B Inference Examples

This appendix is designed to provide you with examples of the five basic hypothesis tests and their corresponding confidence intervals. Traditional theory-based methods as well as computational-based methods are presented. You can also use this appendix as a way to check for understanding of which statistical graphic is most appropriate given the problem set-up.

Needed packages

library(dplyr)

library(ggplot2)

library(mosaic)

library(knitr)

library(readr)B.1 Inference mind map

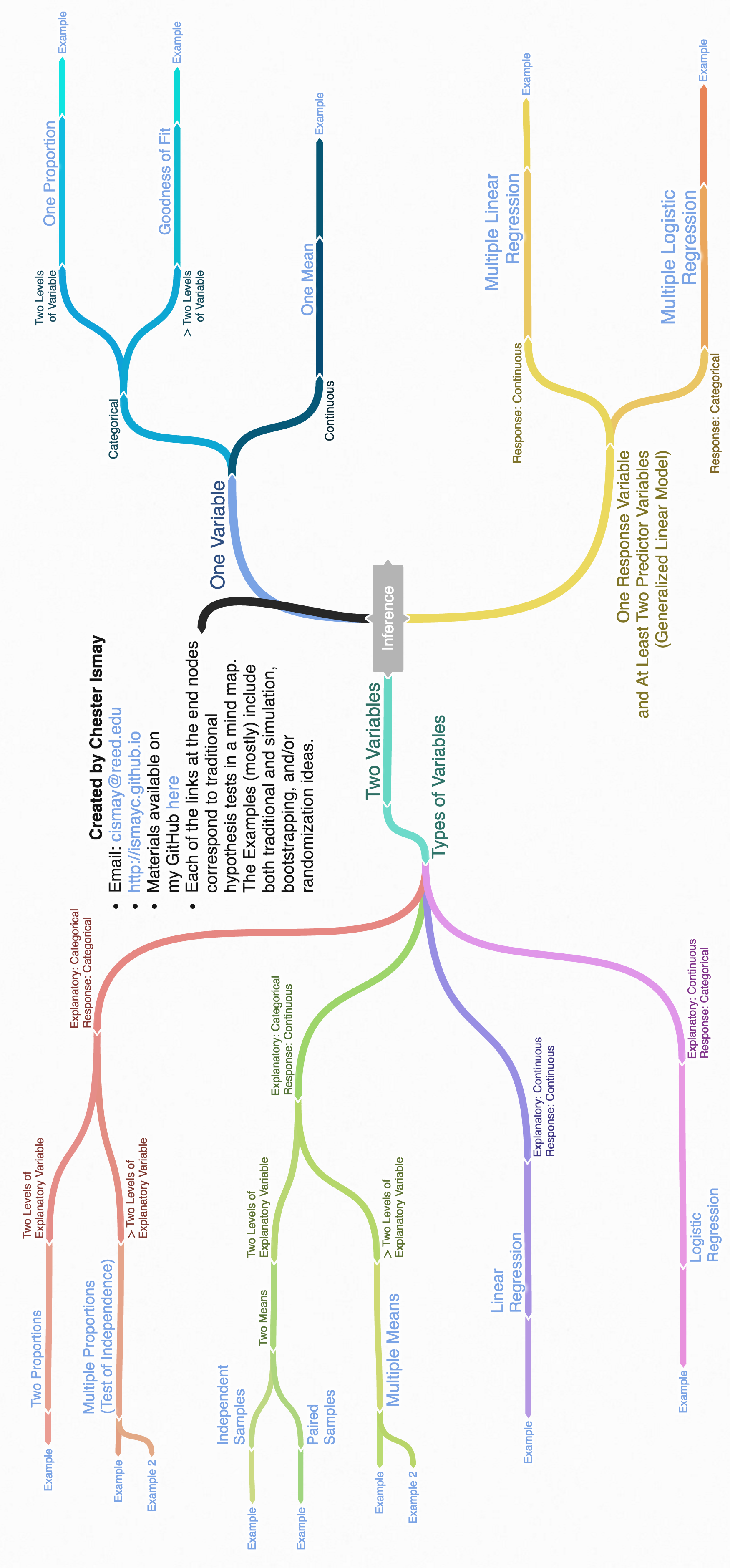

To help you better navigate and choose the appropriate analysis, we’ve created a mind map on http://coggle.it available here and below.

Figure B.1: Mind map for Inference

B.2 One mean

B.2.1 Problem statement

The National Survey of Family Growth conducted by the Centers for Disease Control gathers information on family life, marriage and divorce, pregnancy, infertility, use of contraception, and men’s and women’s health. One of the variables collected on this survey is the age at first marriage. 5,534 randomly sampled US women between 2006 and 2010 completed the survey. The women sampled here had been married at least once. Do we have evidence that the mean age of first marriage for all US women from 2006 to 2010 is greater than 23 years? (Tweaked a bit from Diez, Barr, and Çetinkaya-Rundel 2014 [Chapter 4])

B.2.2 Competing hypotheses

B.2.2.1 In words

Null hypothesis: The mean age of first marriage for all US women from 2006 to 2010 is equal to 23 years.

Alternative hypothesis: The mean age of first marriage for all US women from 2006 to 2010 is greater than 23 years.

B.2.2.2 In symbols (with annotations)

- \(H_0: \mu = \mu_{0}\), where \(\mu\) represents the mean age of first marriage for all US women from 2006 to 2010 and \(\mu_0\) is 23.

- \(H_A: \mu > 23\)

B.2.2.3 Set \(\alpha\)

It’s important to set the significance level before starting the testing using the data. Let’s set the significance level at 5% here.

B.2.3 Exploring the sample data

#download.file("http://ismayc.github.io/teaching/sample_problems/ageAtMar.csv",

# destfile = "data/ageAtMar.csv",

# method = "curl")

ageAtMar <- read_csv("data/ageAtMar.csv")age_summ <- ageAtMar %>%

summarize(sample_size = n(),

mean = mean(age),

sd = sd(age),

minimum = min(age),

lower_quartile = quantile(age, 0.25),

median = median(age),

upper_quartile = quantile(age, 0.75),

max = max(age))

kable(age_summ)| sample_size | mean | sd | minimum | lower_quartile | median | upper_quartile | max |

|---|---|---|---|---|---|---|---|

| 5534 | 23.44 | 4.721 | 10 | 20 | 23 | 26 | 43 |

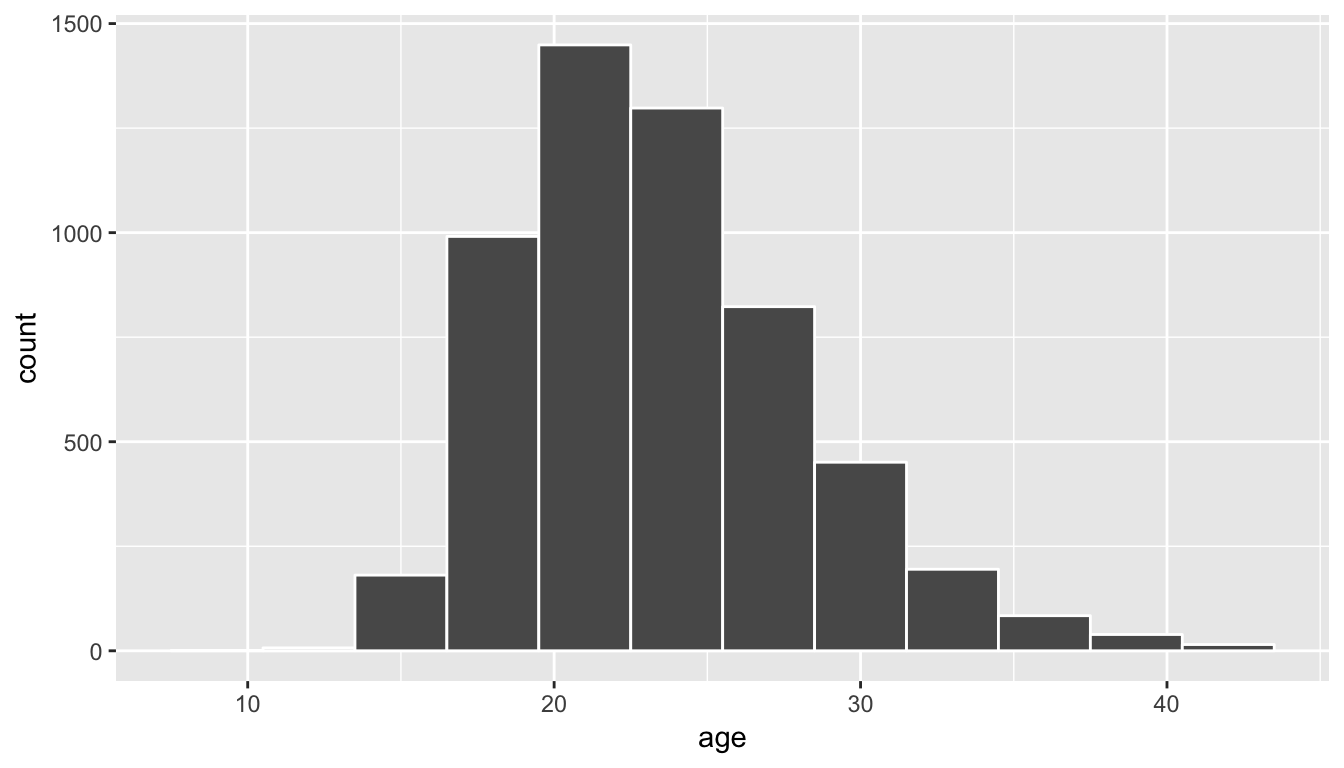

The histogram below also shows the distribution of age.

ageAtMar %>% ggplot(aes(x = age)) +

geom_histogram(binwidth = 3, color = "white")

B.2.3.1 Guess about statistical significance

We are looking to see if the observed sample mean of 23.4402 is statistically greater than \(\mu_0 = 23\). They seem to be quite close, but we have a large sample size here. Let’s guess that the large sample size will lead us to reject this practically small difference.

B.2.4 Non-traditional methods

B.2.4.1 Bootstrapping for hypothesis test

In order to look to see if the observed sample mean of 23.4402 is statistically greater than \(\mu_0 = 23\), we need to account for the sample size. We also need to determine a process that replicates how the original sample of size 5534 was selected.

We can use the idea of bootstrapping to simulate the population from which the sample came and then generate samples from that simulated population to account for sampling variability. Recall how bootstrapping would apply in this context:

- Sample with replacement from our original sample of 5534 women and repeat this process 10,000 times,

- calculate the mean for each of the 10,000 bootstrap samples created in Step 1.,

- combine all of these bootstrap statistics calculated in Step 2 into a

boot_distnobject, and - shift the center of this distribution over to the null value of 23. (This is needed since it will be centered at 23.4402 via the process of bootstrapping.)

set.seed(2017)

mu0 <- 23

shift <- mu0 - age_summ$mean

null_distn_one_mean <- do(10000) *

resample(ageAtMar, replace = TRUE) %>%

mutate(age = age + shift) %>%

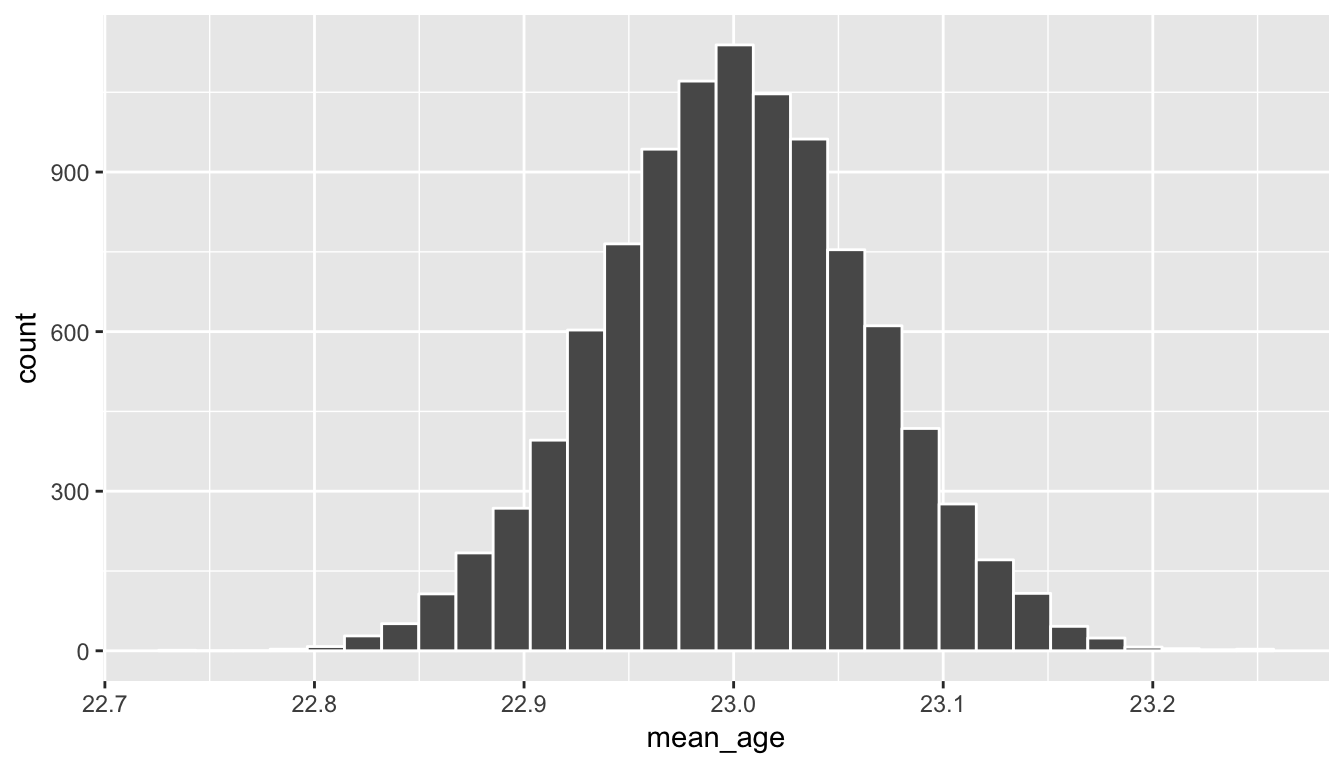

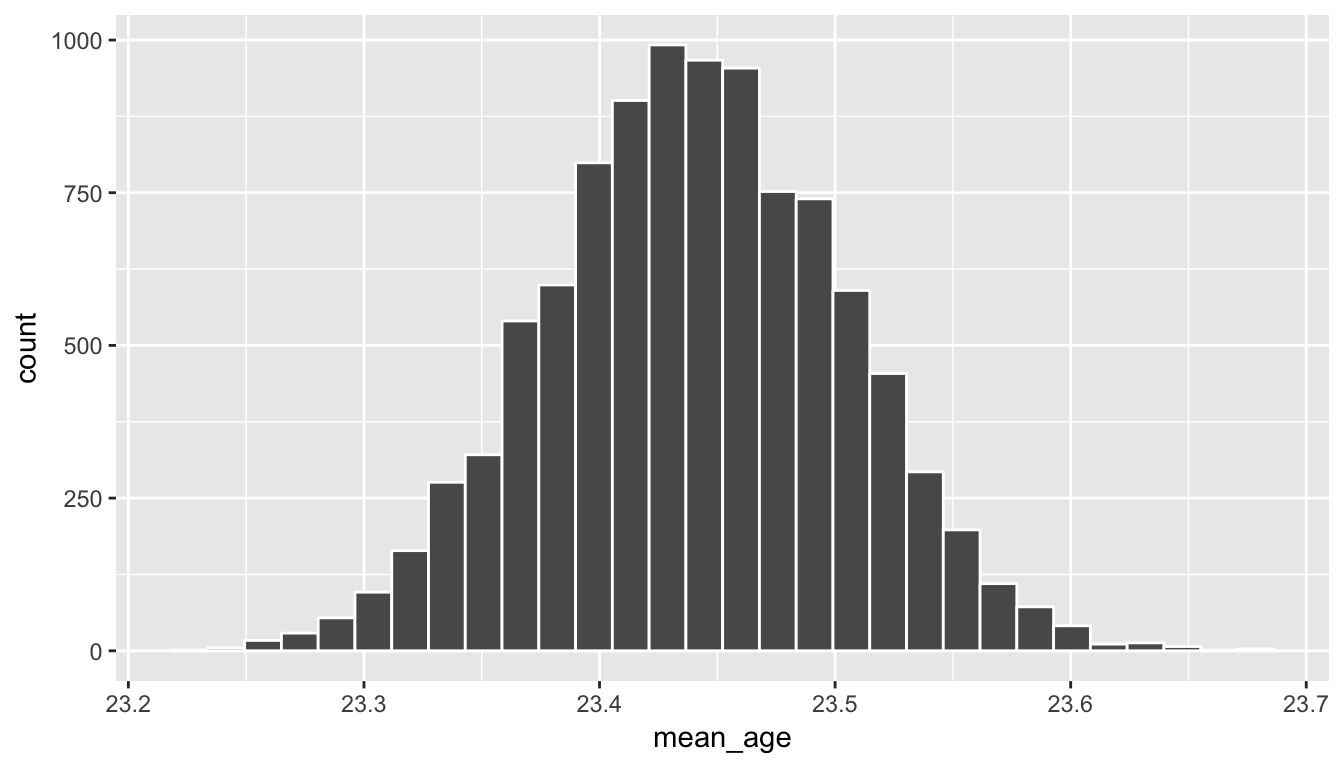

summarize(mean_age = mean(age))ggplot(null_distn_one_mean, aes(x = mean_age)) +

geom_histogram(bins = 30, color = "white")

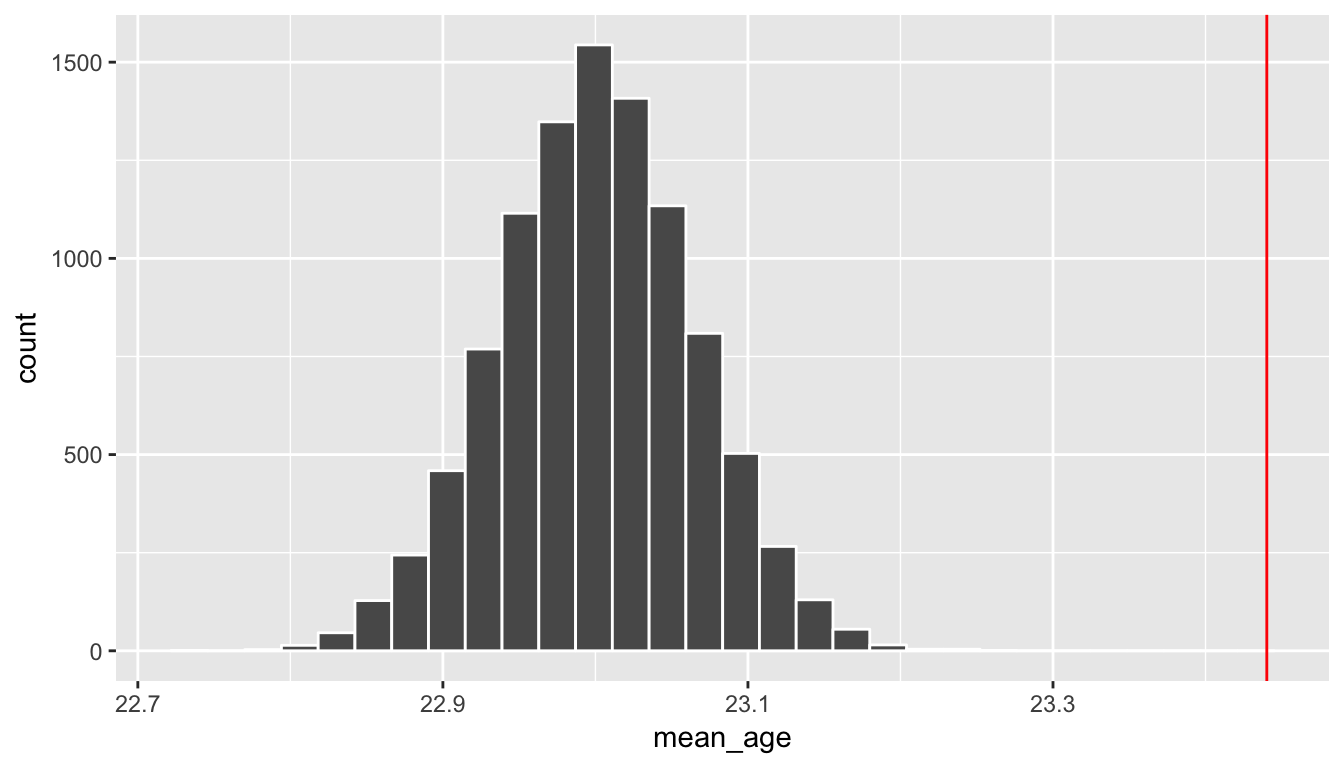

We can next use this distribution to observe our \(p\)-value. Recall this is a right-tailed test so we will be looking for values that are greater than or equal to 23.4402 for our \(p\)-value.

obs_mean <- age_summ$mean

ggplot(null_distn_one_mean, aes(x = mean_age)) +

geom_histogram(bins = 30, color = "white") +

geom_vline(color = "red", xintercept = obs_mean)

B.2.4.1.1 Calculate \(p\)-value

pvalue <- null_distn_one_mean %>%

filter( mean_age >= obs_mean ) %>%

nrow() / nrow(null_distn_one_mean)

pvalue[1] 0So our \(p\)-value is 0 and we reject the null hypothesis at the 5% level. You can also see this from the histogram above that we are far into the tail of the null distribution.

B.2.4.2 Bootstrapping for confidence interval

We can also create a confidence interval for the unknown population parameter \(\mu\) using our sample data using bootstrapping. Note that we don’t need to shift this distribution since we want the center of our confidence interval to be our point estimate \(\bar{x}_{obs} = 23.4402\).

boot_distn_one_mean <- do(10000) *

resample(ageAtMar, replace = TRUE) %>%

summarize(mean_age = mean(age))ggplot(boot_distn_one_mean, aes(x = mean_age)) +

geom_histogram(bins = 30, color = "white")

boot_distn_one_mean %>% summarize(lower = quantile(mean_age, probs = 0.025),

upper = quantile(mean_age, probs = 0.975)) lower upper

1 23.32 23.56We see that 23 is not contained in this confidence interval as a plausible value of \(\mu\) (the unknown population mean) and the entire interval is larger than 23. This matches with our hypothesis test results of rejecting the null hypothesis in favor of the alternative (\(\mu > 23\)).

Interpretation: We are 95% confident the true mean age of first marriage for all US women from 2006 to 2010 is between and .

B.2.5 Traditional methods

B.2.5.1 Check conditions

Remember that in order to use the shortcut (formula-based, theoretical) approach, we need to check that some conditions are met.

Independent observations: The observations are collected independently.

The cases are selected independently through random sampling so this condition is met.

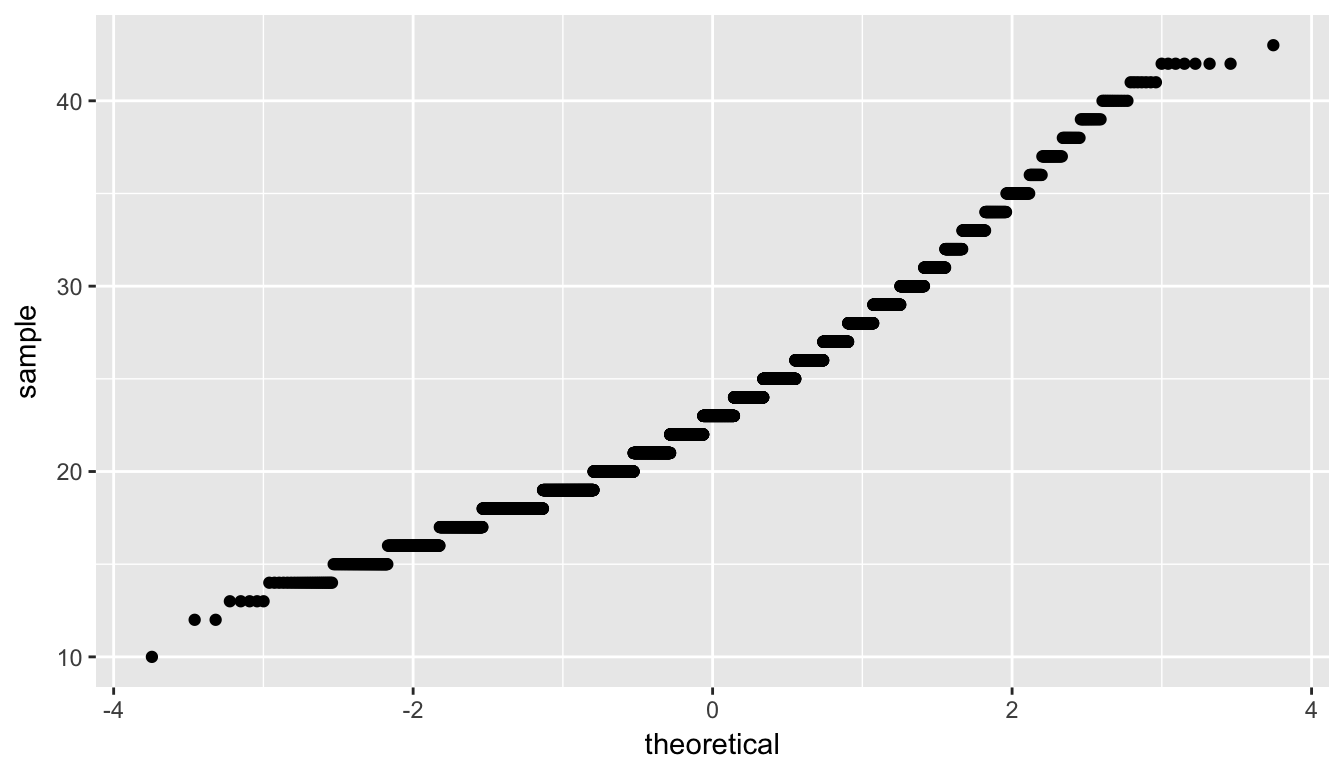

Approximately normal: The distribution of the response variable should be normal or the sample size should be at least 30.

The histogram for the sample above does show some skew.

The Q-Q plot below also shows some skew.

ggplot(data = ageAtMar, mapping = aes(sample = age)) +

stat_qq()

The sample size here is quite large though (\(n = 5534\)) so both conditions are met.

B.2.5.2 Test statistic

The test statistic is a random variable based on the sample data. Here, we want to look at a way to estimate the population mean \(\mu\). A good guess is the sample mean \(\bar{X}\). Recall that this sample mean is actually a random variable that will vary as different samples are (theoretically, would be) collected. We are looking to see how likely is it for us to have observed a sample mean of \(\bar{x}_{obs} = 23.4402\) or larger assuming that the population mean is 23 (assuming the null hypothesis is true). If the conditions are met and assuming \(H_0\) is true, we can “standardize” this original test statistic of \(\bar{X}\) into a \(T\) statistic that follows a \(t\) distribution with degrees of freedom equal to \(df = n - 1\):

\[ T =\dfrac{ \bar{X} - \mu_0}{ S / \sqrt{n} } \sim t (df = n - 1) \]

where \(S\) represents the standard deviation of the sample and \(n\) is the sample size.

B.2.5.2.1 Observed test statistic

While one could compute this observed test statistic by “hand”, the focus here is on the set-up of the problem and in understanding which formula for the test statistic applies. We can use the t.test function to perform this analysis for us.

t.test(x = ageAtMar$age,

alternative = "greater",

mu = 23)

One Sample t-test

data: ageAtMar$age

t = 6.9, df = 5500, p-value = 0.000000000002

alternative hypothesis: true mean is greater than 23

95 percent confidence interval:

23.34 Inf

sample estimates:

mean of x

23.44 We see here that the \(t_{obs}\) value is around 6.94. Recall that for large sample sizes the \(t\) distribution is essentially the standard normal distribution and this is why the statistic is reported as Z.

B.2.5.3 Compute \(p\)-value

The \(p\)-value—the probability of observing an \(t_{obs}\) value of 6.94 or more in our null distribution of a \(t\) with 5433 degrees of freedom—is essentially 0. This can also be calculated in R directly:

pt(6.936, df = nrow(ageAtMar) - 1, lower.tail = FALSE)[1] 0.000000000002247We can also use the \(N(0, 1)\) distribution here:

pnorm(6.936, lower.tail = FALSE)[1] 0.000000000002017B.2.5.4 State conclusion

We, therefore, have sufficient evidence to reject the null hypothesis. Our initial guess that our observed sample mean was statistically greater than the hypothesized mean has supporting evidence here. Based on this sample, we have evidence that the mean age of first marriage for all US women from 2006 to 2010 is greater than 23 years.

B.2.5.5 Confidence interval

The confidence interval reported above with t.test is known as a one-sided confidence interval and gives the lowest value one could expect \(\mu\) to be with 95% confidence. We usually want a range of values so we can use alternative = "two.sided" to get the similar values compared to the bootstrapping process:

t.test(x = ageAtMar$age,

alternative = "two.sided",

mu = 23)$conf[1] 23.32 23.56

attr(,"conf.level")

[1] 0.95B.2.6 Comparing results

Observing the bootstrap distribution that were created, it makes quite a bit of sense that the results are so similar for traditional and non-traditional methods in terms of the \(p\)-value and the confidence interval since these distributions look very similar to normal distributions. The conditions also being met (the large sample size was the driver here) leads us to better guess that using any of the methods whether they are traditional (formula-based) or non-traditional (computational-based) will lead to similar results.

B.3 One proportion

B.3.1 Problem statement

The CEO of a large electric utility claims that 80 percent of his 1,000,000 customers are satisfied with the service they receive. To test this claim, the local newspaper surveyed 100 customers, using simple random sampling. 73 were satisfied and the remaining were unsatisfied. Based on these findings from the sample, can we reject the CEO’s hypothesis that 80% of the customers are satisfied? [Tweaked a bit from http://stattrek.com/hypothesis-test/proportion.aspx?Tutorial=AP]

B.3.2 Competing hypotheses

B.3.2.1 In words

Null hypothesis: The proportion of all customers of the large electric utility satisfied with service they receive is equal 0.80.

Alternative hypothesis: The proportion of all customers of the large electric utility satisfied with service they receive is different from 0.80.

B.3.2.2 In symbols (with annotations)

- \(H_0: \pi = p_{0}\), where \(\pi\) represents the proportion of all customers of the large electric utility satisfied with service they receive and \(p_0\) is 0.8.

- \(H_A: \pi \ne 0.8\)

B.3.2.3 Set \(\alpha\)

It’s important to set the significance level before starting the testing using the data. Let’s set the significance level at 5% here.

B.3.3 Exploring the sample data

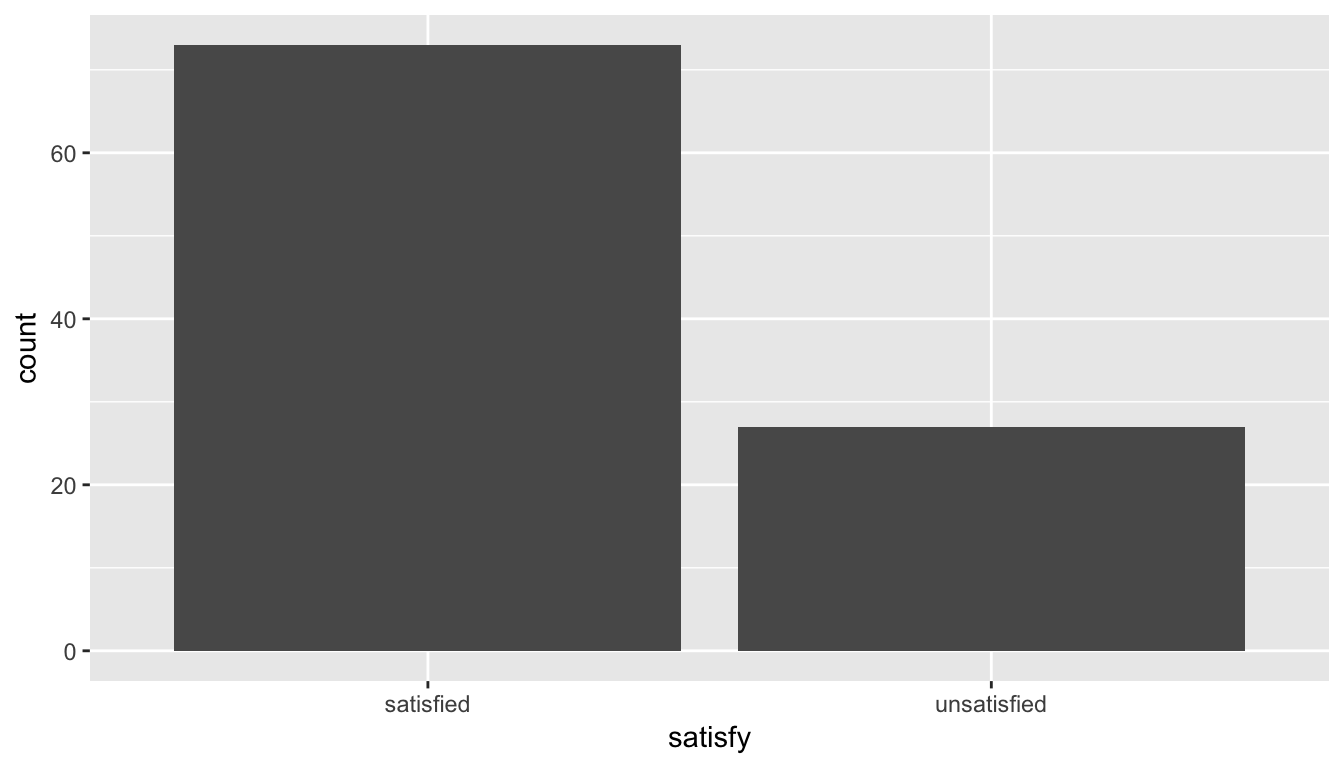

elec <- c(rep("satisfied", 73), rep("unsatisfied", 27)) %>%

as_data_frame() %>%

rename("satisfy" = value)The bar graph below also shows the distribution of satisfy.

ggplot(data = elec, aes(x = satisfy)) +

geom_bar()

B.3.3.1 Guess about statistical significance

We are looking to see if the sample proportion of 0.73 is statistically different from \(p_0 = 0.8\) based on this sample. They seem to be quite close, and our sample size is not huge here (\(n = 100\)). Let’s guess that we do not have evidence to reject the null hypothesis.

B.3.4 Non-traditional methods

B.3.4.1 Simulation for hypothesis test

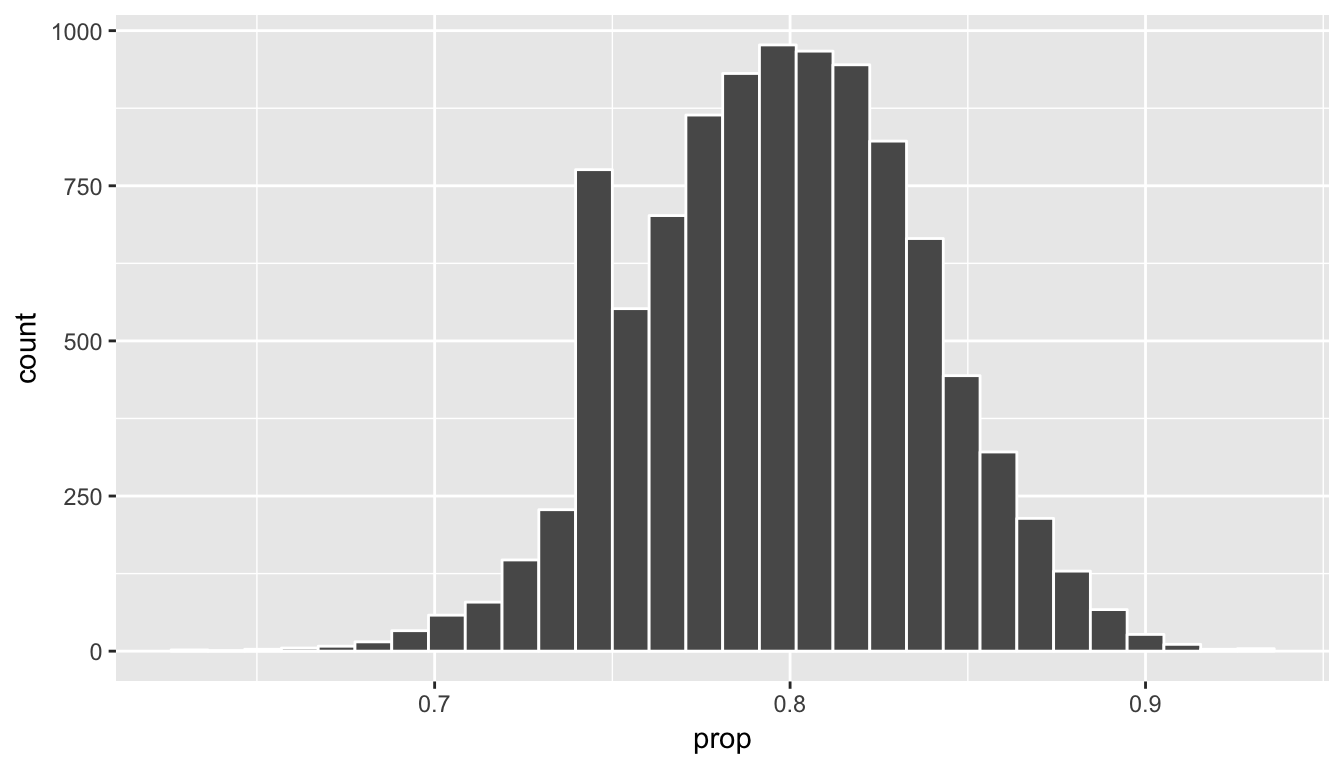

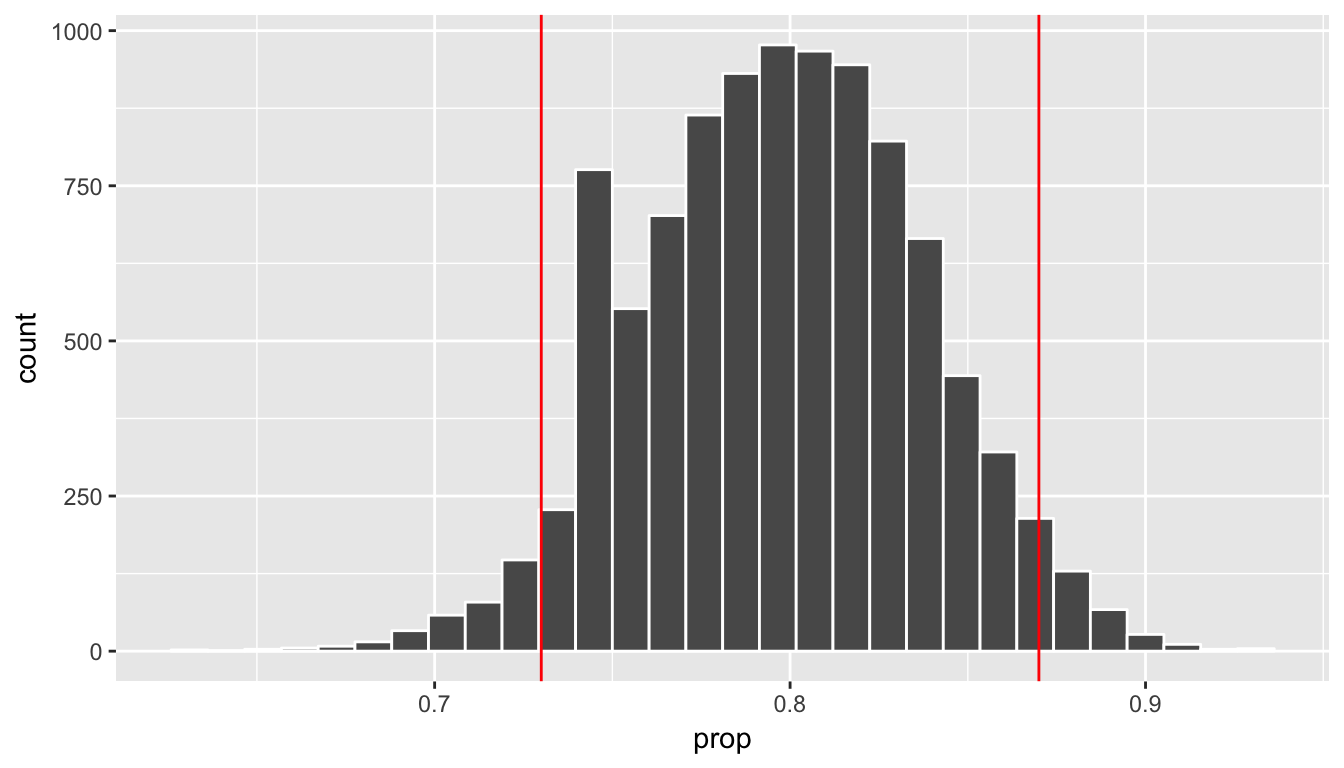

In order to look to see if 0.73 is statistically different from 0.8, we need to account for the sample size. We also need to determine a process that replicates how the original sample of size 100 was selected. We can use the idea of an unfair coin to simulate this process. We will simulate flipping an unfair coin (with probability of success 0.8 matching the null hypothesis) 100 times. Then we will keep track of how many heads come up in those 100 flips. Our simulated statistic matches with how we calculated the original statistic \(\hat{p}\): the number of heads (satisfied) out of our total sample of 100. We then repeat this process many times (say 10,000) to create the null distribution looking at the simulated proportions of successes:

set.seed(2017)

null_distn_one_prop <- do(10000) * rflip(100, prob = 0.8)ggplot(null_distn_one_prop, aes(x = prop)) +

geom_histogram(bins = 30, color = "white")

We can next use this distribution to observe our \(p\)-value. Recall this is a two-tailed test so we will be looking for values that are 0.8 - 0.73 = 0.07 away from 0.8 in BOTH directions for our \(p\)-value:

p_hat <- 73/100

dist <- 0.8 - p_hat

ggplot(null_distn_one_prop, aes(x = prop)) +

geom_histogram(bins = 30, color = "white") +

geom_vline(color = "red", xintercept = 0.8 + dist) +

geom_vline(color = "red", xintercept = p_hat)

B.3.4.1.1 Calculate \(p\)-value

pvalue <- null_distn_one_prop %>%

filter( (prop >= 0.8 + dist) | (prop <= p_hat) ) %>%

nrow() / nrow(null_distn_one_prop)

pvalue[1] 0.082So our \(p\)-value is 0.082 and we fail to reject the null hypothesis at the 5% level.

B.3.4.2 Bootstrapping for confidence interval

We can also create a confidence interval for the unknown population parameter \(\pi\) using our sample data. To do so, we use bootstrapping, which involves

- sampling with replacement from our original sample of 100 survey respondents and repeating this process 10,000 times,

- calculating the proportion of successes for each of the 10,000 bootstrap samples created in Step 1.,

- combining all of these bootstrap statistics calculated in Step 2 into a

boot_distnobject, - identifying the 2.5th and 97.5th percentiles of this distribution (corresponding to the 5% significance level chosen) to find a 95% confidence interval for \(\pi\), and

- interpret this confidence interval in the context of the problem.

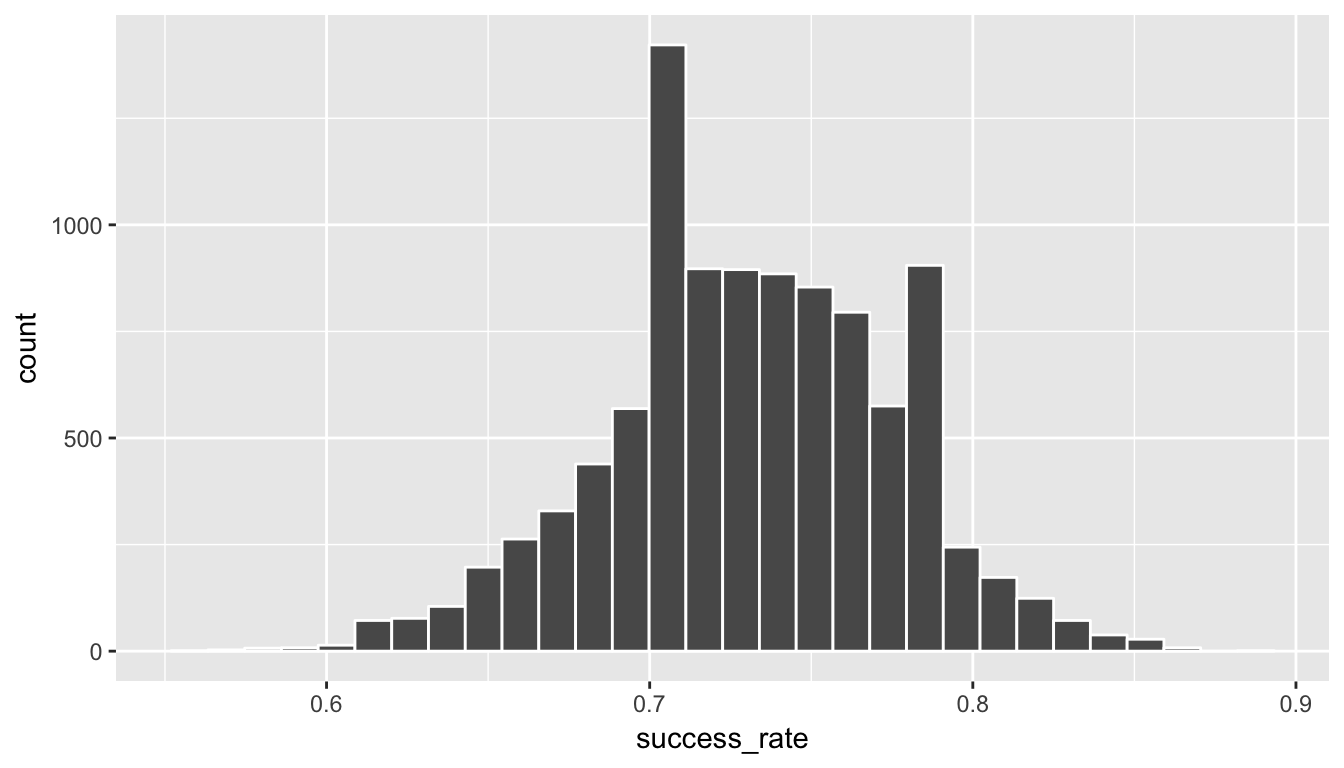

boot_distn_one_prop <- do(10000) *

(elec %>% resample(size = 100, replace = TRUE) )%>%

summarize(success_rate = mean(satisfy == "satisfied"))Just as we use the mean function for calculating the mean over a numerical variable, we can also use it to compute the proportion of successes for a categorical variable where we specify what we are calling a “success” after the ==. (Think about the formula for calculating a mean and how R handles logical statements such as satisfy == "satisfied" for why this must be true.)

ggplot(boot_distn_one_prop, aes(x = success_rate)) +

geom_histogram(bins = 30, color = "white")

boot_distn_one_prop %>% summarize(lower = quantile(success_rate, probs = 0.025),

upper = quantile(success_rate, probs = 0.975)) lower upper

1 0.64 0.82We see that 0.80 is contained in this confidence interval as a plausible value of \(\pi\) (the unknown population proportion). This matches with our hypothesis test results of failing to reject the null hypothesis.

Interpretation: We are 95% confident the true proportion of customers who are satisfied with the service they receive is between and .

Note: You could also use the null distribution with a shift to have its center at \(\hat{p} = 0.73\) instead of at \(p_0 = 0.8\) and calculate its percentiles. The confidence interval produced via this method should be comparable to the one done using bootstrapping above.

B.3.5 Traditional methods

B.3.5.1 Check conditions

Remember that in order to use the shortcut (formula-based, theoretical) approach, we need to check that some conditions are met.

Independent observations: The observations are collected independently.

The cases are selected independently through random sampling so this condition is met.

Approximately normal: The number of expected successes and expected failures is at least 10.

This condition is met since 73 and 27 are both greater than 10.

B.3.5.2 Test statistic

The test statistic is a random variable based on the sample data. Here, we want to look at a way to estimate the population proportion \(\pi\). A good guess is the sample proportion \(\hat{P}\). Recall that this sample proportion is actually a random variable that will vary as different samples are (theoretically, would be) collected. We are looking to see how likely is it for us to have observed a sample proportion of \(\hat{p}_{obs} = 0.73\) or larger assuming that the population proportion is 0.80 (assuming the null hypothesis is true). If the conditions are met and assuming \(H_0\) is true, we can standardize this original test statistic of \(\hat{P}\) into a \(Z\) statistic that follows a \(N(0, 1)\) distribution.

\[ Z =\dfrac{ \hat{P} - p_0}{\sqrt{\dfrac{p_0(1 - p_0)}{n} }} \sim N(0, 1) \]

B.3.5.2.1 Observed test statistic

While one could compute this observed test statistic by “hand” by plugging the observed values into the formula, the focus here is on the set-up of the problem and in understanding which formula for the test statistic applies. The calculation has been done in R below for completeness though:

p_hat <- 0.73

p0 <- 0.8

n <- 100

(z_obs <- (p_hat - p0) / sqrt( (p0 * (1 - p0)) / n))[1] -1.75We see here that the \(z_{obs}\) value is around -1.75. Our observed sample proportion of 0.73 is 1.75 standard errors below the hypothesized parameter value of 0.8.

B.3.5.3 Compute \(p\)-value

2 * pnorm(z_obs)[1] 0.08012The \(p\)-value—the probability of observing an \(z_{obs}\) value of -1.75 or more extreme (in both directions) in our null distribution—is around 8%.

Note that we could also do this test directly using the prop.test function.

stats::prop.test(x = table(elec$satisfy),

n = length(elec$satisfy),

alternative = "two.sided",

p = 0.8,

correct = FALSE)

1-sample proportions test without continuity correction

data: table(elec$satisfy), null probability 0.8

X-squared = 3.1, df = 1, p-value = 0.08

alternative hypothesis: true p is not equal to 0.8

95 percent confidence interval:

0.6357 0.8073

sample estimates:

p

0.73 prop.test does a \(\chi^2\) test here but this matches up exactly with what we would expect: \(x^2_{obs} = 3.06 = (-1.75)^2 = (z_{obs})^2\) and the \(p\)-values are the same because we are focusing on a two-tailed test.

Note that the 95 percent confidence interval given above matches well with the one calculated using bootstrapping.

B.3.5.4 State conclusion

We, therefore, do not have sufficient evidence to reject the null hypothesis. Our initial guess that our observed sample proportion was not statistically greater than the hypothesized proportion has not been invalidated. Based on this sample, we have do not evidence that the proportion of all customers of the large electric utility satisfied with service they receive is different from 0.80, at the 5% level.

B.3.6 Comparing results

Observing the bootstrap distribution and the null distribution that were created, it makes quite a bit of sense that the results are so similar for traditional and non-traditional methods in terms of the \(p\)-value and the confidence interval since these distributions look very similar to normal distributions. The conditions also being met leads us to better guess that using any of the methods whether they are traditional (formula-based) or non-traditional (computational-based) will lead to similar results.

B.4 Two proportions

B.4.1 Problem statement

A 2010 survey asked 827 randomly sampled registered voters in California “Do you support? Or do you oppose? Drilling for oil and natural gas off the Coast of California? Or do you not know enough to say?” Conduct a hypothesis test to determine if the data provide strong evidence that the proportion of college graduates who do not have an opinion on this issue is different than that of non-college graduates. (Tweaked a bit from Diez, Barr, and Çetinkaya-Rundel 2014 [Chapter 6])

B.4.2 Competing hypotheses

B.4.2.1 In words

Null hypothesis: There is no association between having an opinion on drilling and having a college degree for all registered California voters in 2010.

Alternative hypothesis: There is an association between having an opinion on drilling and having a college degree for all registered California voters in 2010.

B.4.2.2 Another way in words

Null hypothesis: The probability that a Californian voter in 2010 having no opinion on drilling and is a college graduate is the same as that of a non-college graduate.

Alternative hypothesis: These parameter probabilities are different.

B.4.2.3 In symbols (with annotations)

- \(H_0: \pi_{college} = \pi_{no\_college}\) or \(H_0: \pi_{college} - \pi_{no\_college} = 0\), where \(\pi\) represents the probability of not having an opinion on drilling.

- \(H_A: \pi_{college} - \pi_{no\_college} \ne 0\)

B.4.2.4 Set \(\alpha\)

It’s important to set the significance level before starting the testing using the data. Let’s set the significance level at 5% here.

B.4.3 Exploring the sample data

#download.file("http://ismayc.github.io/teaching/sample_problems/offshore.csv",

# destfile = "data/offshore.csv",

# method = "curl")

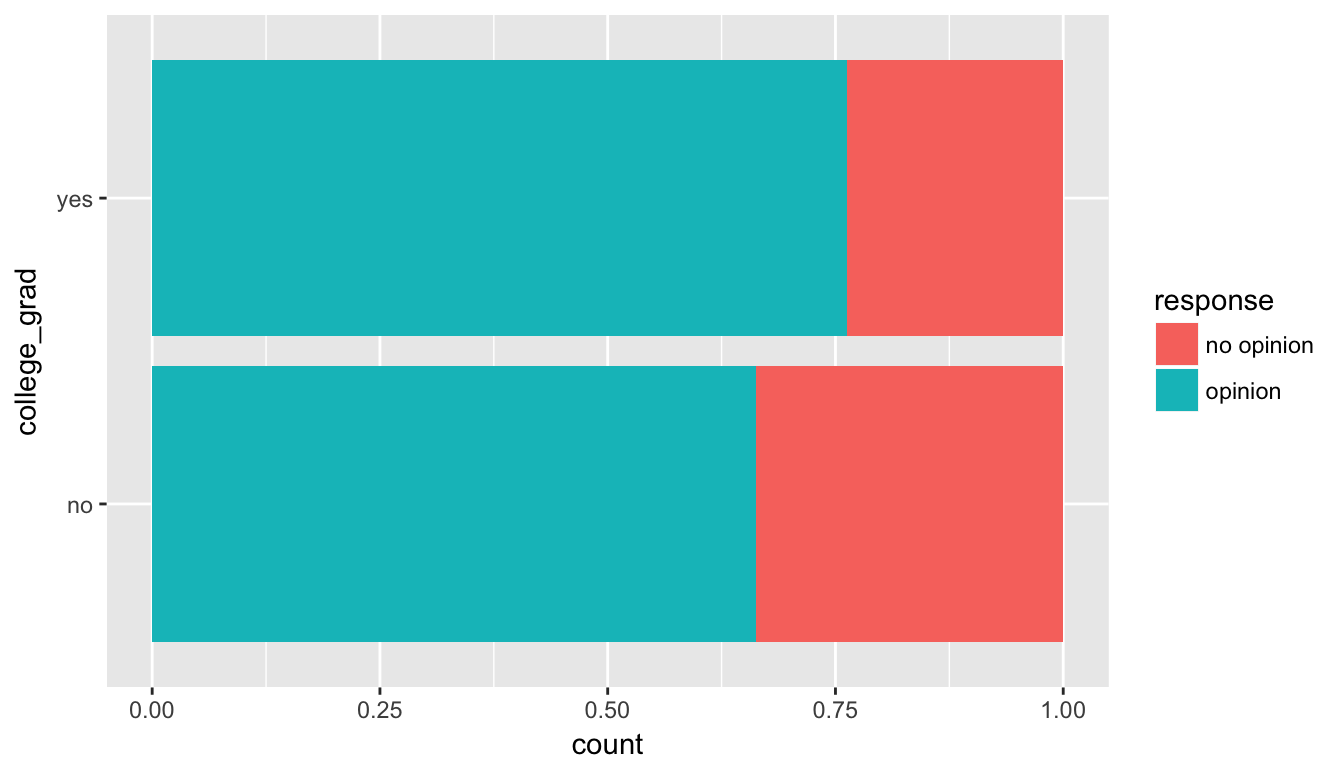

offshore <- read_csv("data/offshore.csv")table(offshore$college_grad, offshore$response)

no opinion opinion

no 131 258

yes 104 334off_summ <- offshore %>%

group_by(college_grad) %>%

summarize(prop_no_opinion = mean(response == "no opinion"),

sample_size = n())ggplot(offshore, aes(x = college_grad, fill = response)) +

geom_bar(position = "fill") +

coord_flip()

B.4.3.1 Guess about statistical significance

We are looking to see if a difference exists in the heights of the bars corresponding to no opinion for the plot. Based solely on the plot, we have little reason to believe that a difference exists since the bars seem to be about the same height, BUT…it’s important to use statistics to see if that difference is actually statistically significant!

B.4.4 Non-traditional methods

B.4.4.1 Collecting summary info

Next we will assign some key values to variable names in R:

phat_nograd <- off_summ$prop_no_opinion[1]

phat_grad <- off_summ$prop_no_opinion[2]

obs_diff <- phat_grad - phat_nograd

n_nograd <- off_summ$sample_size[1]

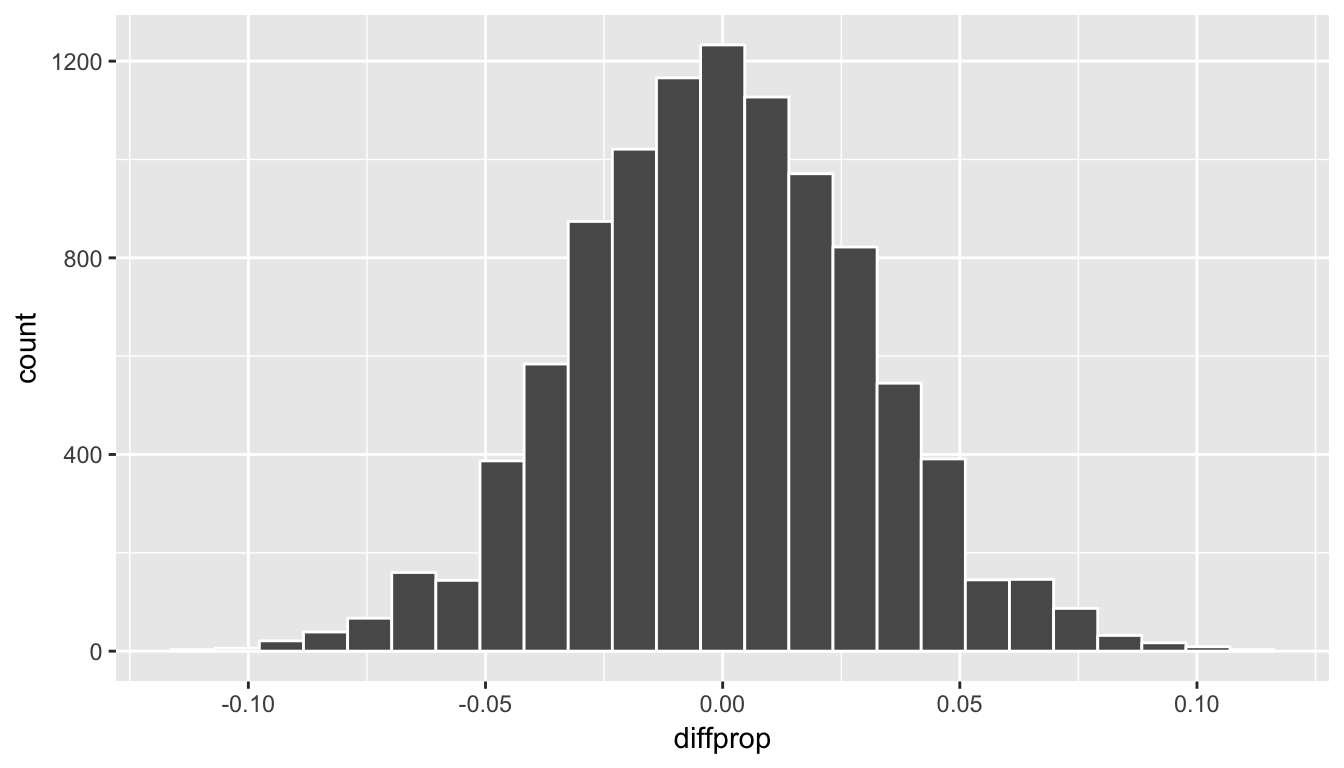

n_grad <- off_summ$sample_size[2]B.4.4.2 Randomization for hypothesis test

In order to look to see if the observed sample proportion of no opinion for college graduates of 0.3368 is statistically different than that for graduates of 0.2374, we need to account for the sample sizes. Note that this is the same as looking to see if \(\hat{p}_{grad} - \hat{p}_{nograd}\) is statistically different than 0. We also need to determine a process that replicates how the original group sizes of 389 and 438 were selected.

We can use the idea of randomization testing (also known as permutation testing) to simulate the population from which the sample came (with two groups of different sizes) and then generate samples using shuffling from that simulated population to account for sampling variability.

set.seed(2017)

many_shuffles <- do(10000) *

(offshore %>%

mutate(college_grad = shuffle(college_grad)) %>%

group_by(college_grad) %>%

summarize(prop_no_opinion = mean(response == "no opinion"))

)

null_distn_two_props <- many_shuffles %>%

group_by(.index) %>%

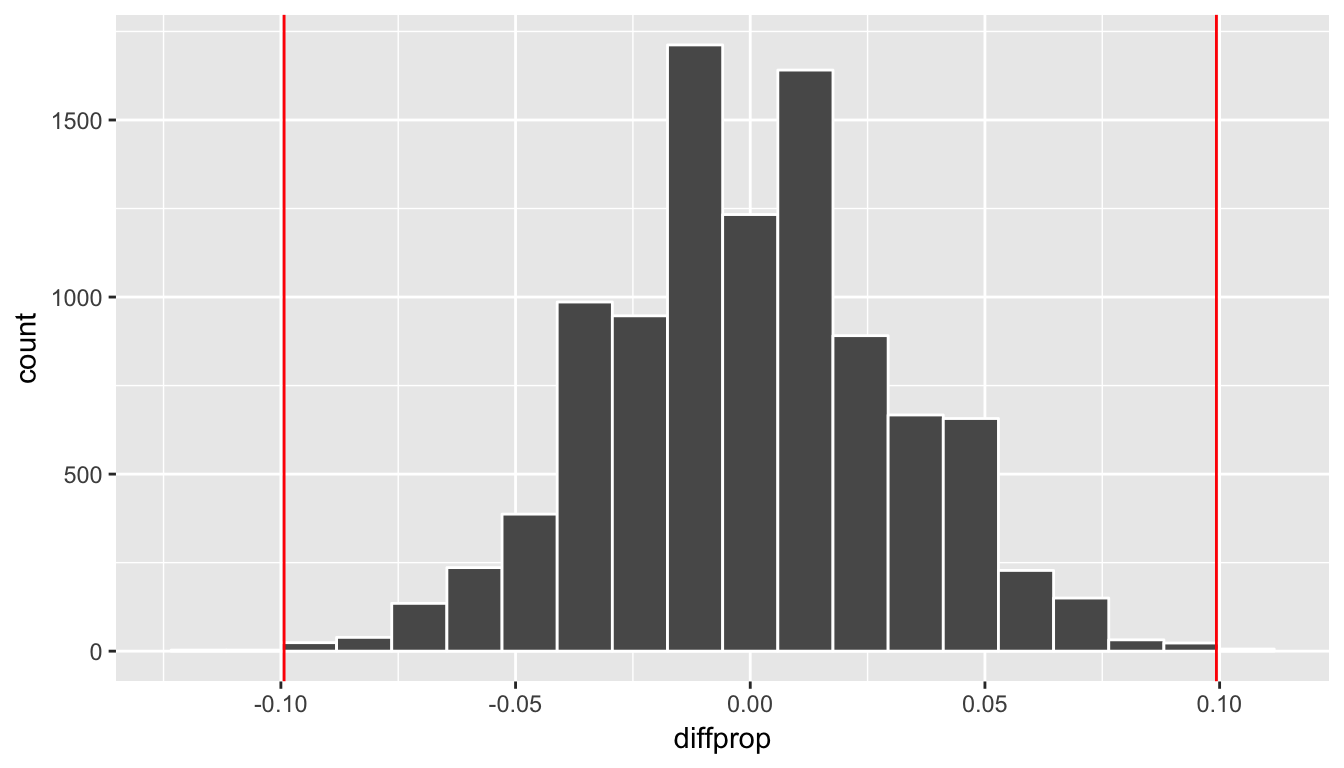

summarize(diffprop = diff(prop_no_opinion))ggplot(null_distn_two_props, aes(x = diffprop)) +

geom_histogram(bins = 25, color = "white")

We can next use this distribution to observe our \(p\)-value. Recall this is a two-tailed test so we will be looking for values that are greater than or equal to -0.0993 or less than or equal to 0.0993 for our \(p\)-value.

ggplot(null_distn_two_props, aes(x = diffprop)) +

geom_histogram(bins = 20, color = "white") +

geom_vline(color = "red", xintercept = obs_diff) +

geom_vline(color = "red", xintercept = -obs_diff)

B.4.4.2.1 Calculate \(p\)-value

pvalue <- null_distn_two_props %>%

filter( (diffprop <= obs_diff) | (diffprop >= -obs_diff) ) %>%

nrow() / nrow(null_distn_two_props)

pvalue[1] 0.0021So our \(p\)-value is 0.0021 and we reject the null hypothesis at the 5% level. You can also see this from the histogram above that we are far into the tails of the null distribution.

B.4.4.3 Bootstrapping for confidence interval

We can also create a confidence interval for the unknown population parameter \(\pi_{college} - \pi_{no\_college}\) using our sample data with bootstrapping. Here we will bootstrap each of the groups with replacement instead of shuffling. This is done using the groups argument in the resample function to fix the size of each group to be the same as the original group sizes of 389 for non-college graduates and 438 for college graduates.

boot_props <- do(10000) *

offshore %>%

resample(replace = TRUE, groups = college_grad) %>%

group_by(college_grad) %>%

summarize(prop_no_opinion = mean(response == "no opinion"))

# Next, we calculate the difference in sample proportions for each of the 10,000 replications:

boot_distn_two_props <- boot_props %>%

group_by(.index) %>%

summarize(diffprop = diff(prop_no_opinion))ggplot(boot_distn_two_props, aes(x = diffprop)) +

geom_histogram(bins = 30, color = "white")

ci_boot <- boot_distn_two_props %>%

summarize(lower = quantile(diffprop, probs = 0.025),

upper = quantile(diffprop, probs = 0.975))

ci_boot# A tibble: 1 x 2

lower upper

<dbl> <dbl>

1 -0.1619 -0.03681We see that 0 is not contained in this confidence interval as a plausible value of \(\pi_{college} - \pi_{no\_college}\) (the unknown population parameter). This matches with our hypothesis test results of rejecting the null hypothesis. Since zero is not a plausible value of the population parameter, we have evidence that the proportion of college graduates in California with no opinion on drilling is different than that of non-college graduates.

Interpretation: We are 95% confident the true proportion of non-college graduates with no opinion on offshore drilling in California is between 0.16 dollars smaller to 0.04 dollars smaller than for college graduates.

Note: You could also use the null distribution based on randomization with a shift to have its center at \(\hat{p}_{college} - \hat{p}_{no\_college} = \$-0.1\) instead of at 0 and calculate its percentiles. The confidence interval produced via this method should be comparable to the one done using bootstrapping above.

B.4.5 Traditional methods

B.4.6 Check conditions

Remember that in order to use the short-cut (formula-based, theoretical) approach, we need to check that some conditions are met.

Independent observations: Each case that was selected must be independent of all the other cases selected.

This condition is met since cases were selected at random to observe.

Sample size: The number of pooled successes and pooled failures must be at least 10 for each group.

We need to first figure out the pooled success rate: \[\hat{p}_{obs} = \dfrac{131 + 104}{827} = 0.28.\] We now determine expected (pooled) success and failure counts:

\(0.28 \cdot (131 + 258) = 108.92\), \(0.72 \cdot (131 + 258) = 280.08\)

\(0.28 \cdot (104 + 334) = 122.64\), \(0.72 \cdot (104 + 334) = 315.36\)

Independent selection of samples: The cases are not paired in any meaningful way.

We have no reason to suspect that a college graduate selected would have any relationship to a non-college graduate selected.

B.4.7 Test statistic

The test statistic is a random variable based on the sample data. Here, we are interested in seeing if our observed difference in sample proportions corresponding to no opinion on drilling (\(\hat{p}_{college, obs} - \hat{p}_{no\_college, obs}\) = 0.0326) is statistically different than 0. Assuming that conditions are met and the null hypothesis is true, we can use the standard normal distribution to standardize the difference in sample proportions (\(\hat{P}_{college} - \hat{P}_{no\_college}\)) using the standard error of \(\hat{P}_{college} - \hat{P}_{no\_college}\) and the pooled estimate:

\[ Z =\dfrac{ (\hat{P}_1 - \hat{P}_2) - 0}{\sqrt{\dfrac{\hat{P}(1 - \hat{P})}{n_1} + \dfrac{\hat{P}(1 - \hat{P})}{n_2} }} \sim N(0, 1) \] where \(\hat{P} = \dfrac{\text{total number of successes} }{ \text{total number of cases}}.\)

B.4.7.1 Observed test statistic

While one could compute this observed test statistic by “hand”, the focus here is on the set-up of the problem and in understanding which formula for the test statistic applies. We can use the prop.test function to perform this analysis for us.

stats::prop.test(x = table(offshore$college_grad, offshore$response),

n = nrow(offshore),

alternative = "two.sided",

correct = FALSE)

2-sample test for equality of proportions without continuity

correction

data: table(offshore$college_grad, offshore$response)

X-squared = 10, df = 1, p-value = 0.002

alternative hypothesis: two.sided

95 percent confidence interval:

0.03773 0.16091

sample estimates:

prop 1 prop 2

0.3368 0.2374 prop.test does a \(\chi^2\) test here but this matches up exactly with what we would expect from the test statistic above since \(Z^2 = \chi^2\) so \(\sqrt{9.99} = 3.16 = z_{obs}\): The \(p\)-values are the same because we are focusing on a two-tailed test. The observed difference in sample proportions is 3.16 standard deviations larger than 0.

The \(p\)-value—the probability of observing a \(Z\) value of 3.16 or more extreme in our null distribution—is 0.0016. This can also be calculated in R directly:

2 * pnorm(3.16, lower.tail = FALSE)[1] 0.001578The 95% confidence interval is also stated above in the prop.test results.

B.4.8 State conclusion

We, therefore, have sufficient evidence to reject the null hypothesis. Our initial guess that a statistically significant difference did not exist in the proportions of no opinion on offshore drilling between college educated and non-college educated Californians was not validated. We do have evidence to suggest that there is a dependency between college graduation and position on offshore drilling for Californians.

B.4.9 Comparing results

Observing the bootstrap distribution and the null distribution that were created, it makes quite a bit of sense that the results are so similar for traditional and non-traditional methods in terms of the \(p\)-value and the confidence interval since these distributions look very similar to normal distributions. The conditions were not met since the number of pairs was small, but the sample data was not highly skewed. Using any of the methods whether they are traditional (formula-based) or non-traditional (computational-based) lead to similar results.

B.5 Two means (independent samples)

B.5.1 Problem statement

Average income varies from one region of the country to another, and it often reflects both lifestyles and regional living expenses. Suppose a new graduate is considering a job in two locations, Cleveland, OH and Sacramento, CA, and he wants to see whether the average income in one of these cities is higher than the other. He would like to conduct a hypothesis test based on two randomly selected samples from the 2000 Census. (Tweaked a bit from Diez, Barr, and Çetinkaya-Rundel 2014 [Chapter 5])

B.5.2 Competing hypotheses

B.5.2.1 In words

Null hypothesis: There is no association between income and location (Cleveland, OH and Sacramento, CA).

Alternative hypothesis: There is an association between income and location (Cleveland, OH and Sacramento, CA).

B.5.2.2 Another way in words

Null hypothesis: The mean income is the same for both cities.

Alternative hypothesis: The mean income is different for the two cities.

B.5.2.3 In symbols (with annotations)

- \(H_0: \mu_{sac} = \mu_{cle}\) or \(H_0: \mu_{sac} - \mu_{cle} = 0\), where \(\mu\) represents the average income.

- \(H_A: \mu_{sac} - \mu_{cle} \ne 0\)

B.5.2.4 Set \(\alpha\)

It’s important to set the significance level before starting the testing using the data. Let’s set the significance level at 5% here.

B.5.3 Exploring the sample data

inc_summ <- cleSac %>% group_by(metro_area) %>%

summarize(sample_size = n(),

mean = mean(income),

sd = sd(income),

minimum = min(income),

lower_quartile = quantile(income, 0.25),

median = median(income),

upper_quartile = quantile(income, 0.75),

max = max(income))

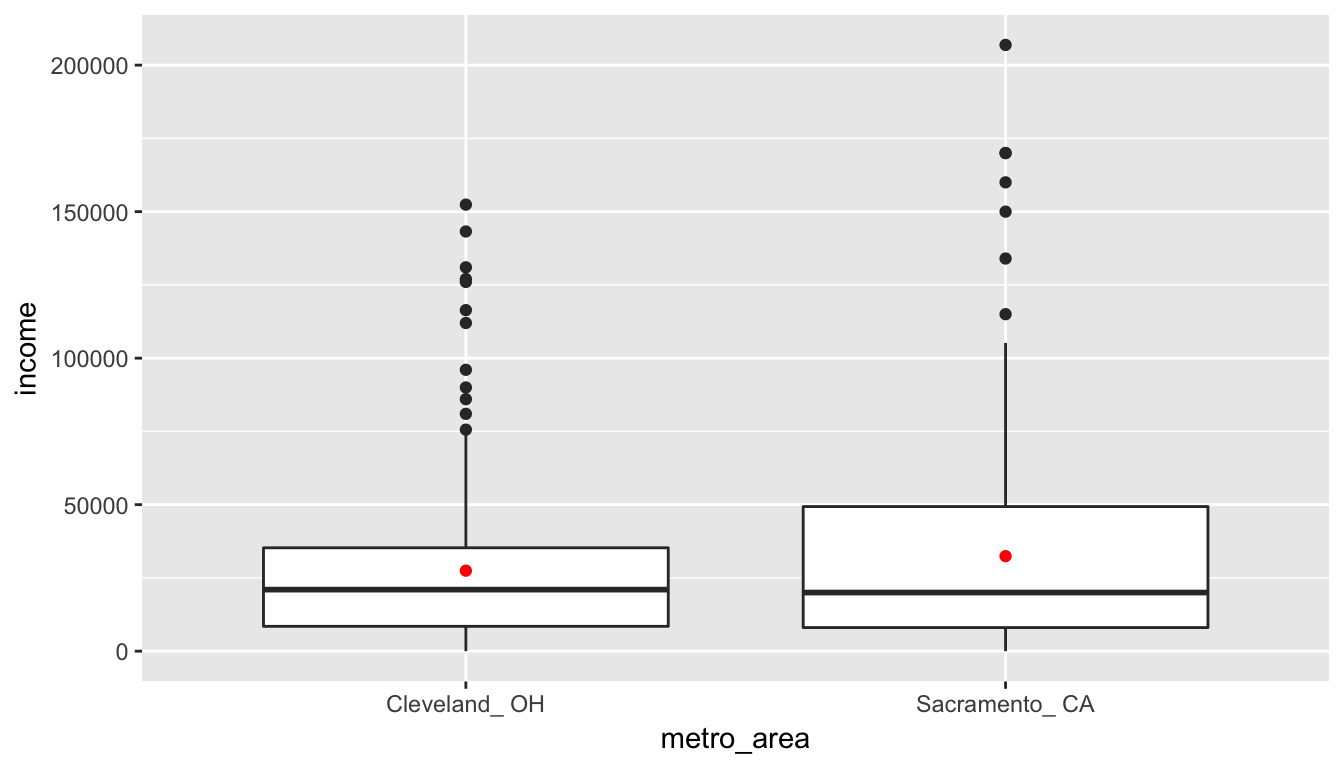

kable(inc_summ)| metro_area | sample_size | mean | sd | minimum | lower_quartile | median | upper_quartile | max |

|---|---|---|---|---|---|---|---|---|

| Cleveland_ OH | 212 | 27467 | 27681 | 0 | 8475 | 21000 | 35275 | 152400 |

| Sacramento_ CA | 175 | 32428 | 35774 | 0 | 8050 | 20000 | 49350 | 206900 |

The boxplot below also shows the mean for each group highlighted by the red dots.

ggplot(cleSac, aes(x = metro_area, y = income)) +

geom_boxplot() +

stat_summary(fun.y = "mean", geom = "point", color = "red")

B.5.3.1 Guess about statistical significance

We are looking to see if a difference exists in the mean income of the two levels of the explanatory variable. Based solely on the boxplot, we have reason to believe that no difference exists. The distributions of income seem similar and the means fall in roughly the same place.

B.5.4 Non-traditional methods

B.5.4.1 Collecting summary info

Next we will assign some key values to variable names in R:

xbar_cle <- inc_summ$mean[1]

xbar_sac <- inc_summ$mean[2]

obs_diff <- xbar_sac - xbar_cle

n_cle <- inc_summ$sample_size[1]

n_sac <- inc_summ$sample_size[2]B.5.4.2 Randomization for hypothesis test

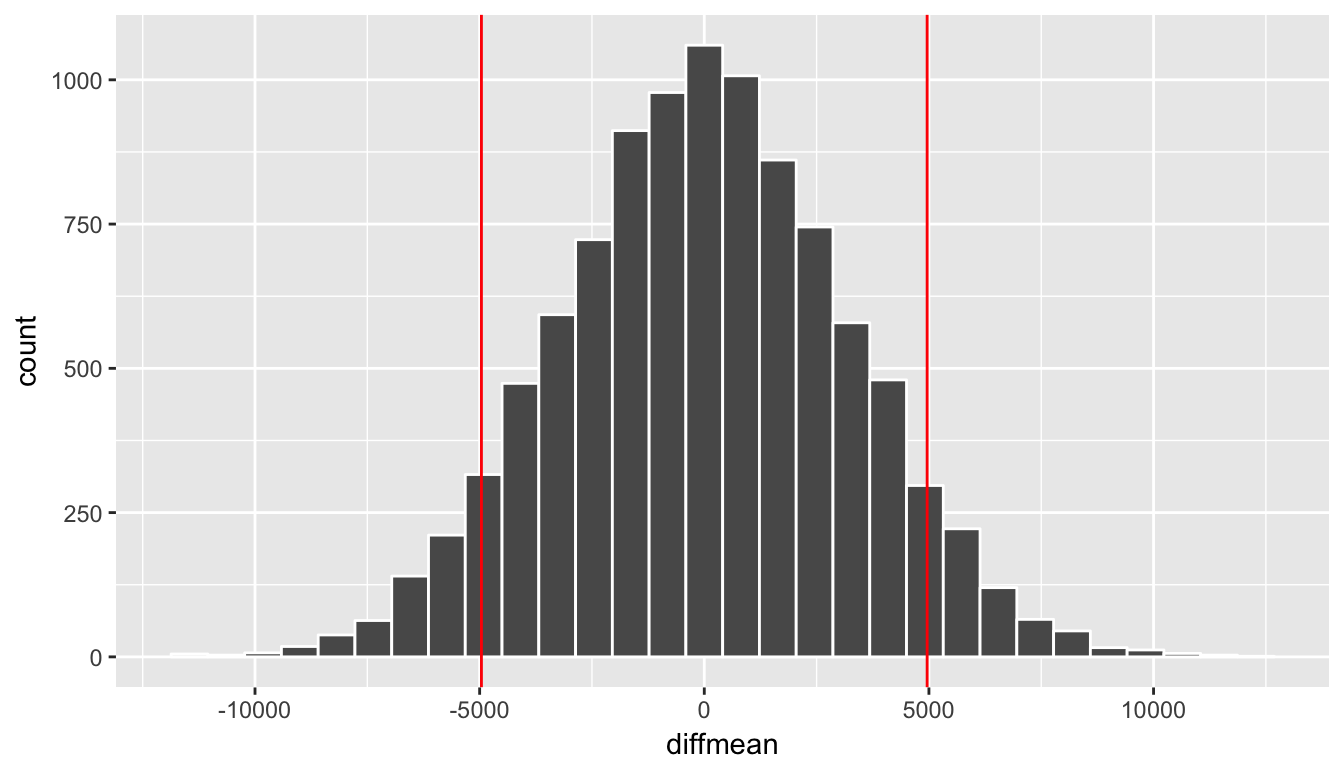

In order to look to see if the observed sample mean for Sacramento of 27467.066 is statistically different than that for Cleveland of 32427.5429, we need to account for the sample sizes. Note that this is the same as looking to see if \(\bar{x}_{sac} - \bar{x}_{cle}\) is statistically different than 0. We also need to determine a process that replicates how the original group sizes of 212 and 175 were selected.

We can use the idea of randomization testing (also known as permutation testing) to simulate the population from which the sample came (with two groups of different sizes) and then generate samples using shuffling from that simulated population to account for sampling variability.

set.seed(2017)

many_shuffles <- do(10000) *

(cleSac %>%

mutate(metro_area = shuffle(metro_area)) %>%

group_by(metro_area) %>%

summarize(mean_inc = mean(income))

)

null_distn_two_means <- many_shuffles %>%

group_by(.index) %>%

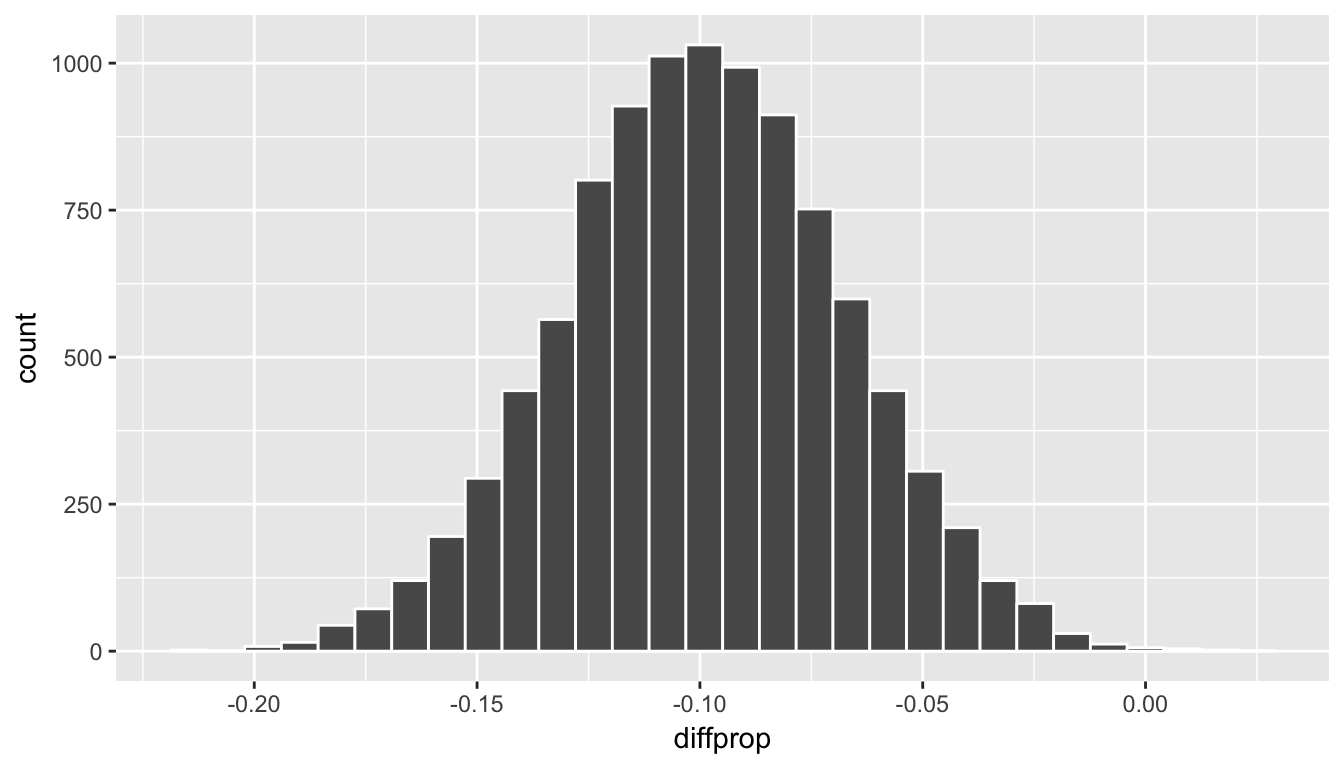

summarize(diffmean = diff(mean_inc))ggplot(null_distn_two_means, aes(x = diffmean)) +

geom_histogram(bins = 30, color = "white")

We can next use this distribution to observe our \(p\)-value. Recall this is a two-tailed test so we will be looking for values that are greater than or equal to 4960.4768 or less than or equal to -4960.4768 for our \(p\)-value.

ggplot(null_distn_two_means, aes(x = diffmean)) +

geom_histogram(bins = 30, color = "white") +

geom_vline(color = "red", xintercept = obs_diff) +

geom_vline(color = "red", xintercept = -obs_diff)

B.5.4.2.1 Calculate \(p\)-value

pvalue <- null_distn_two_means %>%

filter( (diffmean >= obs_diff) | (diffmean <= -obs_diff) ) %>%

nrow() / nrow(null_distn_two_means)

pvalue[1] 0.1211So our \(p\)-value is 0.1211 and we fail to reject the null hypothesis at the 5% level. You can also see this from the histogram above that we are not very far into the tail of the null distribution.

B.5.4.3 Bootstrapping for confidence interval

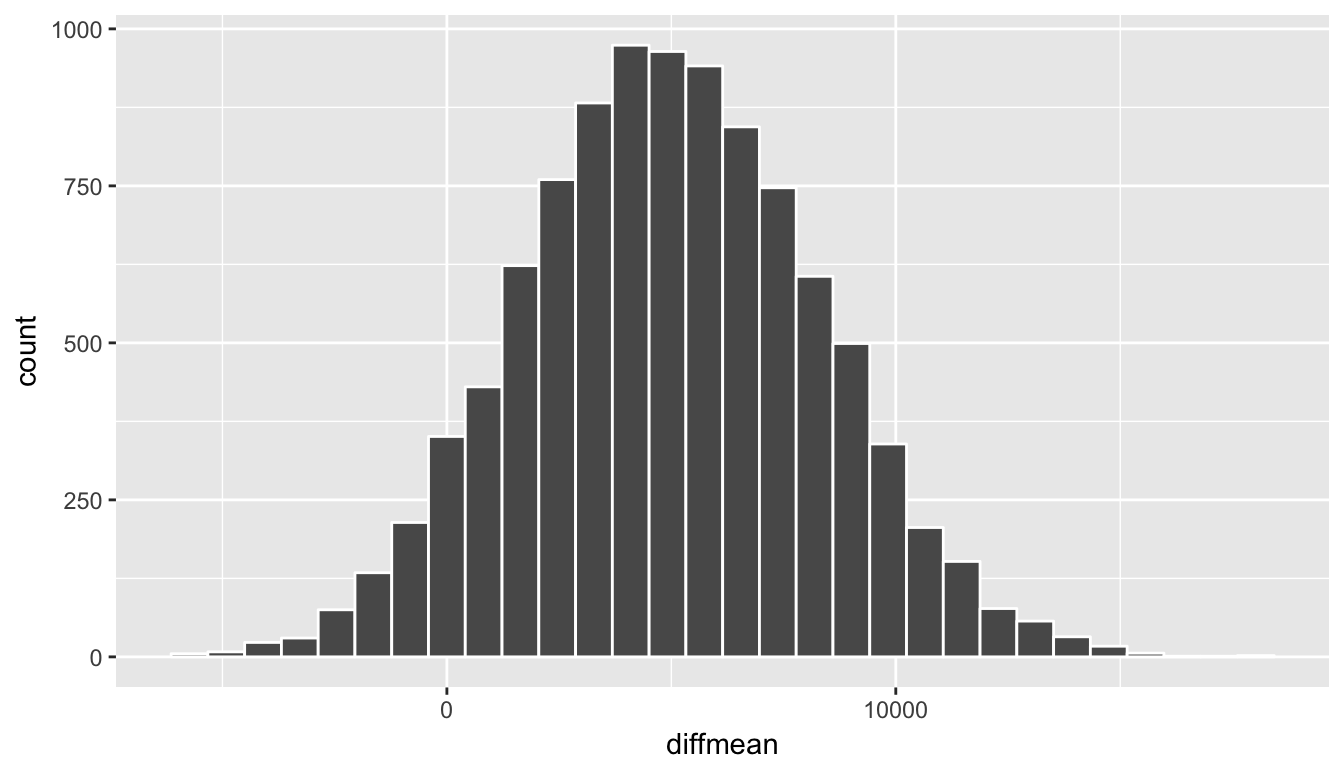

We can also create a confidence interval for the unknown population parameter \(\mu_{sac} - \mu_{cle}\) using our sample data with bootstrapping. Here we will bootstrap each of the groups with replacement instead of shuffling. This is done using the groups argument in the resample function to fix the size of each group to be the same as the original group sizes of 175 for Sacramento and 212 for Cleveland.

boot_means <- do(10000) *

cleSac %>%

resample(replace = TRUE, groups = metro_area) %>%

group_by(metro_area) %>%

summarize(mean_inc = mean(income))

# Next, we calculate the difference in sample means for each of the 10,000 replications:

boot_distn_two_means <- boot_means %>%

group_by(.index) %>%

summarize(diffmean = diff(mean_inc))ggplot(boot_distn_two_means, aes(x = diffmean)) +

geom_histogram(bins = 30, color = "white")

ci_boot <- boot_distn_two_means %>%

summarize(lower = quantile(diffmean, probs = 0.025),

upper = quantile(diffmean, probs = 0.975))

ci_boot# A tibble: 1 x 2

lower upper

<dbl> <dbl>

1 -1346 11441We see that 0 is contained in this confidence interval as a plausible value of \(\mu_{sac} - \mu_{cle}\) (the unknown population parameter). This matches with our hypothesis test results of failing to reject the null hypothesis. Since zero is a plausible value of the population parameter, we do not have evidence that Sacramento incomes are different than Cleveland incomes.

Interpretation: We are 95% confident the true mean yearly income for those living in Sacramento is between 1345.78 dollars smaller to 11440.64 dollars higher than for Cleveland.

Note: You could also use the null distribution based on randomization with a shift to have its center at \(\bar{x}_{sac} - \bar{x}_{cle} = \$4960.48\) instead of at 0 and calculate its percentiles. The confidence interval produced via this method should be comparable to the one done using bootstrapping above.

B.5.5 Traditional methods

B.5.5.0.1 Check conditions

Remember that in order to use the short-cut (formula-based, theoretical) approach, we need to check that some conditions are met.

Independent observations: The observations are independent in both groups.

This

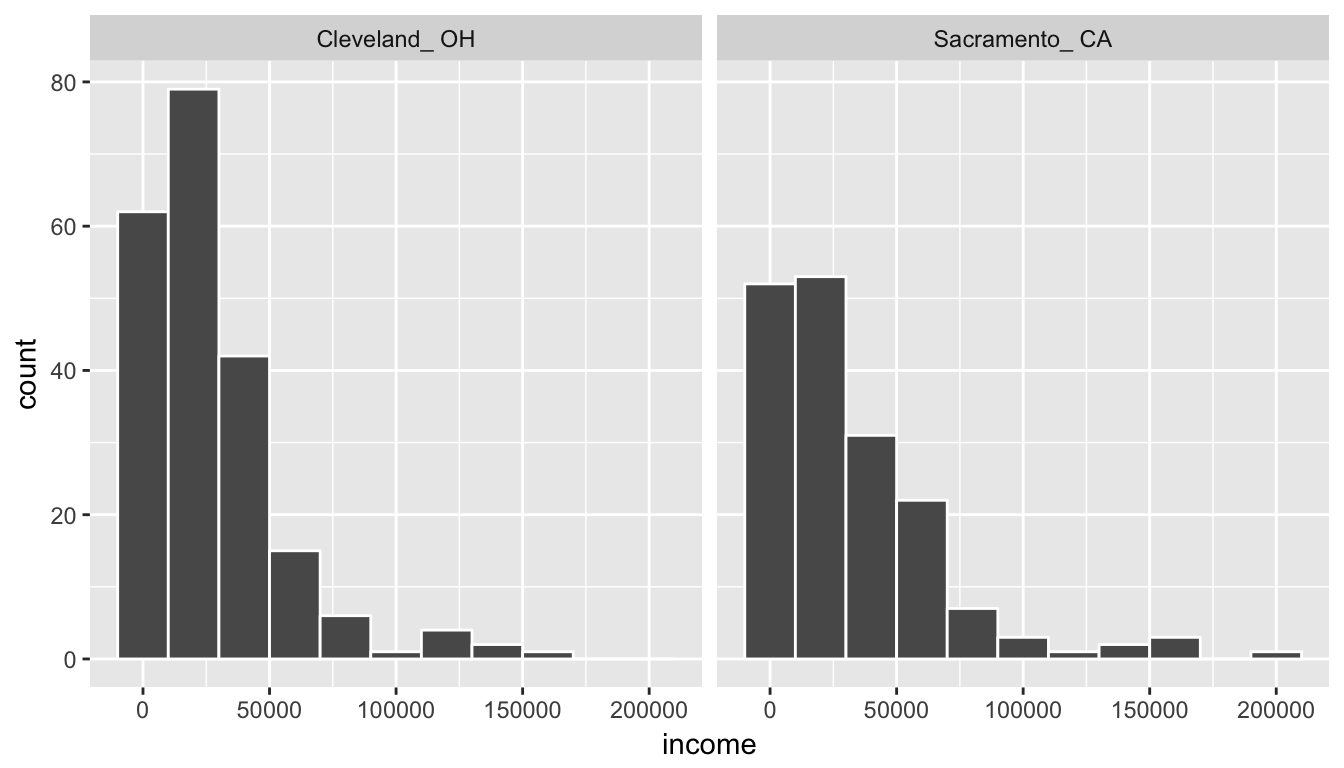

metro_areavariable is met since the cases are randomly selected from each city.Approximately normal: The distribution of the response for each group should be normal or the sample sizes should be at least 30.

ggplot(cleSac, aes(x = income)) +

geom_histogram(color = "white", binwidth = 20000) +

facet_wrap(~ metro_area)

We have some reason to doubt the normality assumption here since both the histograms show deviation from a normal model fitting the data well for each group. The sample sizes for each group are greater than 100 though so the assumptions should still apply.Independent samples: The samples should be collected without any natural pairing.

There is no mention of there being a relationship between those selected in Cleveland and in Sacramento.

B.5.6 Test statistic

The test statistic is a random variable based on the sample data. Here, we are interested in seeing if our observed difference in sample means (\(\bar{x}_{sac, obs} - \bar{x}_{cle, obs}\) = 4960.4768) is statistically different than 0. Assuming that conditions are met and the null hypothesis is true, we can use the \(t\) distribution to standardize the difference in sample means (\(\bar{X}_{sac} - \bar{X}_{cle}\)) using the approximate standard error of \(\bar{X}_{sac} - \bar{X}_{cle}\) (invoking \(S_{sac}\) and \(S_{cle}\) as estimates of unknown \(\sigma_{sac}\) and \(\sigma_{cle}\)).

\[ T =\dfrac{ (\bar{X}_1 - \bar{X}_2) - 0}{ \sqrt{\dfrac{S_1^2}{n_1} + \dfrac{S_2^2}{n_2}} } \sim t (df = min(n_1 - 1, n_2 - 1)) \] where 1 = Sacramento and 2 = Cleveland with \(S_1^2\) and \(S_2^2\) the sample variance of the incomes of both cities, respectively, and \(n_1 = 175\) for Sacramento and \(n_2 = 212\) for Cleveland.

B.5.6.1 Observed test statistic

Note that we could also do (ALMOST) this test directly using the t.test function. The x and y arguments are expected to both be numeric vectors here so we’ll need to appropriately filter our datasets.

cleveland <- cleSac %>% filter(metro_area == "Cleveland_ OH")

sacramento <- cleSac %>% filter(metro_area != "Cleveland_ OH")

t.test(y = cleveland$income, x = sacramento$income,

alternative = "two.sided")

Welch Two Sample t-test

data: sacramento$income and cleveland$income

t = 1.5, df = 320, p-value = 0.1

alternative hypothesis: true difference in means is not equal to 0

95 percent confidence interval:

-1543 11464

sample estimates:

mean of x mean of y

32428 27467 Note that the degrees of freedom reported above are different than what we used above in specifying the Test Statistic. The degrees of freedom used here is also known as the Satterthwaite approximation and involves a quite complicated formula. For most problems, the must simpler smaller of sample sizes minus one will suffice.

While one could compute this observed test statistic by “hand”, the focus here is on the set-up of the problem and in understanding which formula for the test statistic applies.

We see here that the observed test statistic value is around -1.5 with \(df = min(212 - 1, 175 - 1) = 174\). Recall that for large degrees of freedom, the \(t\) distribution is roughly equal to the standard normal curve so our difference in df for the Satterthwaite and “min” variations doesn’t really matter.

B.5.7 Compute \(p\)-value

The \(p\)-value—the probability of observing an \(t_{174}\) value of -1.501 or more extreme (in both directions) in our null distribution—is 0.13. This can also be calculated in R directly:

2 * pt(-1.501, df = min(212 - 1, 175 - 1), lower.tail = TRUE)[1] 0.1352We can also approximate by using the standard normal curve:

2 * pnorm(-1.501)[1] 0.1334Note that the 95 percent confidence interval given above matches well with the one calculated using bootstrapping.

B.5.8 State conclusion

We, therefore, do not have sufficient evidence to reject the null hypothesis. Our initial guess that a statistically significant difference not existing in the means was backed by this statistical analysis. We do not have evidence to suggest that the true mean income differs between Cleveland, OH and Sacramento, CA based on this data.

B.5.9 Comparing results

Observing the bootstrap distribution and the null distribution that were created, it makes quite a bit of sense that the results are so similar for traditional and non-traditional methods in terms of the \(p\)-value and the confidence interval since these distributions look very similar to normal distributions. The conditions also being met leads us to better guess that using any of the methods whether they are traditional (formula-based) or non-traditional (computational-based) will lead to similar results.

B.6 Two means (paired samples)

B.6.0.1 Problem statement

Trace metals in drinking water affect the flavor and an unusually high concentration can pose a health hazard. Ten pairs of data were taken measuring zinc concentration in bottom water and surface water at 10 randomly selected locations on a stretch of river. Do the data suggest that the true average concentration in the surface water is smaller than that of bottom water? (Note that units are not given.) [Tweaked a bit from https://onlinecourses.science.psu.edu/stat500/node/51]

B.6.1 Competing hypotheses

B.6.1.1 In words

Null hypothesis: The mean concentration in the bottom water is the same as that of the surface water at different paired locations.

Alternative hypothesis: The mean concentration in the surface water is smaller than that of the bottom water at different paired locations.

B.6.1.2 In symbols (with annotations)

- \(H_0: \mu_{diff} = 0\), where \(\mu_{diff}\) represents the mean difference in concentration for surface water minus bottom water.

- \(H_A: \mu_{diff} < 0\)

B.6.1.3 Set \(\alpha\)

It’s important to set the significance level before starting the testing using the data. Let’s set the significance level at 5% here.

B.6.2 Exploring the sample data

#download.file("http://ismayc.github.io/teaching/sample_problems/zinc_tidy.csv",

# destfile = "data/zinc_tidy.csv",

# method = "curl")

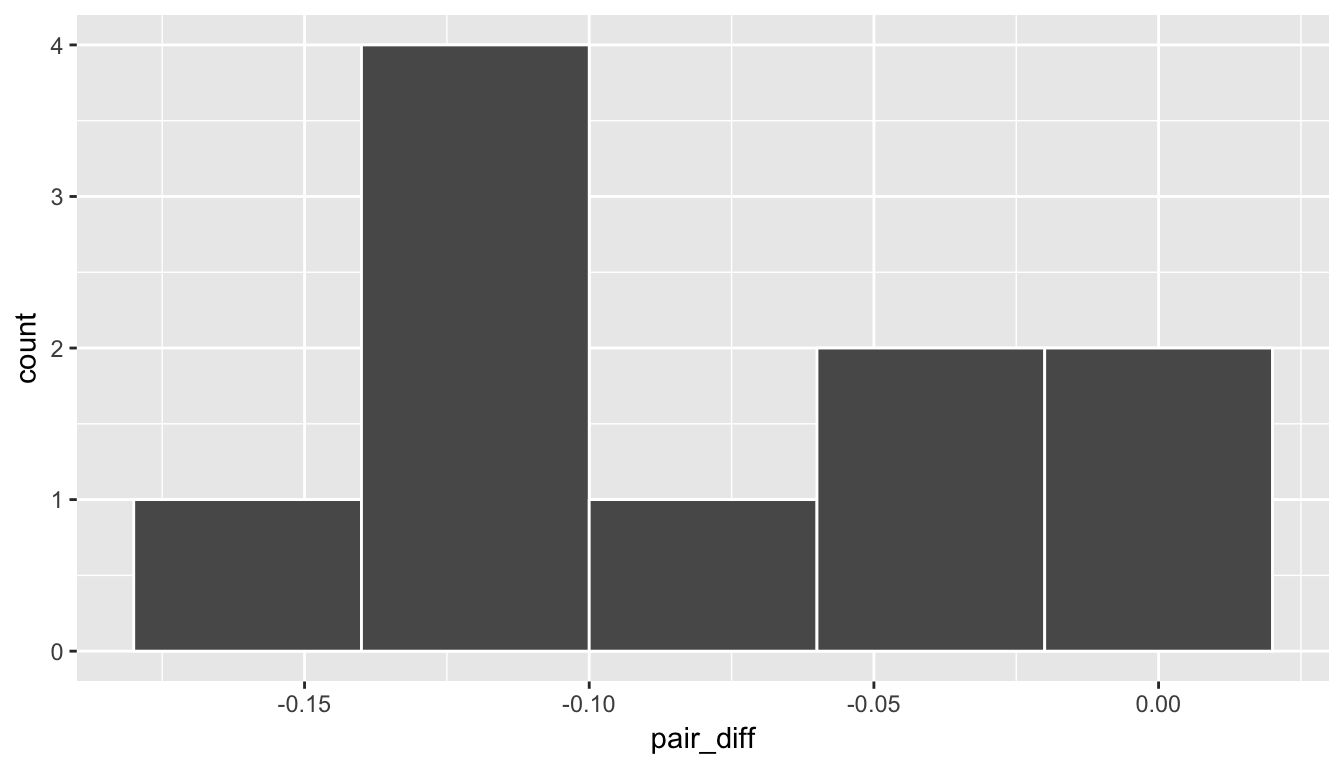

zinc_tidy <- read_csv("data/zinc_tidy.csv")We want to look at the differences in surface - bottom for each location:

zinc_diff <- zinc_tidy %>%

group_by(loc_id) %>%

summarize(pair_diff = diff(concentration))zinc_summ <- zinc_diff %>%

summarize(sample_size = n(),

mean = mean(pair_diff),

sd = sd(pair_diff),

minimum = min(pair_diff),

lower_quartile = quantile(pair_diff, 0.25),

median = median(pair_diff),

upper_quartile = quantile(pair_diff, 0.75),

max = max(pair_diff))

kable(zinc_summ)| sample_size | mean | sd | minimum | lower_quartile | median | upper_quartile | max |

|---|---|---|---|---|---|---|---|

| 10 | -0.0804 | 0.0523 | -0.177 | -0.11 | -0.084 | -0.0355 | -0.015 |

The histogram below also shows the distribution of pair_diff.

ggplot(zinc_diff, aes(x = pair_diff)) +

geom_histogram(binwidth = 0.04, color = "white")

B.6.2.1 Guess about statistical significance

We are looking to see if the sample paired mean difference of -0.0804 is statistically less than 0. They seem to be quite close, but we have a small number of pairs here. Let’s guess that we will fail to reject the null hypothesis.

B.6.3 Non-traditional methods

B.6.3.1 Collecting summary info

Next we will assign some key values to variable names in R:

obs_diff <- zinc_summ$mean

n_pairs <- zinc_summ$sample_sizeB.6.3.2 Randomization for hypothesis test

In order to look to see if the observed sample mean difference \(\bar{x}_{diff} = -0.0804\) is statistically less than 0, we need to account for the number of pairs. We also need to determine a process that replicates how the paired data was selected in a way similar to how we calculated our original difference in sample means.

We can use the idea of randomization testing (also known as permutation testing) to simulate the population from which the sample came and then generate samples using shuffling from that simulated population to account for sampling variability. In this case, we will shuffle along each paired location. So values that were on the bottom of location 1 may now be switched to be on the surface or vice versa.

set.seed(2017)

many_shuffles <- do(10000) *

(zinc_tidy %>%

mutate(location = shuffle(location, groups = loc_id)) %>%

group_by(loc_id) %>%

summarize(pair_diff = diff(concentration))

)

null_distn_paired_means <- many_shuffles %>%

group_by(.index) %>%

summarize(mean_diff = mean(pair_diff))ggplot(null_distn_paired_means, aes(x = mean_diff)) +

geom_histogram(bins = 30, color = "white")

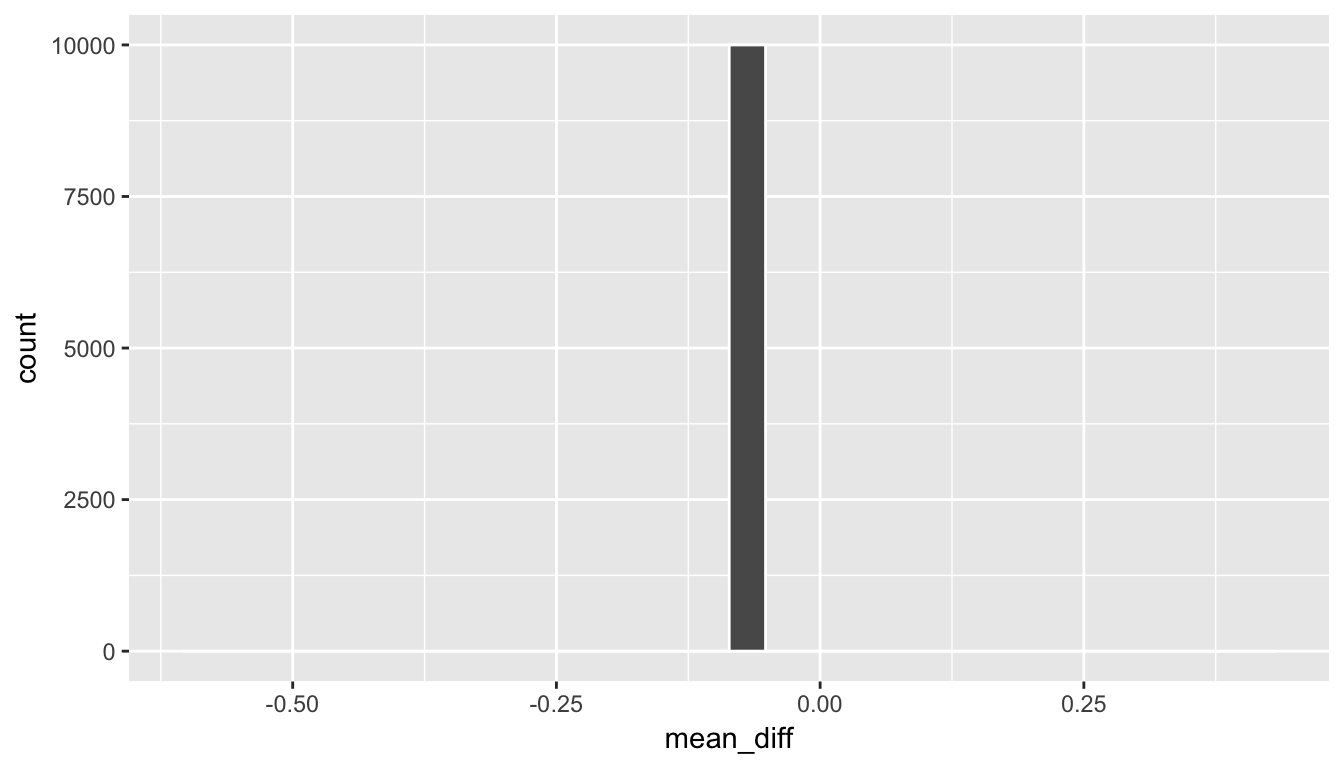

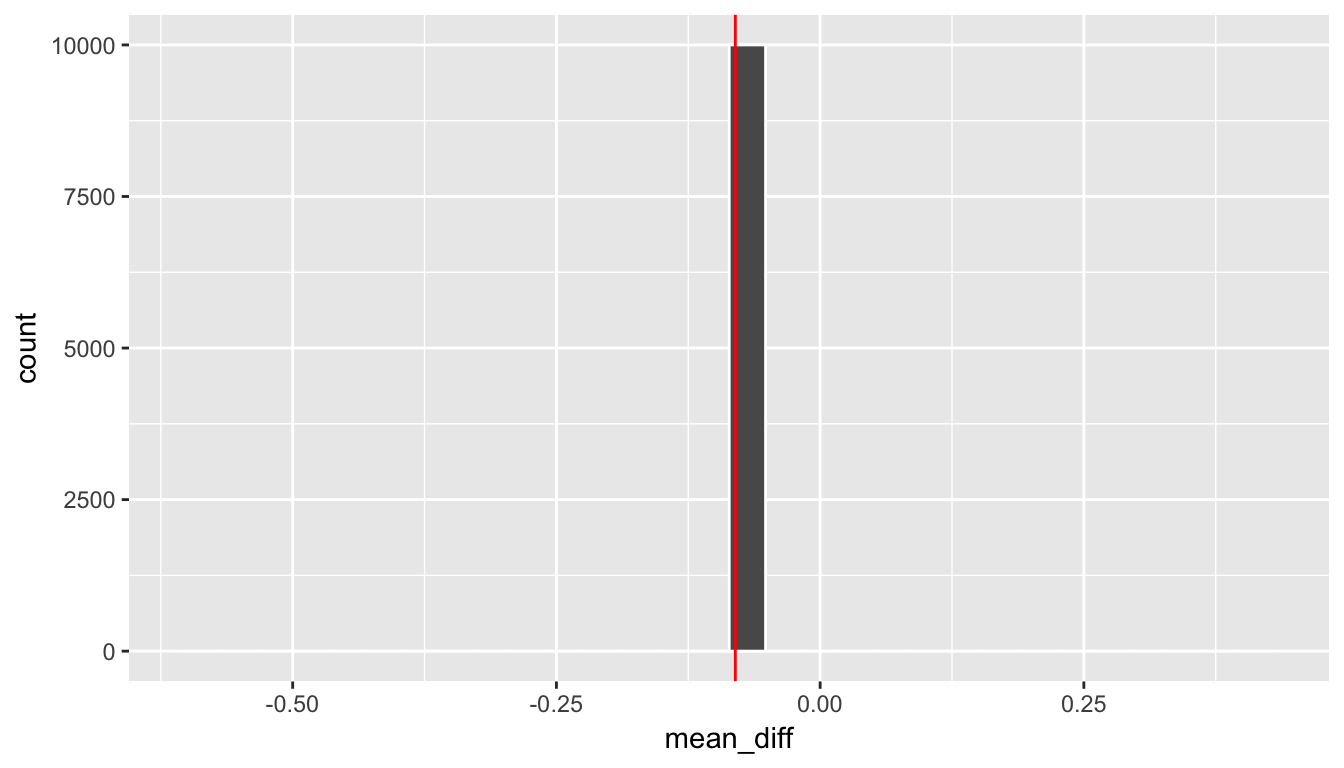

We can next use this distribution to observe our \(p\)-value. Recall this is a left-tailed test so we will be looking for values that are less than or equal to -0.0804 for our \(p\)-value.

ggplot(null_distn_paired_means, aes(x = mean_diff)) +

geom_histogram(bins = 30, color = "white") +

geom_vline(color = "red", xintercept = obs_diff)

B.6.3.2.1 Calculate \(p\)-value

pvalue <- null_distn_paired_means %>%

filter(mean_diff <= obs_diff) %>%

nrow() / nrow(null_distn_paired_means)

pvalue[1] 1So our \(p\)-value is essentially 1 and we reject the null hypothesis at the 5% level. You can also see this from the histogram above that we are far into the left tail of the null distribution.

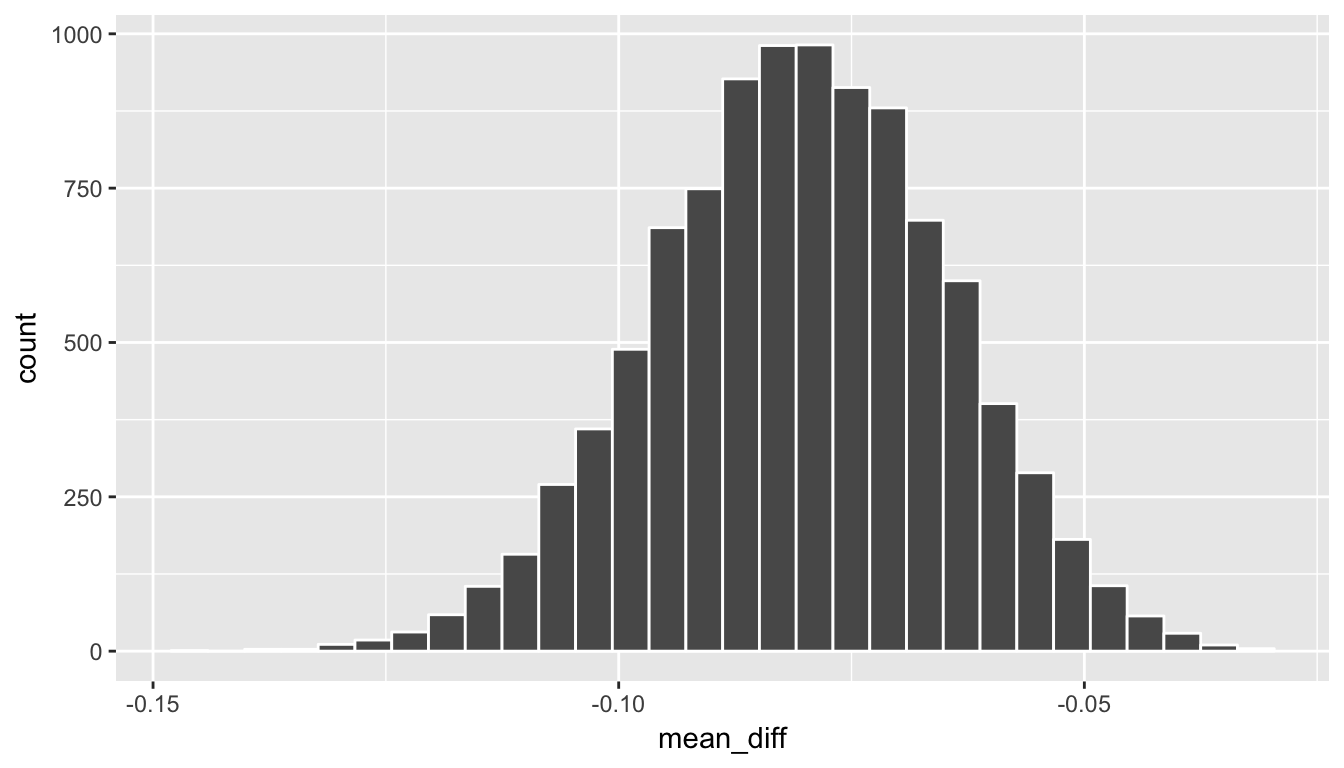

B.6.3.3 Bootstrapping for confidence interval

We can also create a confidence interval for the unknown population parameter \(\mu_{diff}\) using our sample data (the calculated differences) with bootstrapping. This is similar to the bootstrapping done in a one sample mean case, except now our data is differences instead of raw numerical data.

boot_distn_paired_means <- do(10000) *

resample(zinc_diff, replace = TRUE) %>%

summarize(mean_diff = mean(pair_diff))ggplot(boot_distn_paired_means, aes(x = mean_diff)) +

geom_histogram(bins = 30, color = "white")

boot_distn_paired_means %>%

summarize(lower = quantile(mean_diff, probs = 0.025),

upper = quantile(mean_diff, probs = 0.975)) lower upper

1 -0.1119 -0.0506We see that 0 is not contained in this confidence interval as a plausible value of \(\mu_{diff}\) (the unknown population parameter). This matches with our hypothesis test results of rejecting the null hypothesis. Since zero is not a plausible value of the population parameter and since the entire confidence interval falls below zero, we have evidence that surface zinc concentration levels are lower, on average, than bottom level zinc concentrations.

Interpretation: We are 95% confident the true mean zinc concentration on the surface is between 1345.78 units smaller to -11440.64 units smaller than on the bottom.

Note: You could also use the null distribution based on randomization with a shift to have its center at \(\bar{x}_{diff} = -0.08\) instead of at 0 and calculate its percentiles. The confidence interval produced via this method should be comparable to the one done using bootstrapping above.

B.6.4 Traditional methods

B.6.4.1 Check conditions

Remember that in order to use the shortcut (formula-based, theoretical) approach, we need to check that some conditions are met.

- Independent observations: The observations among pairs are independent.

The locations are selected independently through random sampling so this condition is met.

Approximately normal: The distribution of population of differences is normal or the number of pairs is at least 30.

The histogram above does show some skew so we have reason to doubt the population being normal based on this sample. We also only have 10 pairs which is fewer than the 30 needed. A theory-based test may not be valid here.

B.6.4.2 Test statistic

The test statistic is a random variable based on the sample data. Here, we want to look at a way to estimate the population mean difference \(\mu_{diff}\). A good guess is the sample mean difference \(\bar{X}_{diff}\). Recall that this sample mean is actually a random variable that will vary as different samples are (theoretically, would be) collected. We are looking to see how likely is it for us to have observed a sample mean of \(\bar{x}_{diff, obs} = 0.0804\) or larger assuming that the population mean difference is 0 (assuming the null hypothesis is true). If the conditions are met and assuming \(H_0\) is true, we can “standardize” this original test statistic of \(\bar{X}_{diff}\) into a \(T\) statistic that follows a \(t\) distribution with degrees of freedom equal to \(df = n - 1\):

\[ T =\dfrac{ \bar{X}_{diff} - 0}{ S_{diff} / \sqrt{n} } \sim t (df = n - 1) \]

where \(S\) represents the standard deviation of the sample differences and \(n\) is the number of pairs.

B.6.4.2.1 Observed test statistic

While one could compute this observed test statistic by “hand”, the focus here is on the set-up of the problem and in understanding which formula for the test statistic applies. We can use the t.test function on the differences to perform this analysis for us.

stats::t.test(x = zinc_diff$pair_diff,

alternative = "less",

mu = 0)

One Sample t-test

data: zinc_diff$pair_diff

t = -4.9, df = 9, p-value = 0.0004

alternative hypothesis: true mean is less than 0

95 percent confidence interval:

-Inf -0.0501

sample estimates:

mean of x

-0.0804 We see here that the \(t_{obs}\) value is around -5.

B.6.4.3 Compute \(p\)-value

The \(p\)-value—the probability of observing a \(t_{obs}\) value of -5 or less in our null distribution of a \(t\) with 9 degrees of freedom—is 0.0004. This can also be calculated in R directly:

pt(-5, df = nrow(zinc_diff) - 1, lower.tail = TRUE)[1] 0.0003695B.6.4.4 State conclusion

We, therefore, have sufficient evidence to reject the null hypothesis. Our initial guess that our observed sample mean difference was not statistically less than the hypothesized mean of 0 has been invalidated here. Based on this sample, we have evidence that the mean concentration in the bottom water is greater than that of the surface water at different paired locations.

B.6.5 Comparing results

Observing the bootstrap distribution and the null distribution that were created, it makes quite a bit of sense that the results are so similar for traditional and non-traditional methods in terms of the \(p\)-value and the confidence interval since these distributions look very similar to normal distributions. The conditions were not met since the number of pairs was small, but the sample data was not highly skewed. Using any of the methods whether they are traditional (formula-based) or non-traditional (computational-based) lead to similar results.