5 Asset Allocation and Factors

The core of asset allocation is really about the inputs into mean-variance investing. You can add a lot of bells and whistles to this framework, but you’ll keep coming back to your capital market assumptions, such as expected returns, the risk of each asset or factor, and how the assets or factors move together (covariance). You are looking for a diversified set of risk premiums to collect together in a portfolio.

You’ve done this in FIN 412 when you found optimal portfolios along the efficient frontier. These are the portfolios that maximize expected return for a given level of risk. Or, equivalently. minimize risk for a given expected return. In this chapter, we’re going to focus on one particular aspect of this process: forecasting the equity risk premium, one of the most important returns that we need to consider. There are, of course, other returns, such as bond yields and other types of equities and factor premiums that you might be interested in. And you also need to estimate how assets and factors will move together. This last part often takes the form of a covariance matrix.

This chapter ends with some thoughts on how institutional investors might then delegate the investment decision. Let’s say that you’ve decided to have 35% of your endowment fund in U.S. equities, perhaps with a tilt towards value or small stocks. How might you select these managers? We discuss how MIT’s endowment goes about this process.

Our case study this week looks at the pension fund for Cook County, Illinois, their asset allocation decisions, and how these relate to their funding status.

Finally, some of this material makes its way into the Levels 2 and 3 CFA curriculum.

](images/04-triumph.jpg)

Figure 5.1: Equity investing is about risk tolerance and optimism. This book, which documents asset class returns across time and countries, came out in 2003 and we’ve seen the optimists triumph again after 2008 – 2009. Source: Princeton University Press

5.1 Importance of Asset Allocation

Let’s start by thinking about strategic asset allocation. Large institutional investors usually first decide on their long-run strategic choices, such as their allocation to U.S. stocks or bonds. Lately, these investors might also think more about their specific factor tilts, such as value vs. growth, but the big choices are still the big risk factors, such as the equity risk premium and deflation hedges, such as Treasuries. These choices gtive the fund their desired, typical portfolio consistent with the investment goals (around which one can implement tactical bets and security selection views). What are the steps?

- Set the strategic portfolio based on investment goals and long-term views.

- Vary asset allocation around strategic holdings based on tactical views on asset classes.

- Implement asset class positions based on security selection views.

Perhaps the most important consideration here is getting your asset-liability match correct. You’ll see this more in our case study. In short, when choosing your asset or factor allocation, you want to keep in mind why you are investing and when you’ll need the cash. You’ll want to be aware of something called sequence risk, or the risk of a big loss right when you need to spend down your investment.

How much does asset allocation matter? A lot, or a little, depending on how you ask the question. A very well-known paper in the asset allocator community attempts to ask these questions.

Let’s start with the first question: For a single fund, how much of the variability of returns across time is explained by policy (i.e. asset allocation to equities, bonds, etc.)? In other words, how much of a fund’s ups and downs does its policy benchmarks explain? To quote Ibbotson and Kaplan (2020), Figure 5.2:

illustrates the meaning of the time-series R2 with the use of a single fund from our sample. In this example, we regressed the 120 monthly returns of a particular mutual fund against the corresponding monthly returns of the fund’s estimated policy benchmark. Because most of the points cluster around the fitted regression line, the R2 is quite high. About 90 percent of the variability of the monthly returns of this fund can be explained by the variability of the fund’s policy benchmark.

The mutual fund in this example allocates to a variety of asset classes, such as stocks and bonds. Their returns over time are basically explained by this decision. The particular stocks and bonds that they bought don’t explain nearly as much.

](images/04-howmuch-fig1.png)

Figure 5.2: Source: Ibbotson and Kaplan (2020)

Note that this is a time series regression. It is asking does asset allocation explain a fund’s returns over time. The answer is - yes! The fact that a fund takes on equity risk, or small-stock risk, or value-stock risk, etc. explains their returns. We saw this when we ran regressions in class. The stocks you pick matter less than the fact that you pick stocks if I want to explain your returns over time, at least if you are a typical mutual fund or pension fund equity allocation. If you just pick one stock and that stock is GME, then this conclusion won’t hold.

But, what about comparing you to other funds? How much of the variation in returns among funds is explained by differences in policy? In other words, how much of the difference between two funds’ performance is a result of their policy difference? Again, quoting Ibbotson and Kaplan (2020), Figure 5.3:

is the plot of the 10-year compound annual total returns against the 10-year compound annual policy returns for the mutual fund sample. This plot demonstrates visually the relationship between policy and total returns. The mutual fund result shows that, because policy explains only 40 percent of the variation of returns across funds, the remaining 60 percent is explained by other factors, such as asset-class timing, style within asset classes, security selection, and fees.

](images/04-howmuch-fig2.png)

Figure 5.3: Source: Ibbotson and Kaplan (2020)

Policy return is what you would earn if the fund had just invested in a passive index that matched their stated policy, or strategic asset allocation. In other words, if all funds had the same benchmark, but invested actively, then 100% of return differences would be explained by things like security selection, rather than their benchmark. However, if all funds were passively managed, but had different benchmarks (i.e. different amounts invested in equities and bonds), then 100% of the return differences between funds would be explained by policy differences, so no fund would be making active decisions, like security selection or market timing. When looking at this small sample of funds, the authors found that 40% of the return differences across funds could be explained by different asset allocations, while the rest of the differences were because some funds were deviating more from their benchmarks.

5.2 Factors, Assets, and Risk

How do sophisticated investors view their portfolios? The details are beyond the scope of our brief time together, but just note that there is software that helps you see into your portfolio and find your exposures. This means that you can know what risks are lurking, assuming that you have access to all of your positions. Of course, any single fund manager will have their entire book in detail. However, if you are an allocator, you might not have access to your underlying hedge fund positions – in fact, you almost certainly won’t. In that case, you might need to infer your exposures from fund returns (which you will observe) and/or your funds’ general underlying strategies.

Here is a Twitter thread discussing how a large market maker like Citadel uses factors to figure out what risks they have on their giant trading book, so that they can hedge the unwanted risks away. Citadel is going to use their own, proprietary software, but there is software that you can buy that does this sort of thing too. We’ve also already seen similar software from Two Sigma and Blackrock’s Aladdin.

You can see how Two Sigma forecasts factor returns from their own research. They are trying to come up with a simple (parsimonious) list of factors that explains most of the returns that you see in a typical institutional portfolio. They use the phrase orthogonal a lot, which is just a math term that can be loosely translated as unrelated. They comment that premiums, such as equity risk, can be found across asset classes, not just in equities themselves. Which leads us to our next topic.

5.3 The Equity Risk Premium

In order to earn a return, you need to take risk. Let’s focus on estimating one particular risk factor – the equity risk premium. How can we forecast the return of this premium? Is that even possible? Should we look to historical performance? Or, can we come up with better forward-looking measures? Finally, if there’s a premium to be earned, how can we think about the risk inherent in the premium?

As we’ve discussed, many premiums come about because they are related to some kind of recession or macroeconomic risk. Here’s Illmanen (2015) on how expected returns (i.e. risk premiums) vary with the business cycle.

Empirical evidence suggests that near-term returns of risky assets are relatively high around business cycle troughs and relatively low around business cycle peaks. The two main explanations for the apparent countercyclic pattern in ex ante returns are (1) rationally time-varying risk premia and (2) irrational market mispricing. Time-varying risk premia may reflect variation in the amount of risk and/or market risk aversion. One compelling rational reason for boom–bust cycles is that risk aversion is wealth dependent and thus amplifies the gyrations in stock market valuations over time. Many people are more risk averse during recessions, which can create a feedback loop that pushes asset prices lower. (A similar feedback loop pushes already high prices higher, causing bubbles.) An alternative interpretation suggests that irrational fear or gloomy cash flow forecasts cause low market valuations during recessions. Market data cannot distinguish between rational and irrational stories, and both may have contributed to the observed return predictability.

So, when you’re coming up with your own estimates, you’ll want to consider where we stand. Our people fearful? Exhuberant? This will show up in the discount rate used for stocks. Are earnings expected to grow? Are they expected to grow faster than seems reasonable? This will show up in your cash flow estimates.

What has the equity risk premium looked like over time? Equity premiums are high around the world, but only over long periods. During the 2000s “Lost Decade,” equities underperformed bonds and cash. A decade of underperformance would matter for just about any investor.

But, over long time horizons, you earn more by allocating to equities, even if there are still risks. These risks are important! If investing in equities was “easy” from a risk standpoint, if it was obvious that you would make high returns, then these future high returns would disappear as everyone bought equities and pushed up the price.

However, this leaves us with a puzzle – why have long-run stock returns been so high? This is called the equity premium puzzle. Equity returns seem to be “too high,” relative to the risks of the equity market.

The equity premium puzzle is that relative to consumption – the representative agent (society) ultimately cares about what is finally consumed – the equity risk premium should be very low. In other words, overall consumption isn’t very volatile, even with the occasional recession, but stock returns are quite volatile. Understanding why the equity premium exists is important for understanding whether equities should have high returns in the future. Recommending an optimal allocation to equities necessitates understanding why equities deliver high returns over the long run, and whether we can stomach years (even decades!) of sub-par performance.

Here’s a quote from an article in the Financial Times about how equity markets around the world can disappoint for many, many years.

First of all, while it is true that in the long run equities tend to outperform — because investors are compensated for the extra risk they present — the “long run” can sometimes be as long as a person’s working life. After the Wall Street crash of 1929, it was not until 1954 that US stock market indices recovered their lost ground.

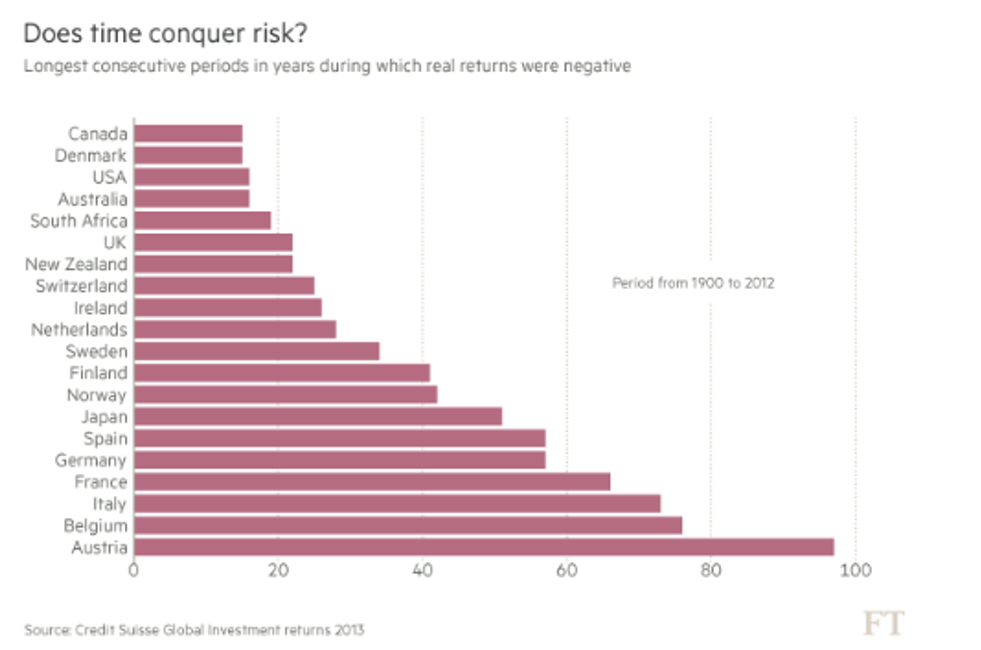

Definitive research by London Business School academics Elroy Dimson, Paul Marsh and Mike Staunton showed that the periods of negative returns endured in stock markets in countries that suffered military and political defeat in the 20th century could be far longer — more than 90 years in the case of Austria.

Source: How to Build a Portfolio Beyond Equities and Bonds (FT)

You can see the underperformance in Figure 5.4. For example, the UK has had a 20+ year period in the 20th Century where real equity returns were negative. As you know, the history of many countries in the 20th Century was violent and destructive. The positive returns that we see in the U.S. is at least partially a function of the U.S. being luckier than many.

Figure 5.4: Equity returns can be below the risk-free rate for a long-time.

Here’s another quote demonstrating the risks that emerge when we look across equity markets around the world. Anarkulova et al. (2020) write:

Although the U.S. historical record is reassuring, there is reason to be cautious when assessing downside risk. The U.S. return history is short. The commonly used sample from the Center for Research in Security Prices (CRSP) spans less than 100 years, which offers limited statistical information about what happens over 30-year horizons. Extending the U.S. sample backward only deepens concerns about survivorship bias [Brown, Goetzmann, and Ross (1995)], suggesting that the historical evidence from the U.S. may be overly optimistic relative to ex ante expectations. One need not look far for examples of long-term losses in other developed markets. At the close of 1989,Japan’s stock market was the largest in the world in terms of aggregate market capitalization. Over the subsequent 30 years from 1990 to 2019, an investment in the Nikkei 225 index produced returns (inclusive of dividends) of 9% in nominal terms and 21% in real terms. Japan’s experience is not unique, and several developed countries have realized worse performance or even complete stock market failure [see, e.g., Jorion and Goetzmann (1999)].

They conclude with a word of caution about the performance of equities.

Our analysis yields three primary findings. First, the long-term outcomes from diversified equity investments are highly uncertain. Based on the historical record of stock market performance in developed markets, the 5th percentile real payoff from a $1.00 buy-and-hold investment over 30 years is $0.47, whereas the 95th percentile is $23.14. This evidence stands in contrast to the conventional view that mean reversion in equity returns makes equity investing relatively safe at long horizons. Second, catastrophic investment outcomes are common even with a 30-year horizon, as the 1st percentile real payoff is $0.14 and the 10th percentile is just $0.85. An investor at age 35 saving for retirement, for example, only realizes one draw from the 30-year return distribution, and we estimate a 12.1% chance that this investor will lose relative to inflation. Third, the empirical findings based on the historical record of stock market performance across dozens of developed markets are notably different from those based on the historical U.S. experience. Estimates that rely solely on U.S. data suggest that long-term real investment losses are rare. The contrast in results highlights the importance of guarding against survivorship and easy data biases in assessing the distribution of distant payoffs and also has economically significant implications for optimal portfolio choice.

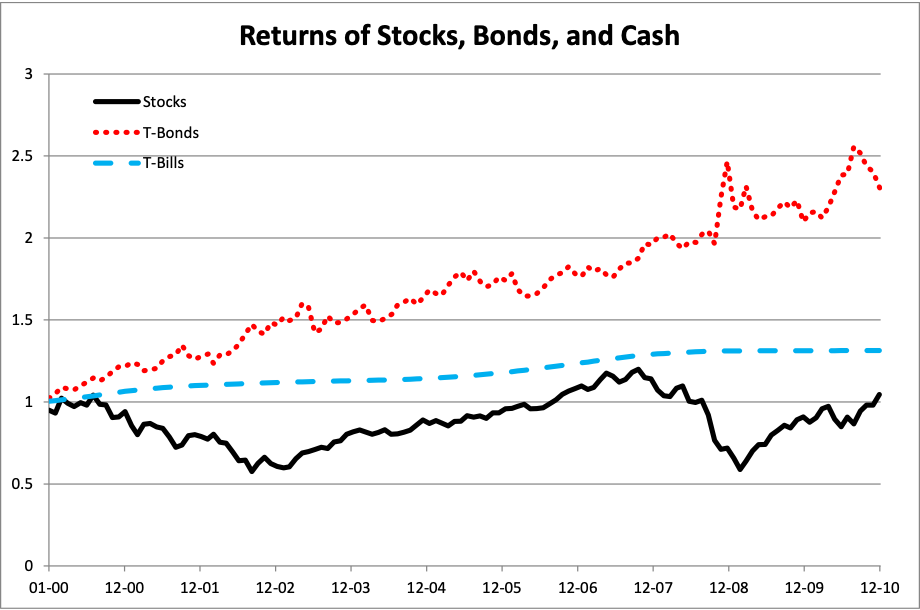

And, we’ve even had underperformance quite recently in U.S. equity markets. The 2000’s weren’t great for U.S. stocks as a whole. And, as the 2008 – 2009 financial crisis unfolded, investors were demanding higher returns in expectation for holding equities. The world seemed much more risky.

Figure 5.5: The 2000’s basically saw flat equity returns. It happens! This is the period that I was actively investing, so these flat returns are probably particularily salient to me. Source: Ang (2014)

More recent returns give a more optimistic view. As discussed in the previous section, the last decade has seen excellent U.S. equity returns. The U.S. has benefited from avoiding another Great Depression in 2008 – 2009, as well as the birth of entirely new industries and firms. Technological shifts have benefited the U.S. more than most, yet again. This does bode well for U.S. firms. But, does this actually reduce the expected equity premium, if we are realizing the U.S. firms might be less risky than others?

Together, I think these global studies answer, at least partially, the equity premium puzzle. U.S. stock returns to look at high, relative to the risks that we’ve faced, at when we look back into history. But, this history wasn’t inevitable. Other countries faced severe hardships that the U.S., even in our most difficult moments, didn’t face. We didn’t experience some of the rare events, some of the disasters, that other countries did, and our stock market did well as a result. High returns is exactly what you would expect if an asset transitions from “risky” to “not as risky.”

To be clear: I am not trying to dissuade you from taking on equity risk. We just want to remember that stonks don’t actually always go up, even it there is still an equity risk premium. The fact that they don’t always go up is what gives us the premium in the first place. No free returns.

5.3.1 Find the Equity Risk Premium

How should investors think about expected returns? What should investors do? Here are some tips:

- Use good statistical techniques. But, even then, we only have so much data to work with. Our ability to forecast is weak.

- Use economic models. For example, Damodaran’s valuation model that we’ll see.

- Be humble. Know that even if you do understand statistics and economics, that predicting returns is very difficult. Do not overestimate your own abilities and confuse luck with skill. This is called the self-attribution bias. It is easy to look at “lucky” investors, think they must know what they are doing, and then equate that luck with skill.

- When in doubt, invest as if markets can not be predicted. Index. Pay attention to fees. Rebalance. Diversify.

Aswath Damodaran has written a lot on how to find the equity risk premium, or the price of risk. I have posted an Excel spreadsheet with comments on Moodle that walk you through his work. He does this work because he wants us to think carefully about the WACC and how we value firms. But, remember, the CAPM cost of equity, which goes into WACC is just the expected return on the stock’s equity. And, to get that cost of equity, we need the equity risk premium. Risk, return, valuation – they are all linked together.

The key to his model is that this is just a DCF, but for the entire market. What cash flows are U.S. stocks expected to produce, in aggregate? How risky are these cash flows? With assumptions about these inputs, you can “solve” for the value of the entire market, just like you would for a single stock. You can also “reverse engineer” things and take the current price as given. Then, if you forecast cash flows, you can find the implied equity risk premium. This would be your expected return on U.S. stocks, above and beyond the current 10-Year Treasury. Damodaran’s method combines economic reasoning (the DCF model) with forecasts for inputs (e.g. earnings growth).

You can also find examples of asset class forecasts from GMO and AQR. GMO’s forecasts have been essentially negative for nearly a decade now, so while they certainly gotten some large over and underweight decisions correct, the last bull market has been painful. The AQR work has a discussion of stock-bond correlations, since correlations/covariances are also an important input into our asset allocation decision.

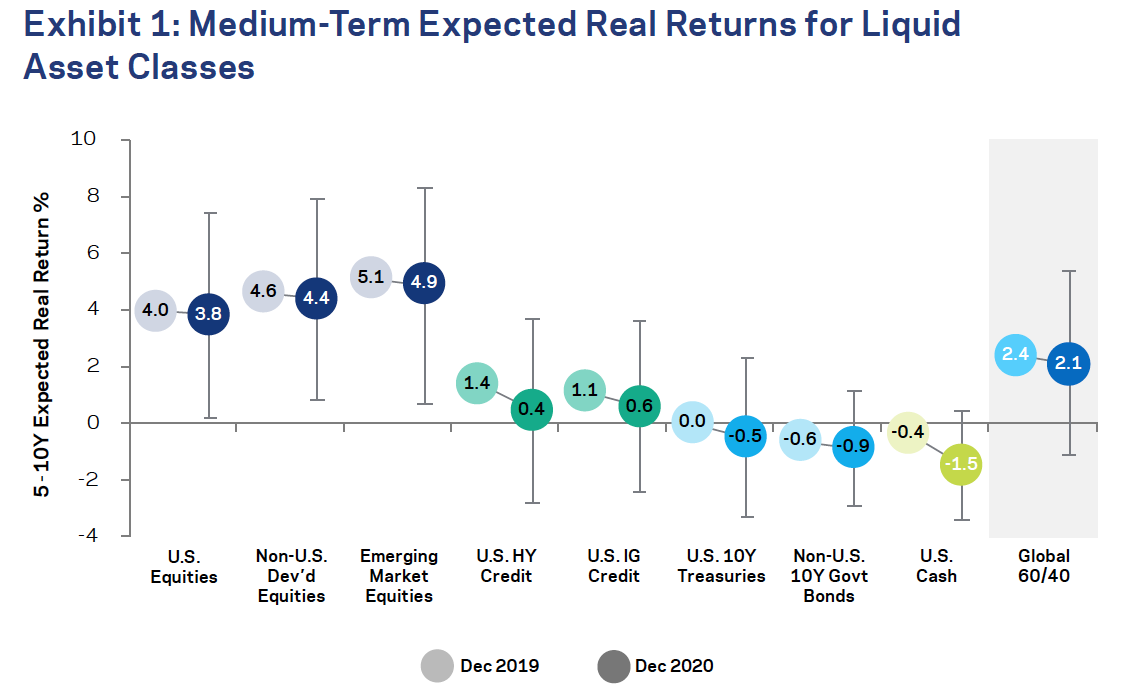

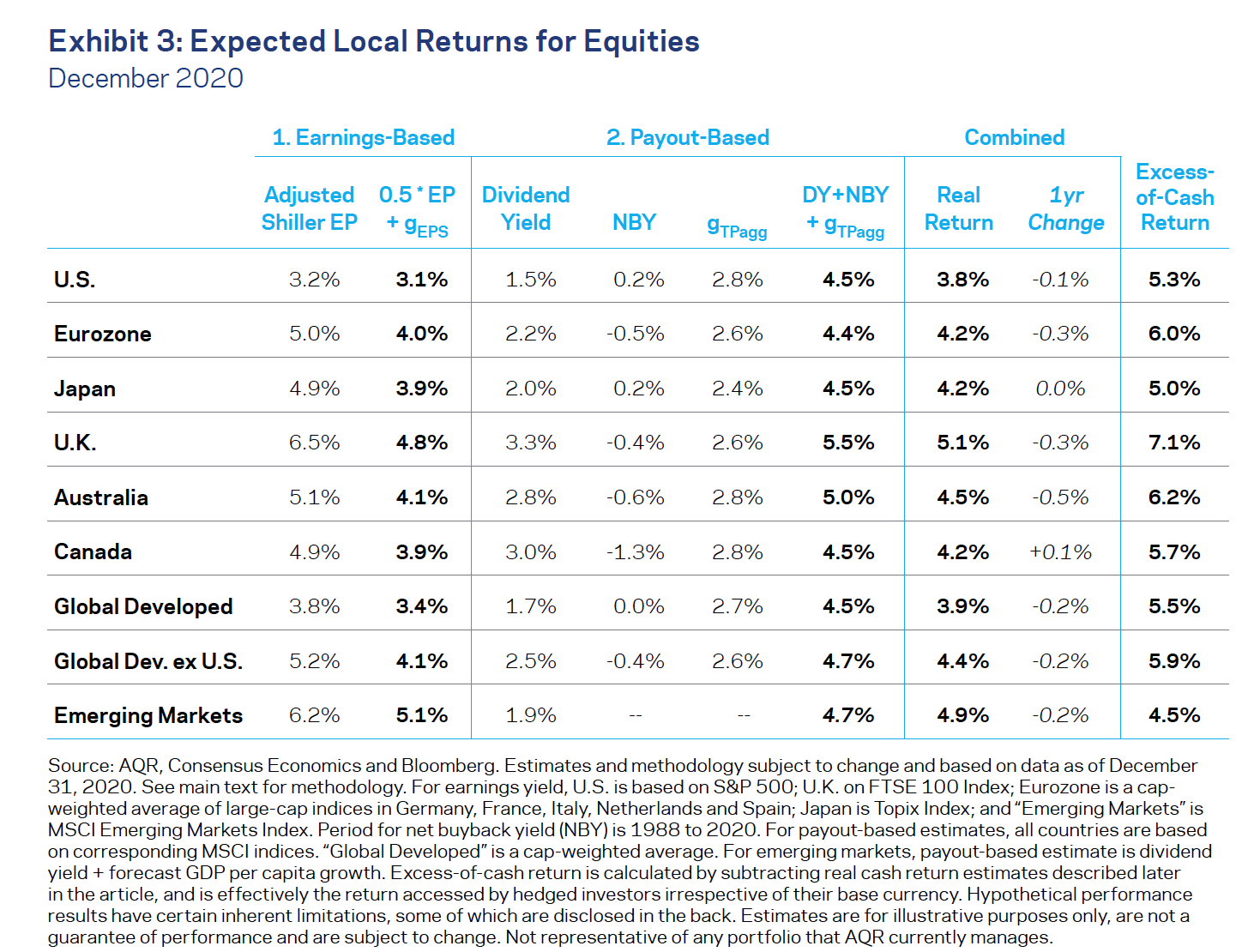

Here are the December 2020 forecasts for AQR, shown in Figure 5.6. They are more optimistic than GMO (like basically everyone), though they are still forecasting real returns that are lower than in the past.

Figure 5.6: Expected returns for major asset classes. Source: AQR

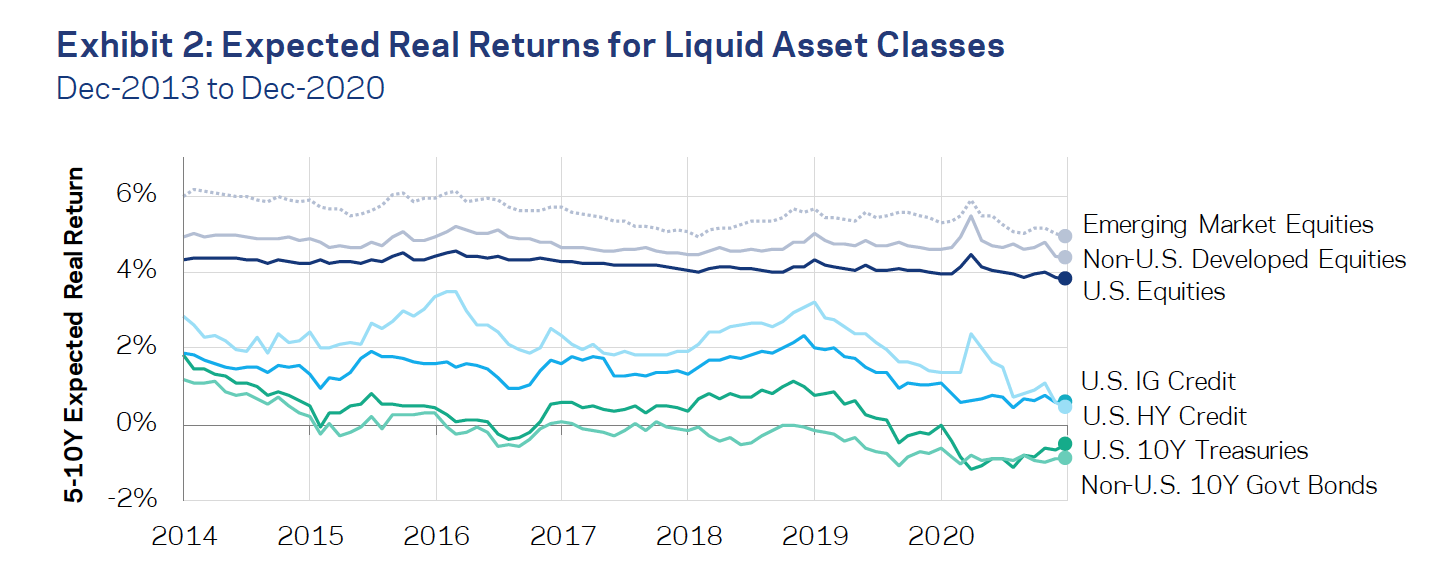

AQR has done this calculation over time, as well. Figure 5.7 shows how their forecasts have varied over time. No one is ever going to get the actual return right in a given year, except by luck.

Figure 5.7: Note how expected returns increased during COVID. Discount rates increasing is the same thing as expected returns increasing. Source: AQR

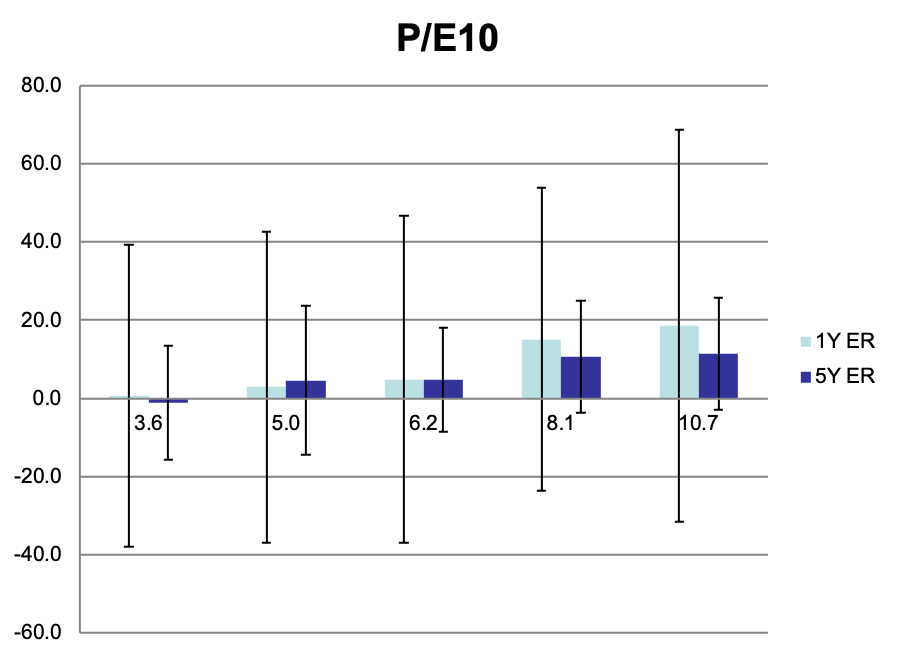

We use statistical, backwards-looking methods and see the uncertainty in the historical data. Figure 5.8 sorts U.S. equity markets (1926 – 2011) into five buckets, based on the E/P ratio (earnings yield) at the start of that year. Generally speaking, lower earnings yields (i.e. high P/E ratios) are related to lower returns over both the next year and next five years. But, the lines on the graph represent the spread of this historical data (+/- 2 standard deviations). So, even if low E/P markets have lower future returns on average, there is still a lot of uncertainty. The next year’s returns could still be very high! Market timing like this is very difficult. This relationship would get even weaker if you added the last nine years of data, since P/E ratios are currently high and market returns have also been high. Note that these relationships are a lot like the value premium that we’ve discussed.

Figure 5.8: Lower P/E ratios are related to higher future returns, especially over longer time horizons. But, the relationship comes with a great of uncertainty. Source: Ang (2014)

Turning back to more economics-based models, we can also forecast returns by thinking about the drivers of returns. Like with a DCF model, it helps to understand the economics behind where stock returns come from. We can decompose returns into their components, much like with the Gordon Growth model. We need to do just a little bit of math. Let’s start with the price-dividend ratio, \(\frac{P_t}{D_t}\), and think about how we can use it to separate returns next period (\(t+1\)) into three basic components – the dividend yield, dividend growth, and valuation changes:

\[E[R_{t+1}] = \frac{D_{t+1}}{P_t} + \frac{D_{t+1} - D_{t}}{D_t} + \frac{\frac{P_t+1}{D_t+1} - \frac{P_t}{D_t}}{\frac{P_t}{D_t}} + \text{small adjustment term}\] The first two terms are the dividend yield and the growth rate in dividends, respectively. You’ve seen this before, when you rearrange the Gordon Growth model to find expected returns. The third term is a little less concrete, as changes in the P/D ratio are related to things like perceptions of risk. For example, you’ll value a dollar of dividends more if you now perceive the dividends to be less risky. So, a reduction in risk increases returns next period.

Also, note that while we are using dividends, this same basic expression works for dividends + buybacks, earnings, free cash flows, etc. The main take-away are the three components help you think about where future returns might come from. Look at the Damodaran workbook for dividend (and buyback) and growth forecasts. Pick the ones you like. Then, do you think there will be any valuation adjustments? With those three numbers, you’ve arrived at an equity return forecast.

Figure 5.9 shows how AQR arrives at their forecasts using this same, basic method. They are using dividends, buybacks, and growth rates in the middle three columns to arrive at a return forecast across various countries and regions.

Figure 5.9: Decomposing returns into their various pieces. Source: AQR

5.4 Institutional Investors and Delegated Investing

Once in the dear dead days beyond recall, an out-of-town visitor was being shown the wonders of the New York financial district. When the party arrived at the Battery, one of his guides indicated some handsome ships riding at anchor. He said, “Look, those are the bankers’ and brokers’ yachts.” “Where are the customers’ yachts?” asked the naïve visitor. - Where are the Customers’ Yachts (1940)

We’ll end by talking about institutional investors themselves. These are the people making the asset allocation decisions and selecting the managers. They may or may not do some of their own security selection, but, typically, most of that is delegated. What incentives shape their decisions? What problems come up? How do they make decisions? And, perhaps, how should they make their selections?

The typical pension plan has 24% of their fund allocated, broadly, to alternatives, such as hedge funds. High-net worth individuals also use a lot of alternatives, though this could include private investments, such as real estate, as well as hedge funds.

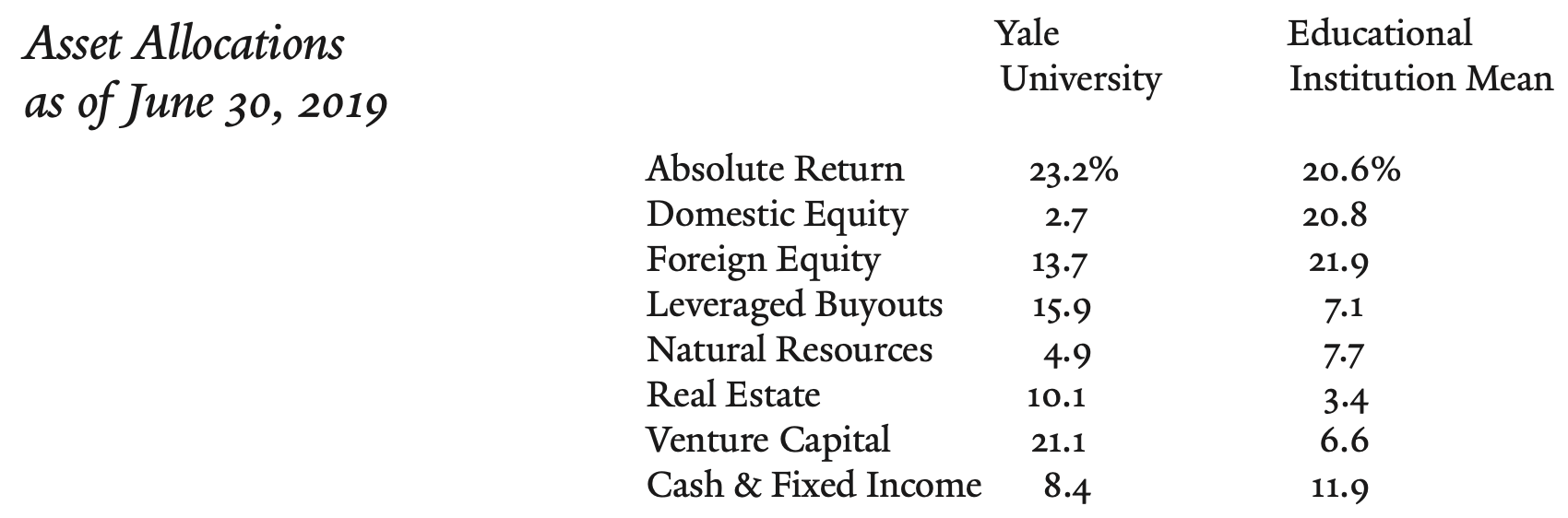

Figure 5.10: A lot of universities, such as Yale, investment in hedge funds, called Absolute Return here. Elon’s endowment also uses hedge funds. Source: 2019 Yale Endowment Report

When you delegate your investment decisions to outside managers, you create a principal-agent relationship, which can lead to principal-agent problems. The principal is the asset owner, like the University, who is allocating via their endowment board or office. The agents are the fund managers that they hire. To reduce conflicts that can arise between these parties, we should think a little bit about contracting and governance among allocators and fund managers. Much of this material comes from Ang (2014).

The two big problems are:

Adverse selection. The allocator can not directly observe the manager’s ability and might even have difficulty observing the actual strategy. This leads to both good and bad funds entering the market.

Moral hazard. The allocator is unlikely to be able to directly observe how hard the manager is working.

To mitigate these issues, the allocator and fund manager will negotiate a contract that aligns their interests, while being agreeable to both parties. This might mean outcome-based contracts, like performance fees, behavior-based contracts that restrict the types of investment that the manager can do, and non-linear, option-like contracts that payoff for the manager when they perform particularly well. You’ve seen these types of contracts already when we discussed hedge funds.

The investment world is also what economists call a repeated game, so reputation is very important. Due diligence visits and phone calls with existing investors are each part of the usual investment process.

5.4.1 Know Your Limitations (and Your Opportunities)

What would I do if I were an institutional investor, allocating capital to meet my organization’s goals? My default would always be to prefer the cheap alternative. Some managers have skill, but it might take a decade or more of returns to show this statistically. By then, it would be too late as flows chase performance and whatever edge the manager had disappears. Markets also change, so an edge in one market cycle might not matter as much in another. To catch a manager earlier, you have to rely on understanding their process, whether or not they can actually do what they say they can, and other difficult to assess factors. It is easy to fool yourself into thinking that you or another manager that you’ve met with has an sustainable edge.

So, I would use cheap, easy-to-understand risk exposures for the bulk of my assets. Some factor exposures might be difficult to get in public markets, so we can keep an open mind here and see what the world of private equity and venture capital might offer in Chapter 6. But, in the end, I would likely spend most of my day doing absolutely nothing.

But, what if you wanted to do more? And, what if your institutional capabilities suggested that you could? What might those capabilities be? Here are a few characteristics of institutional investors that might want to try to do more than the basics:

Stable capital. Few clients and, in fact, maybe only one client. Little to no outside interference (e.g. from political entities, like a state legislature). No real possibility of a run on your capital. These helps in two-sided markets, as the funds that you invest in know that your hand won’t be forced. This description fits many larger university endowments and family offices.

Network of outside funds. Essentially, you need to know people. There’s no real way to find talented managers who are just starting without having that network in place. Venture capital and private equity work like this too. It’s why I’m suspicious of some of the newer vehicles that advertise more complex strategies for “everyday” people. Why weren’t they able to raise capital from the usual pool of sophisticated investors? Why do they need my money?

Knowledge of strategies. Why do certain strategies make money? When will they make money?

You can always use larger, more institutionally friendly hedge funds and private equity firms to get you factor exposures that you think might be difficult to come by using more passive alternatives, if you think that these exposures outweigh the fees. With this mindset, you aren’t focused on alpha, but are instead trying to put together a portfolio of risk premiums.

Figure 5.11: Picking hedge fund managers who have thrived using a niche strategy, but after they have grown their AUM.

You can also, of course, chase returns and allocate to funds and strategies that have a track record of strong performance, with the hope that this alpha continues into the future. I think that the evidence says that this is tough to do, but you can try. Best of luck!

The hard path is to look for small funds. Funds with managers who are not well known, who might have been overlooked. These are, somewhat optimistically, sometimes called emerging managers. These are managers without a long track record, or perhaps just a track record of trading their own money. Some larger university endowments will attempt to find these managers using their alumni network and stable capital base. For example, here’s an interview from 2014 with the investment team at MIT’s Endowment on how they select managers.

When evaluating managers, the MIT team focuses on judgment and process, the risks the manager takes (e.g. the factors they are exposed to), and the alignment of incentives.

We focus on evaluating opportunities that are within our circle of competence, which is bounded by our core investment principles. The nature of our research really boils down to: developing conviction in the quality of an investor’s judgment; understanding the risks to which our capital is exposed; and ensuring that the right structure and alignments exist to serve as the foundation for a long-term partnership. On a practical level, we spend our time conducting in-person meetings; reading any relevant materials, such as letters, investment case studies, or company materials; conducting reference calls; and analyzing historical data.

Again, you need to focus on the process of the manager. This is difficult if you don’t really understand the strategy and why it makes money (and when it doesn’t). For example, if you are looking for a long volatility fund to hedge risk in your portfolio, you need to think carefully about how these funds make money, how they structure their trades, and should understand option “greeks” basics to at least get a handle on their strategy.

Over time, we have learned that great investors tend to be more focused on process than on outcomes. So, we try to follow this principle as well. The idea goes that if the process is correct, results will take care of themselves over the long term. Of course, a track record, if presented over a long period of time, is an important check on whether what should work is working. But we have to be cautious about this, as even great managers have multi-year periods of meaningful underperformance – there is a great Eugene Shahan article from 1985 about how plenty of investors with great long-term track records looked mediocre in any given year and underperformed for three or more years in a row in many cases.

Finally, they meet with very young managers who have smaller AUM. If you want to catch a manager before they become successful, then you need to look at unconventional strategies and funds.

One thing that many people remark on when they meet us the first time is that we are very different from their conception of what a traditional institutional investor would be. They are surprised to hear we spend a lot of time meeting with managers in their 20s and 30s, that we are frequently the first or only institutional investor in a firm, that a meaningful number of our firms are one- and two-person shops, and that we are very content with unconventional firms and strategies. We have made a deliberate effort to invest in un-institutional firms because many investors with exceptional long-term track records have been unconventional and un-institutional.

MIT has an emerging manager program where they select funds with short track records and small AUM. One of their directors has a brief article on the types of funds they have selected with this program.

I try to use the factor thinking we’ve discussed to place managers and strategies into some kind of bucket. Sure, there are managers that might not fit a particular definition, but most get their returns from some kind of risk premiums.