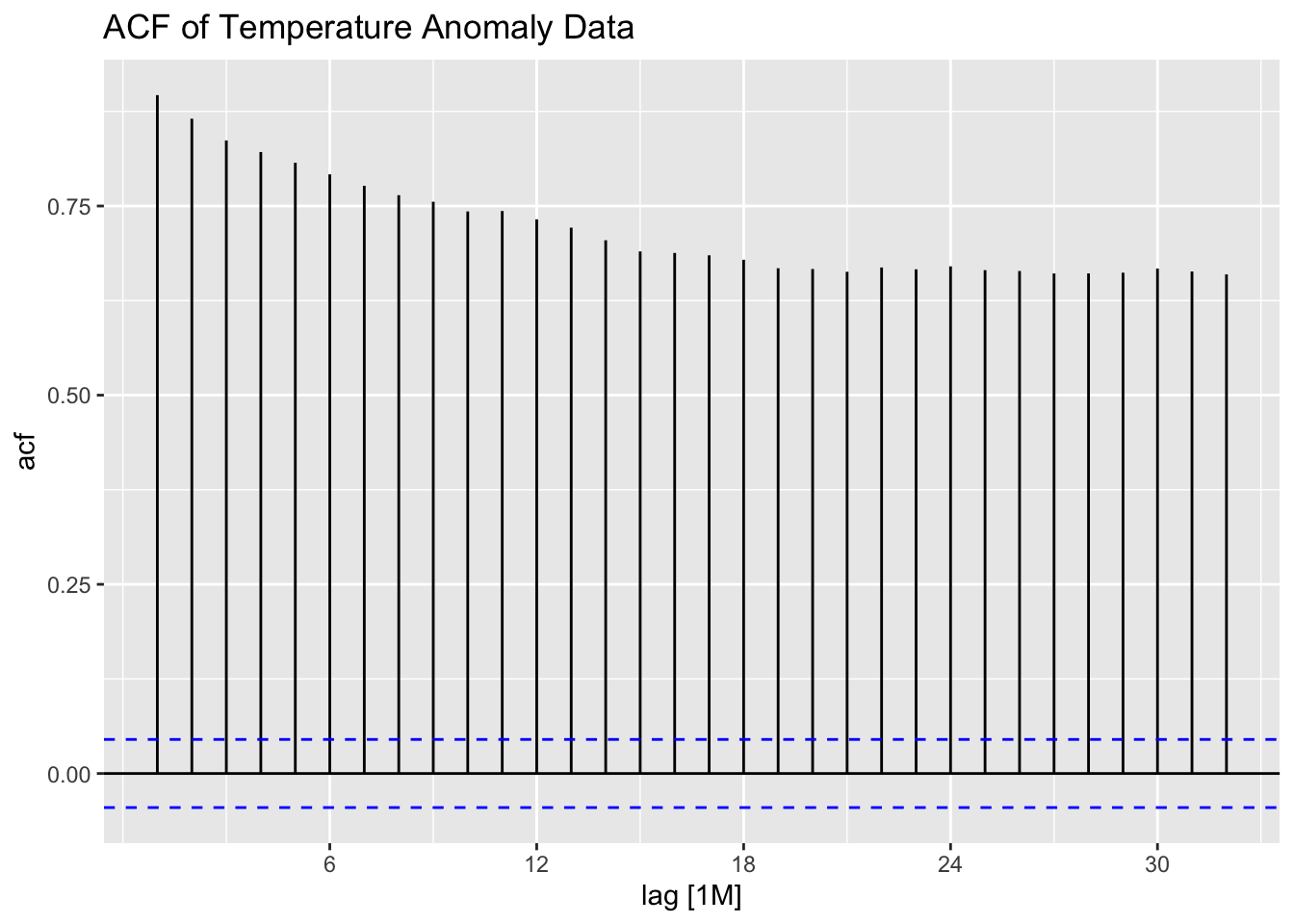

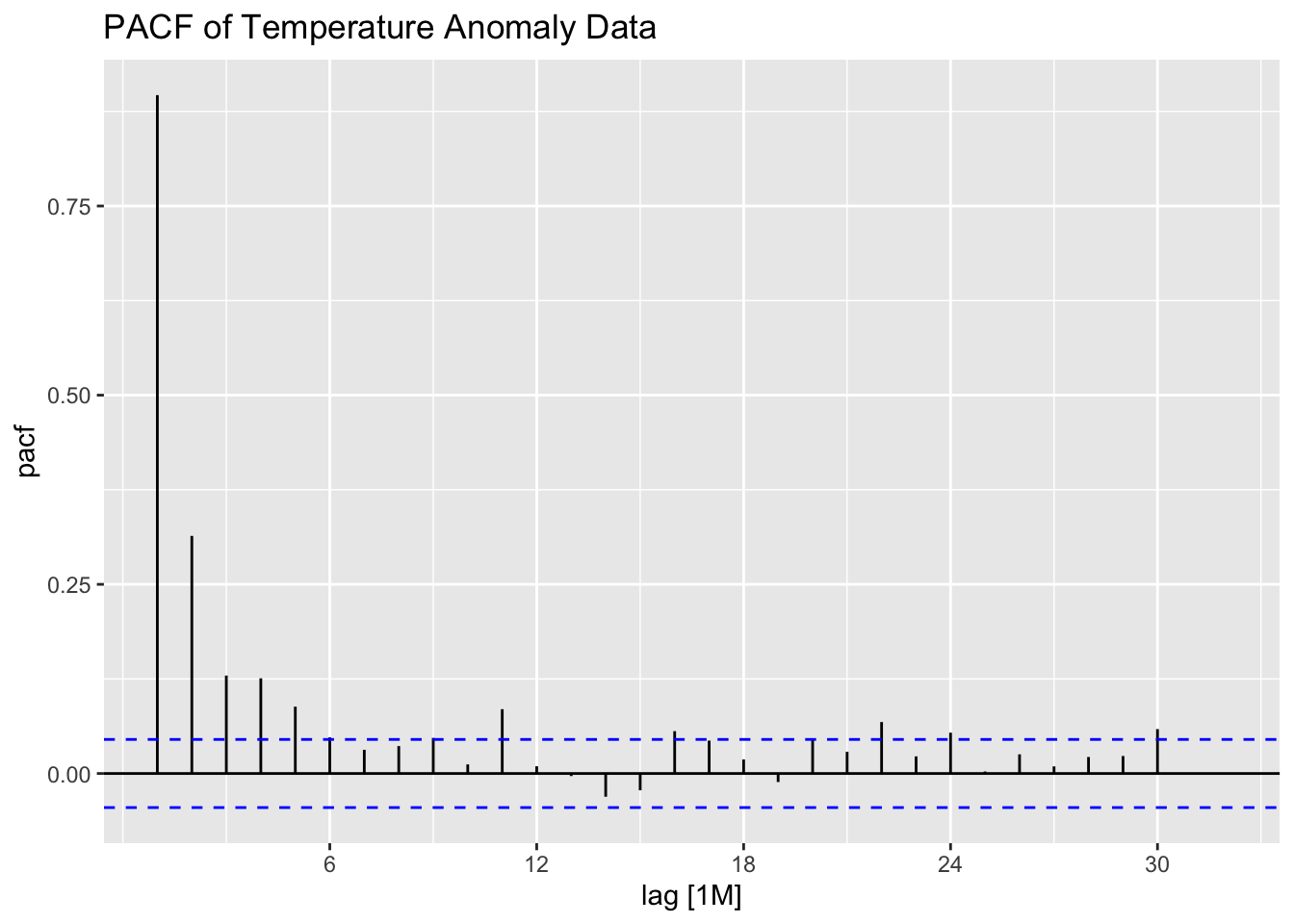

Examining the ACF and PACF of the data, it appears to have very high levels of lingering autocorrelation. This suggests that the data could benefit from differencing.

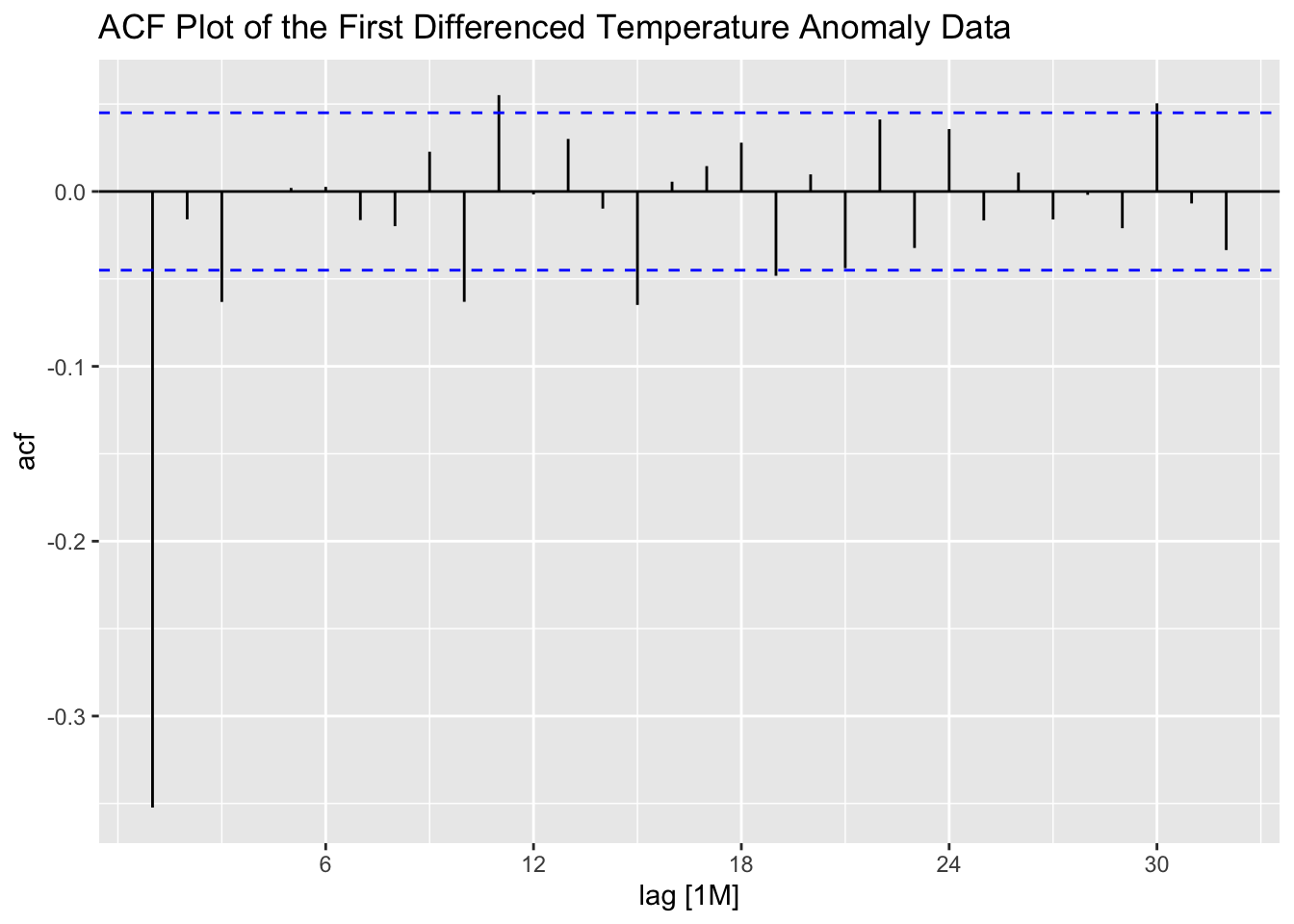

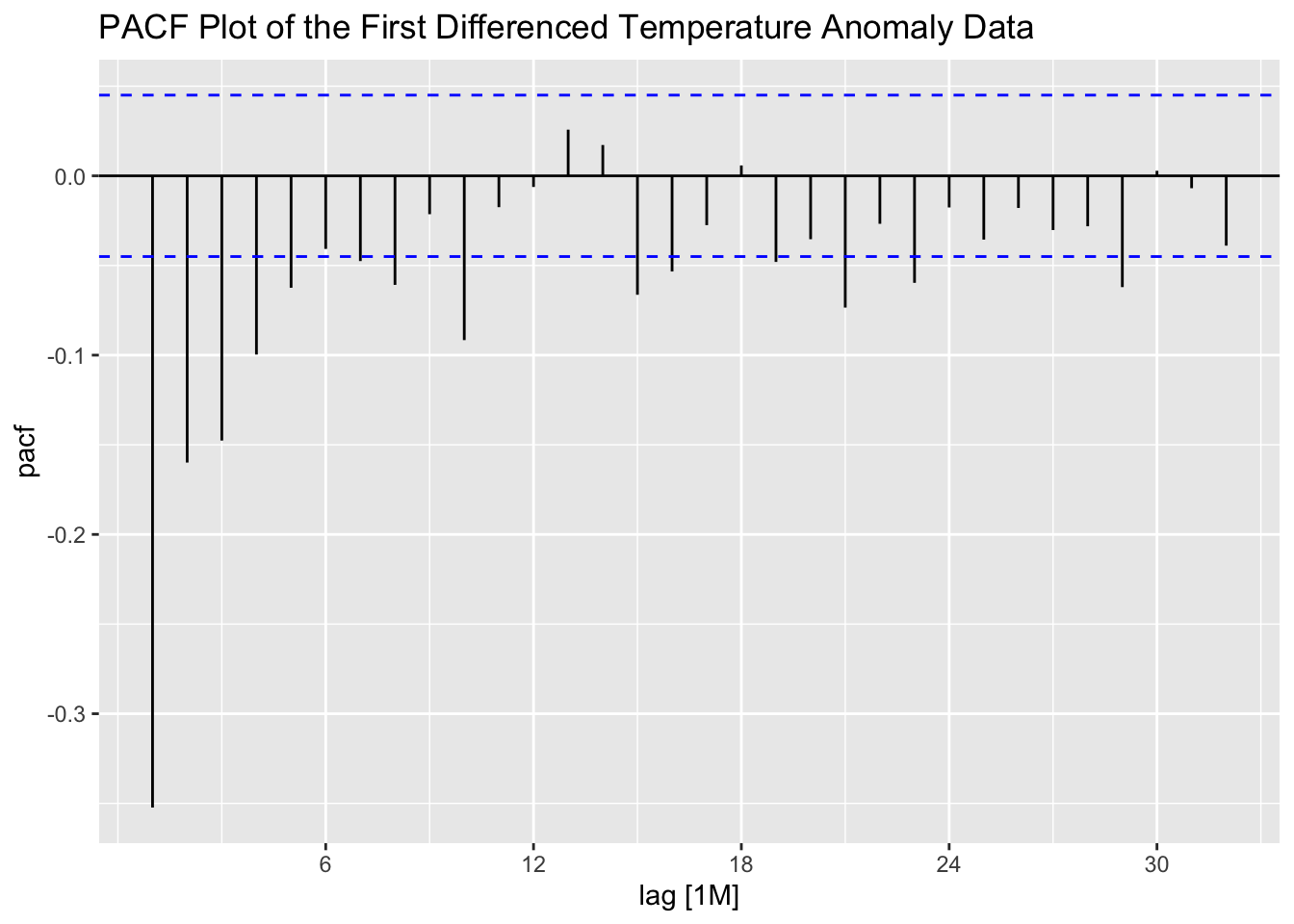

The ACF and PACF of the first differenced series appear to be better than the untreated series, but still show lingering levels of autocorrelation. This suggests that second differencing may improve the ACF and PACF.

stemp |>

ACF(difference(anomaly)) |>

autoplot() +

labs(title = "ACF Plot of the First Differenced Temperature Anomaly Data")

stemp |>

PACF(difference(anomaly)) |>

autoplot() +

labs(title = "PACF Plot of the First Differenced Temperature Anomaly Data")

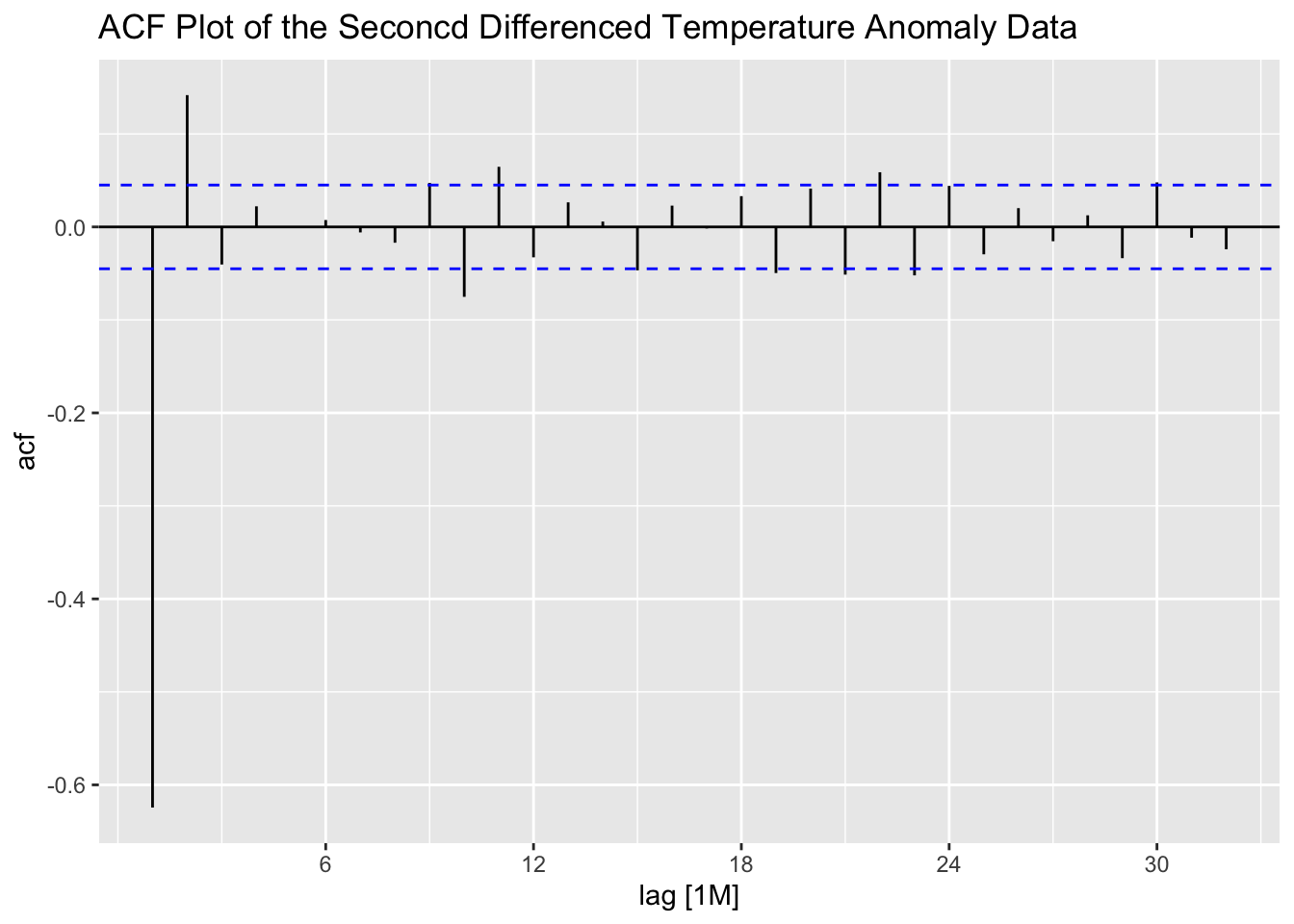

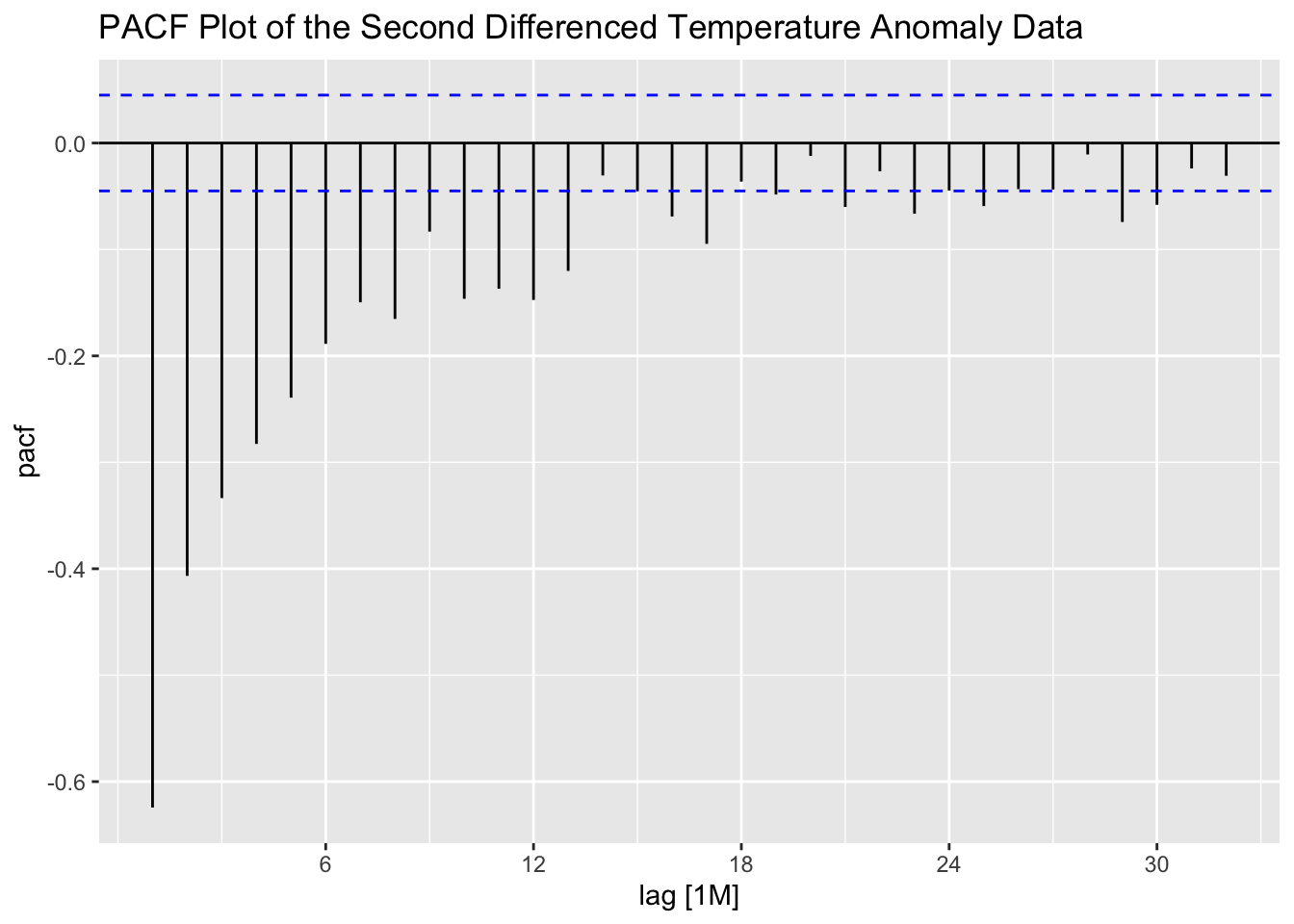

Second differencing the data appears to lead to a higher level of autocorrelation shown in the PACF, suggesting that simply first differencing the data is the best option.

stemp |>

ACF(difference(difference(anomaly, lag = 1), lag = 1)) |>

autoplot() +

labs(title = "ACF Plot of the Seconcd Differenced Temperature Anomaly Data")

stemp |>

PACF(difference(difference(anomaly, lag = 1), lag = 1)) |>

autoplot() +

labs(title = "PACF Plot of the Second Differenced Temperature Anomaly Data")

The next step is to fit an ARIMA model to the data. Below, I create a model object that contains an ARIMA(3,1,1)(2,0,0)[12] model, an ARIMA(1,1,2)(2,0,1)[12] model, and an ARIMA(1,1,2)(1,0,1)[12] model. The first model was selected as the best model by the ARIMA function through minimizing the AICc.

stemp.fit <- stemp |>

model(arima_311_200 = ARIMA(anomaly, stepwise = FALSE),

arima_112_201 = ARIMA(anomaly ~ 0 + pdq(1,1,2) + PDQ(2,0,1)),

arima_112_101 = ARIMA(anomaly ~ 0 + pdq(1,1,2) + PDQ(1,0,1)))Looking at the coefficients and their significance levels, the ARIMA(1,1,2)(1,0,1) model is the only model in which all coefficients are statistically significant. The ARIMA(3,1,1)(2,0,0) model has the lowest AICc, as expected, but performs slightly worse than the other models in measures of accuracy. The ARIMA(1,1,2)(1,0,1) model as the best one, as its measures of accuracy are close the others but all of its coefficients are significant.

| .model | term | estimate | std.error | statistic | p.value |

|---|---|---|---|---|---|

| arima_311_200 | ar1 | 0.491 | 0.024 | 20.347 | 0.000 |

| arima_311_200 | ar2 | 0.183 | 0.026 | 7.119 | 0.000 |

| arima_311_200 | ar3 | 0.066 | 0.024 | 2.772 | 0.006 |

| arima_311_200 | ma1 | -0.978 | 0.007 | -136.565 | 0.000 |

| arima_311_200 | sar1 | 0.039 | 0.024 | 1.644 | 0.100 |

| arima_311_200 | sar2 | 0.026 | 0.024 | 1.092 | 0.275 |

| arima_311_200 | constant | 0.000 | 0.000 | 1.715 | 0.087 |

| arima_112_201 | ar1 | 0.872 | 0.021 | 42.184 | 0.000 |

| arima_112_201 | ma1 | -1.380 | 0.034 | -40.115 | 0.000 |

| arima_112_201 | ma2 | 0.389 | 0.032 | 11.982 | 0.000 |

| arima_112_201 | sar1 | 0.931 | 0.037 | 24.915 | 0.000 |

| arima_112_201 | sar2 | 0.025 | 0.025 | 0.971 | 0.332 |

| arima_112_201 | sma1 | -0.910 | 0.030 | -30.136 | 0.000 |

| arima_112_101 | ar1 | 0.871 | 0.021 | 42.438 | 0.000 |

| arima_112_101 | ma1 | -1.378 | 0.034 | -40.370 | 0.000 |

| arima_112_101 | ma2 | 0.388 | 0.032 | 11.997 | 0.000 |

| arima_112_101 | sar1 | 0.960 | 0.018 | 52.770 | 0.000 |

| arima_112_101 | sma1 | -0.919 | 0.026 | -35.458 | 0.000 |

| .model | sigma2 | log_lik | AIC | AICc | BIC |

|---|---|---|---|---|---|

| arima_311_200 | 0.012 | 1500.008 | -2984.016 | -2983.940 | -2939.640 |

| arima_112_201 | 0.012 | 1518.600 | -3023.200 | -3023.140 | -2984.371 |

| arima_112_101 | 0.012 | 1518.107 | -3024.213 | -3024.169 | -2990.932 |

| .model | .type | ME | RMSE | MAE | MPE | MAPE | MASE | RMSSE | ACF1 |

|---|---|---|---|---|---|---|---|---|---|

| arima_311_200 | Training | 0.000 | 0.110 | 0.083 | Inf | Inf | 0.556 | 0.566 | -0.005 |

| arima_112_201 | Training | 0.003 | 0.108 | 0.082 | Inf | Inf | 0.550 | 0.560 | 0.009 |

| arima_112_101 | Training | 0.003 | 0.109 | 0.082 | Inf | Inf | 0.550 | 0.560 | 0.007 |

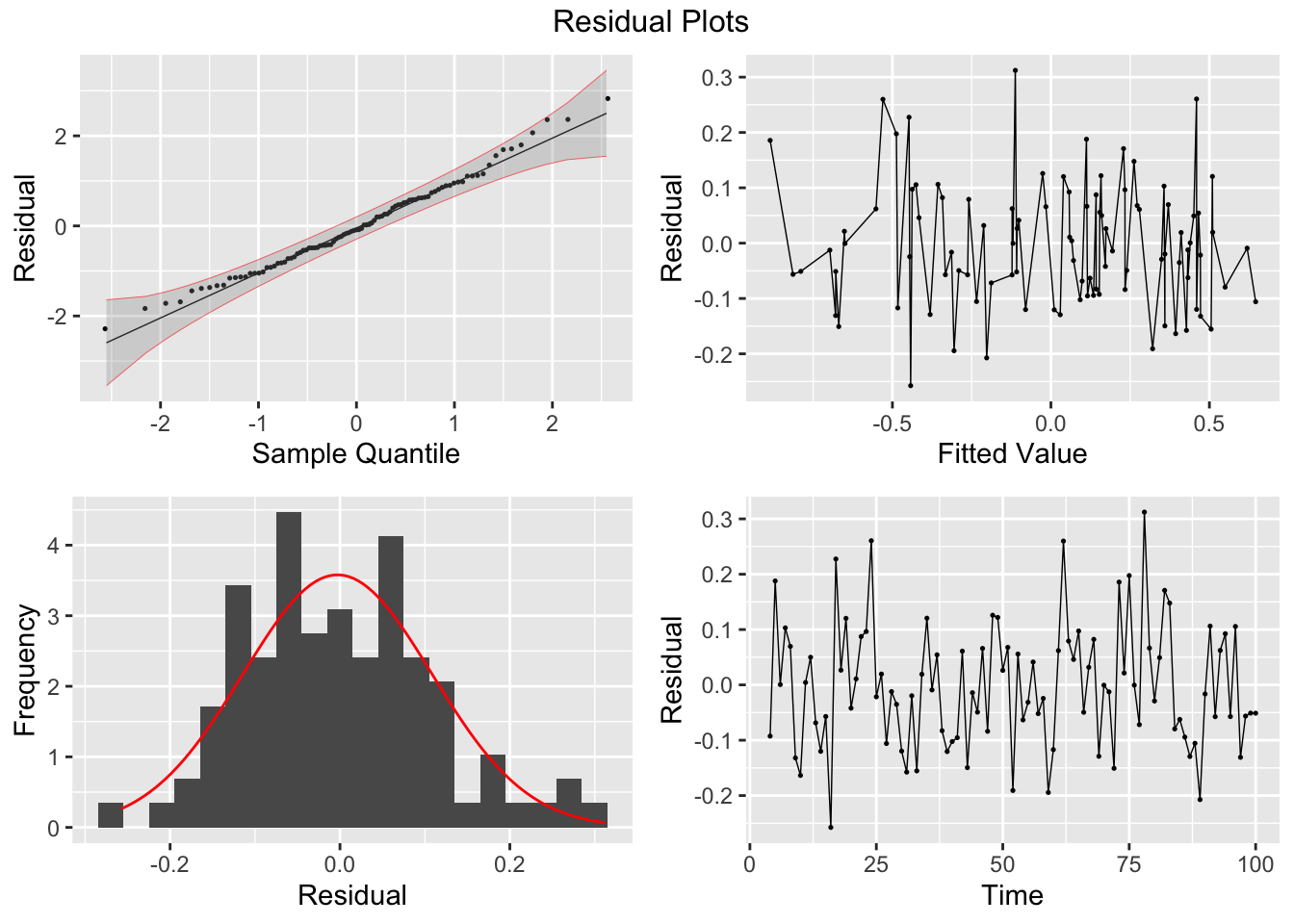

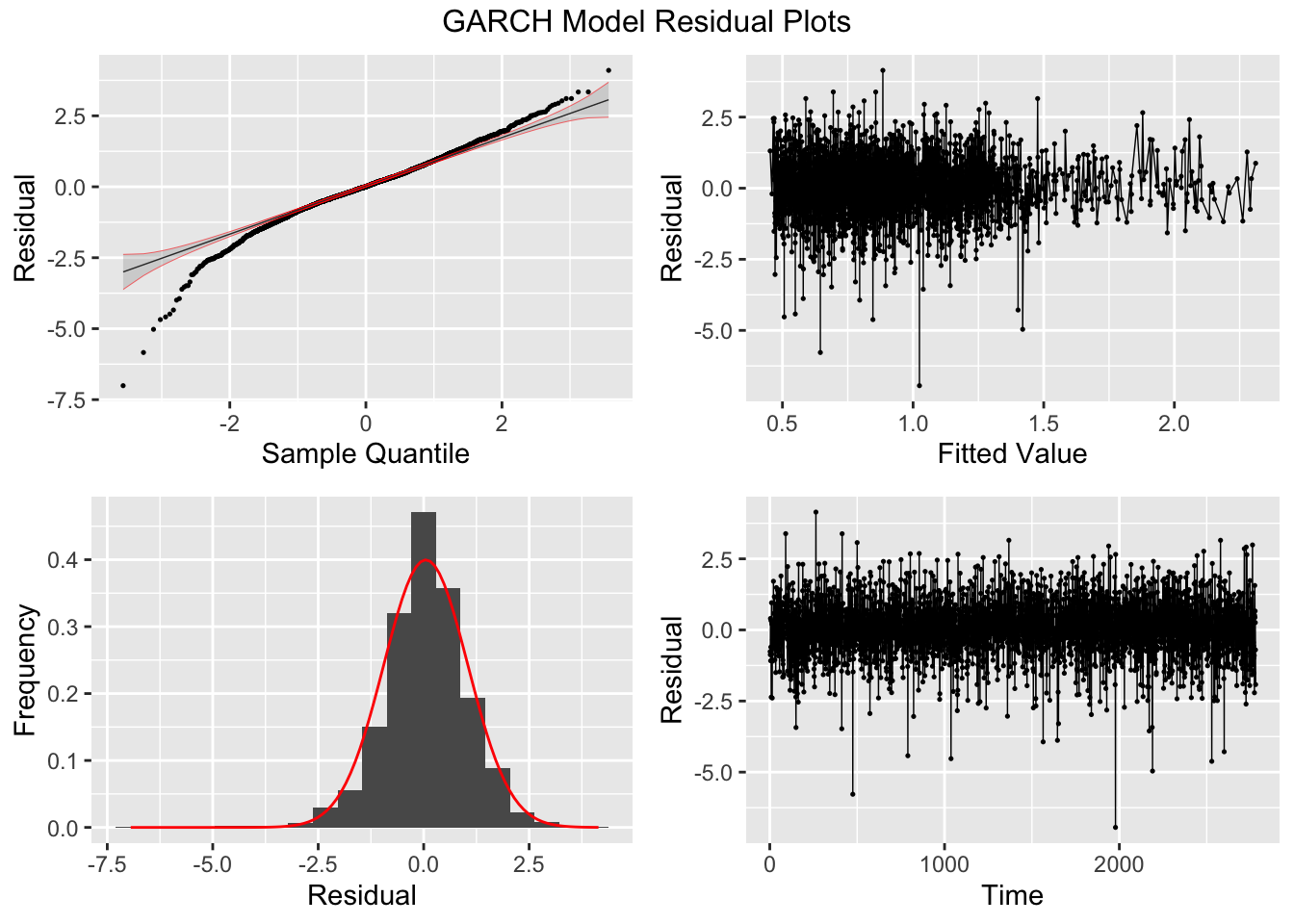

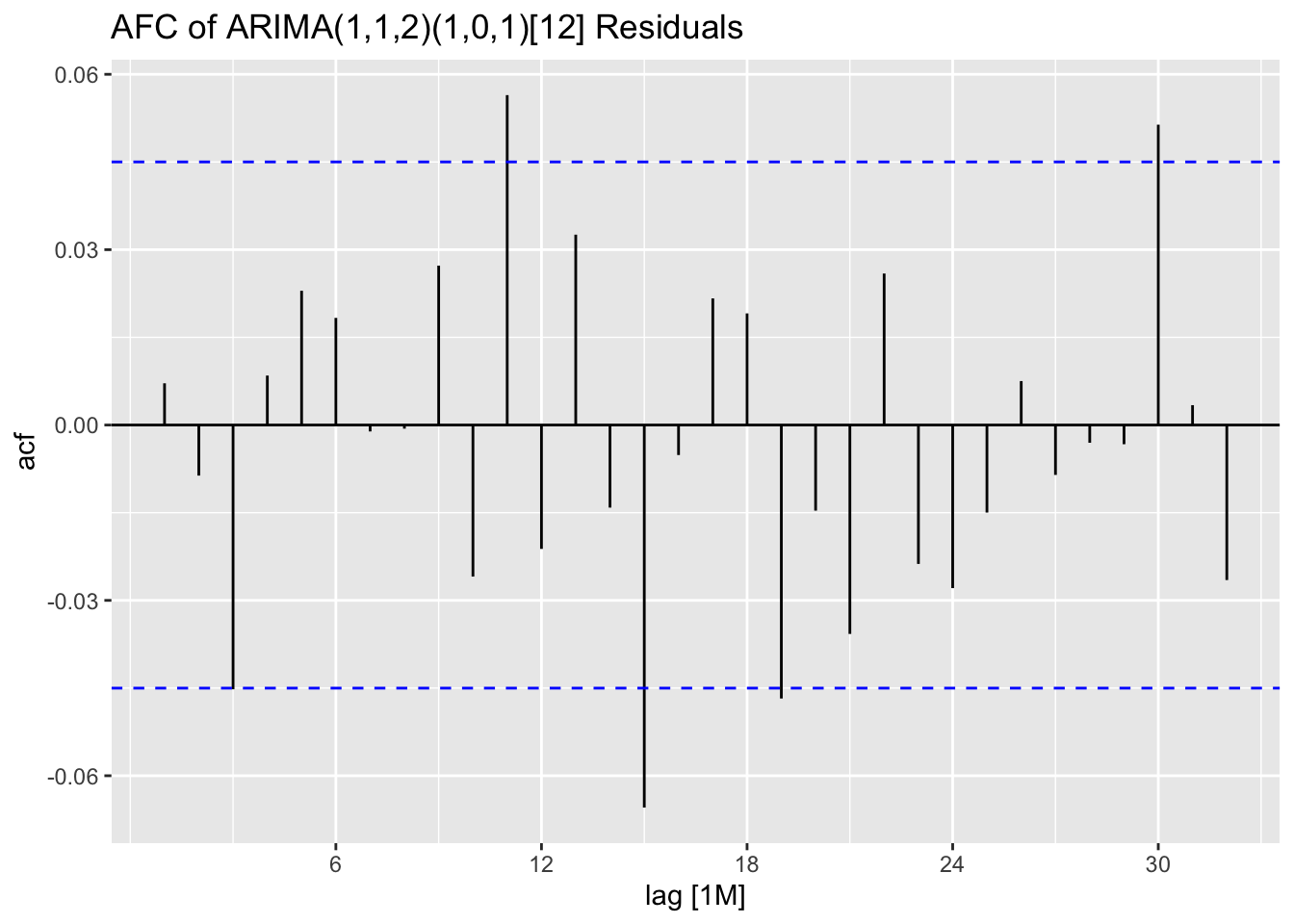

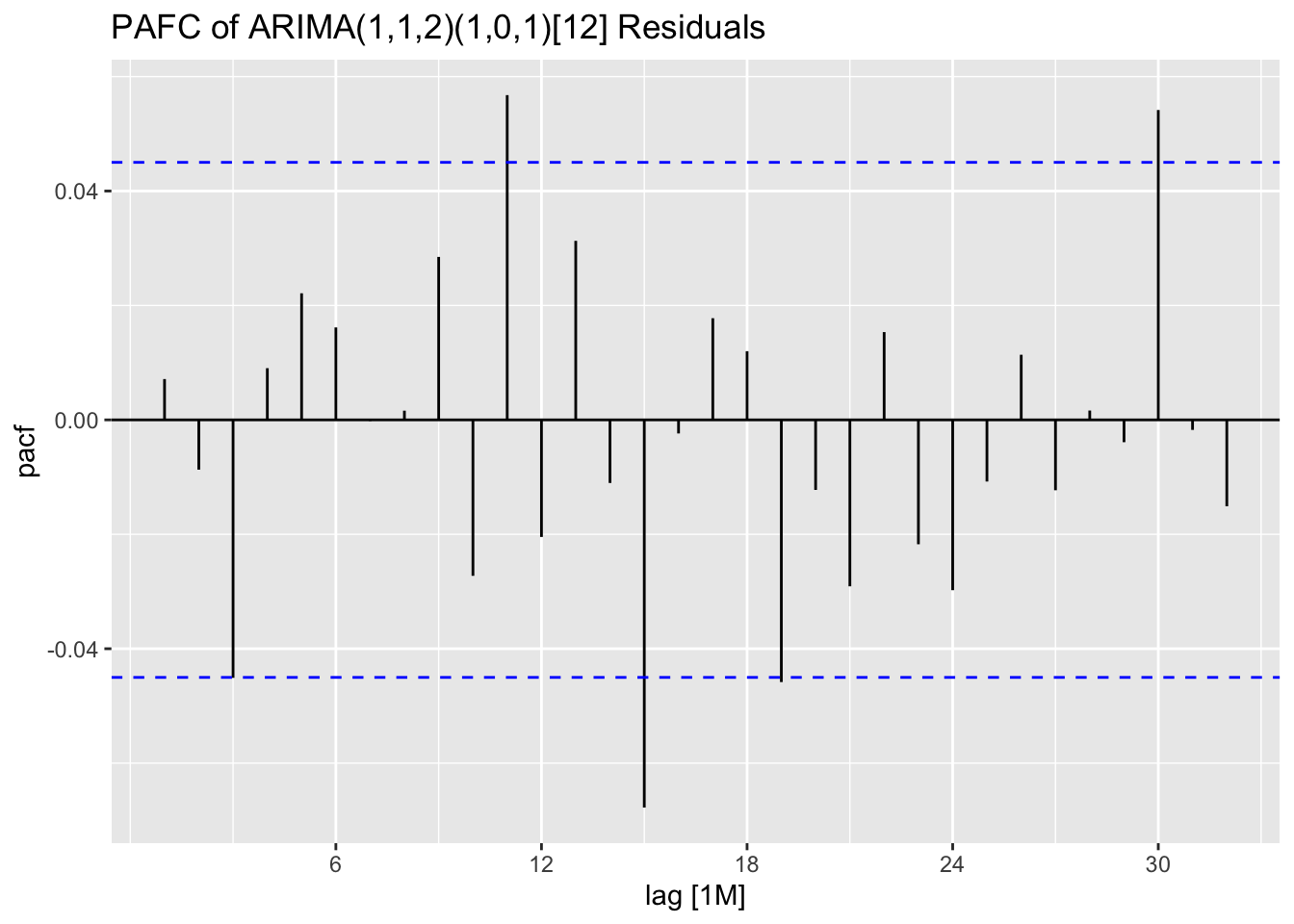

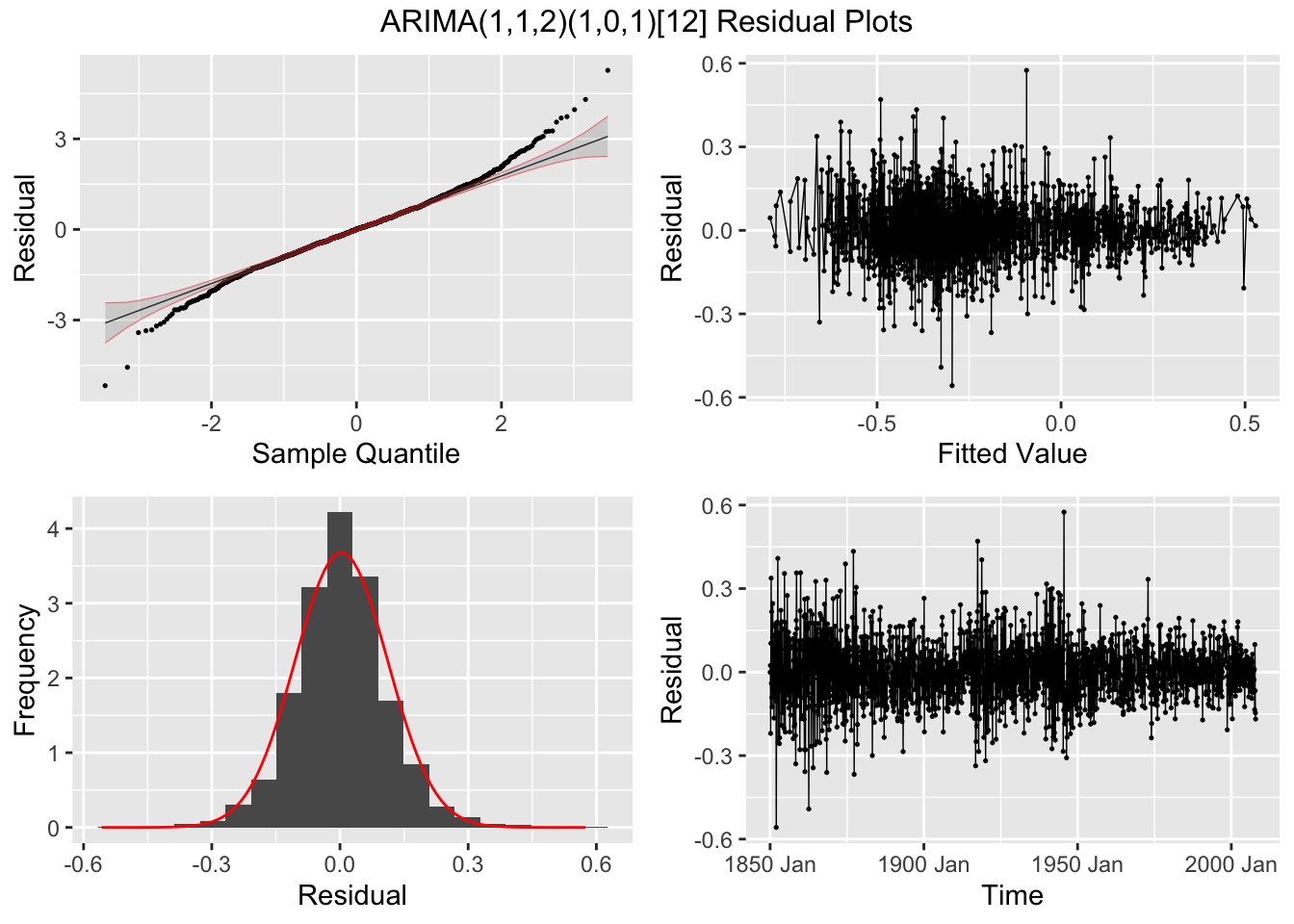

In the code chunk below, I use plot_residuals() to analyze the residuals of the ARIMA(1,1,2)(1,0,1) model. I additionally plot the ACF of the squared residuals. There appears to be lingering autocorrelation shown in all ACF and PACF plots, as well as the results of the Ljung-Box test.

stemp.fit |> select(arima_112_101) |>

augment() |>

plot_residuals(title = "ARIMA(1,1,2)(1,0,1)[12]")## # A tibble: 1 × 3

## .model lb_stat lb_pvalue

## <chr> <dbl> <dbl>

## 1 arima_112_101 0.0966 0.756

## # A tibble: 1 × 3

## .model kpss_stat kpss_pvalue

## <chr> <dbl> <dbl>

## 1 arima_112_101 0.0817 0.1

## NULL

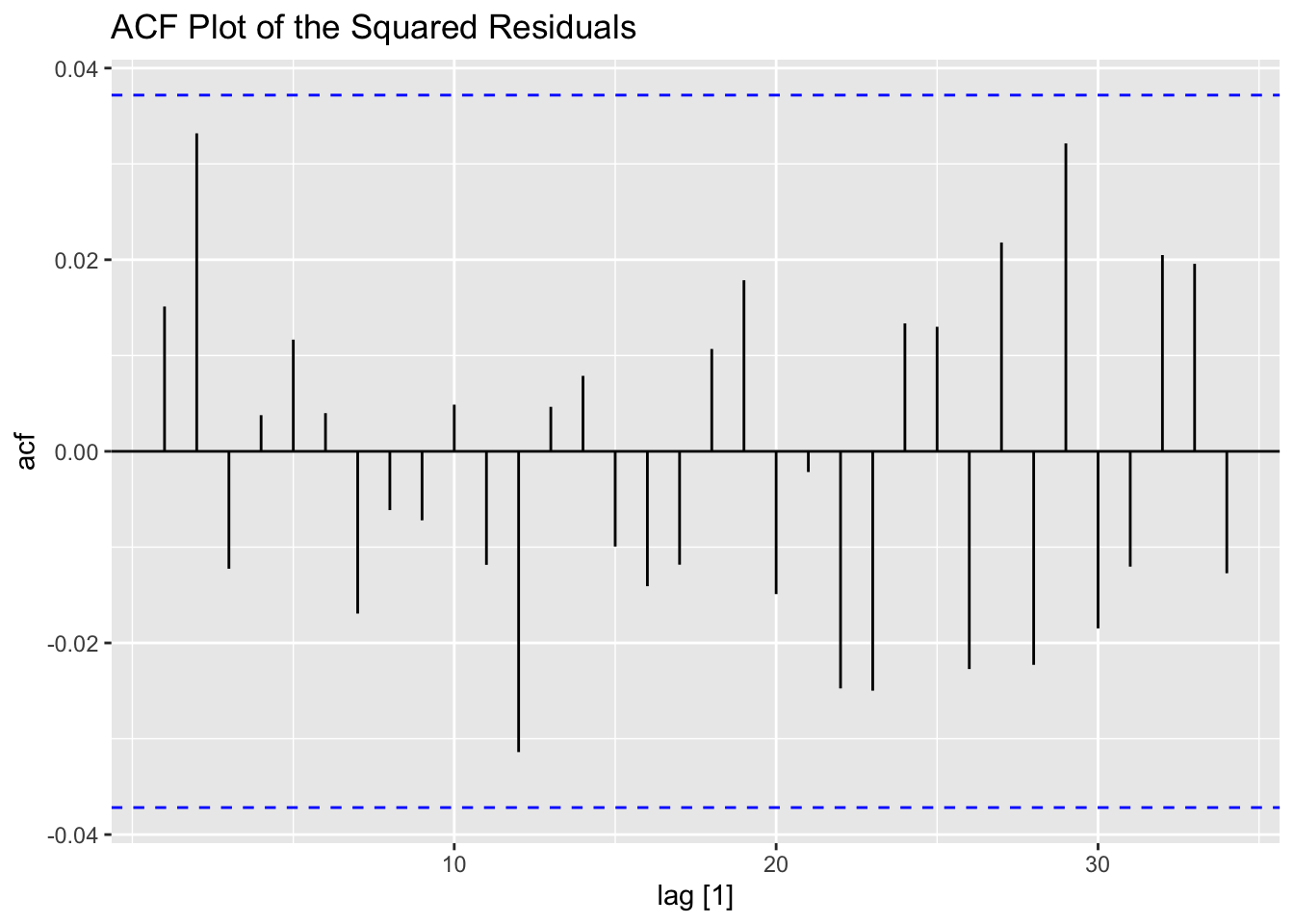

To extract the signal remaining in the residuals, we will model the residuals from the ARIMA(1,1,2)(1,0,1) model using a GARCH model. I extract the residuals using augment(), isolate the residuals from the correct model and time variable using select(), and then declare the residuals as a time series. I use that time series with garch() to model the residuals. After creating a tsibble with the residuals from the GARCH model, I then plot the ACF of the residuals as well as the ACF of the squared residuals.

## Jan Feb Mar Apr May

## 1850 -6.249996e-04 2.371139e-02 -2.202986e-01 1.034806e-01 3.376496e-01

## 1851 -7.921286e-02 1.075650e-01 3.562421e-02 -1.651901e-01 -2.575468e-02

## 1852 -5.579254e-01 -1.049315e-01 2.135839e-02 -2.368521e-02 1.796631e-01

## 1853 -2.569663e-01 -2.360036e-01 1.754709e-01 2.204964e-02 -3.953763e-02

## 1854 5.607779e-03 2.179731e-02 -1.298934e-01 2.208230e-03 -8.327914e-02

## 1855 1.780979e-01 1.467217e-01 -8.218697e-02 -1.075665e-01 -6.055371e-02

## 1856 1.434646e-01 -1.286283e-01 6.662866e-03 -5.156824e-05 1.093022e-01

## 1857 -4.136388e-02 -4.220435e-02 -1.914767e-02 -1.175166e-01 -6.138619e-02

## 1858 -1.862869e-01 4.429881e-02 1.370896e-01 -2.278466e-01 -3.297510e-01

## 1859 2.784932e-02 4.553710e-02 -8.563235e-02 1.118908e-01 -4.303167e-02

## 1860 8.122025e-02 2.524295e-02 -1.675112e-01 -4.604969e-02 -9.227408e-02

## 1861 2.000339e-01 -1.695098e-01 -2.788304e-01 2.620318e-01 -3.576378e-01

## 1862 -6.963887e-02 9.638652e-02 2.652503e-01 1.599423e-01 1.566090e-01

## 1863 1.762760e-01 2.198194e-01 -3.979609e-02 8.500173e-02 -2.661335e-01

## 1864 -3.438521e-01 8.104439e-03 1.150818e-01 -2.381428e-02 1.751537e-01

## 1865 -4.435529e-03 4.874601e-02 1.396614e-01 1.550468e-01 -2.494128e-01

## 1866 1.183223e-01 5.911248e-03 -2.540134e-01 2.098659e-01 1.078431e-01

## 1867 1.500935e-01 -9.471380e-02 1.418054e-01 1.887801e-01 -2.187303e-02

## 1868 -1.587959e-01 1.454043e-01 3.300097e-01 -2.411915e-01 3.772227e-02

## 1869 -1.995598e-02 1.384398e-01 -2.074191e-01 1.022945e-01 -1.777391e-01

## 1870 1.426754e-01 -5.754211e-02 -6.274399e-02 1.199588e-01 -1.084536e-01

## 1871 8.088448e-02 1.648521e-01 1.645798e-01 -1.454833e-01 -1.586277e-02

## 1872 1.331942e-02 6.244337e-02 -1.079777e-01 3.429407e-02 1.020076e-01

## 1873 1.498924e-01 -2.886582e-02 -1.007057e-02 -1.368092e-01 6.491256e-02

## 1874 7.989006e-02 -1.885477e-01 5.150816e-02 -4.069838e-02 -8.814192e-02

## 1875 1.611447e-01 1.650289e-01 -5.909015e-02 2.082598e-02 4.754691e-02

## 1876 5.837252e-02 -2.728638e-02 1.320205e-02 1.988623e-02 -6.511381e-02

## 1877 8.641659e-02 4.336289e-01 8.865378e-02 3.100710e-02 -3.674392e-01

## 1878 3.046559e-01 1.599545e-01 7.110498e-02 2.019147e-02 -2.594228e-01

## 1879 1.176679e-02 -3.998623e-02 -1.088497e-02 -8.917120e-03 -3.820704e-02

## 1880 3.733262e-02 1.099930e-01 1.261094e-01 -6.412889e-02 -1.276212e-01

## 1881 -4.190029e-02 -2.761595e-02 1.068071e-01 4.967381e-02 1.007173e-01

## 1882 4.000605e-02 6.996134e-02 2.039962e-02 -4.565433e-02 -8.696748e-02

## 1883 1.790134e-01 6.539370e-02 1.378944e-01 -2.999864e-01 -7.774711e-03

## 1884 -3.855052e-02 6.965658e-02 5.451837e-02 3.280070e-03 -7.384592e-02

## 1885 -4.844375e-02 -1.175170e-01 -4.084322e-02 -6.287113e-02 3.685440e-02

## 1886 -7.617996e-02 -1.706227e-01 4.224460e-02 7.874914e-02 1.365448e-01

## 1887 3.872333e-02 -2.344524e-01 -3.384376e-02 -7.561455e-03 -6.036120e-02

## 1888 -1.298134e-01 3.877978e-02 -2.324675e-02 1.259235e-02 4.626008e-02

## 1889 1.639552e-01 9.620590e-02 9.055712e-02 -4.869316e-02 -6.892078e-02

## 1890 -1.154635e-01 -1.253736e-01 -1.416234e-01 -1.051391e-02 -8.077609e-02

## 1891 -4.630353e-02 9.268394e-03 6.217763e-02 -1.196781e-03 1.247560e-01

## 1892 8.751422e-03 1.656858e-01 -2.048931e-02 -1.665092e-01 -4.495348e-02

## 1893 6.357985e-02 6.006371e-02 1.629736e-01 -2.855818e-01 -5.480710e-02

## 1894 4.194697e-02 -1.802139e-02 -1.249750e-01 -7.447634e-02 -1.230405e-01

## 1895 8.219851e-02 -5.347158e-02 -4.390440e-02 -8.102773e-02 -9.179090e-02

## 1896 1.709040e-01 8.265198e-02 3.203216e-02 1.857852e-02 -1.120857e-01

## 1897 -6.329920e-02 1.148501e-01 5.953913e-02 5.190563e-02 -1.854901e-02

## 1898 5.114275e-02 -9.801834e-02 -1.673614e-01 -1.738488e-01 -1.699050e-02

## 1899 5.956778e-02 7.055838e-02 6.410520e-02 -4.153805e-02 5.598331e-02

## 1900 7.134536e-02 2.653211e-01 -2.147100e-01 -1.134437e-03 -4.570594e-02

## 1901 4.495628e-02 -5.725067e-02 -1.080992e-01 8.535455e-03 1.165353e-01

## 1902 -2.891143e-02 7.463185e-02 1.177447e-03 2.350353e-02 9.149189e-03

## 1903 -7.232041e-02 7.829613e-02 -4.873927e-02 -1.026826e-01 -1.071566e-02

## 1904 -6.144870e-02 -3.589680e-02 -1.724163e-02 1.085720e-01 -6.311186e-02

## 1905 6.230036e-02 -8.822965e-02 1.169104e-01 -1.095406e-02 5.342690e-02

## 1906 1.970998e-01 9.810147e-02 -7.461635e-02 9.135496e-02 -2.152623e-01

## 1907 4.477037e-02 -2.485716e-02 1.354446e-01 1.587757e-02 -1.297163e-01

## 1908 2.987708e-02 9.598764e-03 -7.885264e-03 -1.113465e-01 1.673755e-02

## 1909 -7.934089e-02 -2.553668e-02 -3.684033e-02 3.938886e-02 -4.887661e-02

## 1910 6.491936e-02 -3.949567e-02 -1.647713e-02 8.579084e-02 2.032004e-02

## 1911 4.060137e-03 -1.459869e-01 -6.293766e-02 -7.632453e-02 -2.112153e-02

## 1912 1.399990e-01 -2.670032e-02 1.489672e-01 -1.502891e-03 -1.102360e-01

## 1913 -6.622143e-02 1.414202e-01 -7.132251e-02 6.687187e-02 3.754848e-02

## 1914 1.462814e-01 1.495706e-02 3.167940e-02 1.158580e-02 1.259528e-02

## 1915 4.662394e-02 1.404513e-01 1.828644e-01 6.316100e-02 -7.136134e-02

## 1916 1.068561e-02 1.258955e-01 -2.946139e-02 -3.403526e-02 4.436361e-02

## 1917 -2.497213e-01 -5.160462e-02 -1.944048e-01 1.802504e-01 -3.144897e-02

## 1918 -7.068051e-02 -1.681418e-01 7.384457e-02 -3.118549e-02 1.191859e-01

## 1919 5.592780e-02 2.857524e-01 -1.040330e-01 4.065560e-02 7.746119e-02

## 1920 -2.796492e-02 -3.185418e-01 2.867765e-01 1.497166e-01 7.043184e-02

## 1921 -2.094557e-01 1.199530e-02 -7.039814e-02 -7.307100e-02 1.487162e-01

## 1922 -1.447568e-01 1.151564e-01 -1.464040e-01 4.461786e-02 -2.536537e-01

## 1923 -2.947838e-02 1.263757e-01 2.283800e-02 1.206293e-01 -1.331560e-01

## 1924 -9.139755e-02 5.274683e-02 1.715600e-03 -4.330634e-02 -3.953788e-02

## 1925 -9.967925e-02 7.167582e-02 1.942593e-01 -5.481715e-02 -1.907535e-02

## 1926 -2.556010e-03 -1.067355e-01 2.296154e-01 1.336020e-02 -3.873923e-02

## 1927 -3.774797e-02 6.108594e-02 -7.299850e-02 4.472702e-02 5.214471e-03

## 1928 8.182184e-02 5.604415e-03 -8.174759e-02 1.677612e-01 -9.482776e-02

## 1929 -2.363578e-02 -1.041314e-01 -1.463695e-01 3.729000e-02 -1.070043e-01

## 1930 -8.524442e-02 -1.019898e-02 1.001029e-01 2.002179e-02 1.214790e-01

## 1931 1.063850e-01 7.502561e-02 2.705241e-02 -6.726931e-02 -5.659143e-02

## 1932 1.849207e-01 5.299542e-02 1.083643e-01 -6.076868e-02 -4.307535e-02

## 1933 -3.110031e-04 1.826462e-02 -8.665483e-02 -9.496771e-03 7.521822e-02

## 1934 1.345911e-01 -1.732988e-01 2.192779e-02 1.336339e-01 6.570544e-02

## 1935 8.376989e-02 -8.160678e-02 -7.615640e-02 2.159907e-02 6.515996e-02

## 1936 -2.317305e-02 1.365620e-01 -1.496245e-01 -1.261522e-02 4.364158e-03

## 1937 5.973185e-02 1.009118e-01 -4.999674e-02 4.050270e-03 -5.829345e-02

## 1938 -2.620107e-02 4.296165e-03 8.136835e-02 3.051147e-02 -1.491622e-02

## 1939 8.925684e-02 -5.928371e-04 -4.596903e-02 9.129230e-02 1.029921e-01

## 1940 2.056866e-01 8.751959e-03 -4.592472e-02 9.171733e-02 1.691688e-01

## 1941 -9.642091e-02 -4.737907e-02 9.940653e-02 2.956864e-01 -1.235091e-01

## 1942 2.632867e-01 -2.333566e-01 6.079031e-03 -1.570908e-01 1.658734e-01

## 1943 9.578738e-02 -7.742049e-02 -3.284294e-03 -1.040964e-01 3.063027e-02

## 1944 -4.937488e-02 -8.810785e-02 2.295232e-01 3.050028e-02 -6.847483e-02

## 1945 -8.995094e-02 5.539268e-02 -8.054958e-02 1.793397e-01 -2.849512e-01

## 1946 -1.793138e-01 -7.484479e-02 -1.757303e-01 -3.834464e-02 -6.580422e-02

## 1947 2.042987e-01 -5.440040e-02 -1.223985e-01 7.197575e-02 -2.742982e-02

## 1948 -1.218209e-01 1.025678e-02 4.475837e-02 -9.932127e-02 9.857656e-02

## 1949 5.722177e-02 -8.516525e-02 3.751959e-03 9.149384e-03 -3.156818e-02

## 1950 -1.546900e-01 -7.408904e-02 -6.231232e-02 3.158441e-02 3.888996e-02

## 1951 -8.627690e-02 -1.840051e-02 3.949847e-02 6.288285e-03 6.835902e-02

## 1952 2.175725e-01 1.547667e-01 1.607728e-02 -8.308257e-02 -4.119636e-02

## 1953 -4.475623e-02 7.301298e-02 5.649036e-02 8.218687e-02 1.876215e-02

## 1954 -1.581160e-01 2.268796e-02 5.700315e-02 -1.866339e-01 -1.323741e-01

## 1955 9.359611e-02 -7.144624e-02 -9.449160e-02 -5.172556e-02 -1.811709e-01

## 1956 -8.375771e-02 7.950043e-02 2.331317e-02 -1.307542e-01 -1.659800e-05

## 1957 5.634765e-02 4.755418e-02 1.070659e-01 9.251789e-02 2.392751e-01

## 1958 1.186373e-01 9.105694e-02 -4.263218e-02 1.526326e-02 2.872642e-02

## 1959 9.506900e-03 1.025415e-02 3.097131e-02 2.504381e-02 1.768864e-02

## 1960 5.872587e-03 -4.152164e-02 -1.864644e-02 -8.883959e-02 -4.297514e-02

## 1961 1.354287e-02 1.059975e-01 -9.115784e-03 7.962862e-02 1.342778e-01

## 1962 -6.052076e-02 6.134622e-02 1.860364e-02 -4.309570e-02 -6.289143e-02

## 1963 -1.104630e-01 -2.154454e-02 4.427655e-02 -4.283694e-04 1.348738e-01

## 1964 -1.176648e-01 -5.206738e-02 -5.494254e-02 -7.877284e-02 -1.207509e-01

## 1965 1.749331e-01 1.407399e-01 -1.079686e-01 1.117762e-02 4.585050e-02

## 1966 3.983521e-03 -5.476927e-02 -1.370279e-02 1.115185e-01 -1.089150e-01

## 1967 -3.862753e-02 -5.879149e-02 -1.030958e-02 5.049124e-04 1.438806e-01

## 1968 2.231957e-02 -9.984459e-02 7.264032e-03 -2.381784e-02 -1.352469e-01

## 1969 1.563005e-01 1.093426e-01 1.092457e-01 8.412182e-02 7.212404e-02

## 1970 7.853078e-02 7.564931e-03 -3.821027e-02 4.366026e-02 -4.557635e-02

## 1971 -5.844479e-02 -1.215200e-01 -4.944485e-02 -4.328167e-02 1.138305e-02

## 1972 1.284484e-01 9.715540e-02 3.911593e-02 3.527299e-02 1.230144e-01

## 1973 -1.687933e-02 7.821661e-04 1.074664e-01 1.203717e-02 5.526499e-04

## 1974 -2.364189e-01 -1.843833e-01 -2.741168e-02 5.387651e-02 9.818013e-02

## 1975 -1.157249e-01 -9.397455e-03 3.865690e-02 1.672336e-02 4.244341e-02

## 1976 -1.673141e-01 2.653930e-02 -7.466035e-02 2.260092e-02 -7.763452e-02

## 1977 1.703232e-01 8.243653e-02 -4.775965e-02 -5.246640e-02 3.290841e-02

## 1978 2.444771e-02 3.960984e-02 3.342934e-02 -1.032421e-01 5.577476e-02

## 1979 1.003157e-01 1.216353e-02 5.915379e-02 9.343763e-02 -6.633059e-02

## 1980 8.404468e-03 8.459836e-02 1.516637e-01 -7.846218e-03 -4.337787e-02

## 1981 -1.486075e-02 -7.193875e-02 1.407090e-02 2.694061e-02 7.341756e-02

## 1982 2.615186e-02 -1.143873e-01 -9.336174e-02 2.678999e-02 7.311469e-02

## 1983 1.935245e-01 1.585049e-01 -4.046186e-02 4.724722e-03 3.144587e-02

## 1984 -4.470211e-02 4.623656e-02 -5.631218e-02 -3.536251e-02 -1.241158e-04

## 1985 5.074335e-02 6.759367e-02 6.051201e-02 -9.956362e-02 -4.193566e-03

## 1986 -4.640509e-02 6.114685e-02 2.570827e-02 -3.320791e-02 -3.070801e-02

## 1987 7.725397e-02 3.984371e-02 6.464138e-02 6.891663e-02 -4.624316e-02

## 1988 1.022134e-01 4.038549e-03 2.664136e-02 -5.341620e-02 6.628988e-03

## 1989 -1.192910e-02 1.325325e-02 -1.904195e-02 -1.855414e-02 -3.342977e-02

## 1990 3.582388e-02 4.737916e-02 5.133827e-02 6.294169e-02 8.006401e-03

## 1991 -3.607577e-02 -2.231227e-02 8.243783e-02 7.515596e-02 1.208122e-01

## 1992 2.598987e-02 4.040298e-02 3.044413e-02 4.705162e-02 -1.882628e-02

## 1993 1.657077e-01 -3.324111e-02 1.303300e-01 -3.468883e-02 7.784399e-03

## 1994 -2.541221e-03 -1.292123e-01 6.294435e-02 -3.881466e-02 1.588985e-01

## 1995 9.383361e-03 2.805561e-02 2.235994e-02 -8.188490e-02 -2.445676e-02

## 1996 -4.190306e-02 1.272278e-01 8.864076e-02 -6.201352e-03 -4.580800e-02

## 1997 -8.873274e-02 2.321499e-04 4.538524e-02 -1.980005e-02 2.650409e-02

## 1998 3.875825e-02 1.157894e-01 1.232532e-01 8.454677e-02 8.464362e-02

## 1999 -4.493537e-02 -1.704735e-02 9.758114e-02 -1.161277e-01 -6.239433e-02

## 2000 8.937883e-03 1.128038e-02 -5.538870e-02 1.222820e-01 -1.678103e-01

## 2001 8.279984e-02 7.380144e-02 1.038507e-01 6.035261e-02 -8.626234e-02

## 2002 1.610008e-01 -2.586906e-02 1.805887e-01 1.637873e-02 6.008624e-02

## 2003 9.658049e-02 8.118796e-02 -5.098901e-03 -8.447595e-03 -3.670827e-02

## 2004 1.727429e-02 4.093055e-02 -5.010691e-02 4.364773e-02 -1.243126e-01

## 2005 2.084444e-02 5.534056e-02 4.658341e-02 2.611046e-02 -2.618512e-02

## 2006 3.245425e-02 4.780635e-02 -4.100370e-02 -3.174253e-02 -6.967219e-02

## 2007 -8.369953e-03 3.615690e-02 -7.266677e-02 2.600826e-03 -7.078632e-02

## Jun Jul Aug Sep Oct

## 1850 -4.024989e-02 2.166876e-01 -9.127531e-02 -1.250457e-01 1.271816e-01

## 1851 7.940774e-02 1.339840e-01 1.642194e-01 -8.919921e-02 9.824102e-02

## 1852 1.422036e-01 4.084533e-01 -2.522586e-01 4.423655e-02 -5.624302e-02

## 1853 2.074913e-02 2.219029e-01 8.170500e-02 -1.906773e-01 -6.811217e-02

## 1854 1.552527e-01 -2.013148e-01 -6.085440e-02 3.542865e-01 -8.648265e-02

## 1855 7.186104e-02 -7.201692e-02 2.750797e-01 -3.590133e-02 -8.072435e-02

## 1856 -2.149766e-01 8.458734e-02 9.496826e-02 -1.546619e-01 -3.681431e-02

## 1857 1.200098e-01 -2.391456e-01 4.141460e-02 1.178188e-01 -7.279007e-02

## 1858 4.463456e-02 1.859150e-01 3.562051e-01 1.564268e-01 -1.213665e-01

## 1859 8.175525e-02 -6.810731e-02 7.932474e-02 -2.788268e-01 2.201022e-01

## 1860 1.588160e-02 3.997235e-02 -7.726416e-04 1.132508e-01 -3.293896e-02

## 1861 2.064274e-01 -2.792672e-01 1.975381e-01 7.918018e-02 -1.299935e-01

## 1862 -7.583529e-02 -1.248615e-01 -4.918925e-01 2.698712e-02 1.175031e-01

## 1863 -9.382254e-02 1.091801e-01 -6.777547e-03 -1.185859e-01 2.074557e-01

## 1864 -1.401646e-01 5.120652e-02 -2.607884e-01 9.714672e-02 2.919877e-02

## 1865 -1.212890e-01 6.225331e-02 1.743461e-01 -1.527103e-01 7.680766e-02

## 1866 5.833198e-02 2.003137e-01 -8.592311e-02 -1.198865e-01 1.276859e-01

## 1867 -5.477135e-02 -3.946928e-02 -7.772912e-02 2.439225e-01 3.841807e-02

## 1868 -3.606322e-01 8.094215e-02 1.544383e-01 1.731163e-01 7.714114e-02

## 1869 -1.120077e-01 -1.624525e-01 1.521763e-01 1.547823e-01 -1.582161e-02

## 1870 -8.429975e-02 2.637893e-01 -8.817720e-02 -6.113866e-02 -1.020846e-01

## 1871 2.661622e-02 1.144111e-01 -1.355583e-01 -6.753168e-02 -1.975027e-01

## 1872 -1.027948e-01 3.942125e-02 6.355862e-02 -6.211058e-02 -1.092505e-02

## 1873 -2.204064e-02 5.073142e-02 2.407264e-02 -1.855369e-01 -7.632545e-02

## 1874 -2.478836e-01 3.887712e-01 -4.651205e-02 -2.458033e-02 -1.755027e-01

## 1875 -1.287798e-01 -1.177463e-01 9.240472e-02 1.125954e-01 -6.645977e-02

## 1876 -2.092278e-01 -6.190689e-03 -7.457060e-02 -1.572033e-01 1.963041e-01

## 1877 8.853945e-02 7.011146e-02 1.555179e-01 1.483640e-01 2.836180e-01

## 1878 -1.883756e-01 8.986965e-02 -3.608760e-02 5.584006e-02 1.772338e-02

## 1879 7.455057e-02 6.109829e-03 1.260488e-01 4.149022e-02 -1.144243e-01

## 1880 -1.581292e-01 1.319996e-04 2.228999e-01 -4.200102e-03 -1.136965e-01

## 1881 -1.148645e-01 4.501243e-02 -4.277388e-02 -7.687018e-02 1.246221e-01

## 1882 -5.240792e-02 1.398178e-02 -5.467794e-02 1.984270e-01 -7.278403e-02

## 1883 2.182772e-01 -8.611627e-02 1.323244e-04 -8.621570e-02 -9.221320e-02

## 1884 -6.763353e-02 -1.206379e-01 8.100660e-02 1.357145e-01 -4.483402e-02

## 1885 -1.181087e-01 -1.738674e-02 3.869778e-02 1.876518e-01 6.756782e-02

## 1886 -1.064071e-01 -8.940515e-02 8.985315e-02 -1.204934e-01 -2.018727e-02

## 1887 -1.627002e-01 7.769075e-02 -2.488527e-02 -2.946496e-02 -1.361022e-01

## 1888 1.910102e-02 -3.740637e-02 5.381646e-02 4.561488e-02 1.458580e-01

## 1889 -8.761068e-02 -2.699332e-03 -1.050501e-01 -7.796932e-02 -3.419917e-02

## 1890 2.750041e-02 -2.578595e-02 -4.968039e-02 -1.143914e-01 -1.057351e-01

## 1891 -1.651123e-01 -1.752218e-01 -4.852117e-02 9.004457e-02 4.421517e-02

## 1892 -1.471568e-01 -1.366272e-01 -9.169019e-03 2.612939e-02 -3.468440e-02

## 1893 -1.080217e-01 1.128084e-01 1.245748e-01 -8.619053e-02 7.894669e-02

## 1894 2.310949e-02 1.520720e-02 -2.291116e-02 -1.513470e-01 3.195084e-02

## 1895 1.650435e-01 -4.480350e-02 1.786640e-01 -9.757920e-02 -9.631195e-02

## 1896 3.447126e-02 9.554430e-02 1.000826e-01 -1.051702e-02 2.362709e-02

## 1897 -7.383386e-03 -1.475623e-01 -1.018000e-02 -1.719556e-02 -1.046470e-01

## 1898 1.257820e-01 -1.095367e-01 1.393442e-02 1.773936e-02 -1.628987e-01

## 1899 4.701765e-02 -9.470477e-02 1.612998e-01 6.670439e-02 -9.160995e-02

## 1900 2.930987e-02 8.460187e-02 -9.364655e-02 1.442824e-02 -5.903916e-02

## 1901 3.136529e-02 -1.324975e-01 -1.641313e-02 -1.974498e-02 -4.013409e-03

## 1902 -8.731117e-02 6.401417e-02 -1.326334e-01 2.086826e-02 -1.593993e-01

## 1903 -1.215057e-01 4.223028e-02 -1.337257e-01 -3.837475e-02 -1.546390e-01

## 1904 3.172469e-02 6.754145e-03 -1.457115e-02 3.893657e-02 -1.295963e-01

## 1905 1.672698e-02 -4.883427e-02 6.882655e-02 -6.813444e-02 4.943234e-02

## 1906 -3.872137e-02 1.206616e-02 -2.879688e-02 -3.536384e-02 -1.386999e-02

## 1907 -7.468956e-02 -1.215036e-02 5.873831e-02 1.116807e-02 3.485742e-02

## 1908 -4.932094e-02 -4.178471e-02 -1.071498e-01 9.824201e-03 -7.864639e-02

## 1909 1.738853e-02 -1.143344e-01 2.174397e-01 2.062413e-02 -1.108126e-01

## 1910 -6.926716e-03 3.245132e-02 -8.920592e-03 -4.390677e-02 -8.028919e-02

## 1911 -5.673980e-02 8.811586e-02 -2.181977e-02 -1.046954e-01 1.375864e-01

## 1912 -3.941066e-02 -9.742173e-03 -5.821751e-02 4.730803e-02 1.015662e-02

## 1913 2.670897e-02 7.218354e-02 1.521290e-04 2.518142e-02 1.973842e-02

## 1914 1.147629e-01 -4.143951e-02 1.766970e-01 4.657106e-02 1.142352e-01

## 1915 -1.546703e-01 1.050371e-01 7.953183e-02 2.843320e-03 -2.216007e-02

## 1916 -1.663080e-01 -1.515078e-01 1.278800e-01 1.477867e-01 -4.661283e-02

## 1917 2.173382e-01 4.702330e-01 -2.812887e-02 1.512316e-01 -1.605245e-01

## 1918 2.398300e-01 -1.691020e-02 -1.093791e-01 1.416915e-01 1.267710e-01

## 1919 -4.377069e-02 -2.347057e-01 -9.171578e-02 6.425210e-03 -9.575234e-03

## 1920 6.650369e-02 -2.166887e-01 7.606376e-02 2.044643e-01 4.887749e-02

## 1921 1.046448e-01 -1.264407e-03 -1.260744e-01 1.641813e-01 4.589121e-02

## 1922 -1.883079e-02 1.794065e-01 -9.440096e-02 1.632520e-02 2.905470e-03

## 1923 6.975970e-02 -2.411458e-01 -1.967963e-02 -1.282764e-01 -5.762094e-02

## 1924 -3.543617e-02 -6.838496e-02 3.805981e-02 -1.741748e-01 1.429512e-02

## 1925 7.389093e-02 5.780732e-02 1.327984e-01 -1.453766e-01 -2.421877e-02

## 1926 7.484170e-02 -1.927791e-01 2.197292e-01 -3.256867e-02 1.258902e-02

## 1927 -4.891122e-02 7.724876e-02 -2.939418e-02 8.662074e-03 -3.869286e-03

## 1928 -4.875963e-02 9.384280e-02 7.853664e-02 -1.296738e-01 8.555320e-02

## 1929 4.537128e-02 -1.172186e-01 7.304768e-02 -4.415631e-02 6.538232e-02

## 1930 3.785153e-02 -3.618813e-02 -2.988353e-02 3.507091e-02 8.228709e-02

## 1931 3.556463e-02 1.313777e-01 -7.925614e-02 -4.440655e-02 -3.056528e-02

## 1932 -8.303402e-02 5.715766e-02 -2.191862e-01 1.649875e-01 -4.810090e-02

## 1933 -3.287484e-02 -1.128165e-01 4.272747e-02 -1.656956e-02 4.452723e-02

## 1934 2.100806e-01 6.741681e-02 6.372680e-02 2.901743e-02 -7.092744e-02

## 1935 3.513982e-02 -6.947063e-03 -9.095178e-02 6.452807e-02 -1.063807e-02

## 1936 -9.490348e-02 1.323132e-01 5.226373e-02 -8.375051e-02 2.801749e-01

## 1937 5.826712e-02 8.757002e-02 8.199153e-02 2.556289e-02 3.080242e-02

## 1938 1.374884e-01 -1.950203e-02 -2.668382e-03 7.141165e-02 1.559598e-01

## 1939 2.517519e-01 2.370895e-02 -4.827212e-02 -2.404122e-01 -2.006662e-01

## 1940 -4.990824e-02 1.567650e-01 -3.183915e-03 1.112789e-01 -1.286527e-01

## 1941 1.634193e-01 9.171564e-02 -1.266889e-02 -2.754106e-01 3.003566e-01

## 1942 -1.560442e-02 -2.180566e-01 7.774896e-02 -9.473506e-02 -2.443157e-01

## 1943 4.056770e-02 1.161234e-01 -1.685446e-01 3.201939e-02 2.849409e-01

## 1944 2.757409e-01 2.567996e-01 8.129787e-02 -6.318264e-02 -1.021358e-01

## 1945 8.051711e-02 -1.362367e-01 5.747660e-01 -6.248186e-02 -1.301527e-01

## 1946 -3.080659e-01 1.091399e-01 -2.344076e-01 1.330093e-01 3.008461e-02

## 1947 9.117808e-02 -3.177103e-03 -1.708404e-01 -2.214931e-01 -8.887567e-02

## 1948 -2.994174e-02 -1.995144e-01 -2.263522e-02 -2.483107e-02 6.365134e-02

## 1949 -1.181376e-01 6.565678e-02 -5.407232e-02 9.837738e-02 -1.332113e-01

## 1950 6.362904e-02 1.486299e-01 -5.436743e-02 -9.962115e-02 -1.291525e-01

## 1951 2.456406e-01 1.812758e-02 -1.278494e-03 -5.653283e-02 4.845589e-02

## 1952 -1.359487e-01 8.058290e-02 5.973547e-02 1.040496e-01 2.727672e-04

## 1953 -2.099334e-02 -1.528834e-01 -3.917983e-02 4.260250e-02 -2.378874e-02

## 1954 -9.265790e-02 -1.506376e-01 7.329094e-02 -1.116946e-02 6.542486e-02

## 1955 1.900242e-02 -8.757813e-02 8.383666e-02 6.250834e-02 -1.359246e-01

## 1956 4.818114e-02 7.789605e-02 -6.078138e-02 1.899343e-02 6.480839e-04

## 1957 7.632377e-02 -9.860122e-02 4.036322e-02 -5.918274e-02 2.671231e-02

## 1958 -3.190613e-02 1.227021e-01 -1.004962e-01 -4.580265e-02 8.853175e-02

## 1959 7.408184e-02 -2.676965e-02 2.290743e-02 9.254342e-03 7.528760e-02

## 1960 -1.790419e-02 2.317835e-02 8.102364e-02 1.084689e-01 3.819166e-03

## 1961 3.061482e-02 -1.087537e-01 7.268667e-02 1.303359e-02 2.567859e-02

## 1962 1.966827e-01 6.372351e-03 -8.240789e-03 9.445646e-02 2.354925e-04

## 1963 -3.237008e-03 1.375409e-01 4.578198e-02 -3.608510e-03 -7.019570e-02

## 1964 -3.928532e-02 -4.866232e-02 -6.504040e-02 -5.367153e-02 -1.165632e-02

## 1965 9.794816e-02 -1.010616e-01 5.630887e-02 4.828682e-02 -1.695091e-02

## 1966 1.041916e-01 3.134914e-02 -1.358595e-01 -1.368445e-02 -1.193872e-01

## 1967 -9.737450e-02 -4.965197e-02 -3.309224e-02 -3.700664e-03 5.780786e-02

## 1968 1.240014e-01 1.117395e-01 9.315834e-02 -2.713849e-02 7.955656e-02

## 1969 -6.725324e-02 -3.840860e-02 5.216881e-02 -1.499781e-02 7.044915e-02

## 1970 -4.352690e-02 -2.821064e-02 -8.763575e-02 6.861128e-02 7.578077e-02

## 1971 -7.412428e-02 1.677450e-01 2.925888e-02 9.684127e-02 -4.494118e-02

## 1972 1.232397e-01 4.188508e-03 7.755130e-02 1.303324e-01 4.399600e-02

## 1973 -5.429159e-02 -5.533086e-02 -2.342992e-02 6.237108e-03 1.876382e-02

## 1974 1.994120e-02 1.110035e-02 6.835880e-02 -8.083922e-02 -5.082272e-02

## 1975 2.723247e-02 -4.073074e-02 -1.118331e-01 -2.617694e-02 -9.233588e-02

## 1976 9.346337e-03 1.652048e-01 -2.291290e-02 3.328561e-02 2.167044e-02

## 1977 9.579460e-03 3.468152e-02 -4.166398e-02 -6.053121e-02 9.272998e-02

## 1978 -2.106792e-02 6.569712e-02 -1.450831e-01 6.129636e-02 -1.008679e-01

## 1979 3.109767e-02 5.227924e-02 1.316154e-01 -2.403339e-02 1.704399e-02

## 1980 -1.286511e-01 -4.568834e-02 -1.942417e-02 1.151922e-02 -3.836124e-02

## 1981 2.628171e-02 4.487311e-02 5.322460e-02 -6.248086e-03 -1.680299e-01

## 1982 -6.495215e-02 8.357515e-03 7.666966e-02 7.784363e-02 4.561605e-03

## 1983 -2.352240e-03 -8.223200e-02 5.247958e-02 5.623029e-03 -1.414840e-02

## 1984 -3.405294e-02 -1.082420e-01 7.952459e-02 1.313643e-01 -3.519801e-02

## 1985 -1.050046e-01 5.569098e-02 4.407335e-02 -6.556151e-02 4.066762e-02

## 1986 2.371422e-02 -1.659396e-03 -4.628878e-02 3.814113e-02 6.850794e-02

## 1987 2.935593e-02 1.847106e-01 -2.565764e-02 1.995145e-02 5.823906e-02

## 1988 -4.296374e-02 -1.058985e-01 4.184277e-02 4.176724e-02 -3.513315e-03

## 1989 -3.036303e-02 4.728606e-02 7.921469e-02 -5.456818e-04 -5.349941e-03

## 1990 -1.515582e-02 1.149274e-02 -2.554006e-02 -1.719984e-01 1.403662e-01

## 1991 1.549245e-02 1.259498e-02 -2.146322e-02 -2.793590e-02 -8.053579e-02

## 1992 2.232329e-02 -1.147639e-01 -3.406283e-02 -6.886651e-02 -1.205749e-01

## 1993 2.414780e-02 -2.152630e-02 -1.242335e-02 1.131552e-02 -2.153803e-02

## 1994 1.976605e-02 -6.221078e-02 -6.428207e-02 -3.485344e-02 1.430678e-02

## 1995 3.107675e-02 1.210185e-01 -2.823330e-02 -6.497870e-02 -2.807174e-02

## 1996 -7.434782e-02 2.469800e-02 6.226668e-02 -6.605953e-02 1.793833e-02

## 1997 1.504190e-01 7.695023e-02 7.950729e-02 1.807822e-01 9.171884e-02

## 1998 3.962534e-02 1.130559e-01 1.623043e-02 -2.074862e-01 -1.360990e-02

## 1999 2.686018e-02 -1.100053e-02 -7.986208e-02 5.220467e-02 -1.147160e-01

## 2000 4.800136e-02 -4.337737e-02 4.959726e-02 1.093672e-01 -4.322969e-02

## 2001 8.555755e-02 2.159783e-02 8.340611e-02 -6.044823e-03 -6.593386e-02

## 2002 -4.046581e-02 1.267965e-02 1.177680e-02 -4.554132e-02 4.336903e-02

## 2003 6.719786e-02 -2.411153e-02 -2.826378e-02 6.029475e-03 2.476258e-02

## 2004 -4.068848e-02 -4.372189e-02 1.863186e-02 2.436982e-02 7.579041e-02

## 2005 -8.420551e-03 -3.644647e-03 1.682792e-02 -8.891528e-02 3.279821e-02

## 2006 -1.278633e-02 4.622204e-02 2.160866e-02 -9.480010e-02 -1.967362e-02

## 2007 -2.786551e-02 1.025668e-02 -1.352673e-01 9.903825e-02 -6.699506e-02

## Nov Dec

## 1850 2.463343e-01 6.440426e-03

## 1851 1.746342e-01 1.306157e-02

## 1852 1.284125e-01 9.025417e-02

## 1853 1.808244e-01 -1.460917e-01

## 1854 -6.085904e-02 -2.154884e-01

## 1855 1.260182e-01 1.212788e-01

## 1856 -1.586971e-02 4.549057e-03

## 1857 -1.946305e-01 9.910227e-03

## 1858 -5.142193e-02 8.232797e-04

## 1859 9.612845e-02 3.569418e-01

## 1860 2.738518e-02 -1.553676e-01

## 1861 -8.273512e-02 1.745788e-01

## 1862 -7.433759e-03 5.659322e-03

## 1863 5.405983e-02 -1.341631e-01

## 1864 3.256510e-01 8.601990e-02

## 1865 -7.998539e-02 8.872527e-02

## 1866 -4.214200e-02 -2.106030e-01

## 1867 -1.200203e-01 -1.828961e-01

## 1868 -1.545690e-02 -9.013240e-02

## 1869 -1.016601e-02 -2.495650e-02

## 1870 6.941055e-02 -3.225861e-03

## 1871 2.711075e-01 1.443693e-02

## 1872 2.914505e-01 -8.997477e-02

## 1873 -9.959202e-02 -7.395955e-02

## 1874 6.813974e-03 1.238752e-01

## 1875 7.792348e-02 -7.709097e-02

## 1876 -8.745575e-02 -7.372455e-03

## 1877 -8.583661e-02 3.559057e-02

## 1878 -8.490170e-02 -3.050775e-02

## 1879 5.013638e-02 -9.239197e-02

## 1880 8.453865e-02 1.291922e-01

## 1881 4.303873e-02 -5.633521e-03

## 1882 -2.725921e-03 -1.504275e-01

## 1883 8.888495e-02 -1.806226e-01

## 1884 -8.170085e-02 -9.979123e-03

## 1885 2.330268e-01 2.512941e-02

## 1886 -5.609370e-02 -3.861231e-02

## 1887 -9.365513e-02 -1.223802e-01

## 1888 1.128615e-01 4.706574e-02

## 1889 3.789210e-02 1.257716e-01

## 1890 -6.869019e-02 1.605168e-01

## 1891 -4.317544e-02 -1.234059e-02

## 1892 6.952004e-02 -1.777702e-01

## 1893 2.238102e-02 4.930016e-02

## 1894 1.249157e-01 1.317606e-02

## 1895 9.102064e-02 4.988956e-02

## 1896 1.873989e-01 1.065429e-01

## 1897 -1.122786e-01 -2.026526e-02

## 1898 9.391841e-03 -2.285683e-03

## 1899 1.087097e-01 -5.096731e-02

## 1900 3.159185e-02 3.824316e-02

## 1901 -1.371642e-01 4.971066e-02

## 1902 -4.908760e-02 1.090550e-01

## 1903 -3.017437e-03 -4.274209e-02

## 1904 -1.592897e-02 6.561735e-02

## 1905 1.949173e-02 1.682165e-01

## 1906 -1.701128e-02 -2.835570e-02

## 1907 -1.412364e-01 -1.307525e-01

## 1908 3.638512e-02 -4.128338e-02

## 1909 -9.547241e-02 -9.992562e-02

## 1910 -1.443767e-01 -8.612157e-02

## 1911 1.542887e-01 2.420262e-01

## 1912 5.765827e-02 5.341172e-02

## 1913 3.816481e-02 -2.390751e-02

## 1914 2.087198e-01 -4.796360e-03

## 1915 6.119957e-02 -1.121642e-01

## 1916 -3.366983e-01 8.092456e-02

## 1917 -2.855195e-01 2.154243e-03

## 1918 4.035921e-01 1.817076e-02

## 1919 -1.365266e-01 1.926005e-01

## 1920 1.272182e-01 -7.828475e-02

## 1921 3.532243e-02 -9.960315e-02

## 1922 -2.036624e-02 1.056043e-02

## 1923 2.216167e-01 1.943489e-01

## 1924 -1.145175e-01 -1.151326e-01

## 1925 2.077335e-01 1.519894e-01

## 1926 -9.235589e-02 -9.173302e-03

## 1927 -8.518449e-02 -5.447045e-02

## 1928 1.073679e-01 -5.510747e-02

## 1929 2.296711e-01 -1.779158e-01

## 1930 1.144697e-01 -2.450571e-02

## 1931 -9.913053e-02 6.757747e-02

## 1932 4.778358e-02 1.194179e-02

## 1933 -1.248013e-01 -1.696056e-01

## 1934 4.566700e-02 -1.019047e-01

## 1935 3.882936e-02 -8.893954e-02

## 1936 -4.138500e-02 -1.660479e-02

## 1937 -2.522545e-02 5.277607e-02

## 1938 -7.407198e-02 -1.185037e-01

## 1939 1.043994e-02 3.169307e-01

## 1940 -1.954700e-01 2.962016e-01

## 1941 1.616720e-01 6.204319e-02

## 1942 -7.166424e-02 6.092209e-02

## 1943 -8.774463e-02 -2.118478e-02

## 1944 -3.727159e-02 8.895731e-02

## 1945 -1.857648e-01 -1.382721e-01

## 1946 -1.347355e-01 -1.311117e-01

## 1947 1.391882e-01 -1.858988e-01

## 1948 -1.031029e-01 -3.894638e-02

## 1949 -6.149533e-02 3.746133e-02

## 1950 -1.894185e-01 -1.485484e-01

## 1951 -4.960412e-02 1.320621e-02

## 1952 -1.776080e-02 1.571030e-02

## 1953 3.691766e-02 4.835982e-02

## 1954 4.529164e-02 -1.328111e-01

## 1955 -7.715156e-02 -8.020357e-02

## 1956 6.670325e-02 2.388451e-02

## 1957 1.058827e-01 -7.573195e-03

## 1958 1.833828e-02 2.392888e-02

## 1959 -1.313112e-02 -7.049151e-02

## 1960 -6.506295e-02 1.185140e-01

## 1961 -5.901191e-02 -6.301065e-02

## 1962 2.478837e-02 -9.923859e-02

## 1963 -9.330412e-02 5.153837e-02

## 1964 -1.523233e-01 -1.425963e-01

## 1965 -8.057793e-02 1.242471e-02

## 1966 7.520870e-02 6.986297e-02

## 1967 -2.903274e-02 -1.307501e-01

## 1968 1.105971e-01 1.089261e-01

## 1969 8.012191e-02 6.090533e-02

## 1970 4.431991e-03 -7.674587e-03

## 1971 2.032521e-03 -1.286063e-01

## 1972 1.902766e-01 3.331887e-01

## 1973 -8.157646e-02 -1.122407e-01

## 1974 1.581313e-02 -6.258146e-02

## 1975 -9.901125e-02 -1.205409e-01

## 1976 1.663524e-01 1.677867e-01

## 1977 1.478634e-02 -1.059527e-01

## 1978 9.871256e-02 2.127289e-02

## 1979 1.299602e-01 1.251777e-01

## 1980 9.936377e-02 4.335394e-03

## 1981 -1.615187e-02 1.594312e-01

## 1982 7.183944e-02 1.267022e-01

## 1983 -2.484590e-02 8.394914e-03

## 1984 -2.350154e-02 -2.256624e-02

## 1985 -1.089289e-01 3.576214e-02

## 1986 -2.178655e-02 -2.913708e-02

## 1987 1.041721e-01 -4.888745e-02

## 1988 -1.197144e-01 -9.192317e-02

## 1989 -3.954172e-02 4.424096e-02

## 1990 4.414703e-02 -1.424826e-02

## 1991 -7.021694e-02 -2.432953e-02

## 1992 -9.892517e-02 -1.059567e-02

## 1993 7.046713e-02 -1.265290e-01

## 1994 6.658802e-02 6.729467e-02

## 1995 6.437338e-02 -1.327070e-01

## 1996 3.658506e-03 2.491027e-02

## 1997 1.331521e-01 1.138438e-01

## 1998 -1.463648e-02 -1.414963e-02

## 1999 -6.210910e-02 -5.941769e-02

## 2000 -1.056516e-02 -6.647347e-02

## 2001 1.154346e-02 -6.670472e-02

## 2002 -6.532282e-02 5.937302e-02

## 2003 2.005638e-02 -2.839483e-02

## 2004 -4.700989e-02 -4.314804e-03

## 2005 -5.372783e-02 -2.276019e-02

## 2006 -2.647353e-02 6.421878e-02

## 2007 -1.465505e-01 -1.685890e-01##

## Call:

## garch(x = stemp.resid, trace = F)

##

## Coefficient(s):

## a0 a1 b1

## 7.961e-05 4.912e-02 9.440e-01## a0 a1 b1

## 2.5 % 1.064251e-05 0.03299181 0.9249315

## 97.5 % 1.485814e-04 0.06525680 0.9630787# residuals do not appear to have a structure

(stemp.garch.res <- tsibble(.resid = c(NA, resid(stemp.garch)[-1]),

time = stemp$time))## Using `time` as index variable.## # A tsibble: 1,896 x 2 [1M]

## .resid time

## <dbl> <mth>

## 1 NA 1850 Jan

## 2 0.226 1850 Feb

## 3 -2.15 1850 Mar

## 4 0.930 1850 Apr

## 5 3.04 1850 May

## 6 -0.306 1850 Jun

## 7 1.69 1850 Jul

## 8 -0.681 1850 Aug

## 9 -0.947 1850 Sep

## 10 0.967 1850 Oct

## # ℹ 1,886 more rows

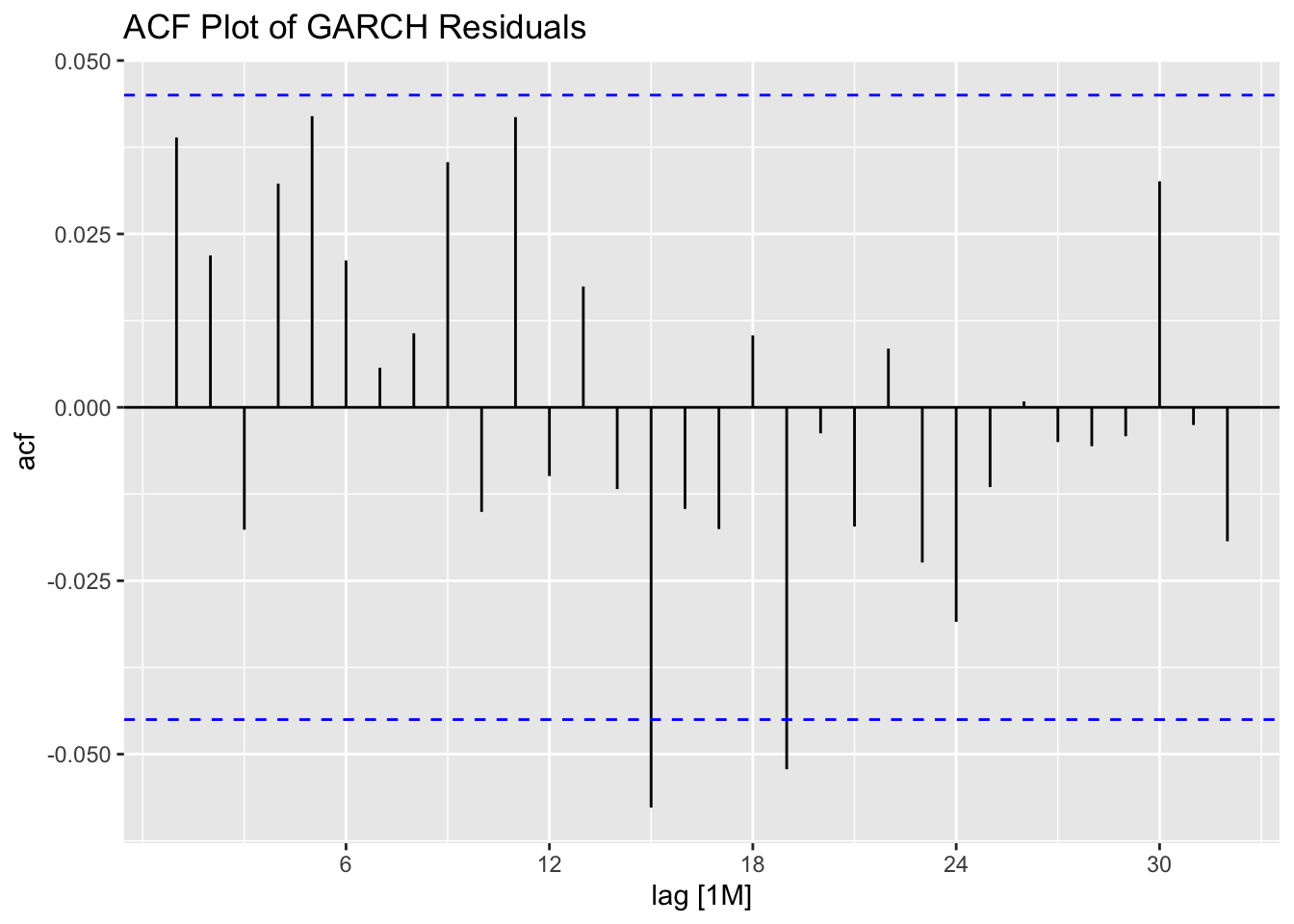

ACF(stemp.garch.res, .resid^2) |> autoplot() +

labs(title = "ACF Plot of the Squared GARCH Residuals")

To implement the GARCH model with the ARIMA model above, both the original model and the GARCH model should be used to generate forecasts. The forecasts from each model can then be added together.

6.3 Harmonic Regressions and Fourier Terms

Jean-Baptiste Fourier, a French mathematician showed that a series of \(sin\) and \(cos\) terms with the correct frequencies can approximate any periodic function.43 These terms, dubbed Fourier terms, can be used to approximate seasonal patterns. Included in regressions and ARIMA models, these terms can be a powerful tool in modeling the seasonality present in data.

For example, if \(m\) is the seasonal period, then the first bunch of Fourier terms are:44

\[ x_{1,t} = sin(\frac{2 \pi t}{m}), \space x_{2,t} = cos(\frac{2 \pi t}{m}), \space x_{3,t} = sin(\frac{4 \pi t}{m}), \\ x_{4,t} = cos(\frac{4 \pi t}{m}), \space x _{5,t} = sin(\frac{6 \pi t}{m}), x_{6,t} = cos(\frac{6 \pi t}{m}), \text{ ect.} \]

The maximum number of fourier terms allow is \(K = m/2\), where \(m\) is the seasonal period.45 The advantages of fourier terms are that they account for any length seasonality and can account for more than one seasonal period through multiple fourier terms.46 For more information on fourier terms, refer to this section on harmonic regression

To show examples of different models with fourier components, I will use the aus_retail data from Forecasting: Principles and Practice containing the total monthly expenditure on cafes, restaurants and takeaway food services in Australia ($billion) from 2004 to 2018.47

(aus_cafe <- aus_retail |>

filter(

Industry == "Cafes, restaurants and takeaway food services",

year(Month) %in% 2004:2018

) |>

summarise(Turnover = sum(Turnover)) |>

rename(time = 1))## # A tsibble: 180 x 2 [1M]

## time Turnover

## <mth> <dbl>

## 1 2004 Jan 1895.

## 2 2004 Feb 1766.

## 3 2004 Mar 1873.

## 4 2004 Apr 1874.

## 5 2004 May 1846

## 6 2004 Jun 1758.

## 7 2004 Jul 1878.

## 8 2004 Aug 1850.

## 9 2004 Sep 1922.

## 10 2004 Oct 1915.

## # ℹ 170 more rowsThe data is monthly, so the seasonal period is 12, meaning K cannot be more than 6. The training set will be the observations from 2004 to 2016 and the test set will be the observations from 2017 to 2018.

First, I examine linear models using all possible fourier terms. I generate measures of accuracy for the training set, forecasts for the training set, and measures of accuracy for the test set. As K increases, generally the amount of error in both the test and training sets both goes down.

aus_cafe.lm <- aus_cafe |>

filter(year(time) <= 2016) |>

model(lm = TSLM(log(Turnover) ~ trend()),

lm1 = TSLM(log(Turnover) ~ trend() + fourier(K = 1)),

lm2 = TSLM(log(Turnover) ~ trend() + fourier(K = 2)),

lm3 = TSLM(log(Turnover) ~ trend() + fourier(K = 3)),

lm4 = TSLM(log(Turnover) ~ trend() + fourier(K = 4)),

lm5 = TSLM(log(Turnover) ~ trend() + fourier(K = 5)),

lm6 = TSLM(log(Turnover) ~ trend() + fourier(K = 6)))

accuracy(aus_cafe.lm)## # A tibble: 7 × 10

## .model .type ME RMSE MAE MPE MAPE MASE RMSSE ACF1

## <chr> <chr> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

## 1 lm Training 3.58 140. 102. -0.138 3.93 0.666 0.780 0.264

## 2 lm1 Training 2.82 121. 89.5 -0.110 3.51 0.586 0.679 0.0754

## 3 lm2 Training 2.53 115. 90.8 -0.0986 3.54 0.594 0.645 0.0303

## 4 lm3 Training 1.71 93.0 75.9 -0.0676 2.99 0.496 0.520 0.0487

## 5 lm4 Training 1.46 84.2 67.0 -0.0578 2.68 0.438 0.471 0.176

## 6 lm5 Training 1.00 68.4 54.8 -0.0410 2.22 0.359 0.383 0.718

## 7 lm6 Training 1.00 68.2 54.5 -0.0409 2.21 0.357 0.381 0.729aus_cafe.lm.fc <- aus_cafe.lm |>

forecast(new_data = aus_cafe |>

filter(year(time) > 2016))

aus_cafe.lm.fc |>

accuracy(aus_cafe)## # A tibble: 7 × 10

## .model .type ME RMSE MAE MPE MAPE MASE RMSSE ACF1

## <chr> <chr> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

## 1 lm Test -196. 261. 227. -5.47 6.21 1.49 1.46 0.165

## 2 lm1 Test -187. 237. 204. -5.14 5.56 1.34 1.33 -0.0778

## 3 lm2 Test -184. 231. 195. -5.03 5.31 1.28 1.29 -0.140

## 4 lm3 Test -181. 210. 181. -4.87 4.88 1.19 1.17 -0.212

## 5 lm4 Test -180. 200. 180. -4.83 4.83 1.18 1.12 -0.0470

## 6 lm5 Test -179. 191. 179. -4.77 4.77 1.17 1.07 0.638

## 7 lm6 Test -179. 191. 179. -4.77 4.77 1.17 1.07 0.669Next, I consider ARIMA models with fourier terms. Additing a fourier term to an ARIMA model creates a linear regression of the dependent variable on the fourier term with ARIMA errors. To make sure ARIMA() does not internally account for the seasonality, PDQ() must be set to 0,0,0. Including both a seasonal ARIMA component and fourier term would not be theoretically consistent, as the seasonality would be accounted for twice.

# THIS TAKES A WHILE TO RUN

aus_cafe.arima <- aus_cafe |>

filter(year(time) <= 2016) |>

model(auto = ARIMA(log(Turnover), stepwise = FALSE),

arima1 = ARIMA(log(Turnover) ~ fourier(K=1) + PDQ(0,0,0)),

arima2 = ARIMA(log(Turnover) ~ fourier(K=2) + PDQ(0,0,0)),

arima3 = ARIMA(log(Turnover) ~ fourier(K=3) + PDQ(0,0,0)),

arima4 = ARIMA(log(Turnover) ~ fourier(K=4) + PDQ(0,0,0)),

arima5 = ARIMA(log(Turnover) ~ fourier(K=5) + PDQ(0,0,0)),

arima6 = ARIMA(log(Turnover) ~ fourier(K=6) + PDQ(0,0,0)))As observed above with the linear models, as K increases the amount of error in the training set decreases. The best fourier model outperforms the ARIMA(3,0,1)(2,1,0)[12] model selected as the best ARIMA model by the algorithm. In the test set, after generating forecasts, the model with the fourier term K = 5 performs the best out of all the models considered.

## # A tibble: 7 × 10

## .model .type ME RMSE MAE MPE MAPE MASE RMSSE ACF1

## <chr> <chr> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

## 1 auto Training 2.39 52.1 41.0 0.0712 1.60 0.269 0.291 -0.00818

## 2 arima1 Training 3.28 110. 82.1 -0.0518 3.14 0.537 0.614 -0.0442

## 3 arima2 Training 2.56 85.4 65.5 -0.00317 2.51 0.428 0.477 -0.0444

## 4 arima3 Training 1.48 69.2 53.1 -0.0110 2.06 0.348 0.387 -0.0446

## 5 arima4 Training 1.47 58.9 47.5 -0.00158 1.83 0.311 0.329 -0.101

## 6 arima5 Training 0.702 45.3 36.4 -0.0137 1.44 0.238 0.253 -0.0435

## 7 arima6 Training 0.717 44.7 35.8 -0.0129 1.42 0.235 0.250 -0.0233## Series: Turnover

## Model: ARIMA(3,0,1)(2,1,0)[12] w/ drift

## Transformation: log(Turnover)

##

## Coefficients:

## ar1 ar2 ar3 ma1 sar1 sar2 constant

## -0.2266 0.6564 0.3438 0.7738 -0.5799 -0.3753 0.0233

## s.e. 0.2027 0.1506 0.0844 0.2117 0.0879 0.0815 0.0032

##

## sigma^2 estimated as 0.0004714: log likelihood=348.02

## AIC=-680.05 AICc=-678.98 BIC=-656.29aus_cafe.arima.fc <- aus_cafe.arima |>

forecast(new_data = aus_cafe |>

filter(year(time) > 2016))

aus_cafe.arima.fc|>

accuracy(aus_cafe)## # A tibble: 7 × 10

## .model .type ME RMSE MAE MPE MAPE MASE RMSSE ACF1

## <chr> <chr> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

## 1 arima1 Test -224. 264. 235. -6.12 6.36 1.54 1.48 -0.0403

## 2 arima2 Test -134. 175. 147. -3.66 3.98 0.960 0.977 -0.176

## 3 arima3 Test -91.6 131. 104. -2.48 2.79 0.678 0.731 -0.310

## 4 arima4 Test -120. 144. 123. -3.23 3.29 0.802 0.803 -0.281

## 5 arima5 Test -96.9 110. 97.1 -2.57 2.58 0.635 0.617 0.538

## 6 arima6 Test -99.5 112. 99.5 -2.64 2.64 0.651 0.628 0.575

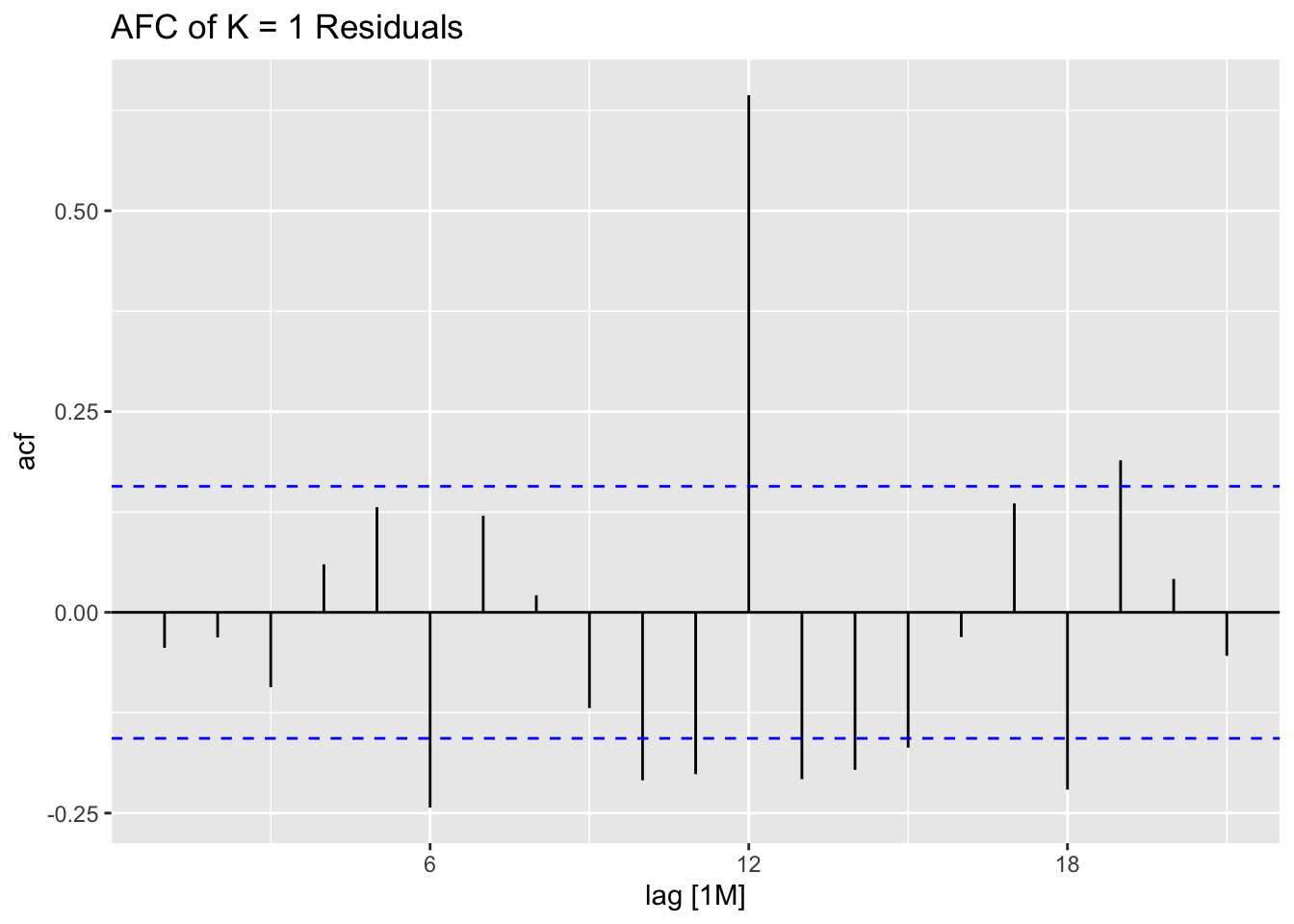

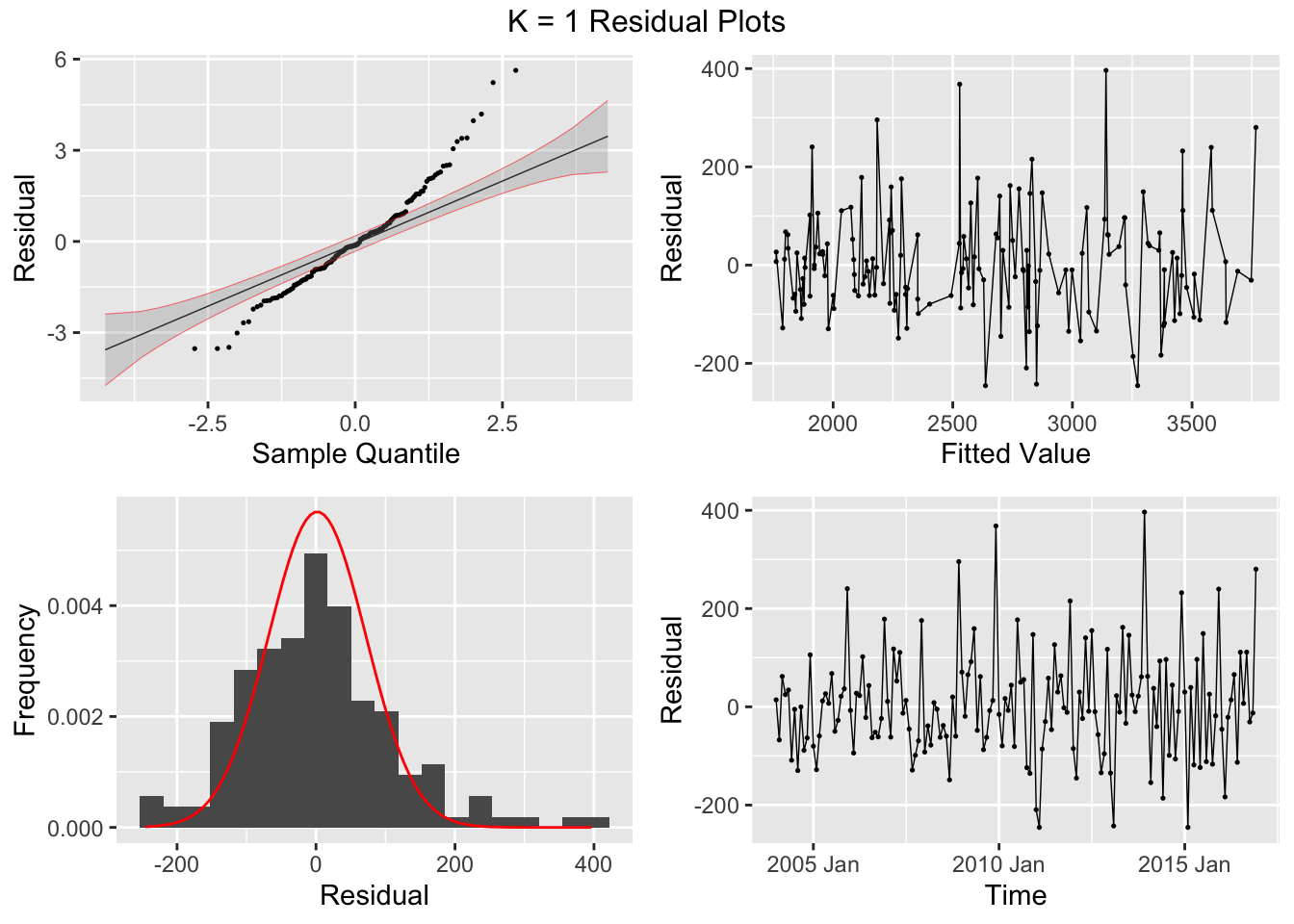

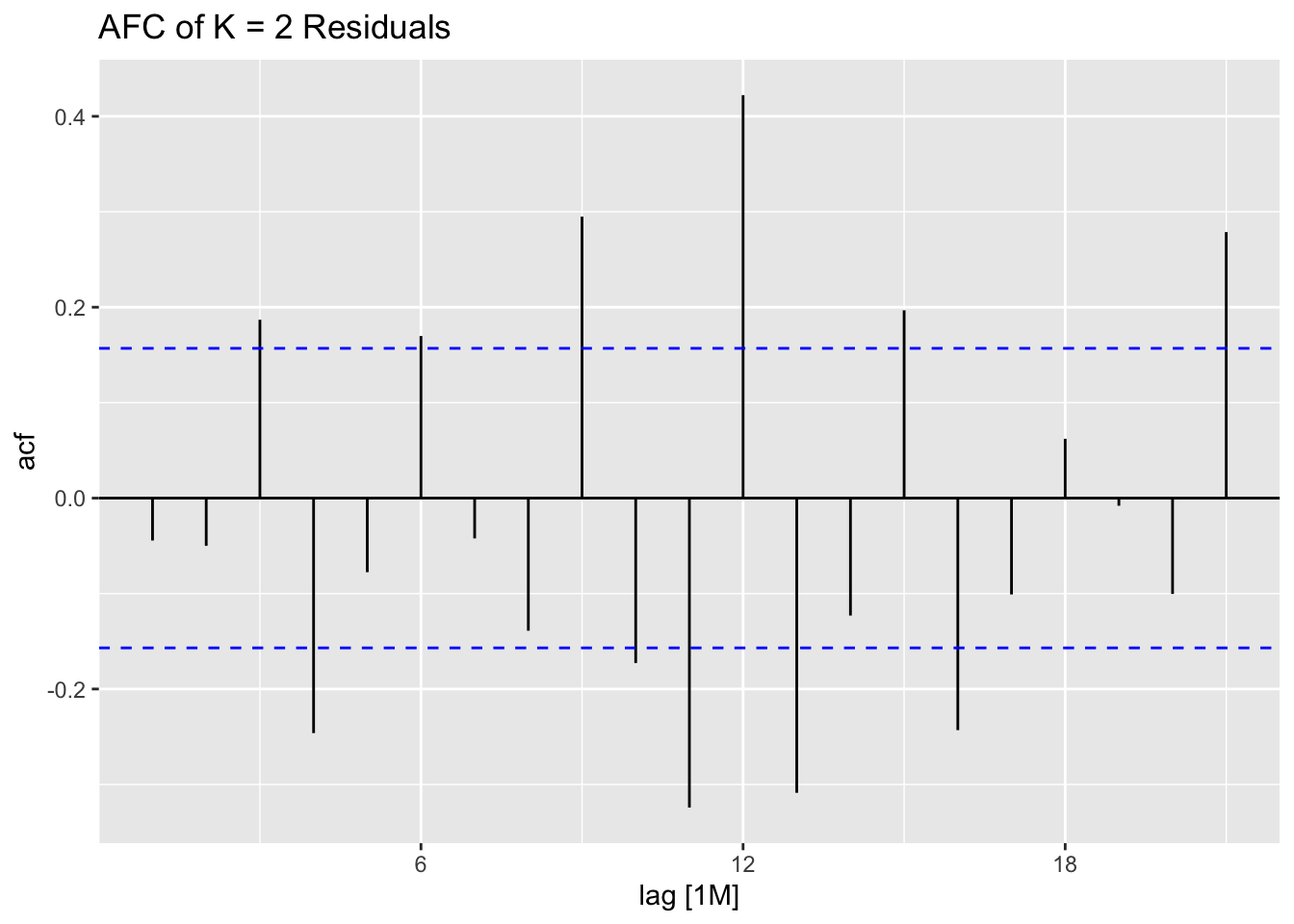

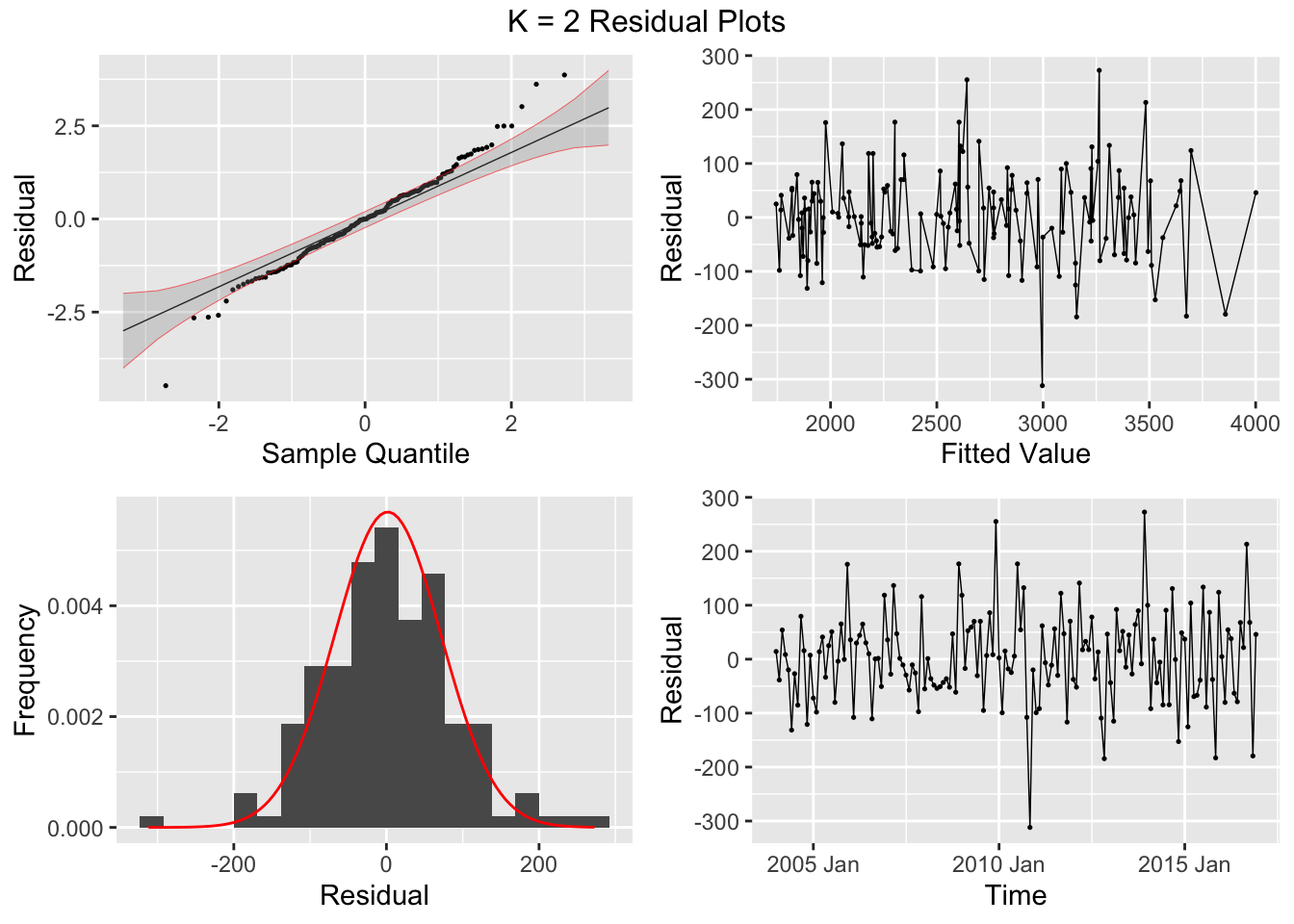

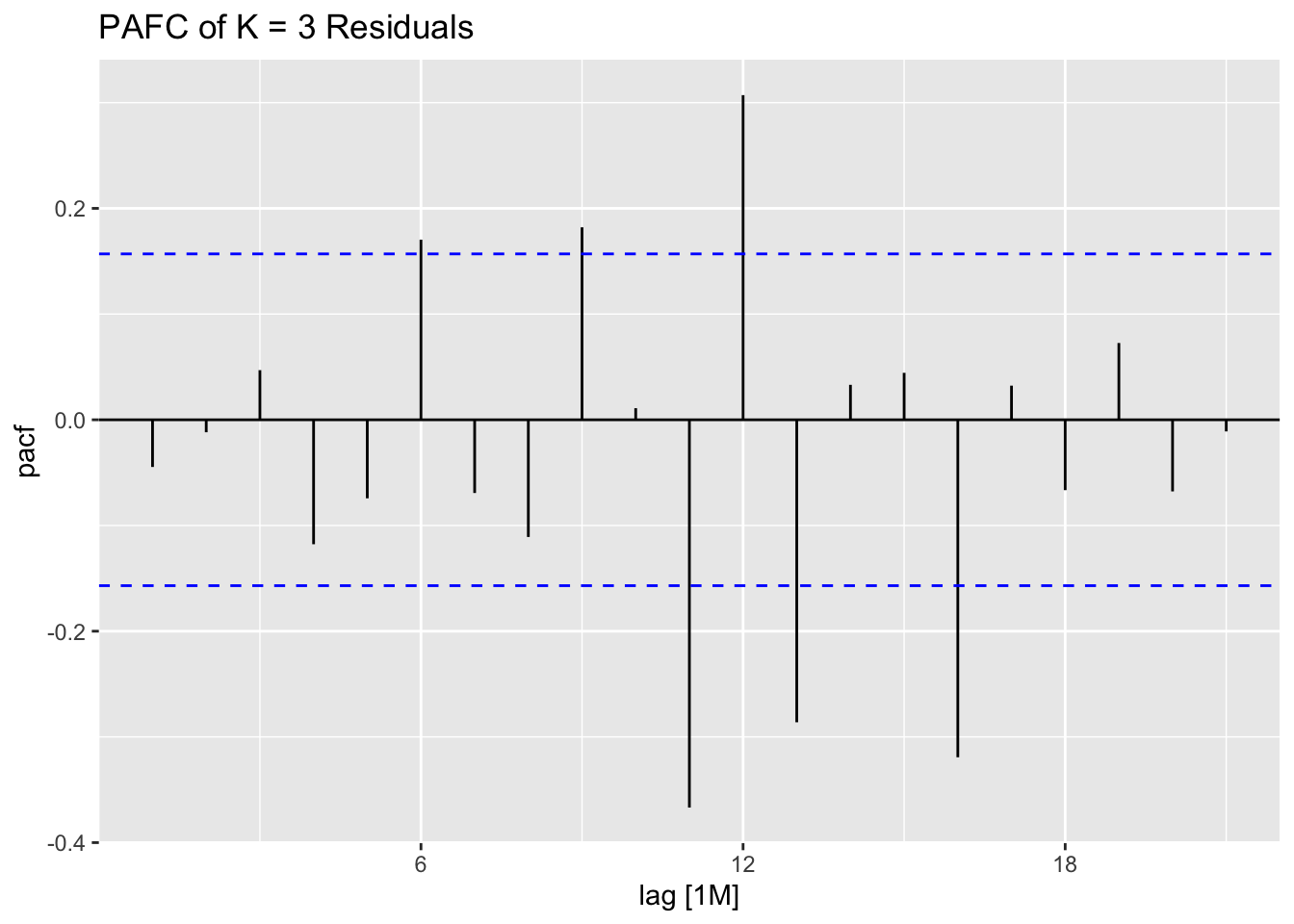

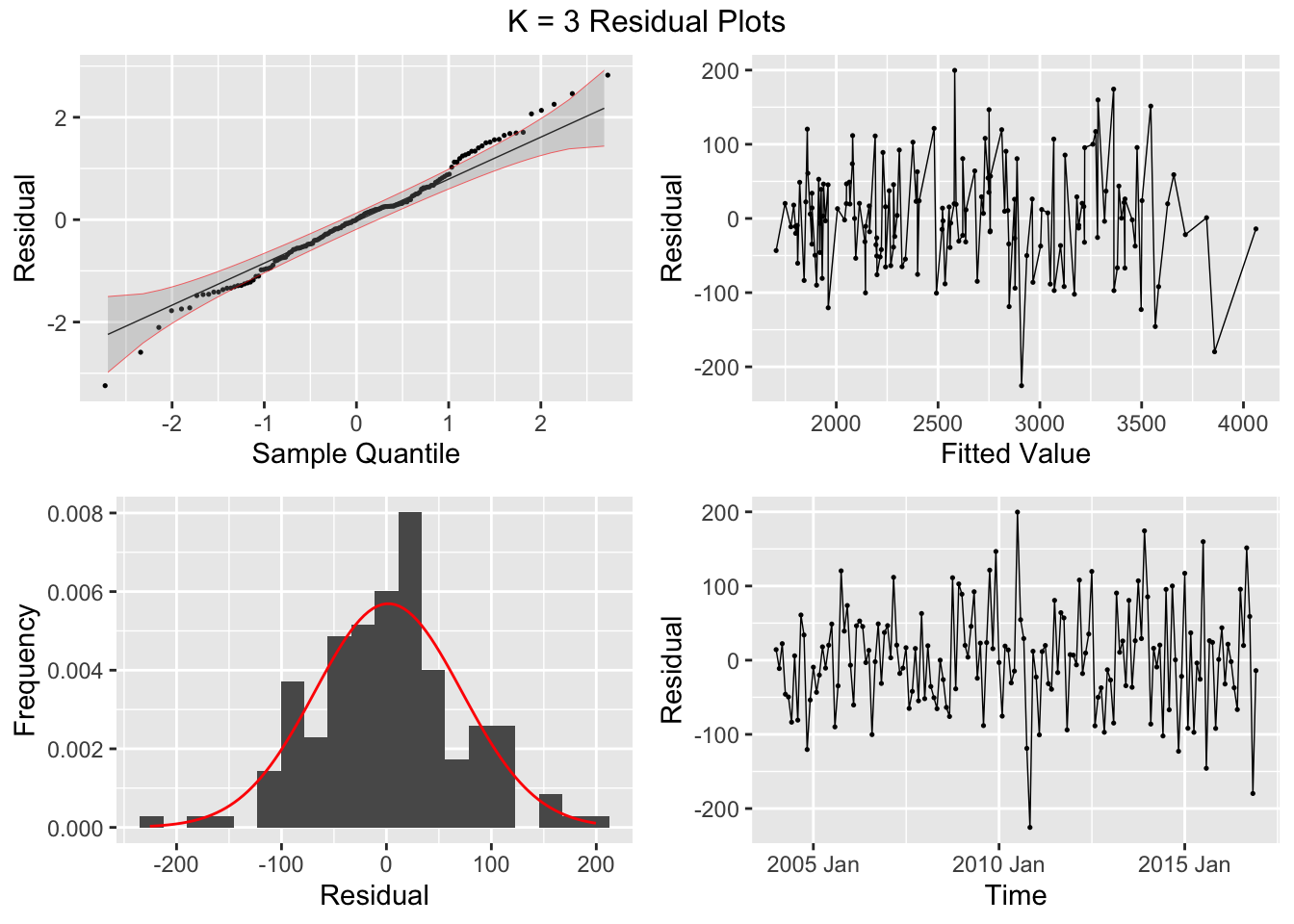

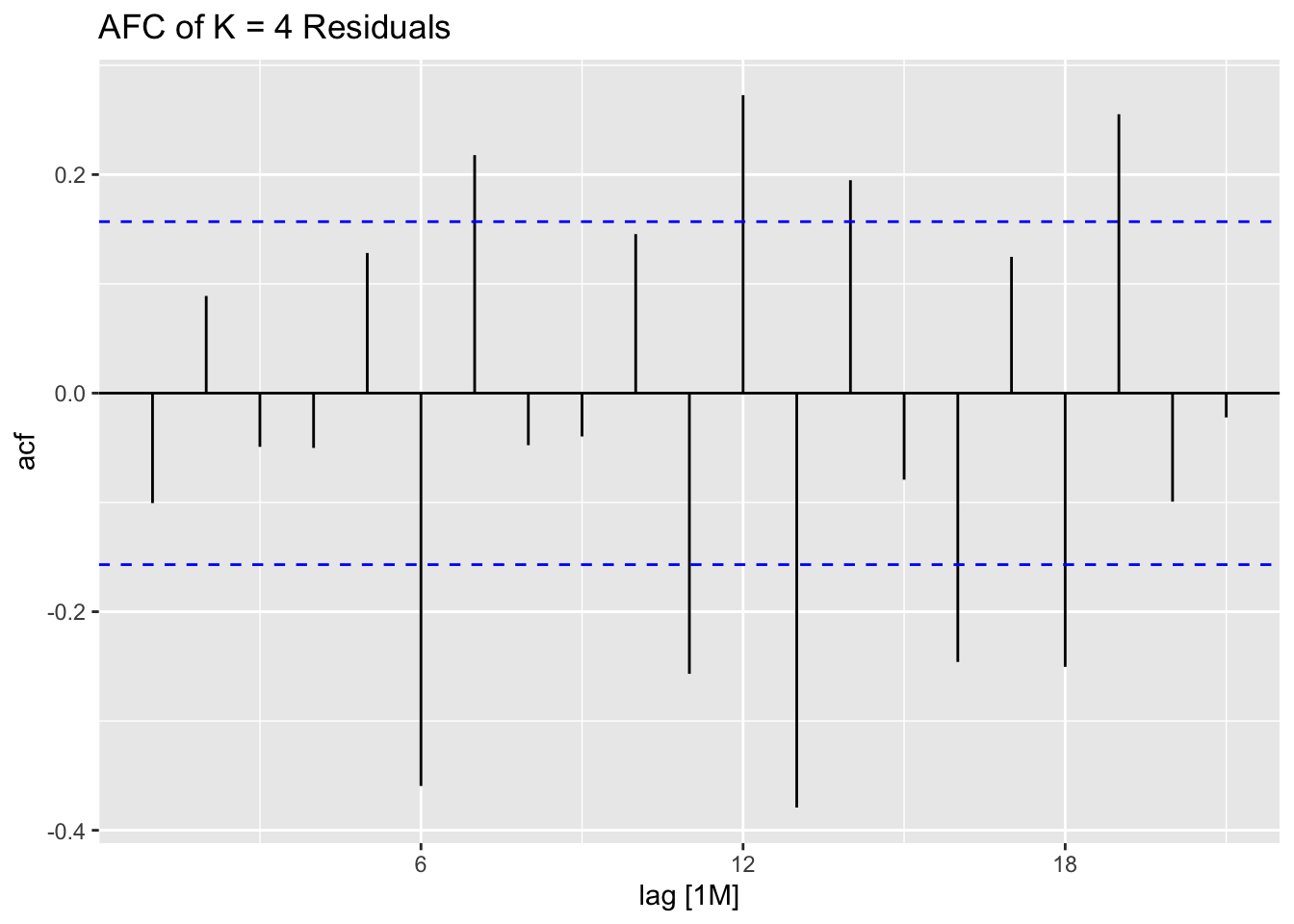

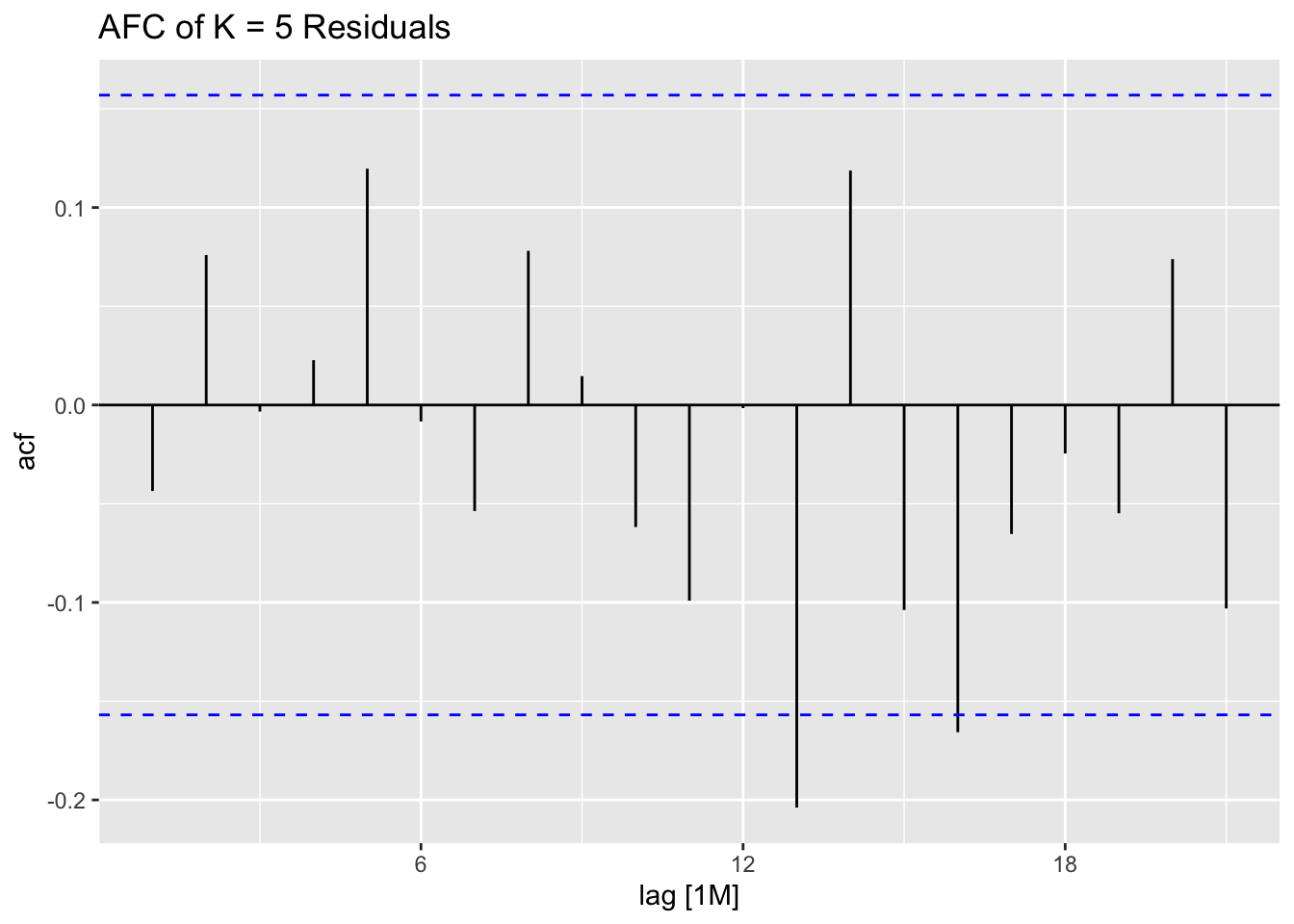

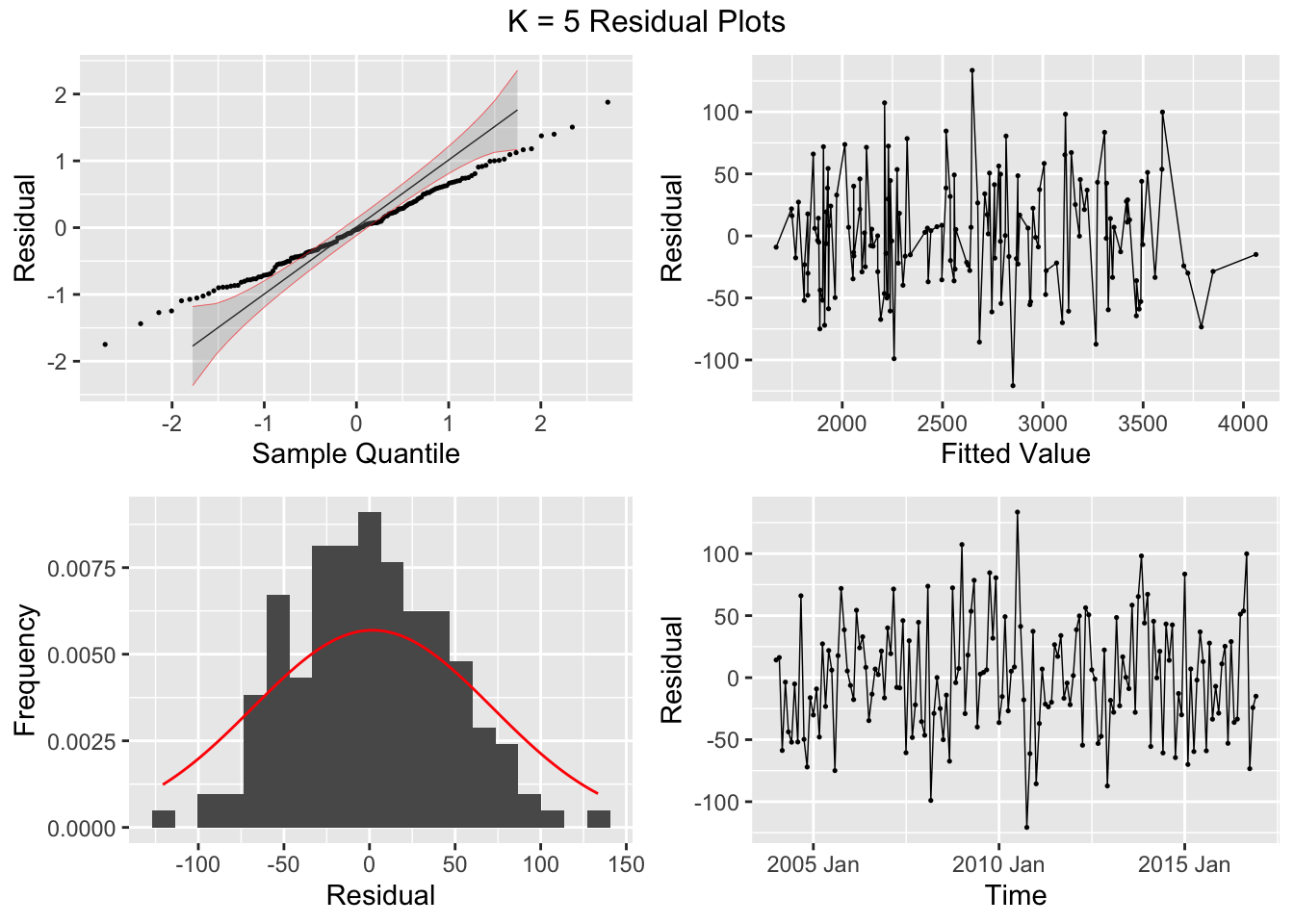

## 7 auto Test -123. 135. 123. -3.26 3.28 0.807 0.756 0.534augment(aus_cafe.arima) |> plot_residuals(title = c("auto",

"K = 1",

"K = 2",

"K = 3",

"K = 4",

"K = 5",

"K = 6"))## # A tibble: 7 × 3

## .model lb_stat lb_pvalue

## <chr> <dbl> <dbl>

## 1 arima1 0.311 0.577

## 2 arima2 0.314 0.576

## 3 arima3 0.317 0.573

## 4 arima4 1.61 0.205

## 5 arima5 0.301 0.583

## 6 arima6 0.0861 0.769

## 7 auto 0.0106 0.918

## # A tibble: 7 × 3

## .model kpss_stat kpss_pvalue

## <chr> <dbl> <dbl>

## 1 arima1 0.0637 0.1

## 2 arima2 0.0473 0.1

## 3 arima3 0.0564 0.1

## 4 arima4 0.0569 0.1

## 5 arima5 0.0902 0.1

## 6 arima6 0.0895 0.1

## 7 auto 0.0428 0.1

## NULL