Lecture 8 Note

2021-07-30

Chapter 1 Some update of goodness of fit

## ── Attaching packages ─────────────────────────────────────── tidyverse 1.3.1 ──## ✓ ggplot2 3.3.5 ✓ purrr 0.3.4

## ✓ tibble 3.1.2 ✓ dplyr 1.0.7

## ✓ tidyr 1.1.3 ✓ stringr 1.4.0

## ✓ readr 1.4.0 ✓ forcats 0.5.1## ── Conflicts ────────────────────────────────────────── tidyverse_conflicts() ──

## x dplyr::filter() masks stats::filter()

## x dplyr::lag() masks stats::lag()## Loading required package: lubridate##

## Attaching package: 'lubridate'## The following objects are masked from 'package:base':

##

## date, intersect, setdiff, union## Loading required package: PerformanceAnalytics## Loading required package: xts## Loading required package: zoo##

## Attaching package: 'zoo'## The following objects are masked from 'package:base':

##

## as.Date, as.Date.numeric##

## Attaching package: 'xts'## The following objects are masked from 'package:dplyr':

##

## first, last##

## Attaching package: 'PerformanceAnalytics'## The following object is masked from 'package:graphics':

##

## legend## Loading required package: quantmod## Loading required package: TTR## Registered S3 method overwritten by 'quantmod':

## method from

## as.zoo.data.frame zoo## ══ Need to Learn tidyquant? ════════════════════════════════════════════════════

## Business Science offers a 1-hour course - Learning Lab #9: Performance Analysis & Portfolio Optimization with tidyquant!

## </> Learn more at: https://university.business-science.io/p/learning-labs-pro </>## Registered S3 method overwritten by 'rmutil':

## method from

## print.response httr##

## Attaching package: 'rmutil'## The following object is masked from 'package:tidyr':

##

## nesting## The following object is masked from 'package:stats':

##

## nobs## The following objects are masked from 'package:base':

##

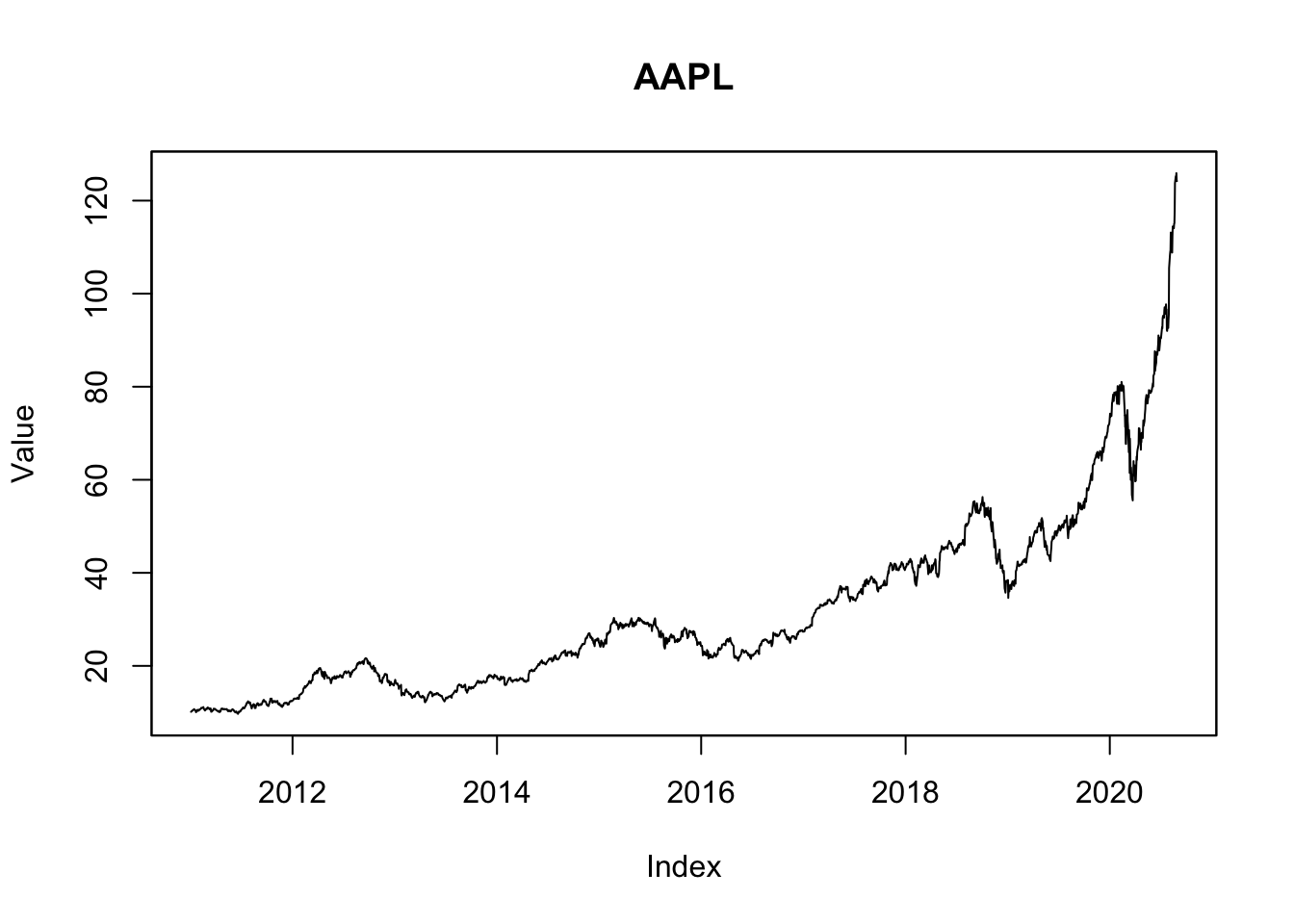

## as.data.frame, units1.1 Plot the value

par(mfcol=c(1,1))

Y00=casestudy1.data0.00[,Y00.name0]

plot(Y00, ylab="Value",main=Y00.name0)

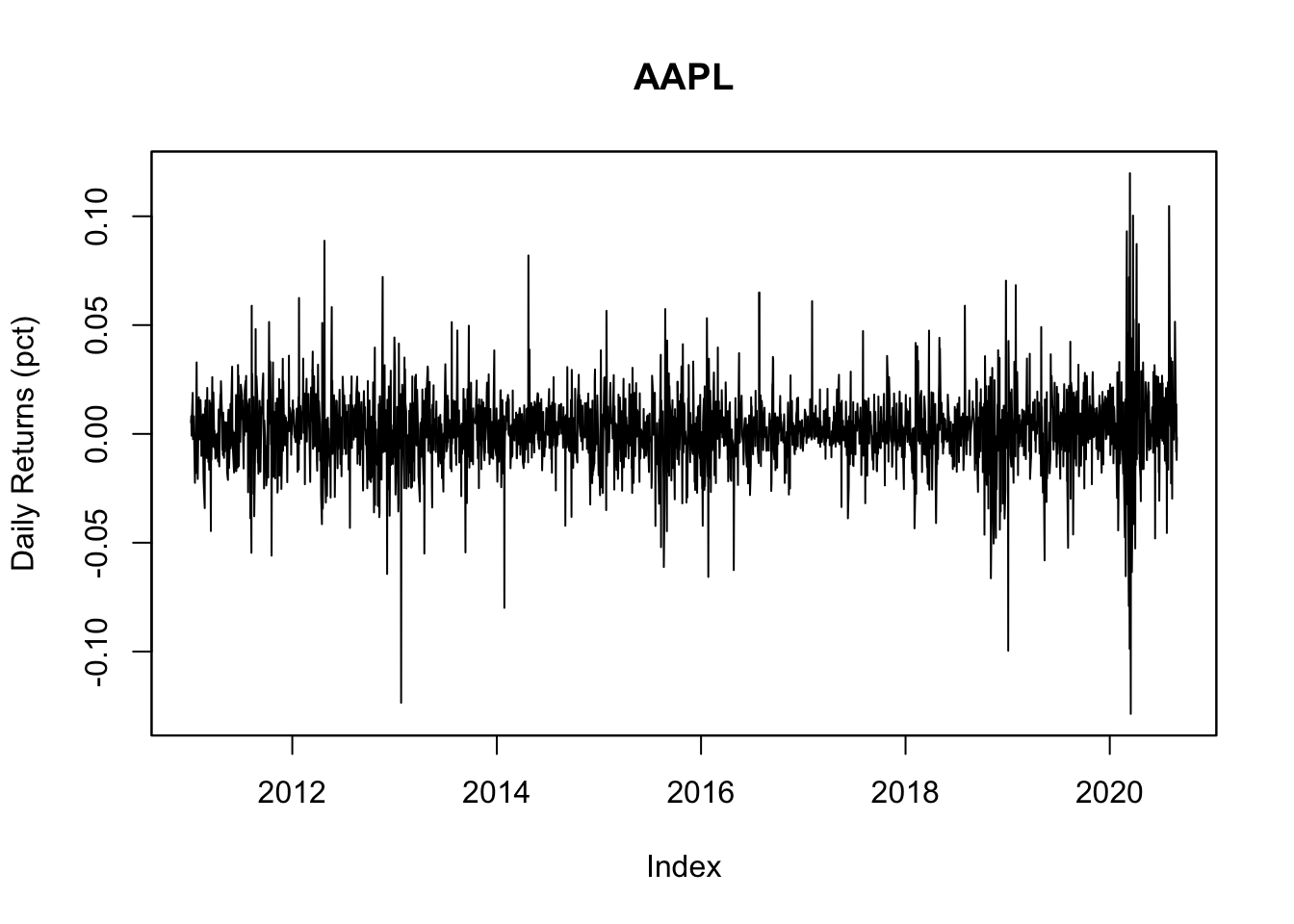

1.2 Plot the daily return

y00<-zoo( x=as.matrix(exp(diff(log(Y00)))-1),

order.by=time(Y00)[-1])

names(y00)<-"y00"

plot(y00, ylab="Daily Returns (pct)",main=Y00.name0)

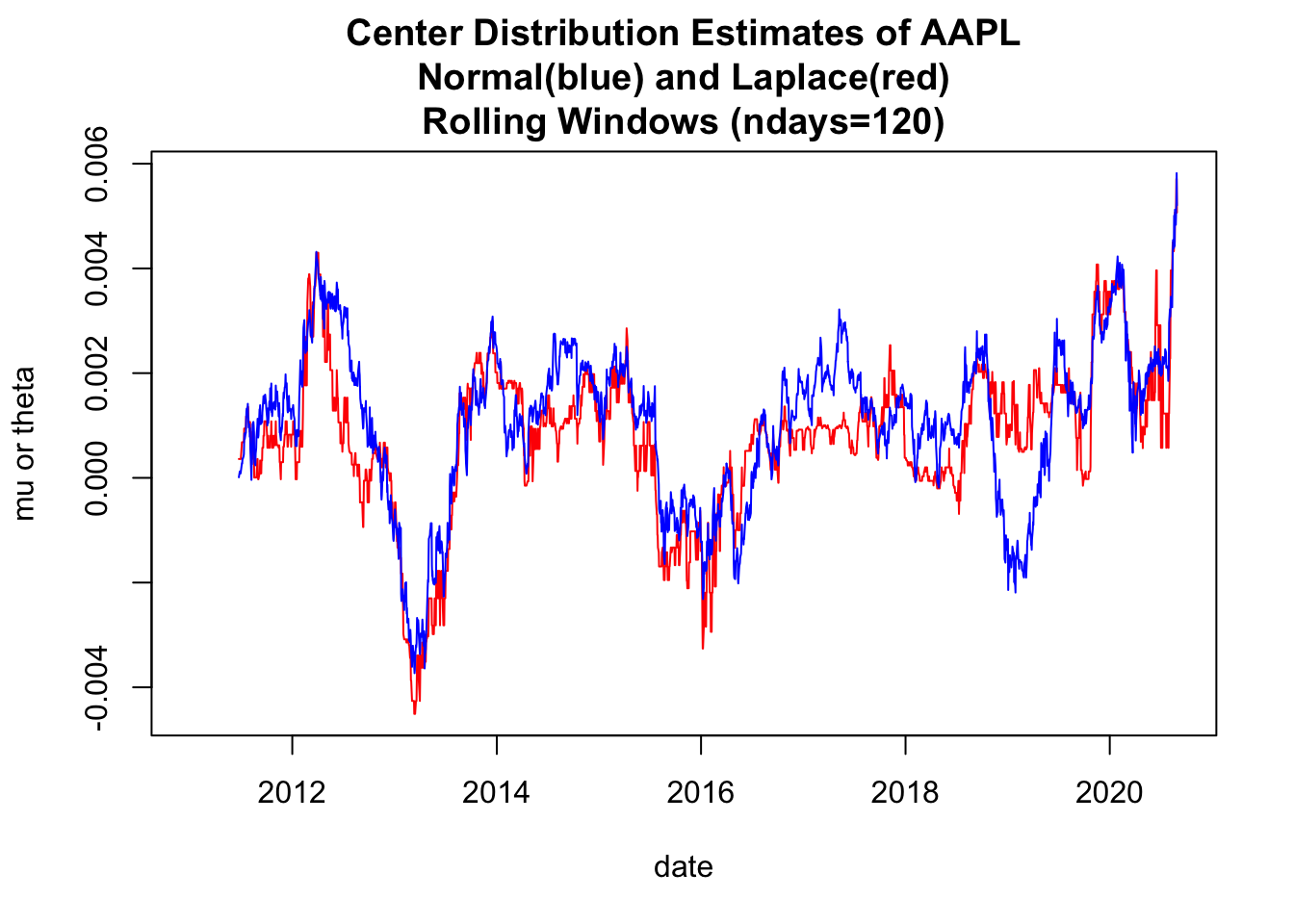

1.3 Use base plot to plot Rolling Estimates of mu/median

# 4.1 Use base plot to plot Rolling Estimates of mu/median -----

y00both<-c(y00_df1$muNormal ,

y00_df1$thetaLaplace)

ylim0<-c(min(y00both,na.rm=TRUE), max(y00both,na.rm=TRUE))

plot(x=y00_df1$date,y=y00_df1$thetaLaplace,

ylim=ylim0,

col='red',type="l",

ylab="mu or theta",xlab="date")

lines(x=y00_df1$date,y=y00_df1$muNormal, col='blue',type="l")

title(main=paste(c(

"Center Distribution Estimates of ", Y00.name0,

"\nNormal(blue) and Laplace(red)",

"\nRolling Windows (ndays=",ndays0,")"),

collapse=""))

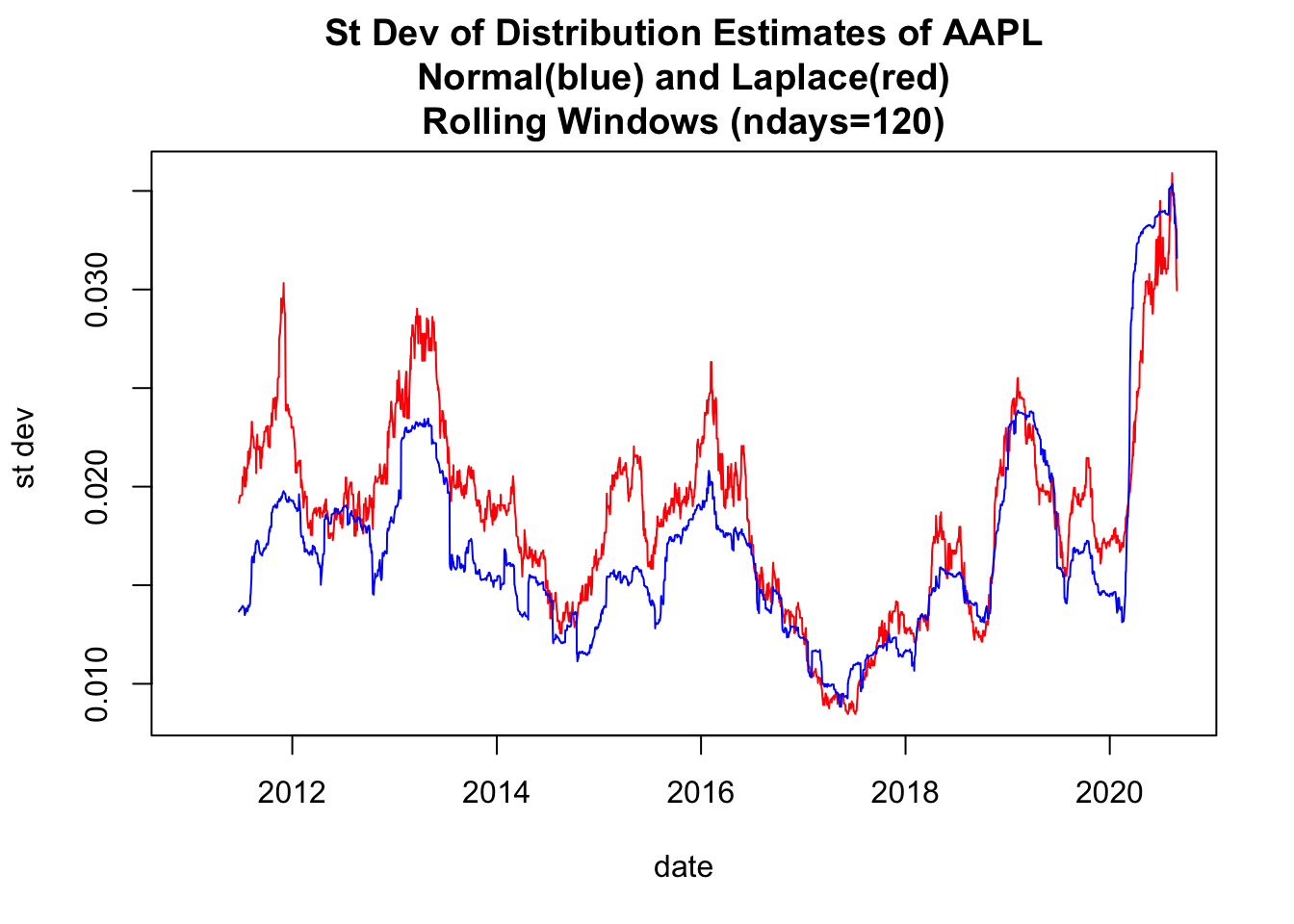

1.4 Use base plot to plot Rolling Estimates of st. devs

# 4.2 Use base plot to plot Rolling Estimates of st. devs -----

y00both<-c(y00_df1$sigmaNormal ,

y00_df1$scaleLaplace*sqrt(2))

ylim0<-c(min(y00both,na.rm=TRUE), max(y00both,na.rm=TRUE))

plot(x=y00_df1$date,y=y00_df1$scaleLaplace*sqrt(2),

ylim=ylim0,

col='red',type="l",

ylab="st dev ",xlab="date")

lines(x=y00_df1$date,y=y00_df1$sigmaNormal, col='blue',type="l")

title(main=paste(c(

"St Dev of Distribution Estimates of ", Y00.name0,

"\nNormal(blue) and Laplace(red)",

"\nRolling Windows (ndays=",ndays0,")"),

collapse=""))

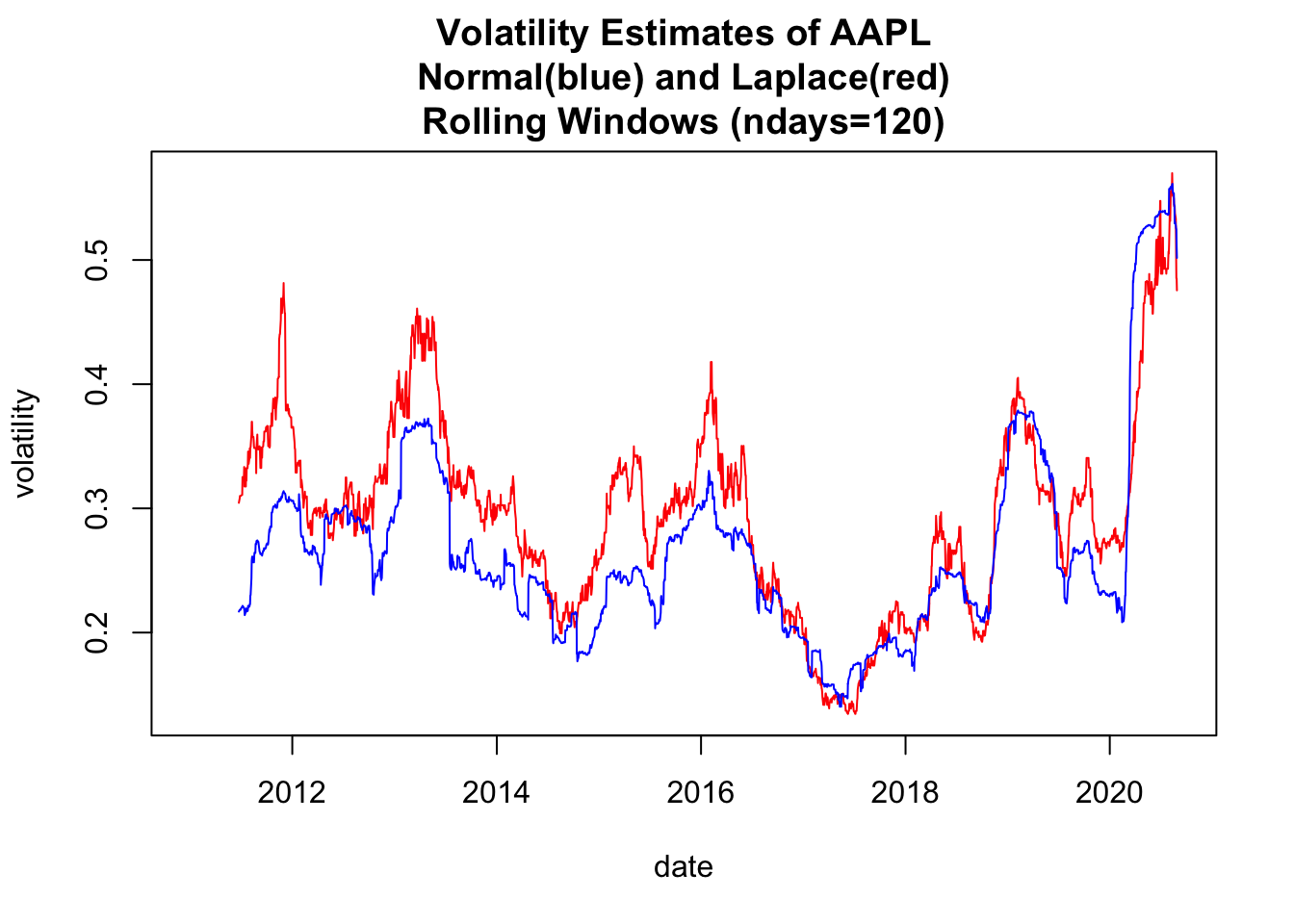

1.5 Use base plot to plot Rolling Volatilities

# 4.3 Use base plot() to plot Rolling Volatilities ----

y00both<-c(y00_df1$volLaplace, y00_df1$volNormal)

ylim0<-c(min(y00both,na.rm=TRUE), max(y00both,na.rm=TRUE))

plot(x=y00_df1$date,y=y00_df1$volLaplace,

ylim=ylim0,

col='red',type="l",

ylab="volatility",xlab="date")

lines(x=y00_df1$date,y=y00_df1$volNormal, col='blue',type="l",

ylab="volatility")

title(main=paste(c(

"Volatility Estimates of ", Y00.name0,

"\nNormal(blue) and Laplace(red)",

"\nRolling Windows (ndays=",ndays0,")"),

collapse=""))

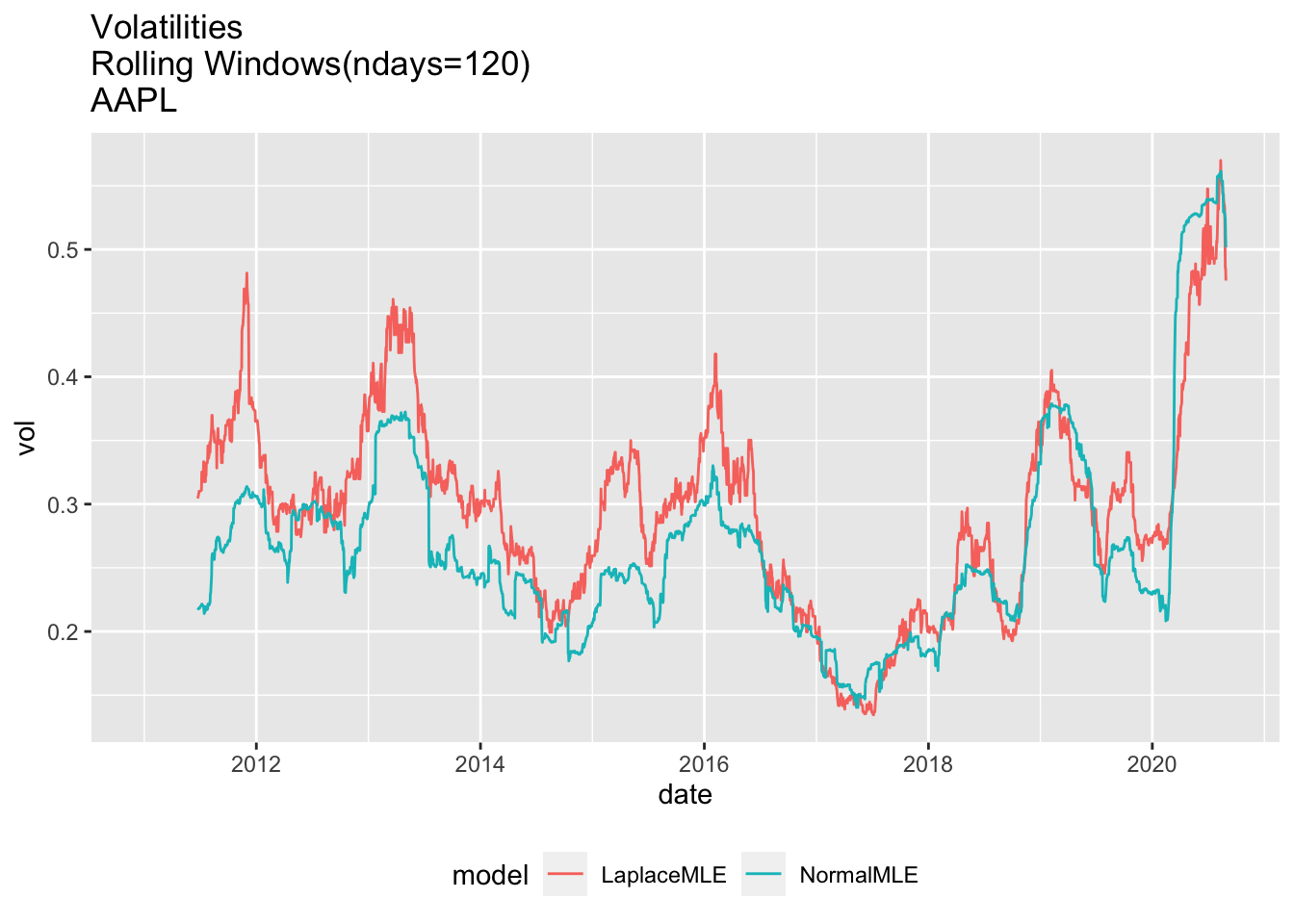

1.6 Use ggplot2 to plot Rolling Volatilities

# 4.4 Use ggplot2 to plot Rolling Volatilities ----

df2<-rbind(

data.frame(

date=y00_df1$date,

vol=y00_df1$volNormal,

model="NormalMLE",

ndays=ndays0),

data.frame(

date=y00_df1$date,

vol=y00_df1$volLaplace,

model="LaplaceMLE",

ndays=ndays0))

df2$model=as.factor(df2$model)

dim(df2)## [1] 4860 4gg0<-ggplot(df2, aes(x=date, y=vol, col=model)) + geom_line() +

theme(legend.position="bottom") +

ggtitle(paste(c("Volatilities \nRolling Windows(ndays=", as.character(ndays0),

")\n", Y00.name0),collapse="")

)

print(gg0)## Warning: Removed 238 row(s) containing missing values (geom_path).

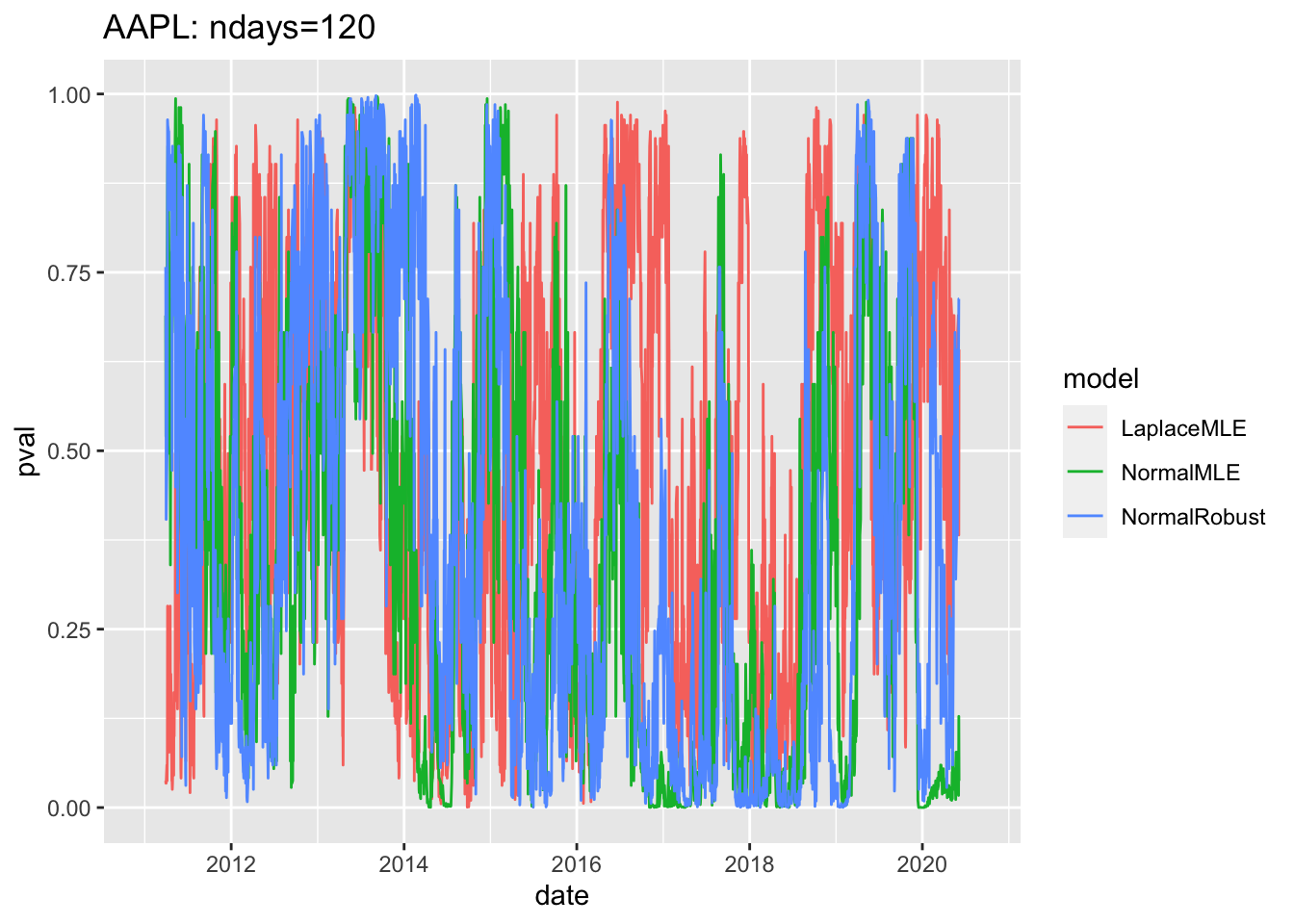

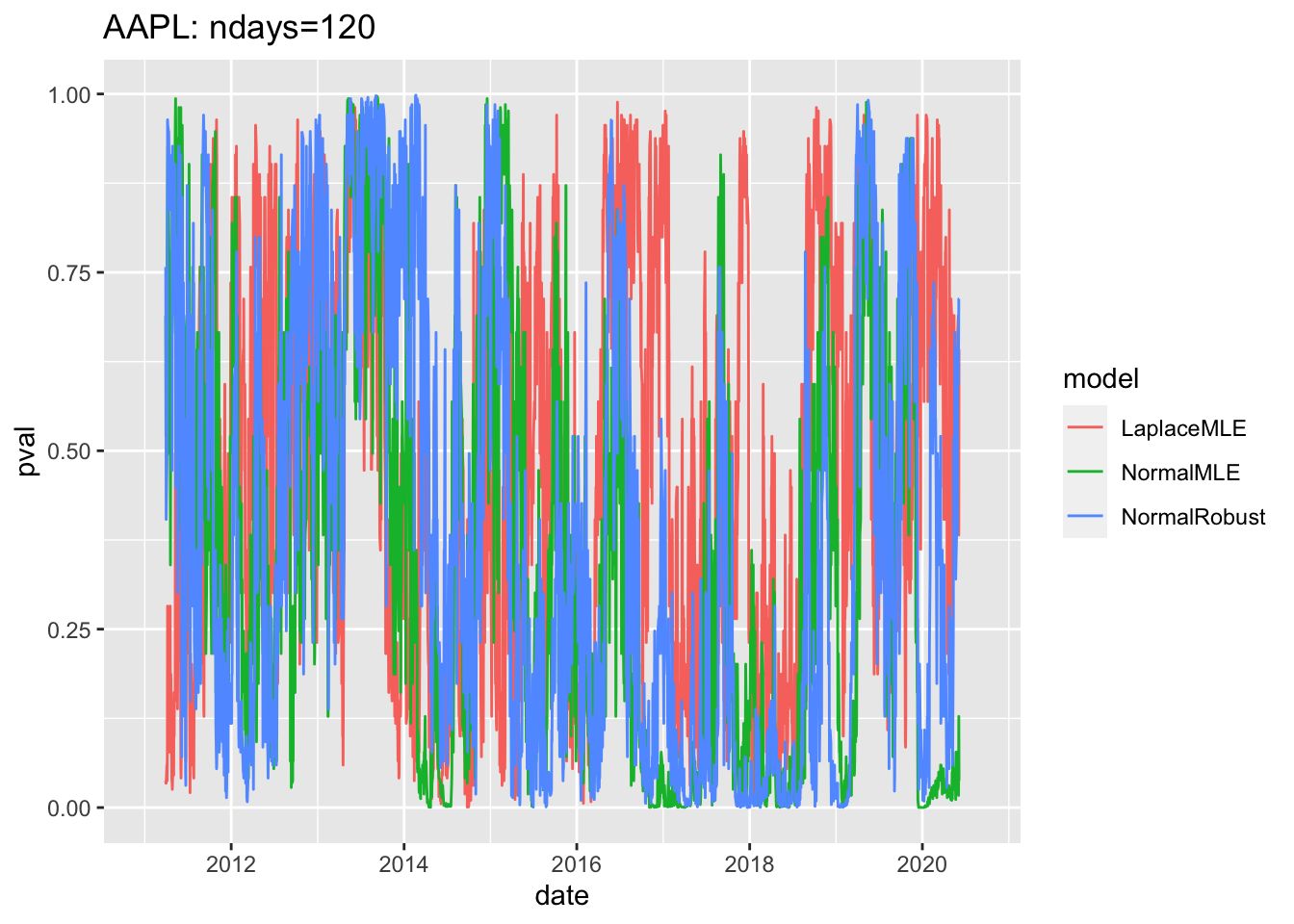

#4.4 Use ggplot2 to plot pvalues of Rolling Fits1.7 Plot pvalues for entire period

# 4.5 Plot pvalues for entire period ----

gg3<-ggplot(df3, aes(x=date, y=pval, col=model))+geom_line()

print(gg3+ggtitle(label=paste(c(

Y00.name0,": ndays=",df3$ndays[1]),

collapse="")

)) ## Warning: Removed 357 row(s) containing missing values (geom_path).

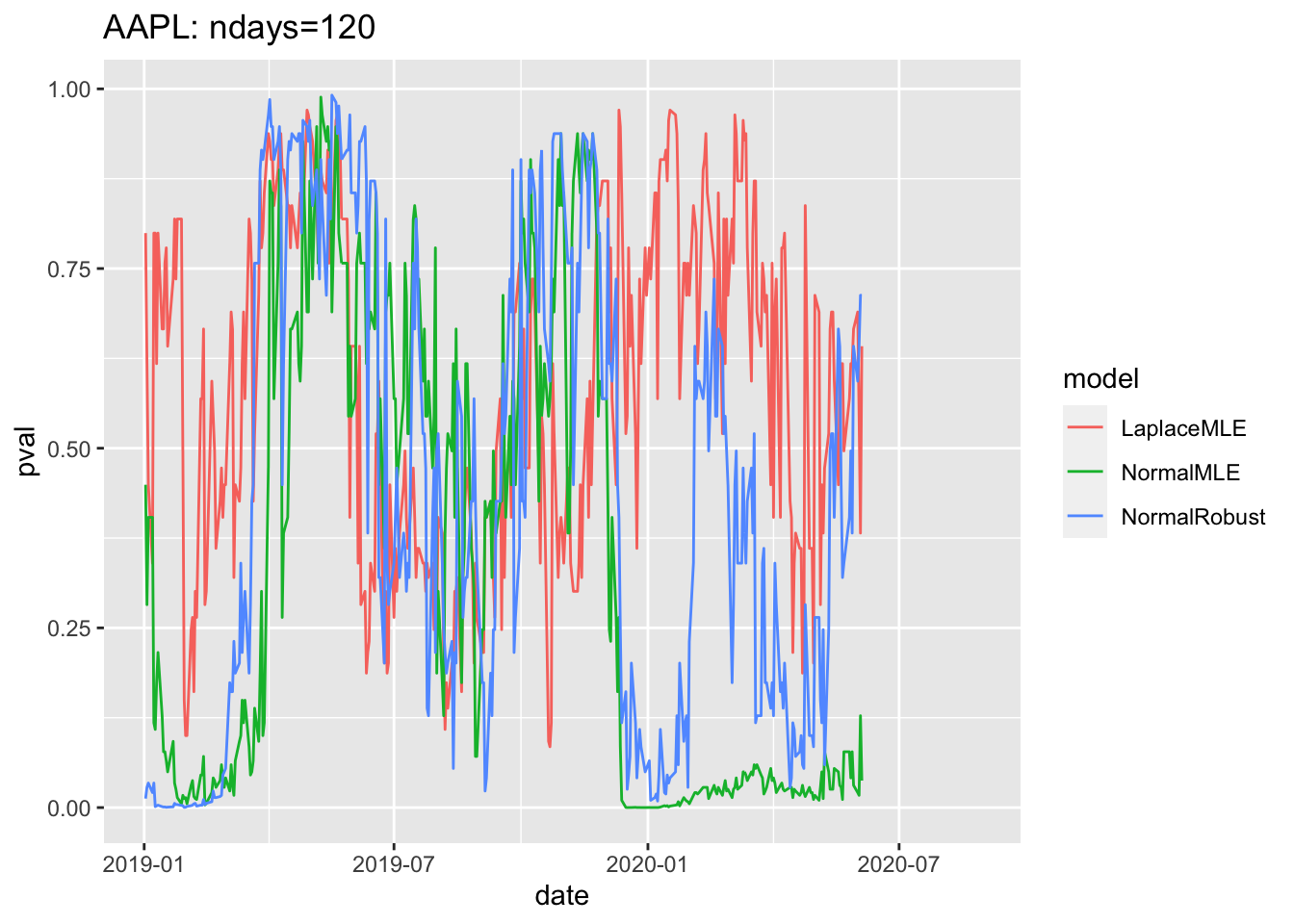

1.8 Sample plot of pvalues since 2019

# 4.6 Sample plot of pvalues since 2019 ----

gg4<-df3 %>% filter(date>=as.Date("2019-01-01")) %>%

ggplot( aes(x=date, y=pval, col=model))+geom_line()

print(gg4 + ggtitle(label=paste(c(

Y00.name0,": ndays=",df3$ndays[1]),

collapse="")

))## Warning: Removed 180 row(s) containing missing values (geom_path).

1.9 Change \(y\) scale to \(log(p)/log(0.05)\)

# 4.5 Plot pvalues for entire period ----

gg3b<-ggplot(df3, aes(x=date, y=log(pval)/log(0.05), col=model))+geom_line()

print(gg3+ggtitle(label=paste(c(

Y00.name0,": ndays=",df3$ndays[1]),

collapse="")

)) ## Warning: Removed 357 row(s) containing missing values (geom_path).

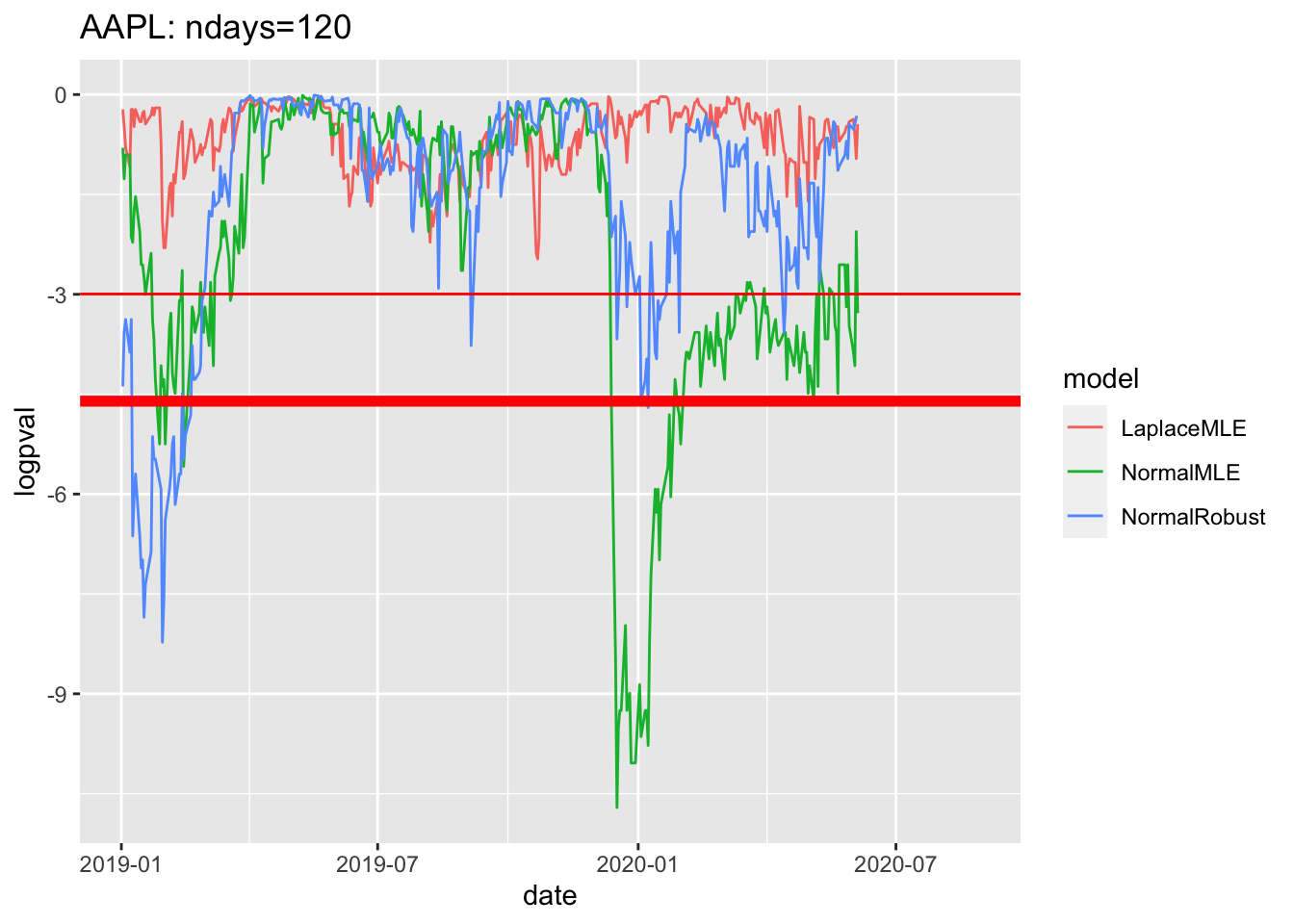

1.10 Sample plot of log pvalues since 2019

# 4.6 Sample plot of pvalues since 2019 ----

df3$logpval=log(df3$pval)

gg4<-df3 %>% filter(date>=as.Date("2019-01-01")) %>%

ggplot( aes(x=date, y=logpval, col=model))+geom_line()+

geom_hline(yintercept=log(0.05), col='red')+

geom_hline(yintercept=log(0.01),col='red', lwd=2)

geom_hline(yintercept=log(0.01),col='red', lwd=2)## mapping: yintercept = ~yintercept

## geom_hline: na.rm = FALSE

## stat_identity: na.rm = FALSE

## position_identityprint(gg4 + ggtitle(label=paste(c(

Y00.name0,": ndays=",df3$ndays[1]),

collapse="")

))## Warning: Removed 180 row(s) containing missing values (geom_path).

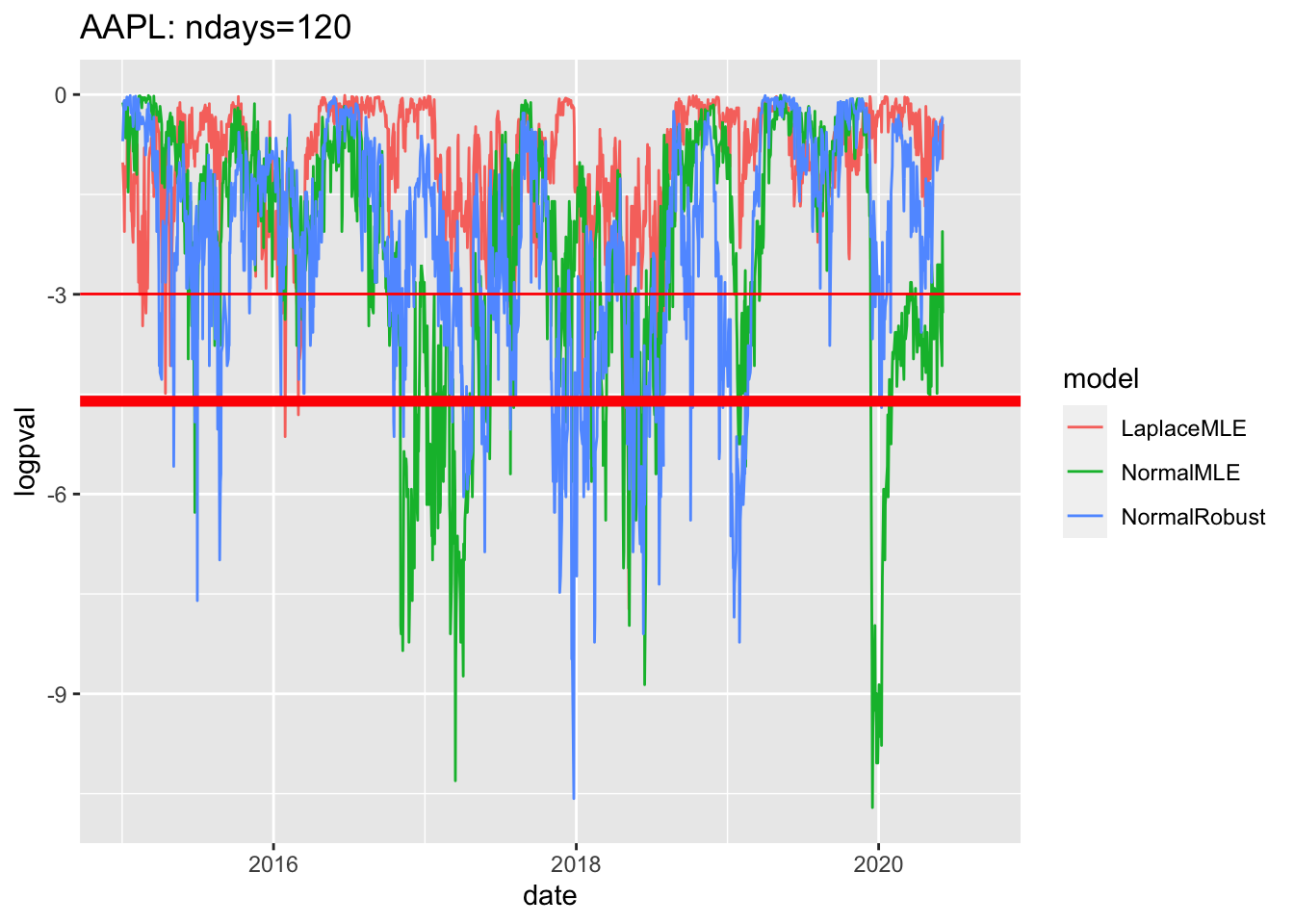

# 4.6 Sample plot of pvalues since 2019 ----

df3$logpval=log(df3$pval)

gg4<-df3 %>% filter(date>=as.Date("2015-01-01")) %>%

ggplot( aes(x=date, y=logpval, col=model))+geom_line()+

geom_hline(yintercept=log(0.05), col='red')+

geom_hline(yintercept=log(0.01),col='red', lwd=2)

geom_hline(yintercept=log(0.01),col='red', lwd=2)## mapping: yintercept = ~yintercept

## geom_hline: na.rm = FALSE

## stat_identity: na.rm = FALSE

## position_identityprint(gg4 + ggtitle(label=paste(c(

Y00.name0,": ndays=",df3$ndays[1]),

collapse="")

))## Warning: Removed 180 row(s) containing missing values (geom_path).

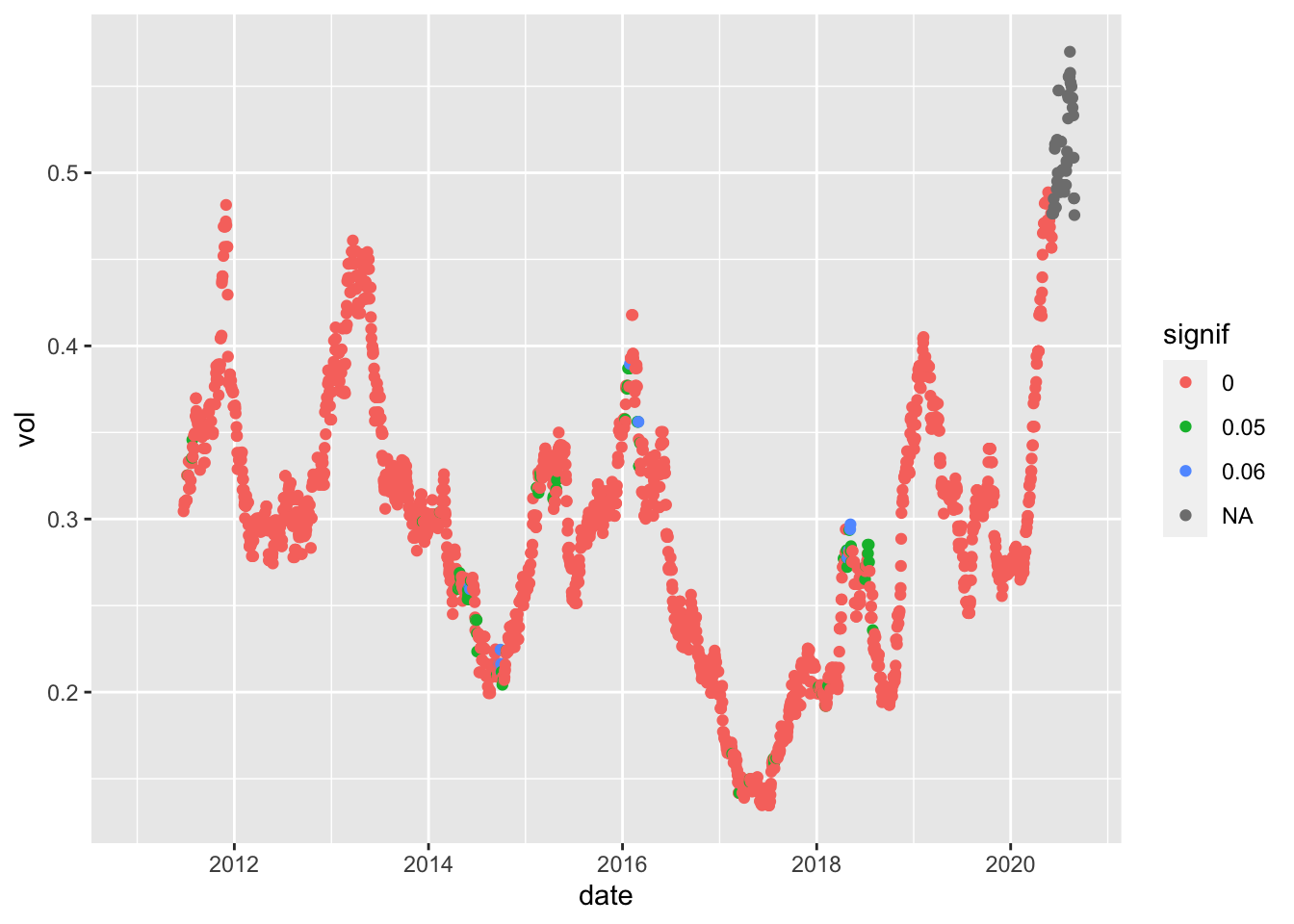

df2_sub1<-df2_AAPL_120 %>% filter(model=="LaplaceMLE")

dim(df2_sub1)## [1] 2430 4pval_sub<-pvals_AAPL_120 %>% filter(model=="LaplaceMLE")

dim(pval_sub)## [1] 2430 4names(pval_sub)## [1] "date" "pval" "model" "ndays"df2_sub1$pval<-pval_sub$pval

df2_sub1$signif<-.05*(pval_sub$pval < .05) + .01*(pval_sub$pval<.01)

df2_sub1$signif<-factor(df2_sub1$signif)

ggplot(df2_sub1, aes(x=date, y=vol, col=signif)) + geom_point()## Warning: Removed 119 rows containing missing values (geom_point).