Chapter 11 Exploratory analysis of time series data: Examples

11.1 Example: Monthly electricity sales for Virginia

11.1.1 Extract data from remote database

esales <- dbGetQuery(db,'SELECT * from eia_elec_sales_va_all_m') # SQL code to retrieve data from a table in the remote database

# str(esales)

esales <- as_tibble(esales) # Convert dataframe to a 'tibble' for tidyverse work

# str(esales)11.1.2 Briefly characterize the dataset

## # A tibble: 233 x 4

## value date year month

## <dbl> <date> <int> <int>

## 1 8282. 2020-05-01 2020 5

## 2 7839. 2020-04-01 2020 4

## 3 8889. 2020-03-01 2020 3

## 4 9368. 2020-02-01 2020 2

## 5 9209. 2020-01-01 2020 1

## 6 10038. 2019-12-01 2019 12

## 7 9291. 2019-11-01 2019 11

## 8 8757. 2019-10-01 2019 10

## 9 9874. 2019-09-01 2019 9

## 10 10912. 2019-08-01 2019 8

## # … with 223 more rows## value date year month

## Min. : 7153 Min. :2001-01-01 Min. :2001 Min. : 1.000

## 1st Qu.: 8200 1st Qu.:2005-11-01 1st Qu.:2005 1st Qu.: 3.000

## Median : 9019 Median :2010-09-01 Median :2010 Median : 6.000

## Mean : 9093 Mean :2010-08-31 Mean :2010 Mean : 6.425

## 3rd Qu.: 9885 3rd Qu.:2015-07-01 3rd Qu.:2015 3rd Qu.: 9.000

## Max. :11724 Max. :2020-05-01 Max. :2020 Max. :12.000

# References: https://www.tidyverse.org/, https://dplyr.tidyverse.org/

# filter(data object, condition) : syntax for filter() command

esales %>%

filter(year == 2019) %>%

filter(value > 9000) %>%

print()

(esales %>%

group_by(year) %>%

summarise(Total = sum(value)) -> total_esales_by_year)

esales %>%

mutate(sales_TWh = value/1000) %>%

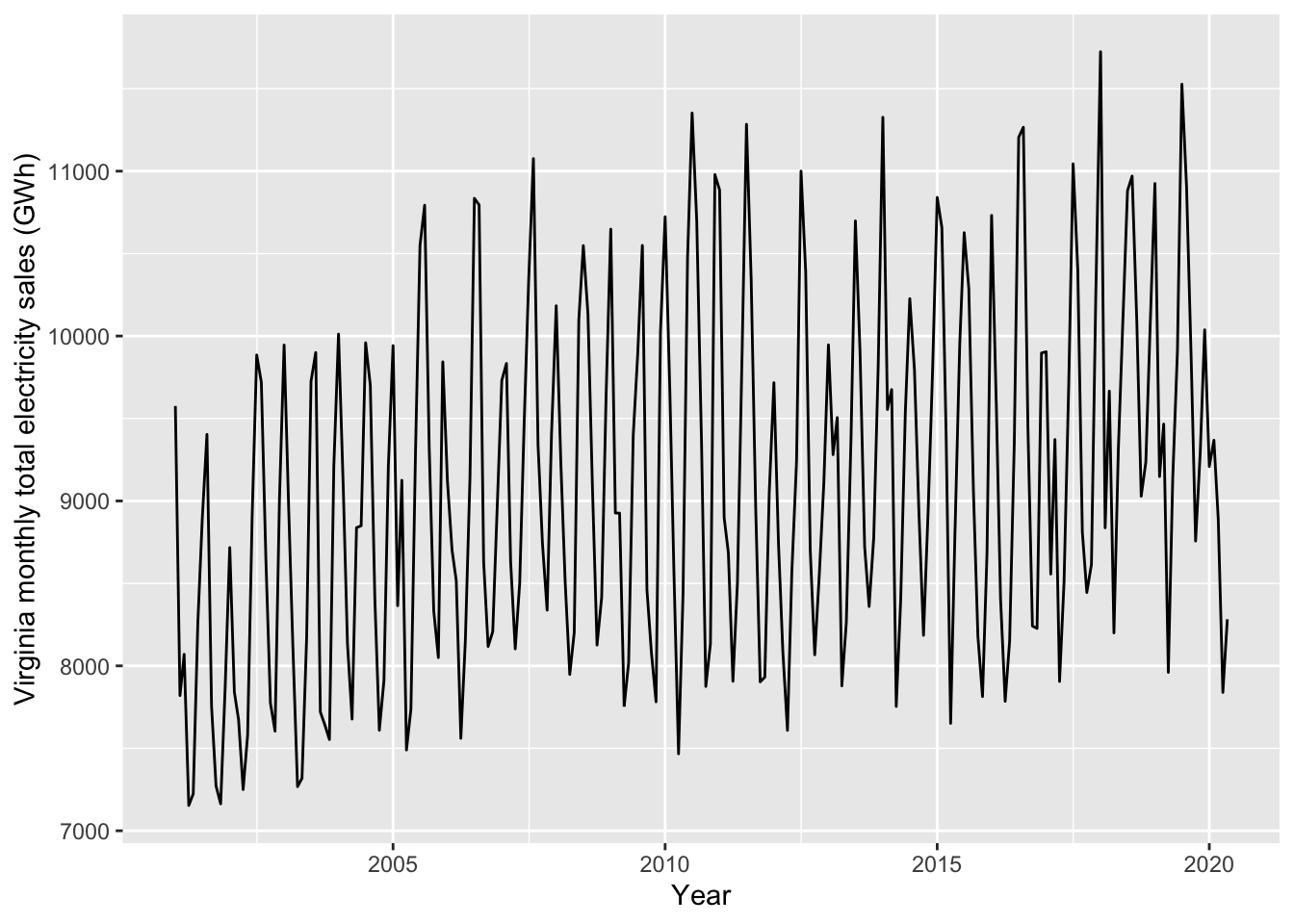

dplyr::select(-value)11.1.3 Plot the time series

#Reference: https://ggplot2.tidyverse.org/

ggplot(data=esales, aes(x=date,y=value)) +

geom_line() + xlab("Year") + ylab("Virginia monthly total electricity sales (GWh)")

# library(lubridate) # Make it easy to deal with dates

esales %>% filter(month==3) # These three lines of code## # A tibble: 20 x 4

## value date year month

## <dbl> <date> <int> <int>

## 1 8889. 2020-03-01 2020 3

## 2 9466. 2019-03-01 2019 3

## 3 9666. 2018-03-01 2018 3

## 4 9372. 2017-03-01 2017 3

## 5 8406. 2016-03-01 2016 3

## 6 9435. 2015-03-01 2015 3

## 7 9676. 2014-03-01 2014 3

## 8 9506. 2013-03-01 2013 3

## 9 8086. 2012-03-01 2012 3

## 10 8688. 2011-03-01 2011 3

## 11 8568. 2010-03-01 2010 3

## 12 8926. 2009-03-01 2009 3

## 13 8512. 2008-03-01 2008 3

## 14 8632. 2007-03-01 2007 3

## 15 8519. 2006-03-01 2006 3

## 16 9125. 2005-03-01 2005 3

## 17 8136. 2004-03-01 2004 3

## 18 8108. 2003-03-01 2003 3

## 19 7675. 2002-03-01 2002 3

## 20 8070. 2001-03-01 2001 3## # A tibble: 20 x 4

## value date year month

## <dbl> <date> <int> <int>

## 1 8889. 2020-03-01 2020 3

## 2 9466. 2019-03-01 2019 3

## 3 9666. 2018-03-01 2018 3

## 4 9372. 2017-03-01 2017 3

## 5 8406. 2016-03-01 2016 3

## 6 9435. 2015-03-01 2015 3

## 7 9676. 2014-03-01 2014 3

## 8 9506. 2013-03-01 2013 3

## 9 8086. 2012-03-01 2012 3

## 10 8688. 2011-03-01 2011 3

## 11 8568. 2010-03-01 2010 3

## 12 8926. 2009-03-01 2009 3

## 13 8512. 2008-03-01 2008 3

## 14 8632. 2007-03-01 2007 3

## 15 8519. 2006-03-01 2006 3

## 16 9125. 2005-03-01 2005 3

## 17 8136. 2004-03-01 2004 3

## 18 8108. 2003-03-01 2003 3

## 19 7675. 2002-03-01 2002 3

## 20 8070. 2001-03-01 2001 3## # A tibble: 20 x 4

## value date year month

## <dbl> <date> <int> <int>

## 1 8889. 2020-03-01 2020 3

## 2 9466. 2019-03-01 2019 3

## 3 9666. 2018-03-01 2018 3

## 4 9372. 2017-03-01 2017 3

## 5 8406. 2016-03-01 2016 3

## 6 9435. 2015-03-01 2015 3

## 7 9676. 2014-03-01 2014 3

## 8 9506. 2013-03-01 2013 3

## 9 8086. 2012-03-01 2012 3

## 10 8688. 2011-03-01 2011 3

## 11 8568. 2010-03-01 2010 3

## 12 8926. 2009-03-01 2009 3

## 13 8512. 2008-03-01 2008 3

## 14 8632. 2007-03-01 2007 3

## 15 8519. 2006-03-01 2006 3

## 16 9125. 2005-03-01 2005 3

## 17 8136. 2004-03-01 2004 3

## 18 8108. 2003-03-01 2003 3

## 19 7675. 2002-03-01 2002 3

## 20 8070. 2001-03-01 2001 3# We don't have to keep the 'year' and 'month' column: can recover them if needed

esales %>%

dplyr::select(date, sales_GWh = value) -> esales_tbl

print(esales_tbl)## # A tibble: 233 x 2

## date sales_GWh

## <date> <dbl>

## 1 2020-05-01 8282.

## 2 2020-04-01 7839.

## 3 2020-03-01 8889.

## 4 2020-02-01 9368.

## 5 2020-01-01 9209.

## 6 2019-12-01 10038.

## 7 2019-11-01 9291.

## 8 2019-10-01 8757.

## 9 2019-09-01 9874.

## 10 2019-08-01 10912.

## # … with 223 more rows11.1.4 Convert the data frame into a time series tsibble object

# install.packages("tsibble")

library(tsibble) # Reference: https://tsibble.tidyverts.org/articles/intro-tsibble.html

esales_tbl %>% as_tsibble(index = date) -> elsales_tbl_ts

print(elsales_tbl_ts)## # A tsibble: 233 x 2 [1D]

## date sales_GWh

## <date> <dbl>

## 1 2001-01-01 9576.

## 2 2001-02-01 7820.

## 3 2001-03-01 8070.

## 4 2001-04-01 7153.

## 5 2001-05-01 7224.

## 6 2001-06-01 8264.

## 7 2001-07-01 8896.

## 8 2001-08-01 9404.

## 9 2001-09-01 7753.

## 10 2001-10-01 7272.

## # … with 223 more rows11.1.5 Make some plots

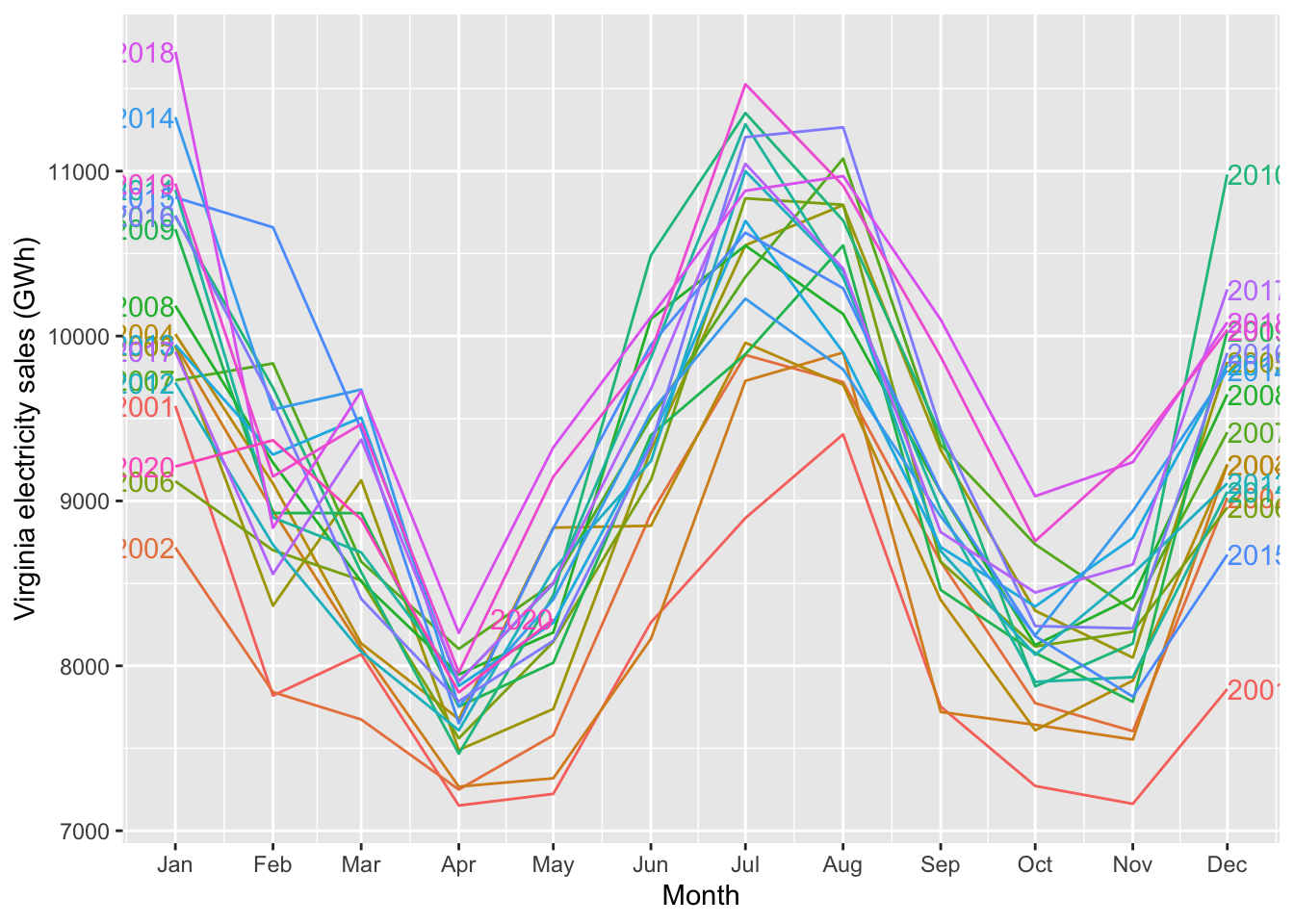

11.1.5.2 Make a seasonal plot

# This plot won't work. Why not?

elsales_tbl_ts %>%

feasts::gg_season(sales_GWh, labels = "both") + ylab("Virginia electricity sales (GWh)")# install.packages("feasts"), Reference: https://feasts.tidyverts.org/

library(feasts)

elsales_tbl_ts %>%

mutate(Month = tsibble::yearmonth(date)) %>%

as_tsibble(index = Month) %>%

dplyr::select(Month,sales_GWh) -> vaelsales_tbl_ts

print(vaelsales_tbl_ts)## # A tsibble: 233 x 2 [1M]

## Month sales_GWh

## <mth> <dbl>

## 1 2001 Jan 9576.

## 2 2001 Feb 7820.

## 3 2001 Mar 8070.

## 4 2001 Apr 7153.

## 5 2001 May 7224.

## 6 2001 Jun 8264.

## 7 2001 Jul 8896.

## 8 2001 Aug 9404.

## 9 2001 Sep 7753.

## 10 2001 Oct 7272.

## # … with 223 more rowsautoplot(vaelsales_tbl_ts, sales_GWh) +

ylab("Virginia monthly total electricity sales (GWh)") +

xlab("") # Leave horiz. axis label blank ### Seasonal plots and seasonal subseries plots

### Seasonal plots and seasonal subseries plots

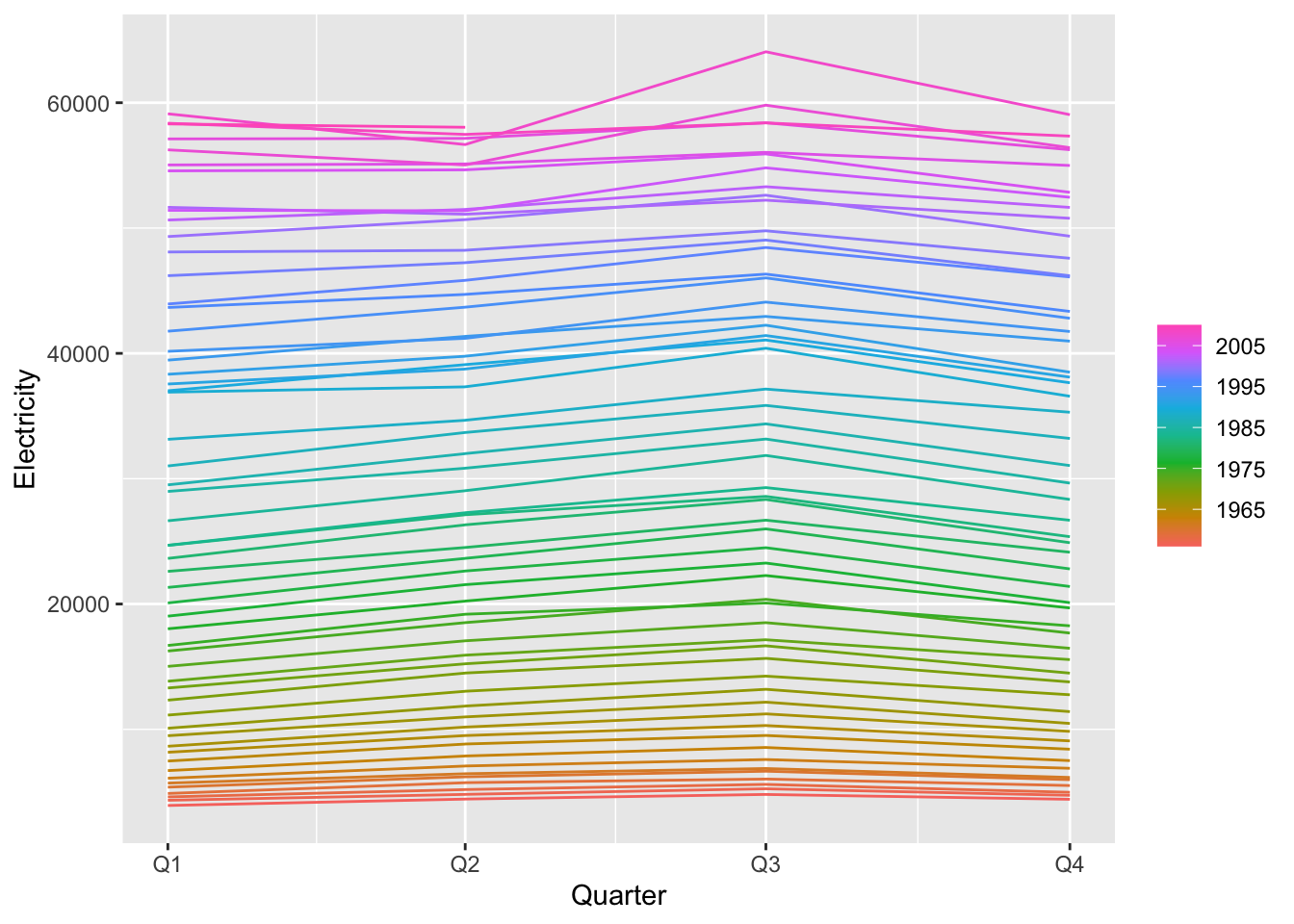

vaelsales_tbl_ts %>% gg_season(sales_GWh, labels = "both") + ylab("Virginia electricity sales (GWh)")

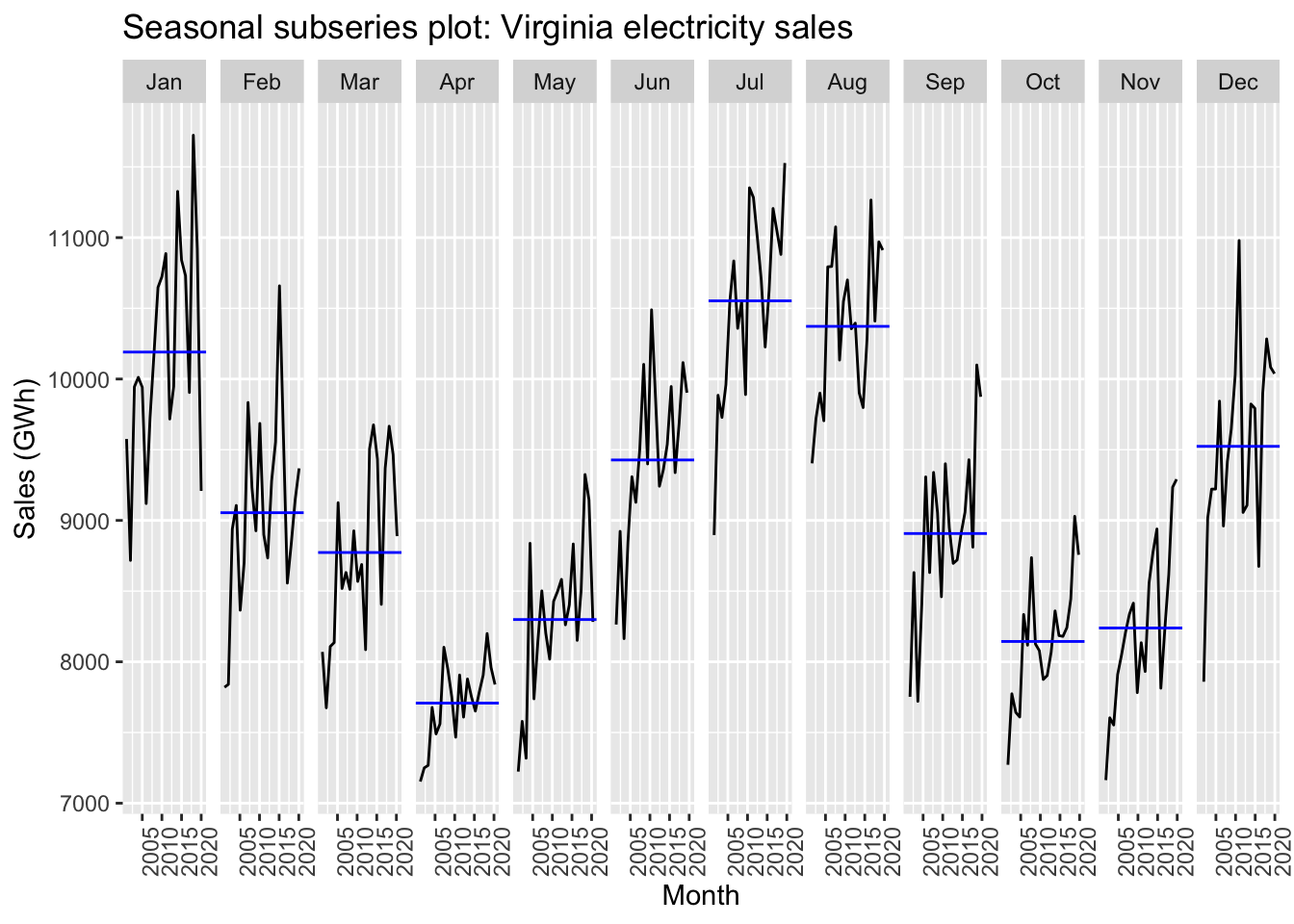

vaelsales_tbl_ts %>%

gg_subseries(sales_GWh) +

labs(

y = "Sales (GWh)",

title = "Seasonal subseries plot: Virginia electricity sales"

)

11.1.6 Scatterplots

Investigating relationships between two variables. Scatterplots. Correlation. Scatterplot matrices.

Readings: FPP Sect. 2.6

## # A tsibble: 52,608 x 5 [30m] <Australia/Melbourne>

## Time Demand Temperature Date Holiday

## <dttm> <dbl> <dbl> <date> <lgl>

## 1 2012-01-01 00:00:00 4383. 21.4 2012-01-01 TRUE

## 2 2012-01-01 00:30:00 4263. 21.0 2012-01-01 TRUE

## 3 2012-01-01 01:00:00 4049. 20.7 2012-01-01 TRUE

## 4 2012-01-01 01:30:00 3878. 20.6 2012-01-01 TRUE

## 5 2012-01-01 02:00:00 4036. 20.4 2012-01-01 TRUE

## 6 2012-01-01 02:30:00 3866. 20.2 2012-01-01 TRUE

## 7 2012-01-01 03:00:00 3694. 20.1 2012-01-01 TRUE

## 8 2012-01-01 03:30:00 3562. 19.6 2012-01-01 TRUE

## 9 2012-01-01 04:00:00 3433. 19.1 2012-01-01 TRUE

## 10 2012-01-01 04:30:00 3359. 19.0 2012-01-01 TRUE

## # … with 52,598 more rows## Time Demand Temperature

## Min. :2012-01-01 00:00:00 Min. :2858 Min. : 1.50

## 1st Qu.:2012-09-30 22:52:30 1st Qu.:3969 1st Qu.:12.30

## Median :2013-07-01 22:45:00 Median :4635 Median :15.40

## Mean :2013-07-01 22:45:00 Mean :4665 Mean :16.27

## 3rd Qu.:2014-04-01 23:37:30 3rd Qu.:5244 3rd Qu.:19.40

## Max. :2014-12-31 23:30:00 Max. :9345 Max. :43.20

## Date Holiday

## Min. :2012-01-01 Mode :logical

## 1st Qu.:2012-09-30 FALSE:51120

## Median :2013-07-01 TRUE :1488

## Mean :2013-07-01

## 3rd Qu.:2014-04-01

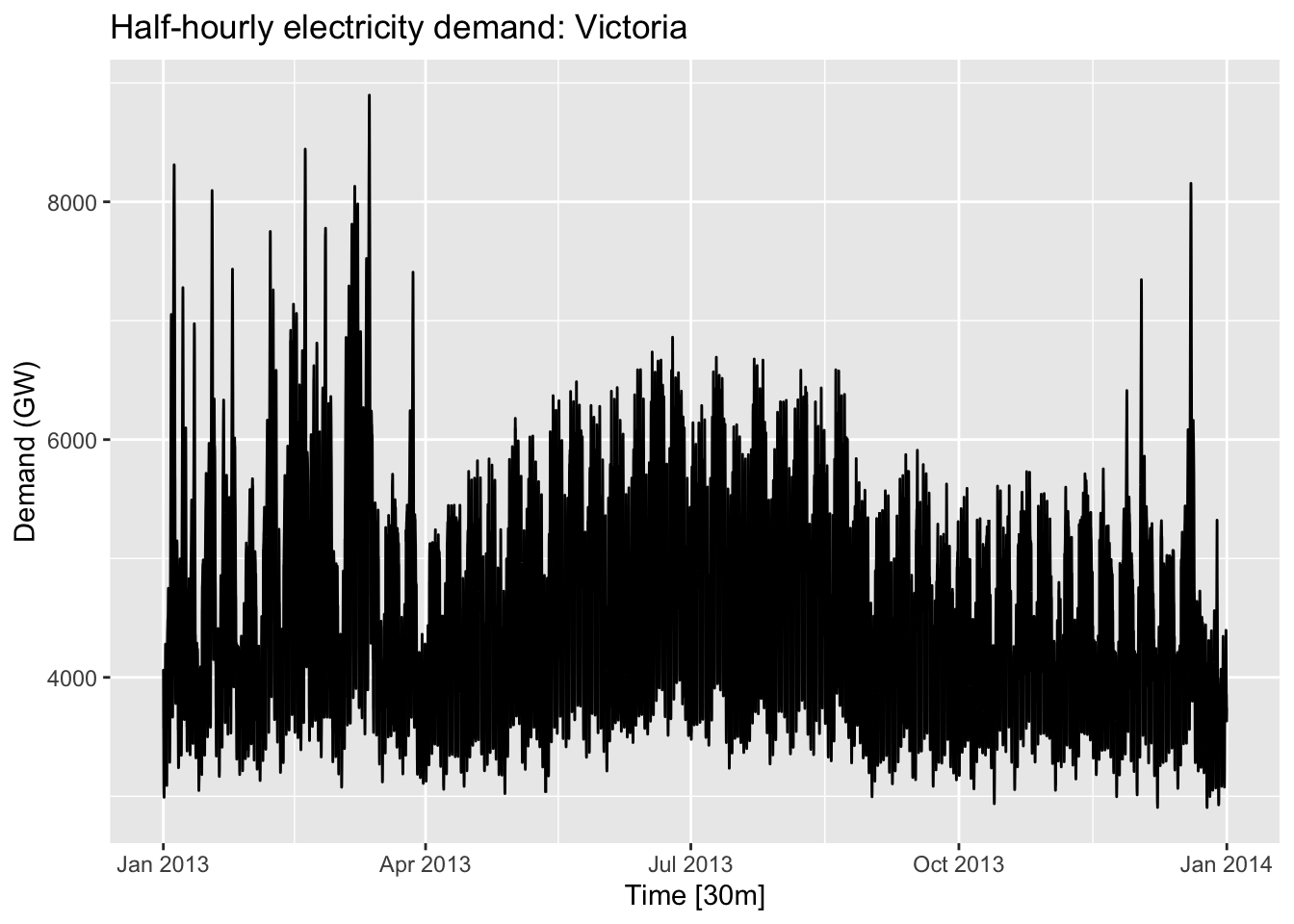

## Max. :2014-12-31vic_elec %>%

filter(year(Time) == 2013) %>%

autoplot(Demand) +

labs(

y = "Demand (GW)",

title = "Half-hourly electricity demand: Victoria"

)

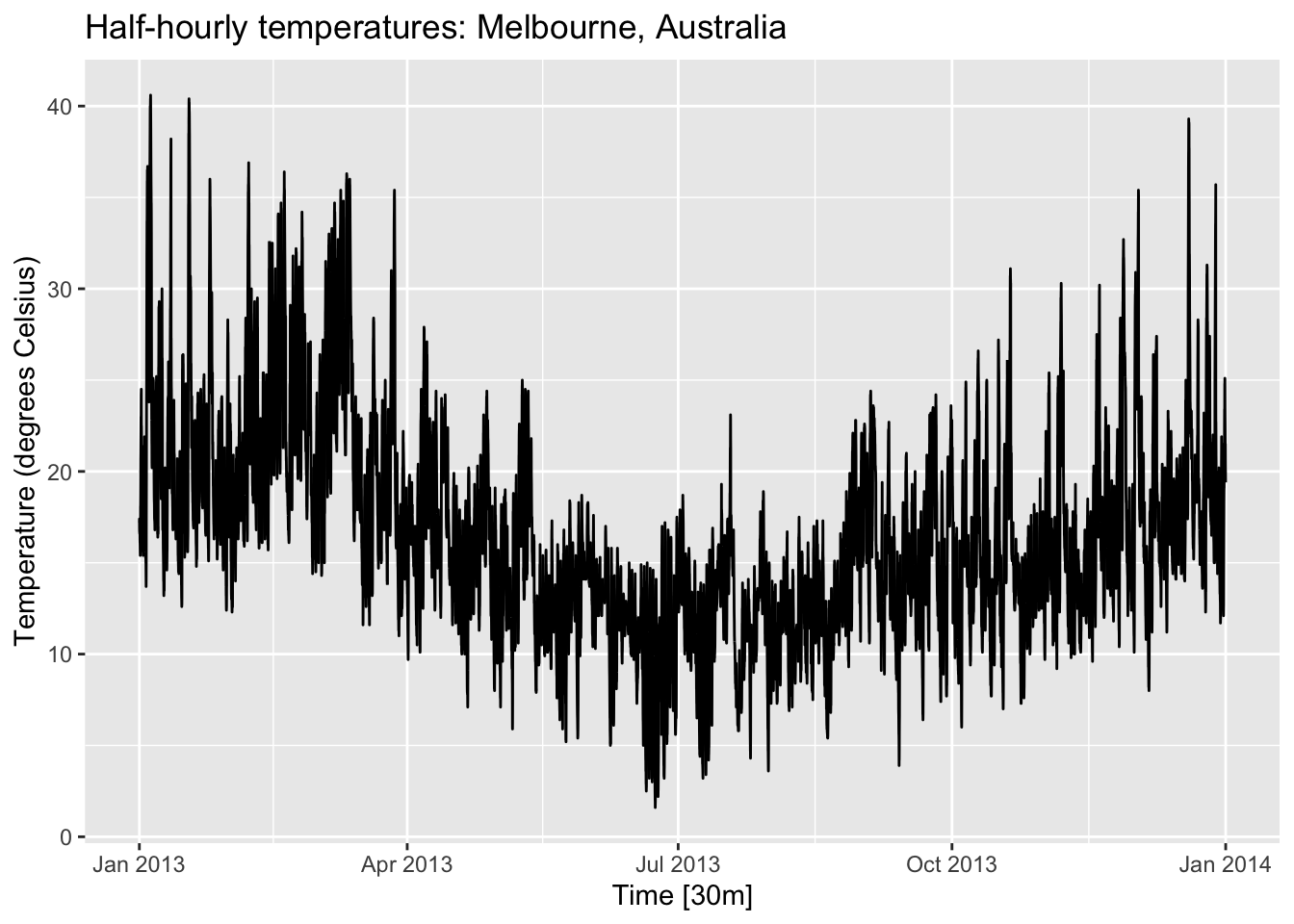

vic_elec %>%

filter(year(Time) == 2013) %>%

autoplot(Temperature) +

labs(

y = "Temperature (degrees Celsius)",

title = "Half-hourly temperatures: Melbourne, Australia"

)

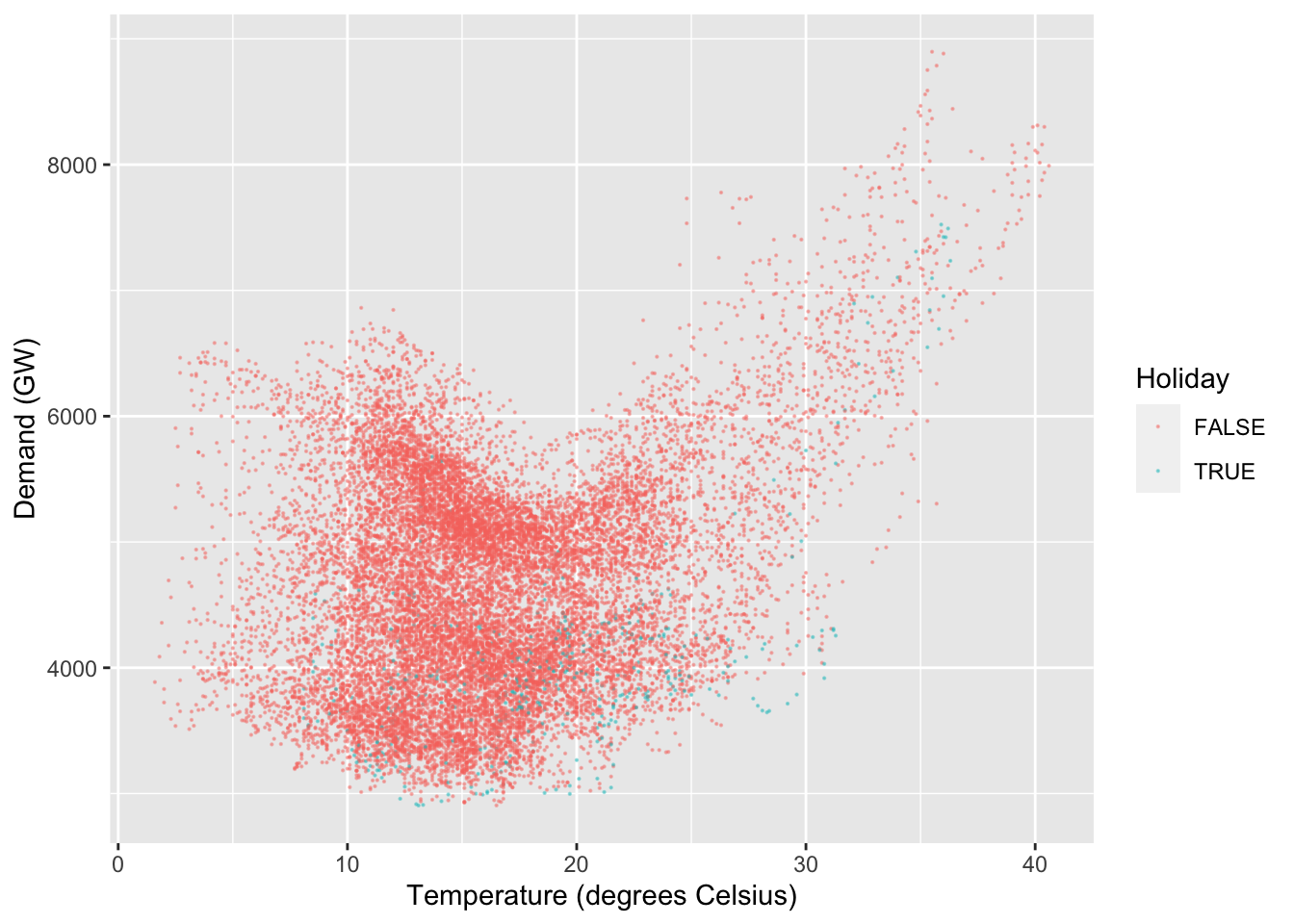

vic_elec %>%

filter(year(Time) == 2013) %>%

ggplot(aes(x = Temperature, y = Demand)) +

# geom_density2d() +

geom_point(size=0.1, aes(colour=Holiday), alpha = 0.4) +

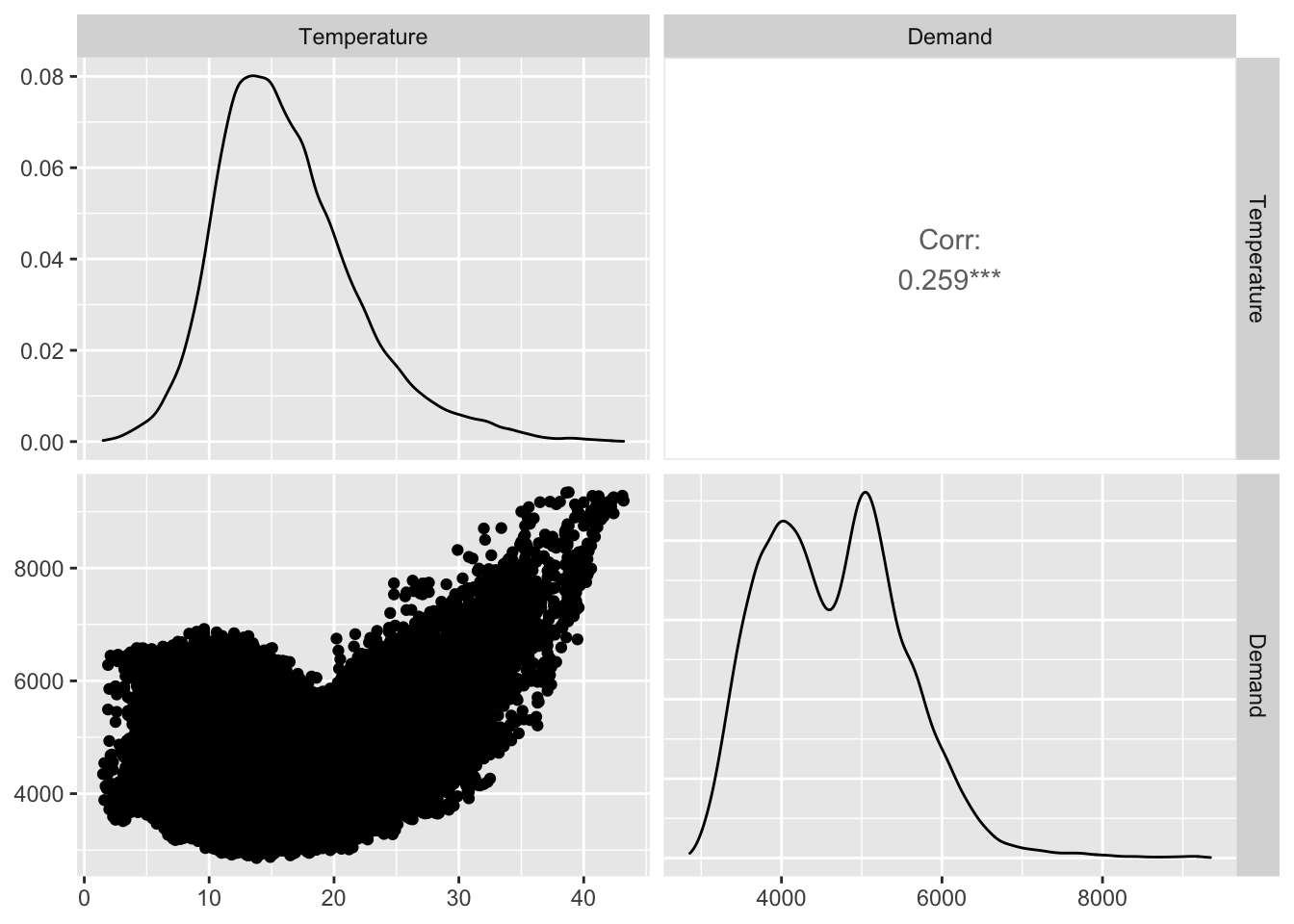

labs(y = "Demand (GW)", x = "Temperature (degrees Celsius)") A Scatterplot matrix

A Scatterplot matrix

## # A tsibble: 52,608 x 5 [30m] <Australia/Melbourne>

## Time Demand Temperature Date Holiday

## <dttm> <dbl> <dbl> <date> <lgl>

## 1 2012-01-01 00:00:00 4383. 21.4 2012-01-01 TRUE

## 2 2012-01-01 00:30:00 4263. 21.0 2012-01-01 TRUE

## 3 2012-01-01 01:00:00 4049. 20.7 2012-01-01 TRUE

## 4 2012-01-01 01:30:00 3878. 20.6 2012-01-01 TRUE

## 5 2012-01-01 02:00:00 4036. 20.4 2012-01-01 TRUE

## 6 2012-01-01 02:30:00 3866. 20.2 2012-01-01 TRUE

## 7 2012-01-01 03:00:00 3694. 20.1 2012-01-01 TRUE

## 8 2012-01-01 03:30:00 3562. 19.6 2012-01-01 TRUE

## 9 2012-01-01 04:00:00 3433. 19.1 2012-01-01 TRUE

## 10 2012-01-01 04:30:00 3359. 19.0 2012-01-01 TRUE

## # … with 52,598 more rows

# install.packages("GGally")

vic_elec %>%

# mutate(Temperature = round(Temperature)) %>%

# pivot_wider(values_from=c(Demand,Temperature), names_from=Holiday) %>%

GGally::ggpairs(columns = 3:2)

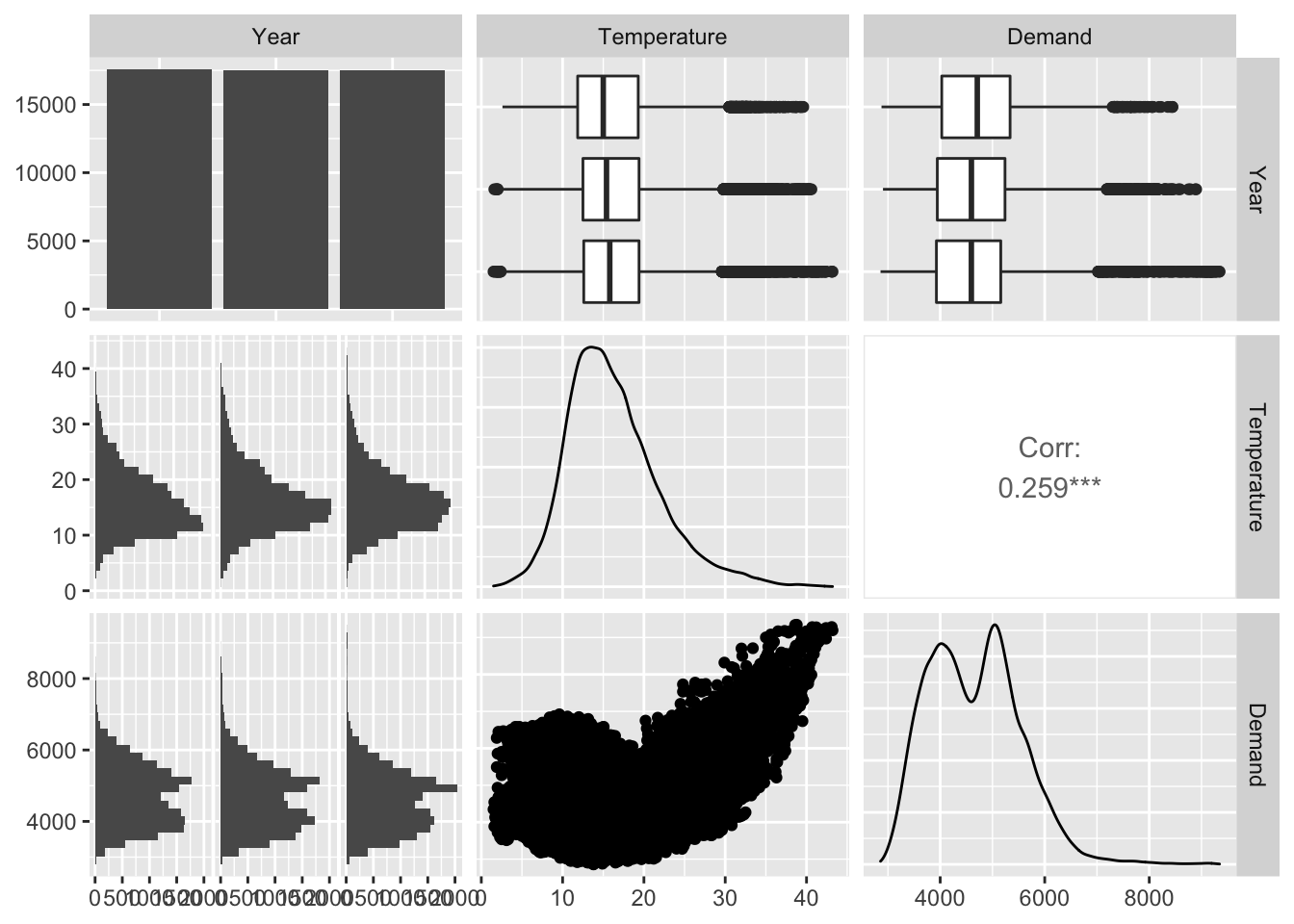

vic_elec %>%

mutate(Year = factor(year(Date))) %>%

dplyr::select(-c(Date, Holiday)) %>%

GGally::ggpairs(columns = 4:2)

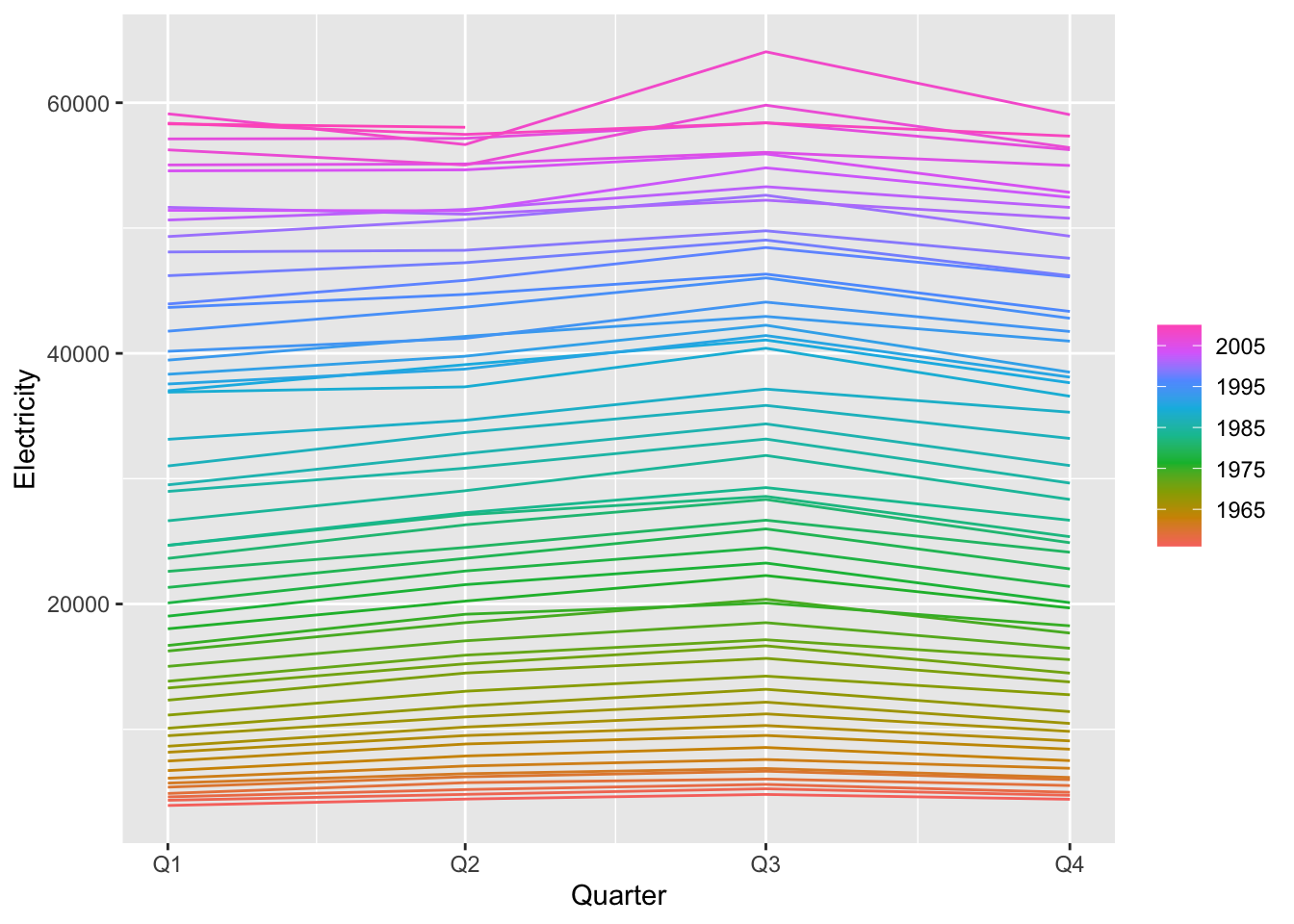

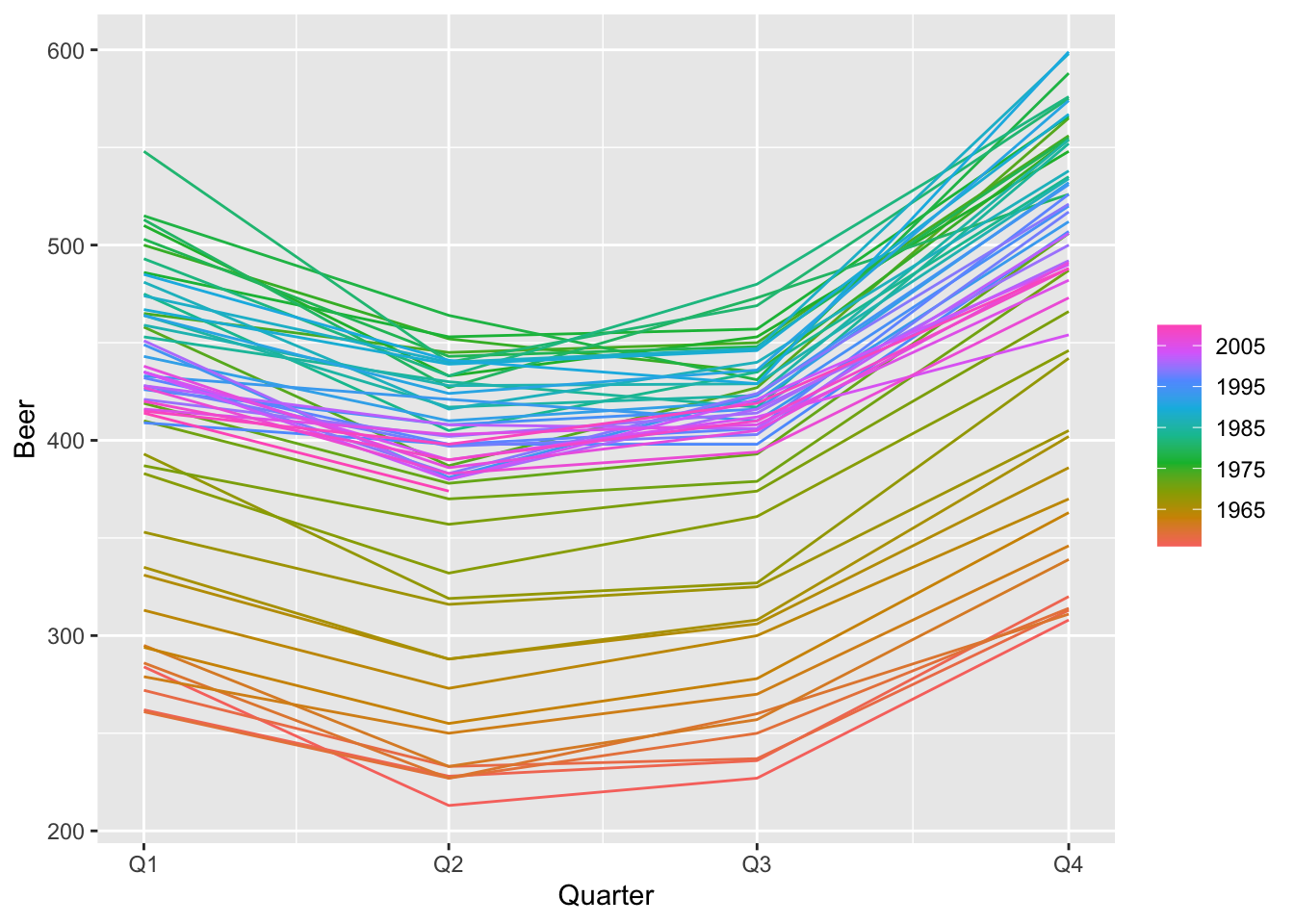

11.2 Example: Australian production

## # A tsibble: 218 x 7 [1Q]

## Quarter Beer Tobacco Bricks Cement Electricity Gas

## <qtr> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

## 1 1956 Q1 284 5225 189 465 3923 5

## 2 1956 Q2 213 5178 204 532 4436 6

## 3 1956 Q3 227 5297 208 561 4806 7

## 4 1956 Q4 308 5681 197 570 4418 6

## 5 1957 Q1 262 5577 187 529 4339 5

## 6 1957 Q2 228 5651 214 604 4811 7

## 7 1957 Q3 236 5317 227 603 5259 7

## 8 1957 Q4 320 6152 222 582 4735 6

## 9 1958 Q1 272 5758 199 554 4608 5

## 10 1958 Q2 233 5641 229 620 5196 7

## # … with 208 more rows

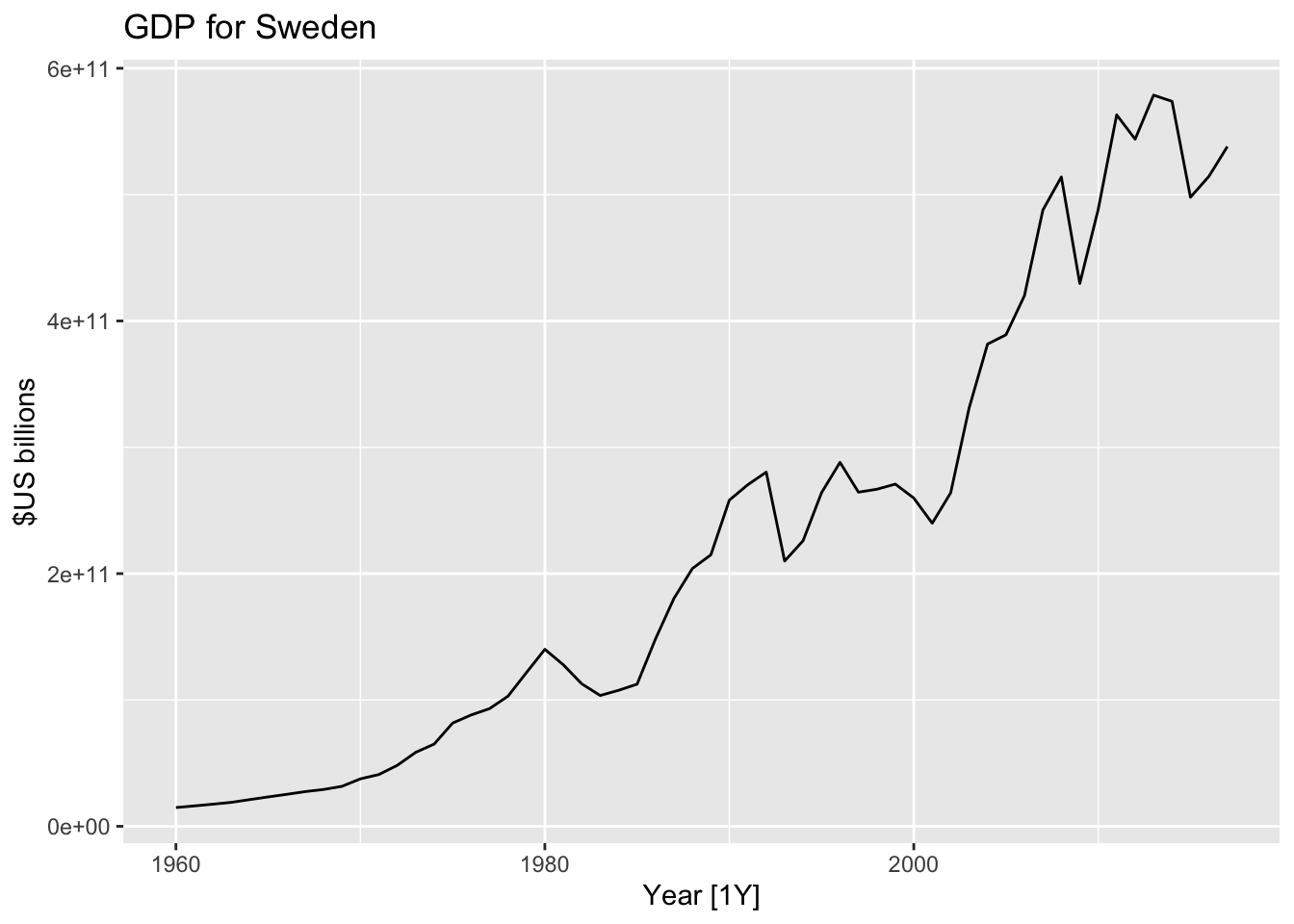

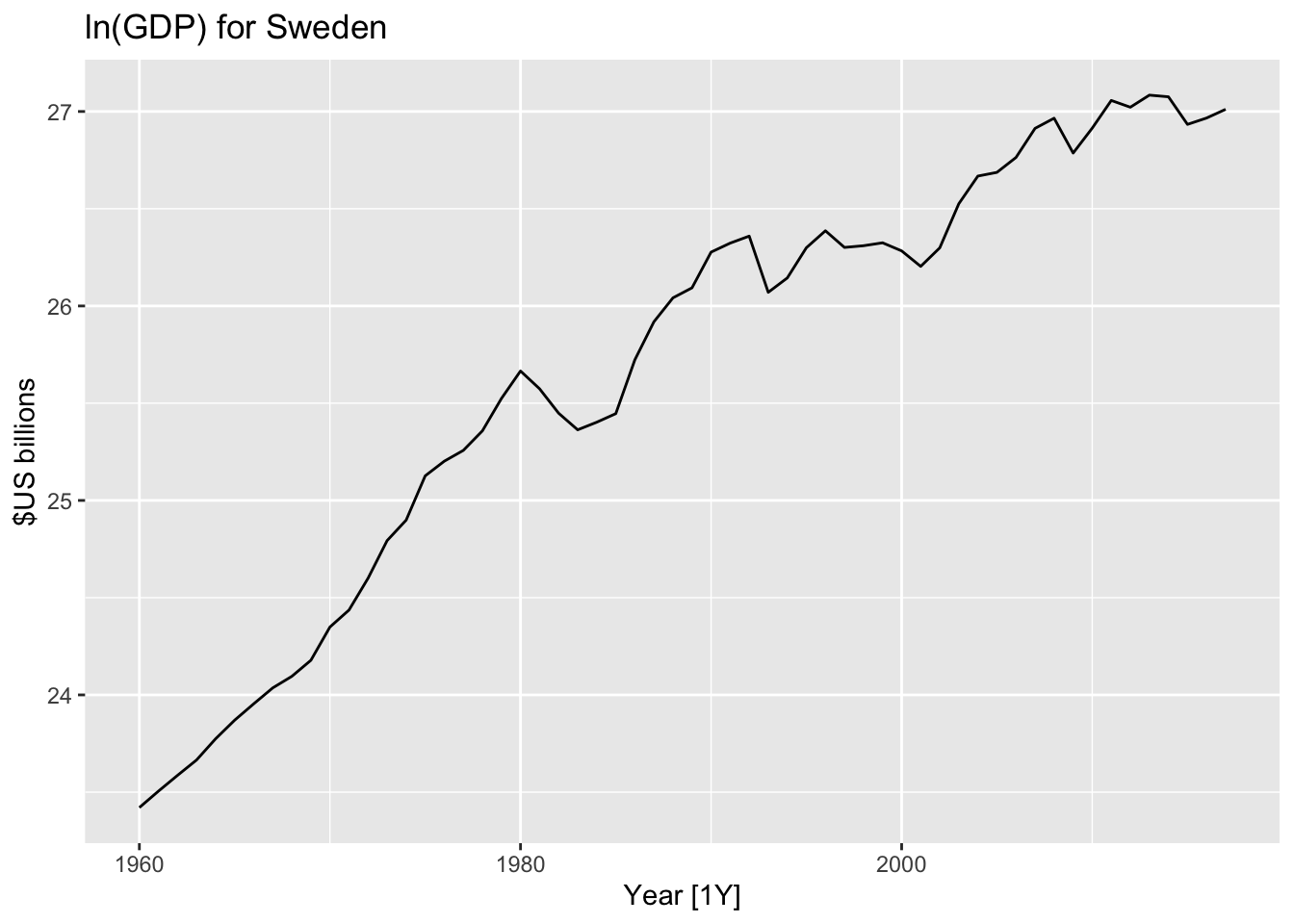

11.3 Example: Gross Domestic Product data

11.3.1 Exploratory data analysis

## # A tsibble: 15,150 x 9 [1Y]

## # Key: Country [263]

## Country Code Year GDP Growth CPI Imports Exports Population

## <fct> <fct> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

## 1 Afghanistan AFG 1960 537777811. NA NA 7.02 4.13 8996351

## 2 Afghanistan AFG 1961 548888896. NA NA 8.10 4.45 9166764

## 3 Afghanistan AFG 1962 546666678. NA NA 9.35 4.88 9345868

## 4 Afghanistan AFG 1963 751111191. NA NA 16.9 9.17 9533954

## 5 Afghanistan AFG 1964 800000044. NA NA 18.1 8.89 9731361

## 6 Afghanistan AFG 1965 1006666638. NA NA 21.4 11.3 9938414

## 7 Afghanistan AFG 1966 1399999967. NA NA 18.6 8.57 10152331

## 8 Afghanistan AFG 1967 1673333418. NA NA 14.2 6.77 10372630

## 9 Afghanistan AFG 1968 1373333367. NA NA 15.2 8.90 10604346

## 10 Afghanistan AFG 1969 1408888922. NA NA 15.0 10.1 10854428

## # … with 15,140 more rows## # A tsibble: 58 x 9 [1Y]

## # Key: Country [1]

## Country Code Year GDP Growth CPI Imports Exports Population

## <fct> <fct> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

## 1 Sweden SWE 1960 14842870293. NA 9.21 23.4 23.0 7484656

## 2 Sweden SWE 1961 16147160123. 5.68 9.41 21.7 22.3 7519998

## 3 Sweden SWE 1962 17511477311. 4.26 9.86 21.4 21.9 7561588

## 4 Sweden SWE 1963 18954132366. 5.33 10.1 21.5 21.9 7604328

## 5 Sweden SWE 1964 21137242561. 6.82 10.5 21.9 22.3 7661354

## 6 Sweden SWE 1965 23260320646. 3.82 11.0 22.5 21.9 7733853

## 7 Sweden SWE 1966 25302033132. 2.09 11.7 21.9 21.4 7807797

## 8 Sweden SWE 1967 27463409202. 3.37 12.2 21.0 21.1 7867931

## 9 Sweden SWE 1968 29143383491. 3.64 12.5 21.6 21.6 7912273

## 10 Sweden SWE 1969 31649203886. 5.01 12.8 23.0 22.8 7968072

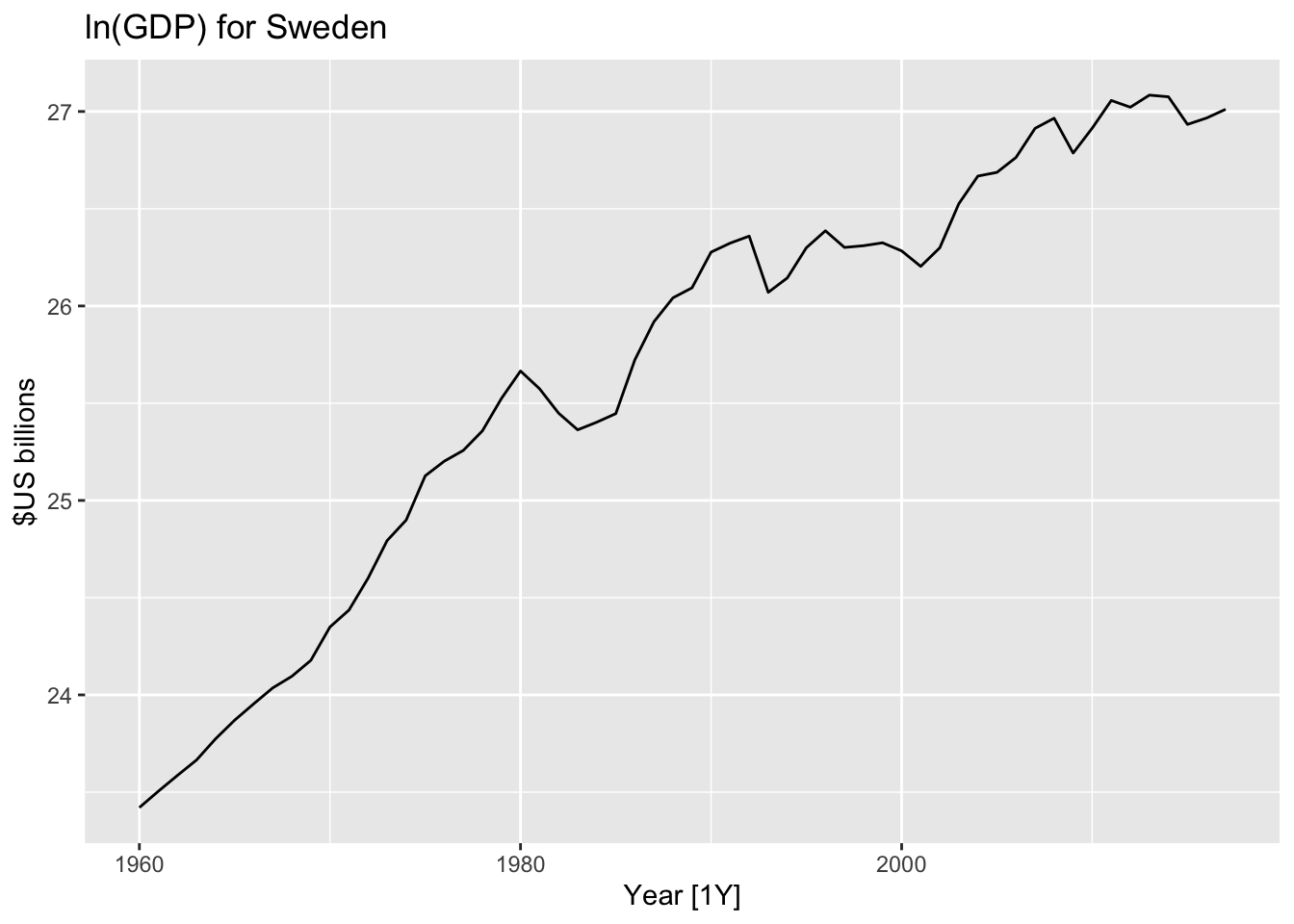

## # … with 48 more rowsglobal_economy %>%

filter(Country=="Sweden") %>%

autoplot(GDP) +

ggtitle("GDP for Sweden") + ylab("$US billions")

11.3.2 Fitting data to simple models

## # A mable: 263 x 2

## # Key: Country [263]

## Country trend_model

## <fct> <model>

## 1 Afghanistan <TSLM>

## 2 Albania <TSLM>

## 3 Algeria <TSLM>

## 4 American Samoa <TSLM>

## 5 Andorra <TSLM>

## 6 Angola <TSLM>

## 7 Antigua and Barbuda <TSLM>

## 8 Arab World <TSLM>

## 9 Argentina <TSLM>

## 10 Armenia <TSLM>

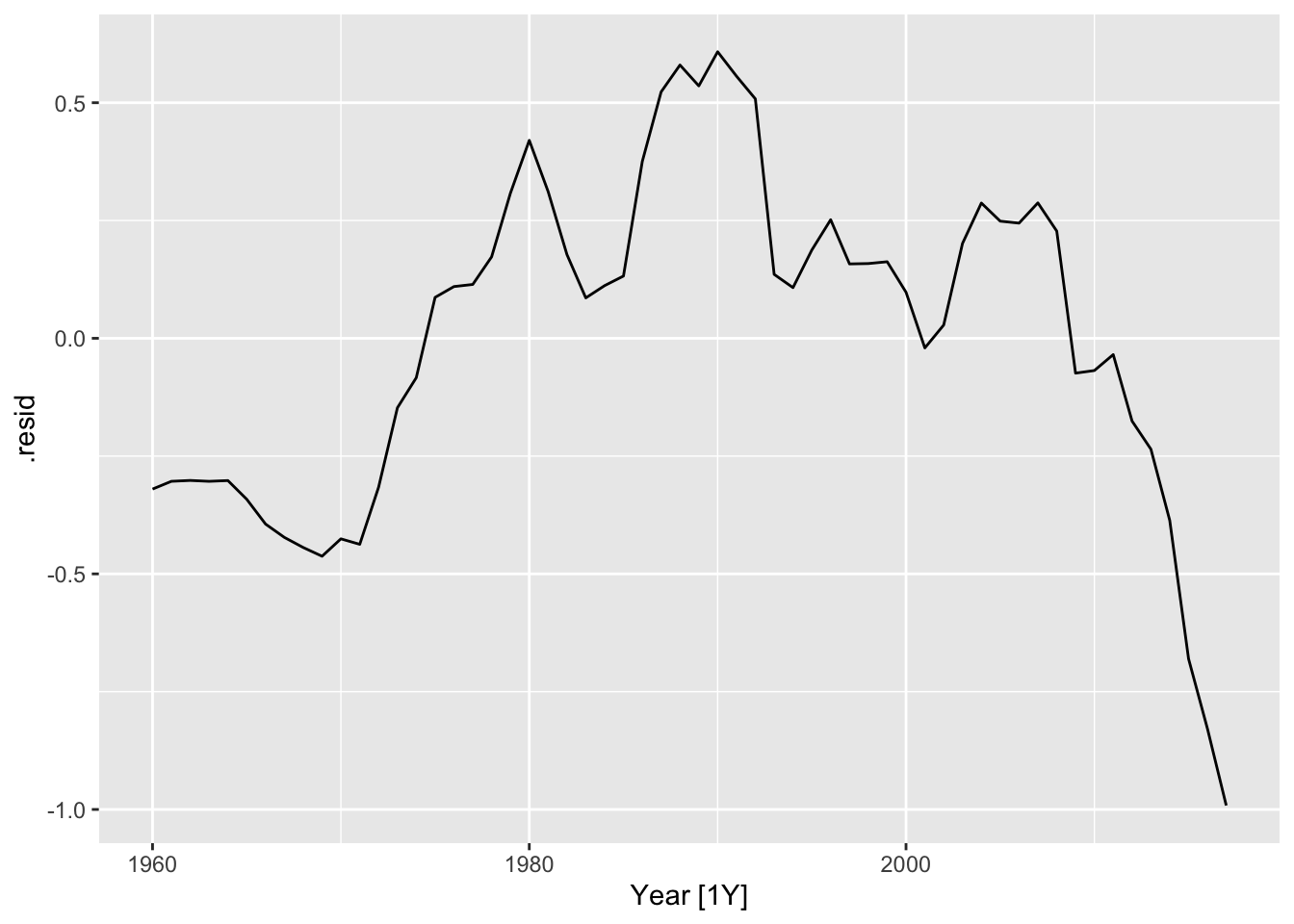

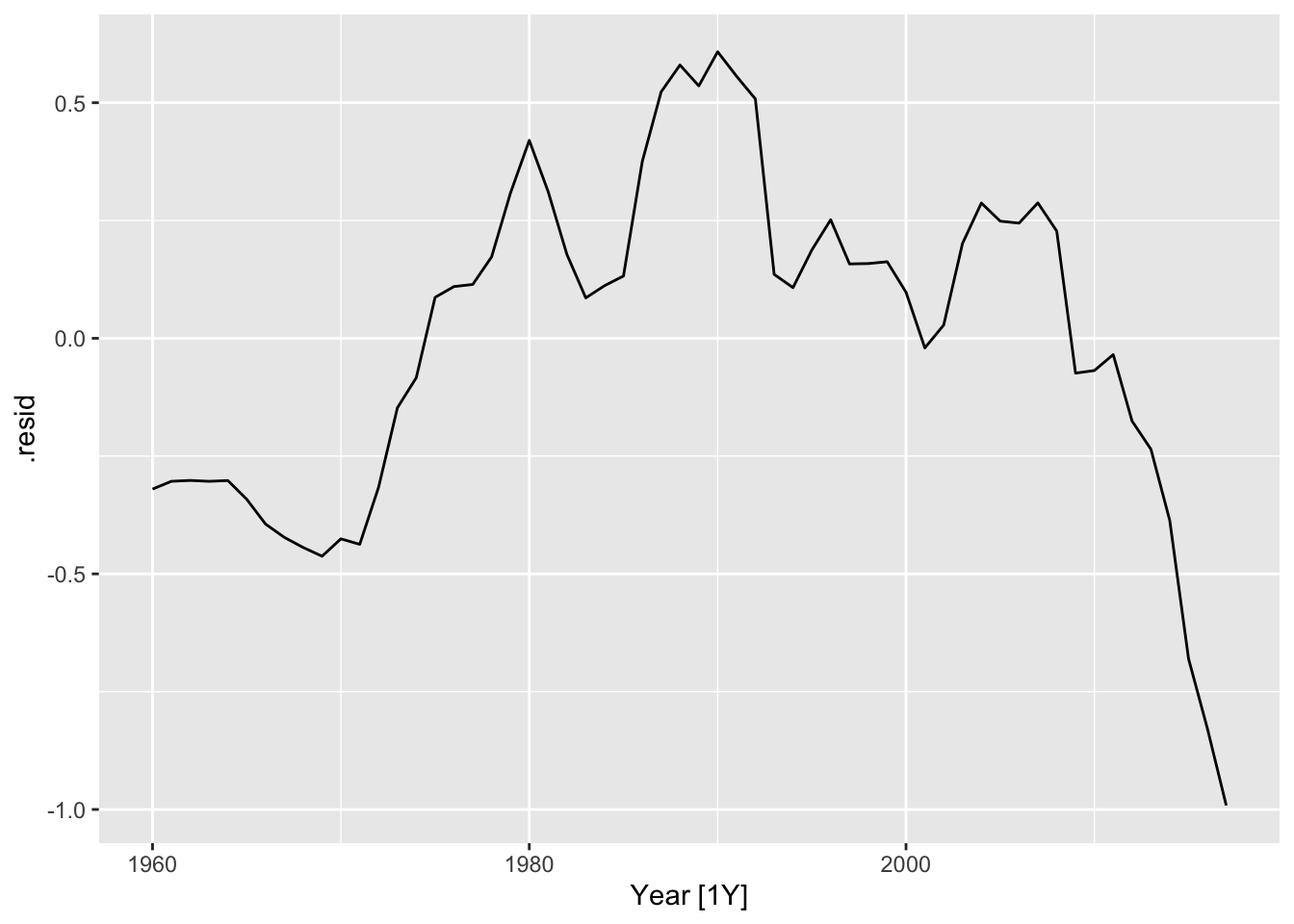

## # … with 253 more rows## # A tsibble: 58 x 4 [1Y]

## # Key: Country, .model [1]

## Country .model Year .resid

## <fct> <chr> <dbl> <dbl>

## 1 Sweden trend_model 1960 79973991821.

## 2 Sweden trend_model 1961 71110300270.

## 3 Sweden trend_model 1962 62306636078.

## 4 Sweden trend_model 1963 53581309752.

## 5 Sweden trend_model 1964 45596438566.

## 6 Sweden trend_model 1965 37551535271.

## 7 Sweden trend_model 1966 29425266377.

## 8 Sweden trend_model 1967 21418661066.

## 9 Sweden trend_model 1968 12930653974.

## 10 Sweden trend_model 1969 5268492989.

## # … with 48 more rows

11.4 Producing forecasts

## # A fable: 789 x 5 [1Y]

## # Key: Country, .model [263]

## Country .model Year GDP .mean

## <fct> <chr> <dbl> <dist> <dbl>

## 1 Afghanistan trend_model 2018 N(1.6e+10, 1.3e+19) 16205101654.

## 2 Afghanistan trend_model 2019 N(1.7e+10, 1.3e+19) 16511878141.

## 3 Afghanistan trend_model 2020 N(1.7e+10, 1.3e+19) 16818654627.

## 4 Albania trend_model 2018 N(1.4e+10, 3.9e+18) 13733734164.

## 5 Albania trend_model 2019 N(1.4e+10, 3.9e+18) 14166852711.

## 6 Albania trend_model 2020 N(1.5e+10, 3.9e+18) 14599971258.

## 7 Algeria trend_model 2018 N(1.6e+11, 9.4e+20) 157895153441.

## 8 Algeria trend_model 2019 N(1.6e+11, 9.4e+20) 161100952126.

## 9 Algeria trend_model 2020 N(1.6e+11, 9.4e+20) 164306750811.

## 10 American Samoa trend_model 2018 N(6.8e+08, 1.7e+15) 682475000

## # … with 779 more rows## fable [1 × 5] (S3: fbl_ts/tbl_ts/tbl_df/tbl/data.frame)

## $ Country: Factor w/ 263 levels "Afghanistan",..: 232

## $ .model : chr "trend_model"

## $ Year : num 2020

## $ GDP : dist [1:1]

## ..$ 3:List of 2

## .. ..$ mu : num 5.45e+11

## .. ..$ sigma: num 5.34e+10

## .. ..- attr(*, "class")= chr [1:2] "dist_normal" "dist_default"

## ..@ vars: chr "GDP"

## $ .mean : num 5.45e+11

## - attr(*, "key")= tibble [1 × 3] (S3: tbl_df/tbl/data.frame)

## ..$ Country: Factor w/ 263 levels "Afghanistan",..: 232

## ..$ .model : chr "trend_model"

## ..$ .rows : list<int> [1:1]

## .. ..$ : int 1

## .. ..@ ptype: int(0)

## ..- attr(*, ".drop")= logi TRUE

## - attr(*, "index")= chr "Year"

## ..- attr(*, "ordered")= logi TRUE

## - attr(*, "index2")= chr "Year"

## - attr(*, "interval")= interval [1:1] 1Y

## ..@ .regular: logi TRUE

## - attr(*, "response")= chr "GDP"

## - attr(*, "dist")= chr "GDP"

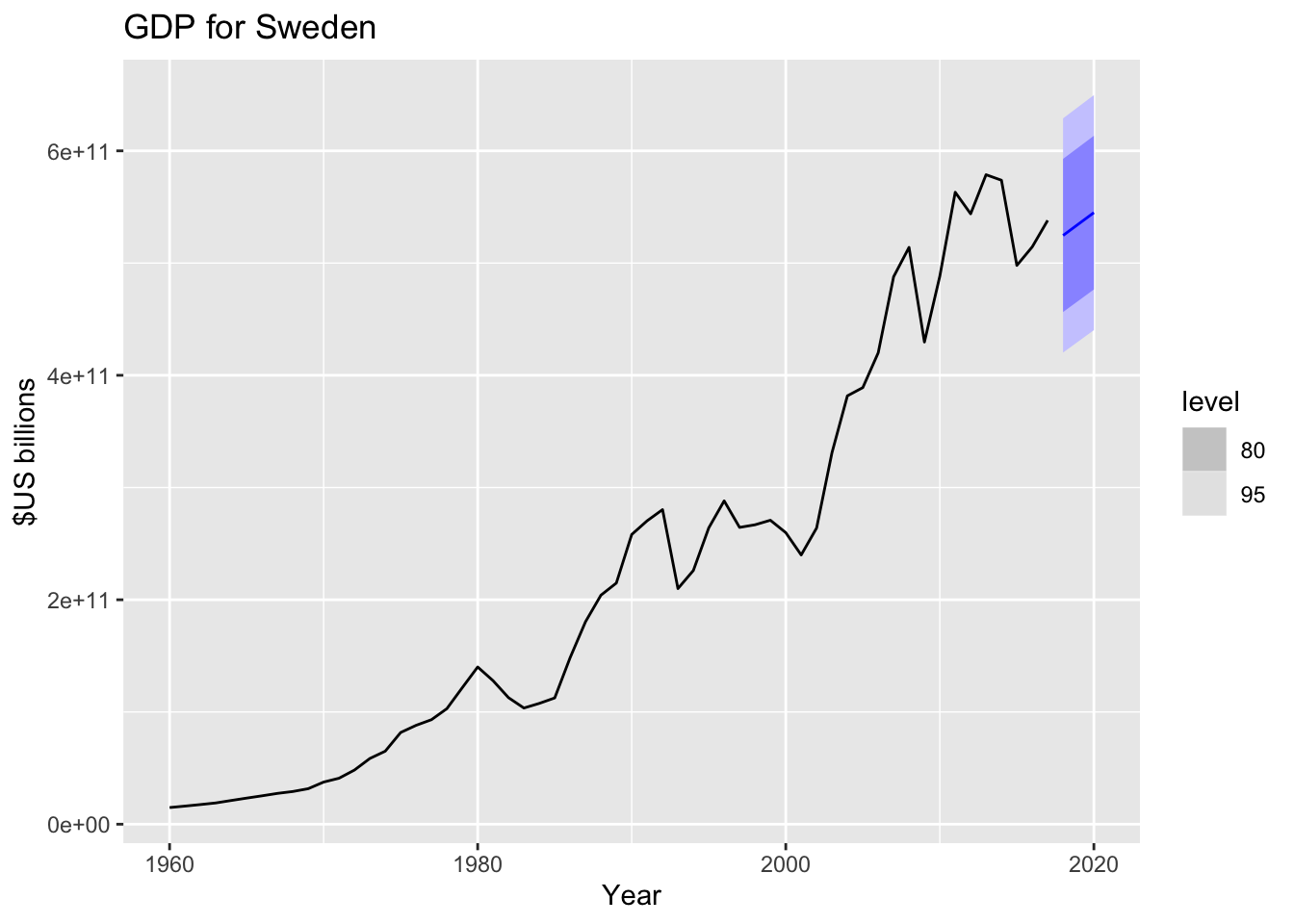

## - attr(*, "model_cn")= chr ".model"fcast3yrs %>%

filter(Country=="Sweden") %>%

autoplot(global_economy) +

ggtitle("GDP for Sweden") + ylab("$US billions")

11.4.1 Model residuals vs. forecast errors

Model residuals:

Your data: \(y_1, y_2, \ldots, y_T\)

Fitted values: \(\hat{y}_1, \hat{y}_2, \ldots, \hat{y}_T\)

Model residuals: \(e_t = y_t - \hat{y}_t\)

Forecast errors:

## # A tsibble: 15,150 x 7 [1Y]

## # Key: Country, .model [263]

## Country .model Year GDP .fitted .resid .innov

## <fct> <chr> <dbl> <dbl> <dbl> <dbl> <dbl>

## 1 Afghanistan trend_model 1960 537777811. -1587934559. 2125712370. 2.13e9

## 2 Afghanistan trend_model 1961 548888896. -1281158073. 1830046968. 1.83e9

## 3 Afghanistan trend_model 1962 546666678. -974381586. 1521048264. 1.52e9

## 4 Afghanistan trend_model 1963 751111191. -667605100. 1418716291. 1.42e9

## 5 Afghanistan trend_model 1964 800000044. -360828613. 1160828658. 1.16e9

## 6 Afghanistan trend_model 1965 1006666638. -54052127. 1060718765. 1.06e9

## 7 Afghanistan trend_model 1966 1399999967. 252724359. 1147275607. 1.15e9

## 8 Afghanistan trend_model 1967 1673333418. 559500846. 1113832572. 1.11e9

## 9 Afghanistan trend_model 1968 1373333367. 866277332. 507056034. 5.07e8

## 10 Afghanistan trend_model 1969 1408888922. 1173053819. 235835103. 2.36e8

## # … with 15,140 more rowsaugment(fit) %>% filter(Country == "Sweden") %>%

ggplot(aes(x = .resid)) +

geom_histogram(bins = 20) +

ggtitle("Histogram of residuals")

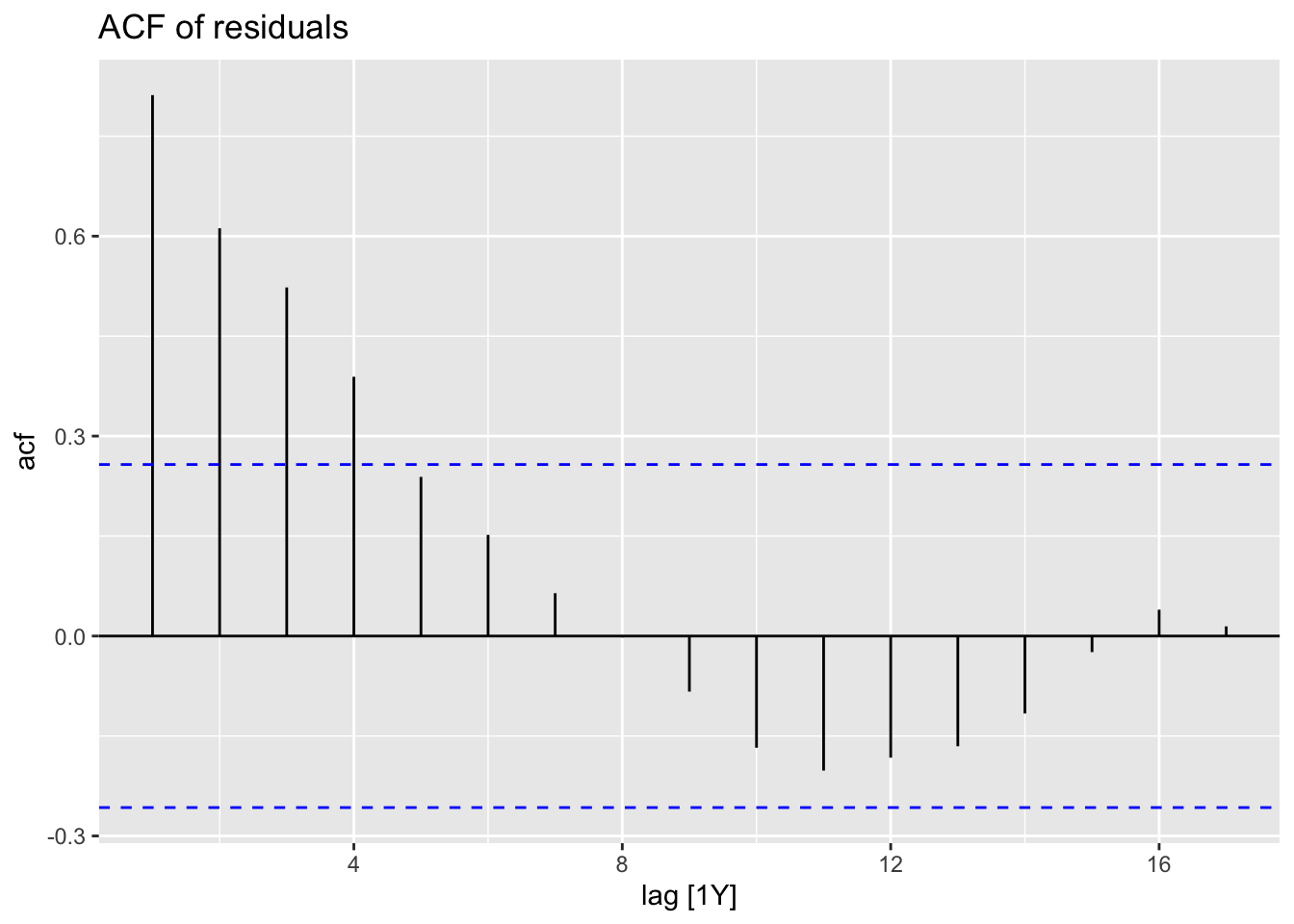

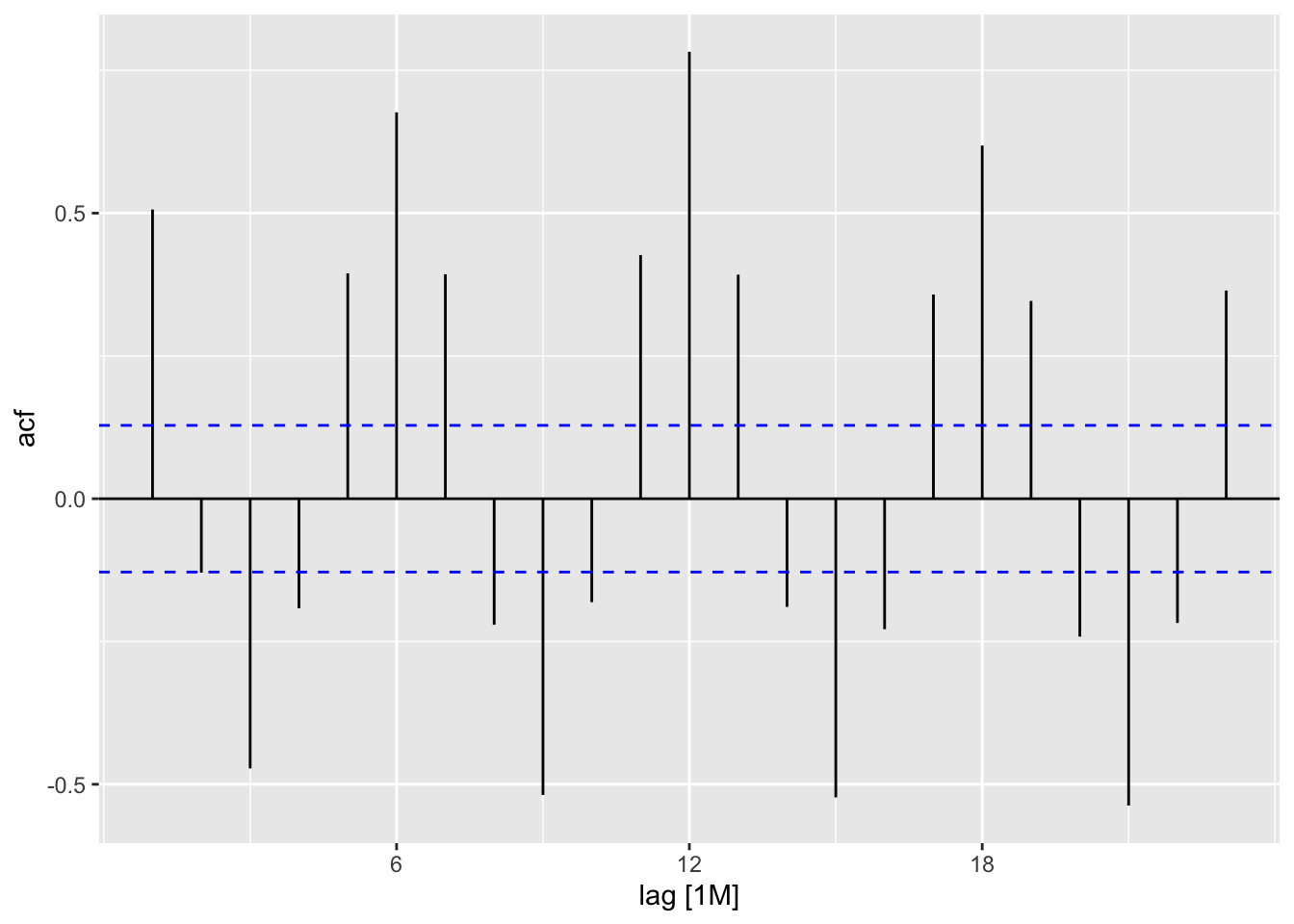

11.4.2 Are the model residuals auto-correlated?

augment(fit) %>% filter(Country == "Sweden") -> augSweden

augSweden %>%

ACF(.resid) %>%

autoplot() + ggtitle("ACF of residuals")

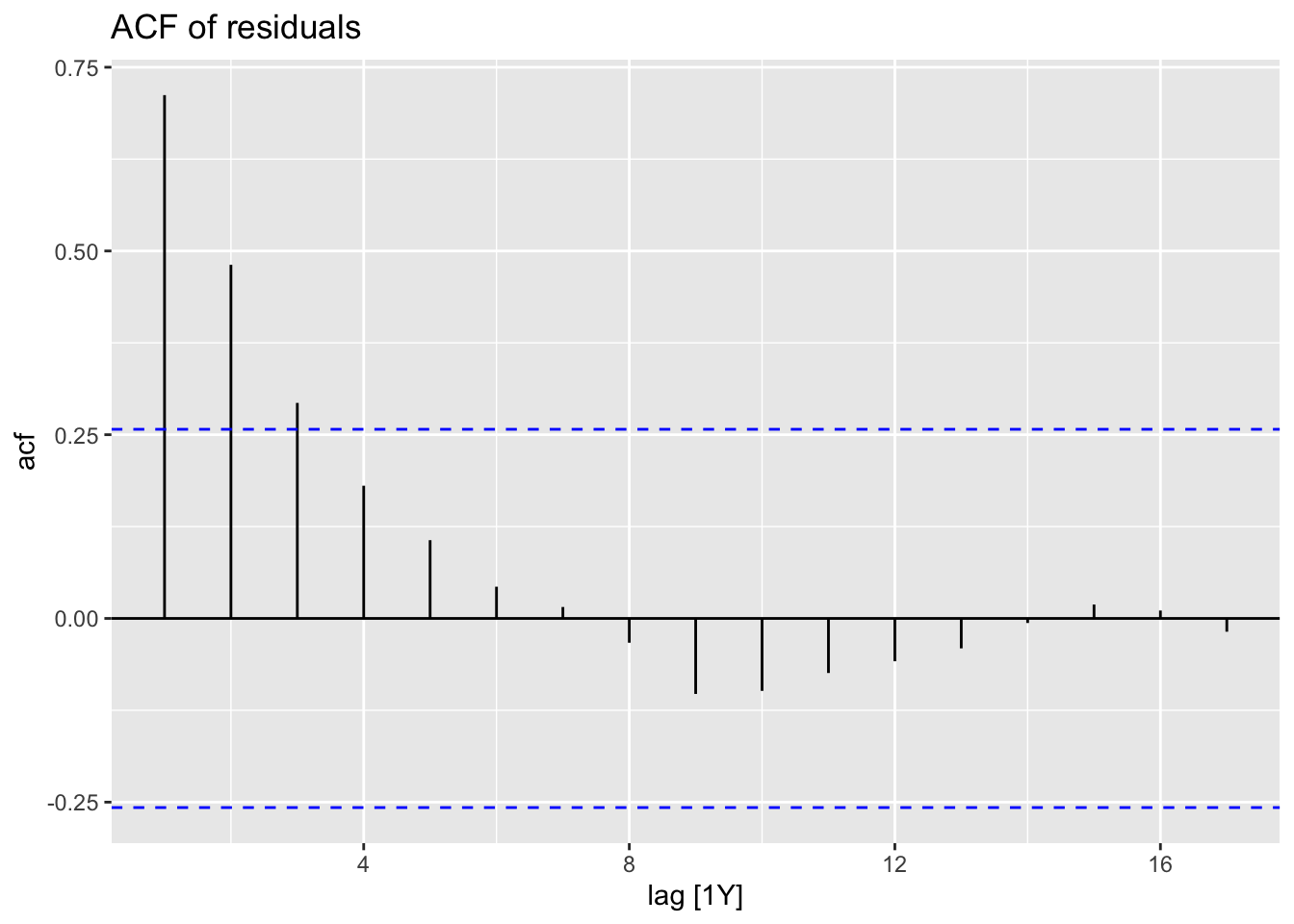

augment(fit3) %>% filter(Country == "Sweden") -> augSweden3

augSweden3 %>%

ACF(.resid) %>%

autoplot() + ggtitle("ACF of residuals")

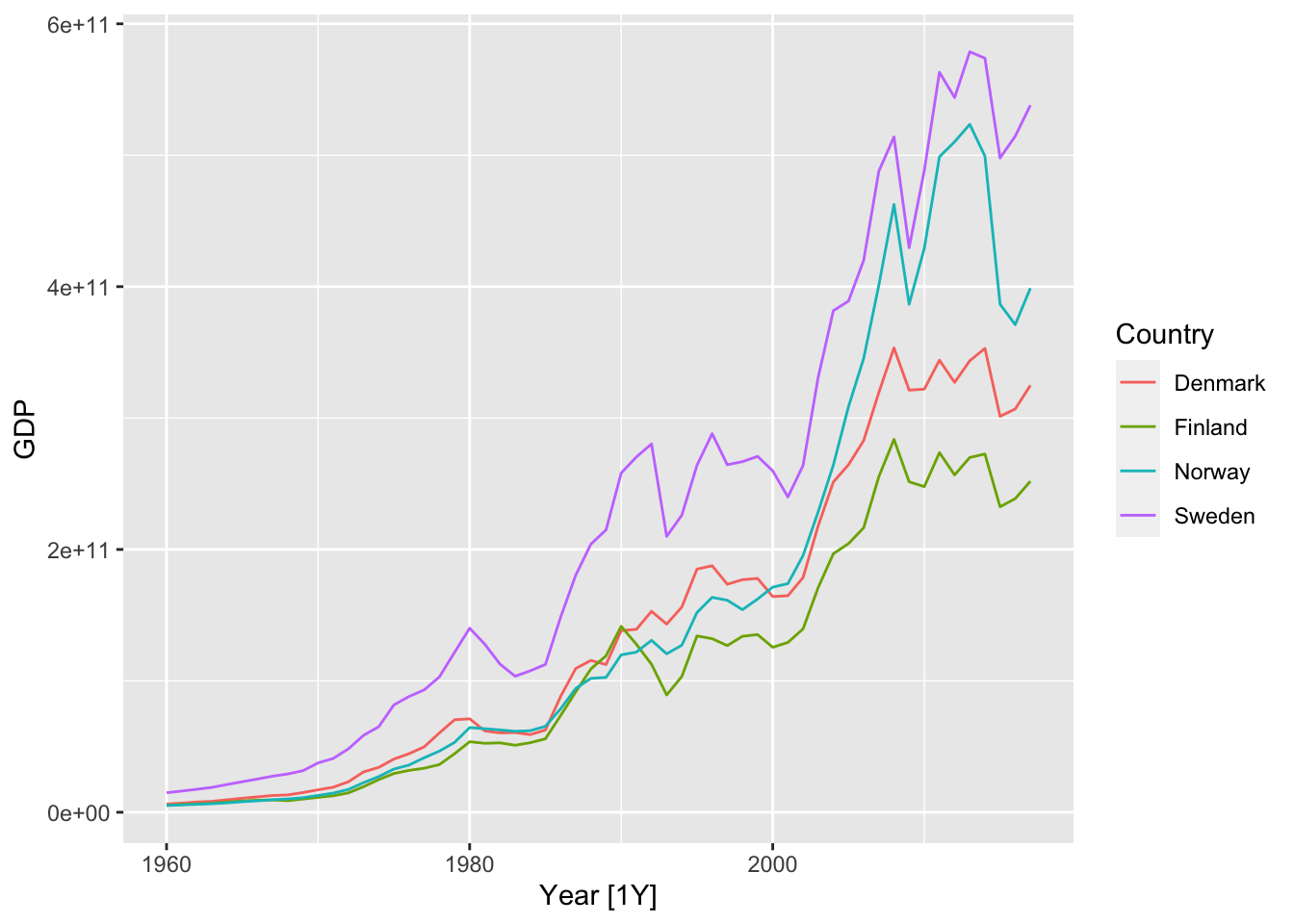

11.5 Example: GDP, several countries

library(tsibbledata) # Data sets package

nordic <- c("Sweden", "Denmark", "Norway", "Finland")

(global_economy %>% filter(Country %in% nordic) -> nordic_economy)## # A tsibble: 232 x 9 [1Y]

## # Key: Country [4]

## Country Code Year GDP Growth CPI Imports Exports Population

## <fct> <fct> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

## 1 Denmark DNK 1960 6248946880. NA 8.25 34.3 32.3 4579603

## 2 Denmark DNK 1961 6933842099. 6.38 8.53 32.3 30.0 4611687

## 3 Denmark DNK 1962 7812968114. 5.67 9.16 32.5 28.6 4647727

## 4 Denmark DNK 1963 8316692386. 0.637 9.72 30.8 30.4 4684483

## 5 Denmark DNK 1964 9506678763. 9.27 10.0 32.6 29.9 4722072

## 6 Denmark DNK 1965 10678897387. 4.56 10.6 31.5 29.3 4759012

## 7 Denmark DNK 1966 11721248101. 2.74 11.3 30.8 28.6 4797381

## 8 Denmark DNK 1967 12788479692. 3.42 12.2 30.0 27.3 4835354

## 9 Denmark DNK 1968 13196541952 3.97 13.2 29.7 27.7 4864883

## 10 Denmark DNK 1969 15009384585. 6.32 13.7 30.4 27.6 4891860

## # … with 222 more rows

fitnord <- nordic_economy %>%

model(

trend_model = TSLM(GDP ~ trend()),

trend_model_ln = TSLM(log(GDP) ~ trend()),

ets = ETS(GDP ~ trend("A")),

arima = ARIMA(GDP)

)

fitnord## # A mable: 4 x 5

## # Key: Country [4]

## Country trend_model trend_model_ln ets arima

## <fct> <model> <model> <model> <model>

## 1 Denmark <TSLM> <TSLM> <ETS(M,A,N)> <ARIMA(1,1,1)>

## 2 Finland <TSLM> <TSLM> <ETS(M,A,N)> <ARIMA(0,1,2)>

## 3 Norway <TSLM> <TSLM> <ETS(M,A,N)> <ARIMA(0,1,1)>

## 4 Sweden <TSLM> <TSLM> <ETS(M,A,N)> <ARIMA(0,1,2)>## # A tibble: 7 x 7

## Country .model term estimate std.error statistic p.value

## <fct> <chr> <chr> <dbl> <dbl> <dbl> <dbl>

## 1 Denmark arima ar1 -0.390 0.206 -1.89 0.0636

## 2 Denmark arima ma1 0.724 0.143 5.05 0.00000484

## 3 Finland arima ma1 0.406 0.120 3.39 0.00126

## 4 Finland arima ma2 -0.221 0.108 -2.05 0.0450

## 5 Norway arima ma1 0.410 0.155 2.65 0.0104

## 6 Sweden arima ma1 0.241 0.121 1.99 0.0510

## 7 Sweden arima ma2 -0.188 0.101 -1.87 0.0670Denmark: ARMA(1,1)

Finland: MA(2)

Norway: MA(1)

Sweden: MA(2)

nordic_economy %>%

model(arima_constrained = ARIMA(GDP ~ pdq(1,0,2))) %>% dplyr::select(arima_constrained) %>% coef()## # A tibble: 0 x 4

## # … with 4 variables: Country <fct>, .model <chr>, term <chr>, estimate <dbl>## # A tibble: 39 x 7

## Country .model term estimate std.error statistic p.value

## <fct> <chr> <chr> <dbl> <dbl> <dbl> <dbl>

## 1 Denmark trend_model (Intercept) -5.65e+10 8.75e+9 -6.46 2.70e- 8

## 2 Denmark trend_model trend() 6.63e+ 9 2.58e+8 25.7 1.14e-32

## 3 Denmark trend_model_ln (Intercept) 2.30e+ 1 8.55e-2 269. 7.68e-89

## 4 Denmark trend_model_ln trend() 7.12e- 2 2.52e-3 28.3 7.68e-35

## 5 Denmark ets alpha 1.00e+ 0 NA NA NA

## 6 Denmark ets beta 3.67e- 1 NA NA NA

## 7 Denmark ets l 4.92e+ 9 NA NA NA

## 8 Denmark ets b 1.24e+ 9 NA NA NA

## 9 Denmark arima ar1 -3.90e- 1 2.06e-1 -1.89 6.36e- 2

## 10 Denmark arima ma1 7.24e- 1 1.43e-1 5.05 4.84e- 6

## # … with 29 more rows## # A tibble: 16 x 21

## Country .model r_squared adj_r_squared sigma2 statistic p_value df

## <fct> <chr> <dbl> <dbl> <dbl> <dbl> <dbl> <int>

## 1 Denmark trend… 0.922 0.920 1.08e+21 660. 1.14e-32 2

## 2 Denmark trend… 0.935 0.933 1.03e- 1 800. 7.68e-35 2

## 3 Denmark ets NA NA 1.04e- 2 NA NA NA

## 4 Denmark arima NA NA 2.41e+20 NA NA NA

## 5 Finland trend… 0.914 0.912 7.34e+20 594. 1.70e-31 2

## 6 Finland trend… 0.930 0.929 1.14e- 1 745. 4.96e-34 2

## 7 Finland ets NA NA 1.32e- 2 NA NA NA

## 8 Finland arima NA NA 1.89e+20 NA NA NA

## 9 Norway trend… 0.824 0.821 4.60e+21 262. 8.54e-23 2

## 10 Norway trend… 0.959 0.958 8.37e- 2 1307. 1.64e-40 2

## 11 Norway ets NA NA 8.23e- 3 NA NA NA

## 12 Norway arima NA NA 6.78e+20 NA NA NA

## 13 Sweden trend… 0.919 0.918 2.65e+21 635. 3.07e-32 2

## 14 Sweden trend… 0.935 0.933 8.19e- 2 800. 7.57e-35 2

## 15 Sweden ets NA NA 1.16e- 2 NA NA NA

## 16 Sweden arima NA NA 8.84e+20 NA NA NA

## # … with 13 more variables: log_lik <dbl>, AIC <dbl>, AICc <dbl>, BIC <dbl>,

## # CV <dbl>, deviance <dbl>, df.residual <int>, rank <int>, MSE <dbl>,

## # AMSE <dbl>, MAE <dbl>, ar_roots <list>, ma_roots <list>## Series: GDP

## Model: ARIMA(1,1,1)

##

## Coefficients:

## ar1 ma1

## -0.3898 0.7240

## s.e. 0.2061 0.1434

##

## sigma^2 estimated as 2.407e+20: log likelihood=-1417.5

## AIC=2840.99 AICc=2841.45 BIC=2847.12## # A tibble: 16 x 11

## Country .model .type ME RMSE MAE MPE MAPE MASE RMSSE

## <fct> <chr> <chr> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

## 1 Denmark trend… Trai… -1.12e+10 6.89e10 3.67e10 -5.17 28.0 3.34 4.24

## 2 Denmark ets Trai… 4.50e+ 7 1.65e10 1.04e10 0.518 7.09 0.946 1.02

## 3 Denmark arima Trai… 4.40e+ 9 1.51e10 1.04e10 5.05 8.16 0.945 0.930

## 4 Denmark trend… Trai… -2.20e- 6 3.23e10 2.63e10 51.1 80.8 2.40 1.99

## 5 Finland trend… Trai… -8.61e+ 9 5.64e10 2.99e10 -5.53 28.6 2.95 3.82

## 6 Finland ets Trai… 1.36e+ 8 1.47e10 9.41e 9 0.795 8.36 0.927 0.996

## 7 Finland arima Trai… 3.54e+ 9 1.34e10 9.14e 9 5.03 8.92 0.900 0.906

## 8 Finland trend… Trai… 2.33e- 6 2.66e10 2.21e10 46.1 80.5 2.18 1.80

## 9 Norway trend… Trai… -1.31e+10 8.20e10 3.51e10 -4.24 24.9 2.24 3.01

## 10 Norway ets Trai… -5.29e+ 8 2.75e10 1.37e10 0.755 6.94 0.870 1.01

## 11 Norway arima Trai… 4.90e+ 9 2.56e10 1.40e10 5.04 8.11 0.890 0.938

## 12 Norway trend… Trai… -1.10e- 5 6.67e10 5.48e10 130. 181. 3.49 2.45

## 13 Sweden trend… Trai… -1.18e+10 8.23e10 4.79e10 -3.96 23.7 2.25 2.68

## 14 Sweden ets Trai… 1.19e+ 9 3.02e10 1.86e10 0.745 7.64 0.875 0.984

## 15 Sweden arima Trai… 8.48e+ 9 2.89e10 2.01e10 5.18 9.37 0.942 0.944

## 16 Sweden trend… Trai… 3.22e- 6 5.05e10 3.90e10 29.4 53.3 1.83 1.65

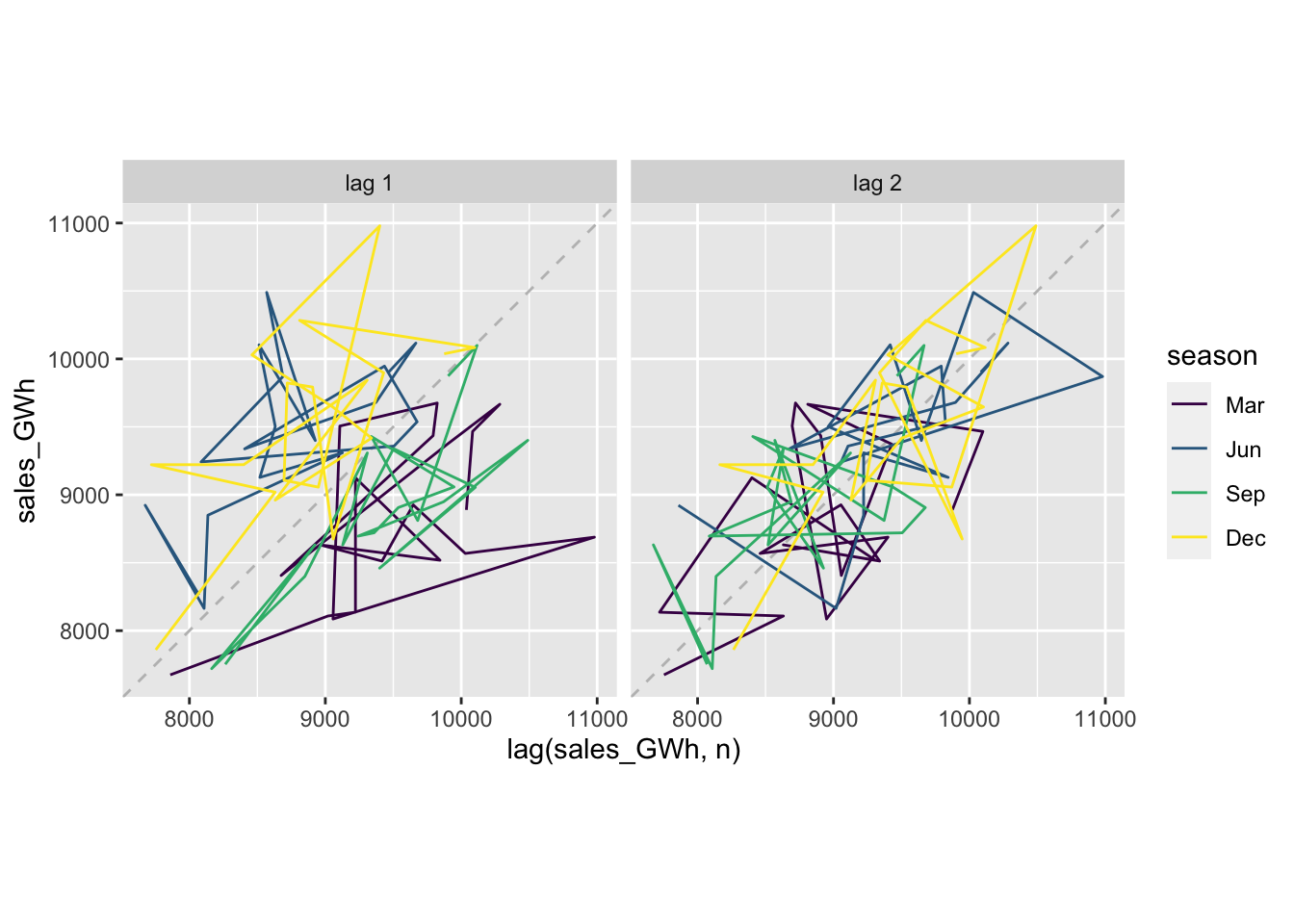

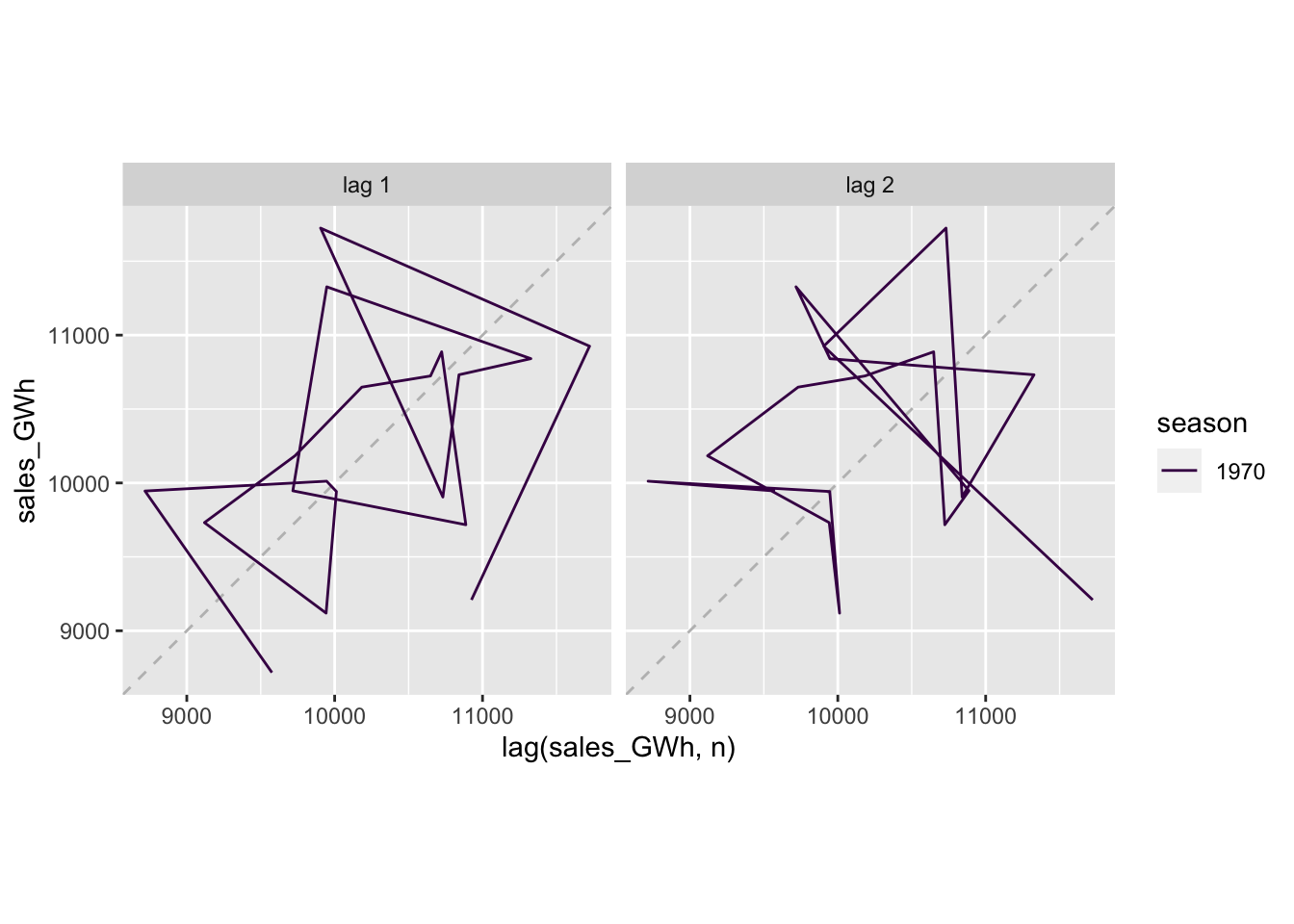

## # … with 1 more variable: ACF1 <dbl>11.5.1 Plot lagged values

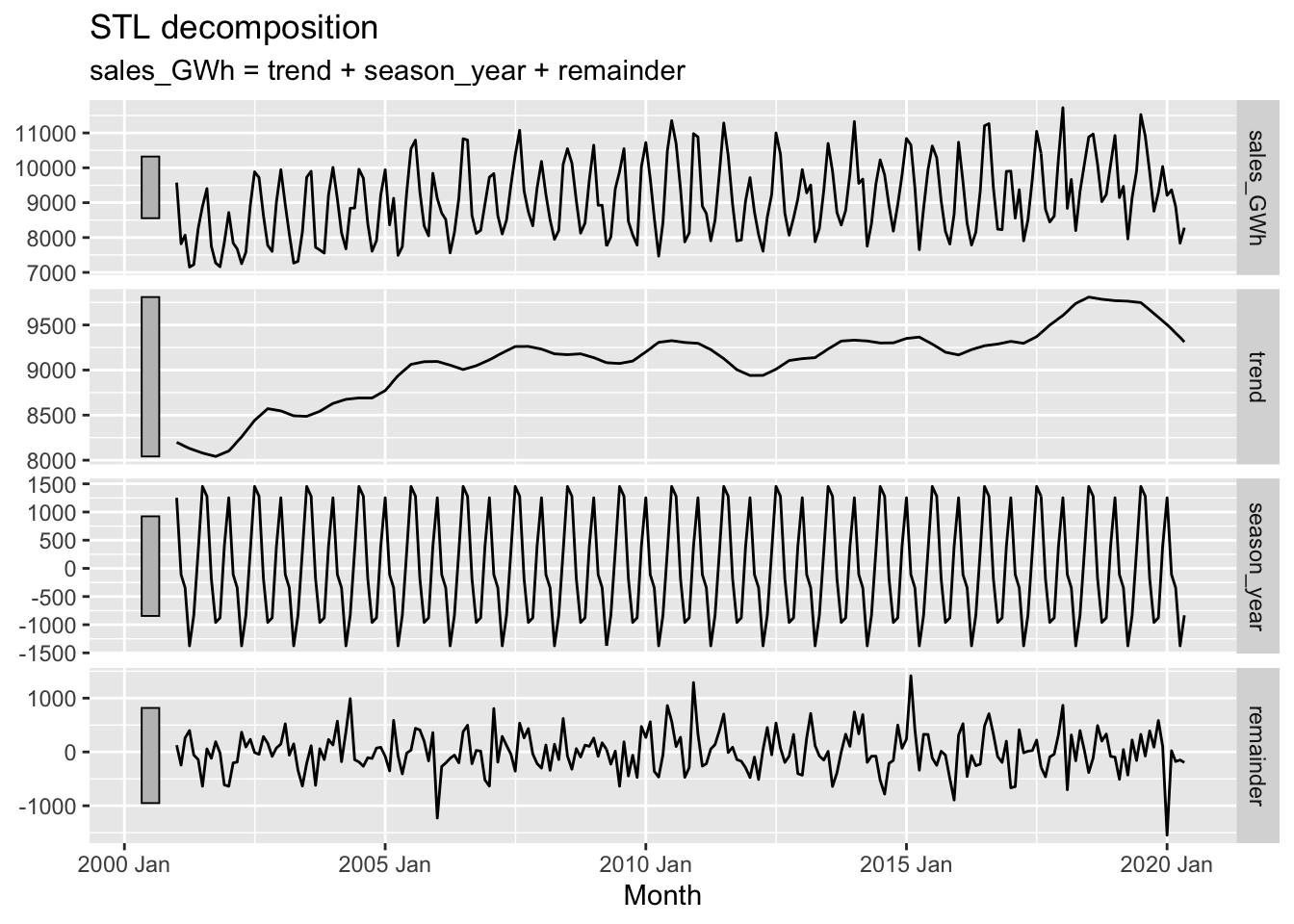

vaelsales_tbl_ts %>%

model(STL(sales_GWh ~ trend(window=21) + season(window='periodic'), robust = TRUE)) %>%

components() %>%

autoplot()

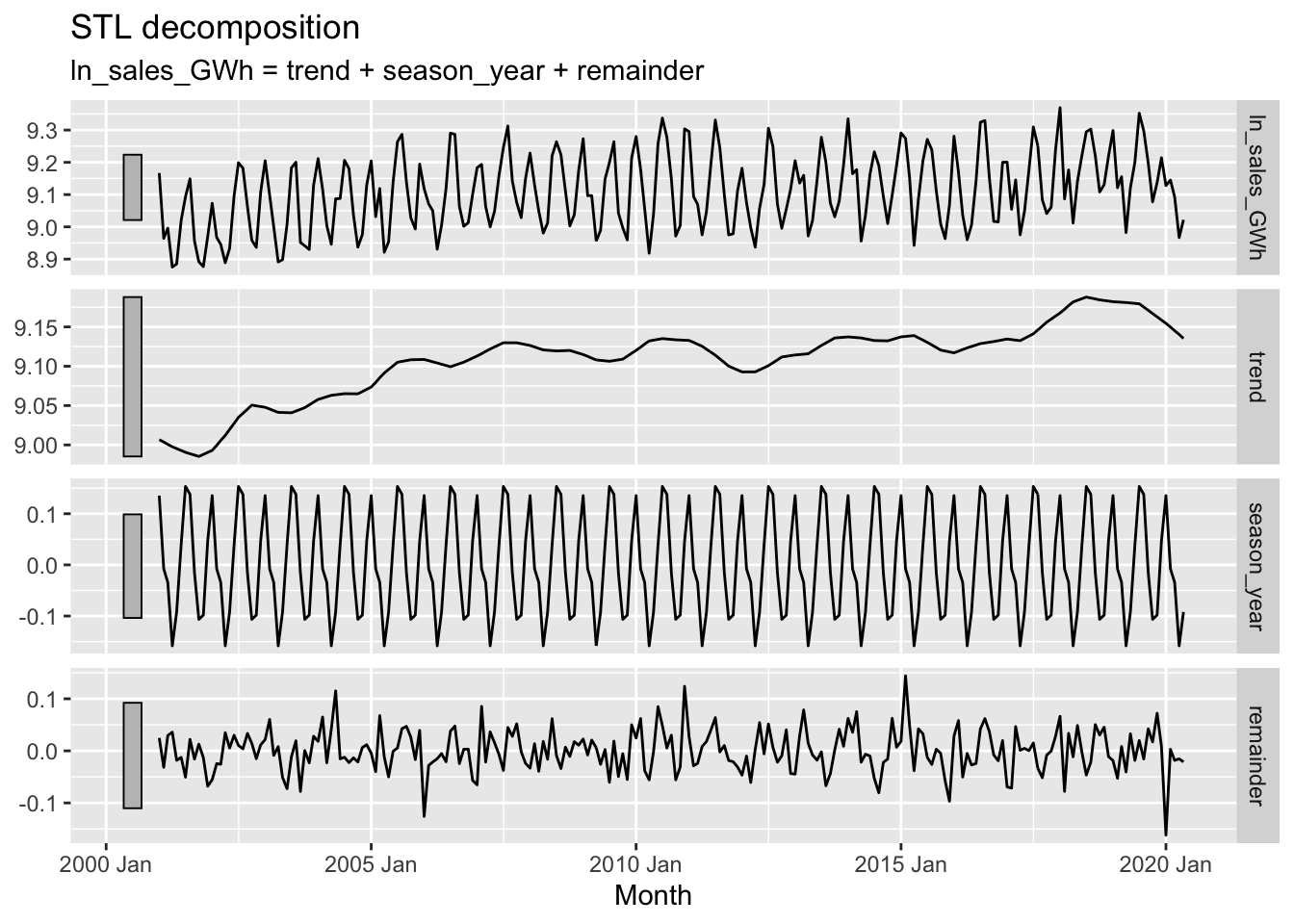

vaelsales_tbl_ts %>%

mutate(ln_sales_GWh = log(sales_GWh)) %>%

model(STL(ln_sales_GWh ~ trend(window=21) + season(window='periodic'),

robust = TRUE)) %>%

components() %>%

autoplot()

## # A tibble: 1 x 9

## trend_strength seasonal_streng… seasonal_peak_y… seasonal_trough… spikiness

## <dbl> <dbl> <dbl> <dbl> <dbl>

## 1 0.597 0.863 7 4 862916.

## # … with 4 more variables: linearity <dbl>, curvature <dbl>, stl_e_acf1 <dbl>,

## # stl_e_acf10 <dbl>## # A tibble: 1 x 48

## trend_strength seasonal_streng… seasonal_peak_y… seasonal_trough… spikiness

## <dbl> <dbl> <dbl> <dbl> <dbl>

## 1 0.597 0.863 7 4 862916.

## # … with 43 more variables: linearity <dbl>, curvature <dbl>, stl_e_acf1 <dbl>,

## # stl_e_acf10 <dbl>, acf1 <dbl>, acf10 <dbl>, diff1_acf1 <dbl>,

## # diff1_acf10 <dbl>, diff2_acf1 <dbl>, diff2_acf10 <dbl>, season_acf1 <dbl>,

## # pacf5 <dbl>, diff1_pacf5 <dbl>, diff2_pacf5 <dbl>, season_pacf <dbl>,

## # zero_run_mean <dbl>, nonzero_squared_cv <dbl>, zero_start_prop <dbl>,

## # zero_end_prop <dbl>, lambda_guerrero <dbl>, kpss_stat <dbl>,

## # kpss_pvalue <dbl>, pp_stat <dbl>, pp_pvalue <dbl>, ndiffs <int>,

## # nsdiffs <int>, bp_stat <dbl>, bp_pvalue <dbl>, lb_stat <dbl>,

## # lb_pvalue <dbl>, var_tiled_var <dbl>, var_tiled_mean <dbl>,

## # shift_level_max <dbl>, shift_level_index <dbl>, shift_var_max <dbl>,

## # shift_var_index <dbl>, shift_kl_max <dbl>, shift_kl_index <dbl>,

## # spectral_entropy <dbl>, n_crossing_points <int>, longest_flat_spot <int>,

## # coef_hurst <dbl>, stat_arch_lm <dbl>